1 Credit Risk I. 2 Session Objectives Discuss Importance of lending to institutions Discuss...

21

1 Credit Risk I Credit Risk I

-

Upload

helena-arnold -

Category

Documents

-

view

217 -

download

1

Transcript of 1 Credit Risk I. 2 Session Objectives Discuss Importance of lending to institutions Discuss...

1

Credit Risk ICredit Risk I

2

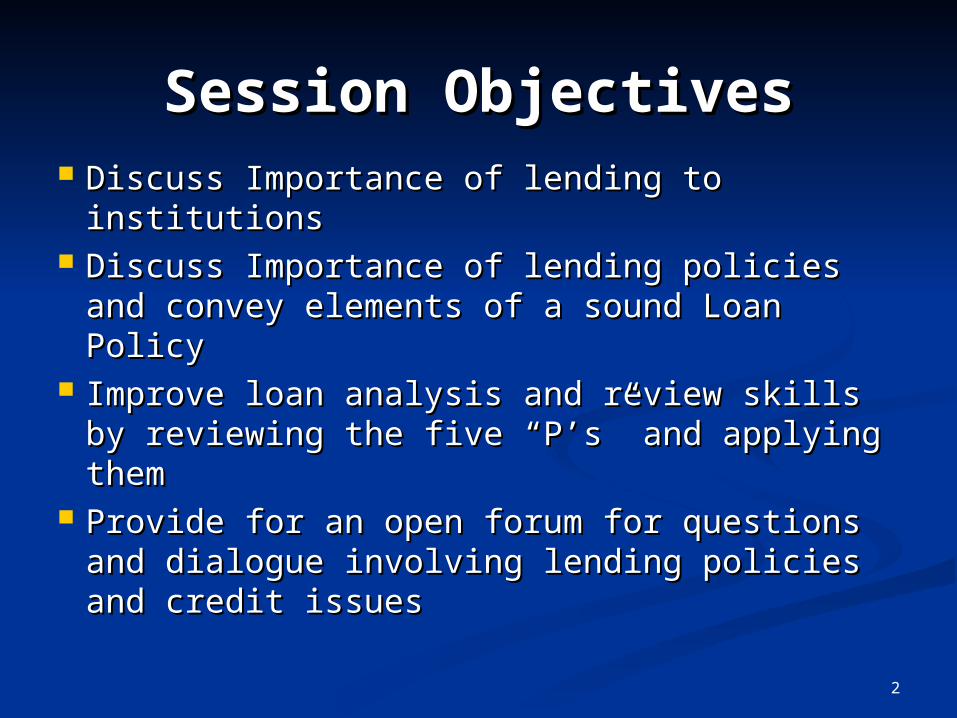

Session ObjectivesSession Objectives Discuss Importance of lending to Discuss Importance of lending to

institutionsinstitutions Discuss Importance of lending policies and Discuss Importance of lending policies and

convey elements of a sound Loan Policyconvey elements of a sound Loan Policy Improve loan analysis and review skills by Improve loan analysis and review skills by

reviewing the five “P’s” and applying themreviewing the five “P’s” and applying them Provide for an open forum for questions Provide for an open forum for questions

and dialogue involving lending policies and and dialogue involving lending policies and credit issuescredit issues

3

Why Review Lending Why Review Lending Activities?Activities?

4

Why are Loans Why are Loans Important?Important?

Major Portion of the Asset StructureMajor Portion of the Asset Structure Have largest Impact on EarningsHave largest Impact on Earnings Greatest Credit Risk and Potential Greatest Credit Risk and Potential

LossLoss Loan Losses/Fraud Cause Loan Losses/Fraud Cause MOSTMOST

Bank FailuresBank Failures

5

Director Role in Credit Director Role in Credit Approval and Approval and MonitoringMonitoring

Outside directors are not expected Outside directors are not expected to be lending expertsto be lending experts

Directors are an independent voice Directors are an independent voice in the management of the bankin the management of the bank

Hire and maintain qualified senior Hire and maintain qualified senior management management

No surprises for directors at an No surprises for directors at an examination examination

Lending PoliciesLending Policies

7

Why are Loan Policies Why are Loan Policies Important?Important?

Establish authority, rules, and Establish authority, rules, and framework to operate and administer framework to operate and administer the loan portfolio effectively,the loan portfolio effectively,

Convey the Board’s tolerance for risk, Convey the Board’s tolerance for risk,

andand Provide for measurable goals and Provide for measurable goals and

standards.standards.

8

Loan PolicyLoan Policy Statement of business and lending Statement of business and lending

philosophyphilosophy Cornerstone of sound lending and loan Cornerstone of sound lending and loan

administrationadministration Establishes basic standards to:Establishes basic standards to:

maintain sound credit underwriting standardsmaintain sound credit underwriting standards control and manage riskcontrol and manage risk evaluate new business opportunitiesevaluate new business opportunities identify, administer, and collect problem loansidentify, administer, and collect problem loans

9

Common Loan Policy Common Loan Policy ProvisionsProvisions

General fields or type of lendingGeneral fields or type of lending Lending authorityLending authority Board responsibility to review, ratify or Board responsibility to review, ratify or

approve loansapprove loans Guidelines for unsecured loansGuidelines for unsecured loans Guidelines for rates and terms on loansGuidelines for rates and terms on loans Loan-to-value ratios for various types of loansLoan-to-value ratios for various types of loans

10

Common Loan Policy Common Loan Policy ProvisionsProvisions

Documentation requirements by loan typeDocumentation requirements by loan type Guidelines for valuations and appraisalsGuidelines for valuations and appraisals Requirements for ongoing documentation Requirements for ongoing documentation

review and update of credit filesreview and update of credit files Collection procedures and responsibilitiesCollection procedures and responsibilities Portfolio mix and diversificationPortfolio mix and diversification

11

Common Loan Policy Common Loan Policy ProvisionsProvisions

Overdraft limits and Overdraft limits and approval authorityapproval authority

Trade areaTrade area ConcentrationsConcentrations Loan review and gradingLoan review and grading

Loan Policy Loan Policy Questions?Questions?

Loan AnalysisLoan Analysis

14

5 ‘Ps’ OF CREDIT5 ‘Ps’ OF CREDIT

PeoplePeople PurposePurpose PaymentPayment ProtectionProtection ProspectsProspects

15

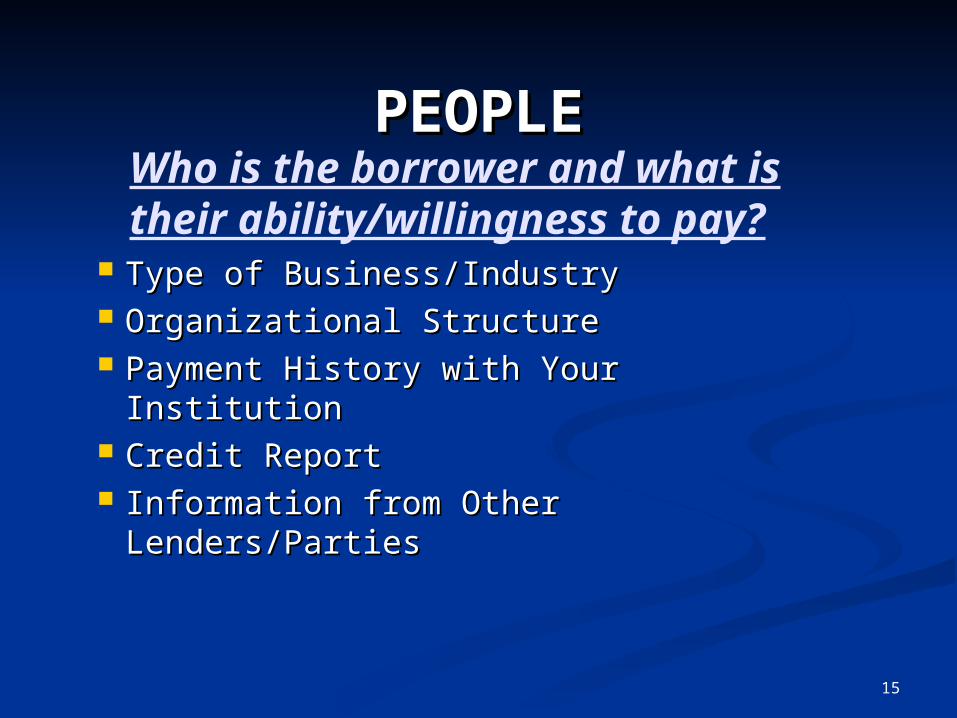

PEOPLEPEOPLE

Type of Business/IndustryType of Business/Industry Organizational StructureOrganizational Structure Payment History with Your InstitutionPayment History with Your Institution Credit ReportCredit Report Information from Other Information from Other

Lenders/PartiesLenders/Parties

Who is the borrower and what is their ability/willingness to pay?

16

PURPOSEPURPOSE

Purchase of Specific AssetsPurchase of Specific Assets General Working Capital General Working Capital Asset-Based Lending Asset-Based Lending Refinance Other DebtRefinance Other Debt Consistency with PeopleConsistency with People

What will the money be used for?

17

PAYMENTPAYMENT

Terms of DebtTerms of Debt Source of Repayment Source of Repayment Income to Debt Service RequirementsIncome to Debt Service Requirements Living/Other ExpensesLiving/Other Expenses Other Sources of IncomeOther Sources of Income Consistency with People and PurposeConsistency with People and Purpose

What are the terms and borrower’s ability to pay?

18

PROTECTIONPROTECTION

Lien Perfection Lien Perfection Lien PositionLien Position Market/Liquidation ValueMarket/Liquidation Value MarketabilityMarketability Access/Control Access/Control

What is the collateral and what would it be worth?

19

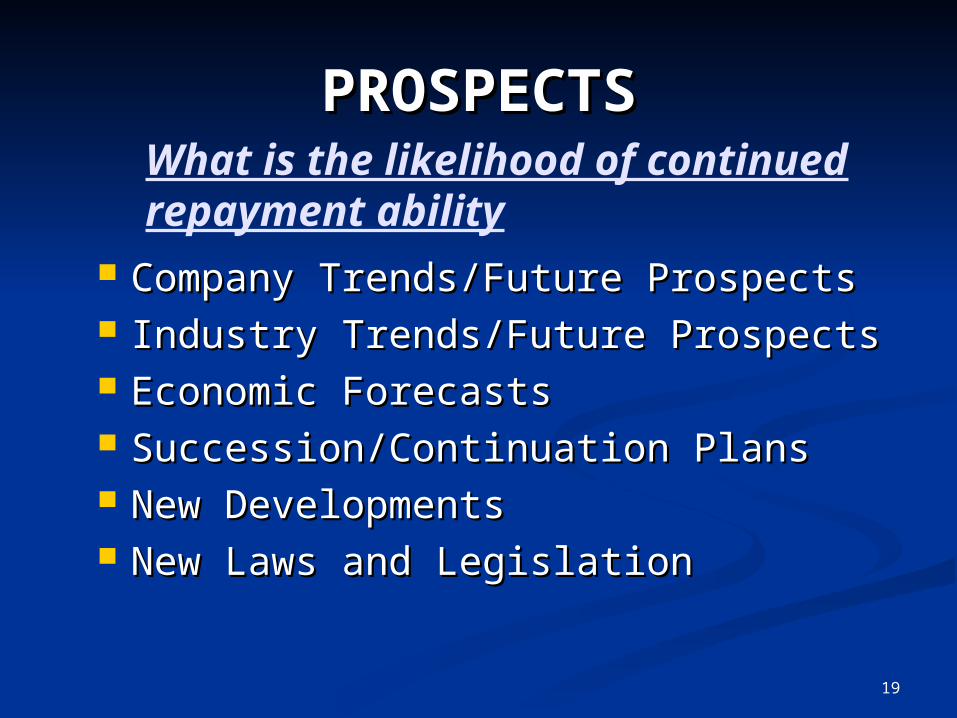

PROSPECTSPROSPECTS

Company Trends/Future ProspectsCompany Trends/Future Prospects Industry Trends/Future Prospects Industry Trends/Future Prospects Economic ForecastsEconomic Forecasts Succession/Continuation PlansSuccession/Continuation Plans New Developments New Developments New Laws and Legislation New Laws and Legislation

What is the likelihood of continued repayment ability

Questions?Questions?

ConclusionConclusion