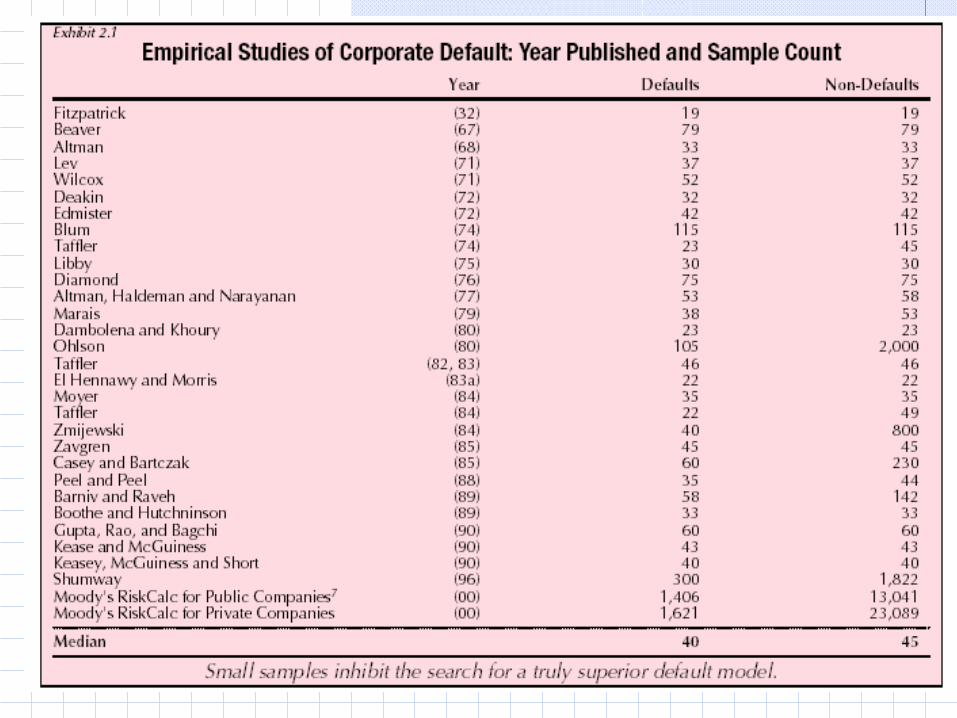

1 Credit Risk Analysis. 2 What is a bond? A long-term debt instrument in which a borrower agrees to...

40

1 Credit Risk Analysis

-

Upload

augusta-newton -

Category

Documents

-

view

213 -

download

0

Transcript of 1 Credit Risk Analysis. 2 What is a bond? A long-term debt instrument in which a borrower agrees to...

1

Credit Risk Analysis

2

What is a bond?

A long-term debt instrument in which a borrower agrees to make payments of principal and interest, on specific dates, to the holders of the bond.

Creditors receive interest and principal payments they have been promised

3

What determines interest rates of corporate bonds?

ki = k* + IP + MRP +DRP + LP

ki = required return on a debt securityk* = real risk-free rate of interestIP = inflation premiumMRP= maturity risk premium (also called

interest rate risk premium) DRP= default risk premiumLP = liquidity premium

4

Default risk

If an issuer defaults, investors receive less than the promised return. Therefore, the expected return on corporate bonds might be less than the promised return.

Default risk is influenced by the issuer’s financial strength and the terms of the bond contract.

5

Default Risk

A bond also has legal rights attached to it: if the borrower doesn’t make the required

payments, bondholders can force bankruptcy proceedings

in the event of bankruptcy, bond holders get paid before equity holders

6

Bankruptcy

Two main chapters of the Federal Bankruptcy Act: Chapter 11, Reorganization Chapter 7, Liquidation

Chapter 11 bankruptcy is a financial reorganization in which the company continues to operate and works with creditors to formulate repayment plans.Chapter 7 bankruptcy is a complete liquidation in which the firm ceases operations and sells all assets.Typically, a company wants Chapter 11, while creditors may prefer Chapter 7.

7

Credit rating

Rely on qualitative and quantitative analyses

Standard & Poor’s (AAA to D) Intermediate “+/-” scores

Moody’s (Aaa to C) Intermediate “1,2,3” scores

Fitch (AAA to D)

8

Bond Quality RatingsRating Grades Standard & Poor’s Moody’s

Highest grade AAA AaaHigh grade AA AaUpper medium A ALower medium BBB BaaMarginally speculative BB BaHighly speculative B B, CaaDefault D Ca, C

Rating Criteria

9

Now more competition!

Of the more than 130 credit-rating agencies, the SEC has granted only five the designation NRSROs: Moody's, S&P, A.M. Best, Dominion Bond Rating Service, and Fitch Ratings. President Bush Signs Rating Agency Reform Act on October 2006A credit-rating company with three years of experience that meets certain standards would be allowed to register with the SEC as a “nationally recognized statistical ratings organization (NRSRO)."

10

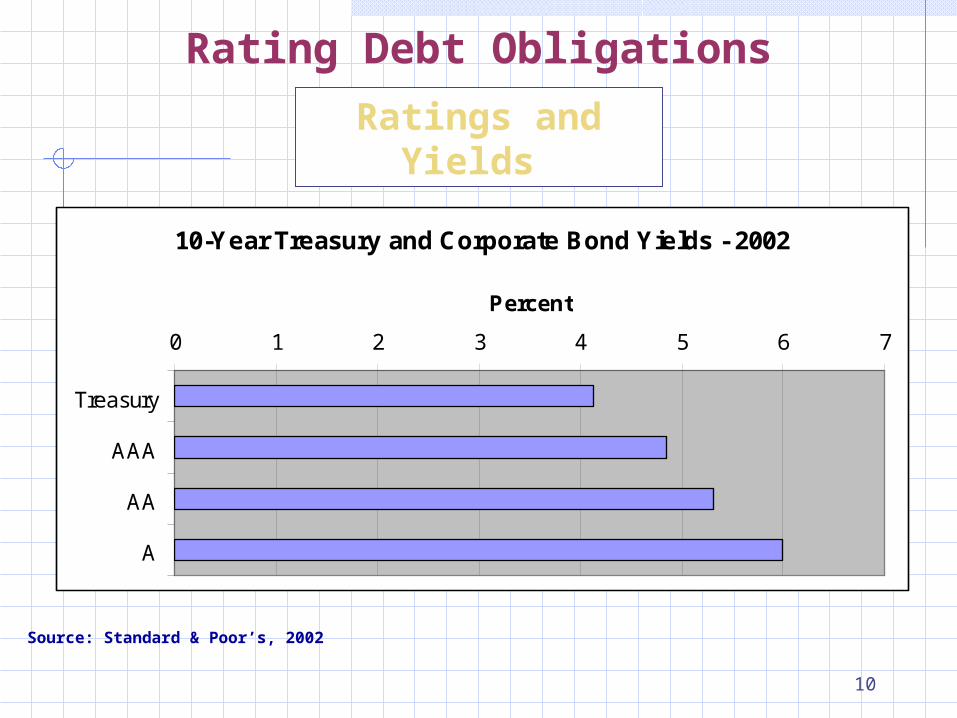

Ratings and Yields

Rating Debt Obligations

Source: Standard & Poor’s, 2002

10-Year Treasury and Corporate Bond Yields - 2002

0 1 2 3 4 5 6 7

Treasury

AAA

AA

A

Percent

11

Factors affecting default risk and bond ratings

Financial performance Debt ratio Current ratio Other ratios Be aware of accounting distortions

Bond contract provisions Secured vs. Unsecured debt Senior vs. subordinated debt Guarantee Debt maturity

12

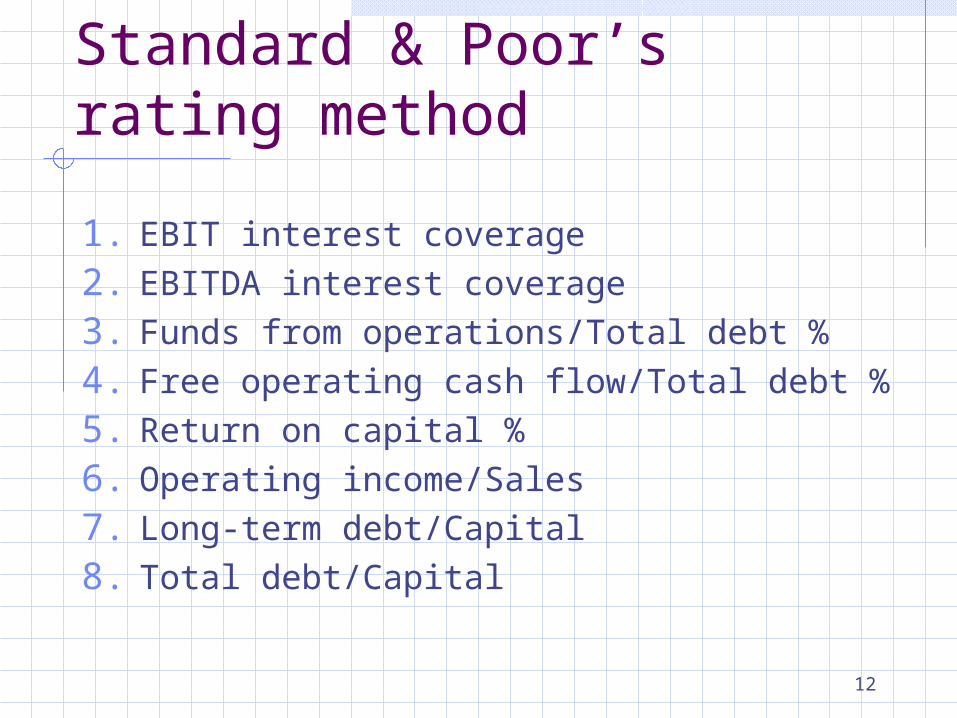

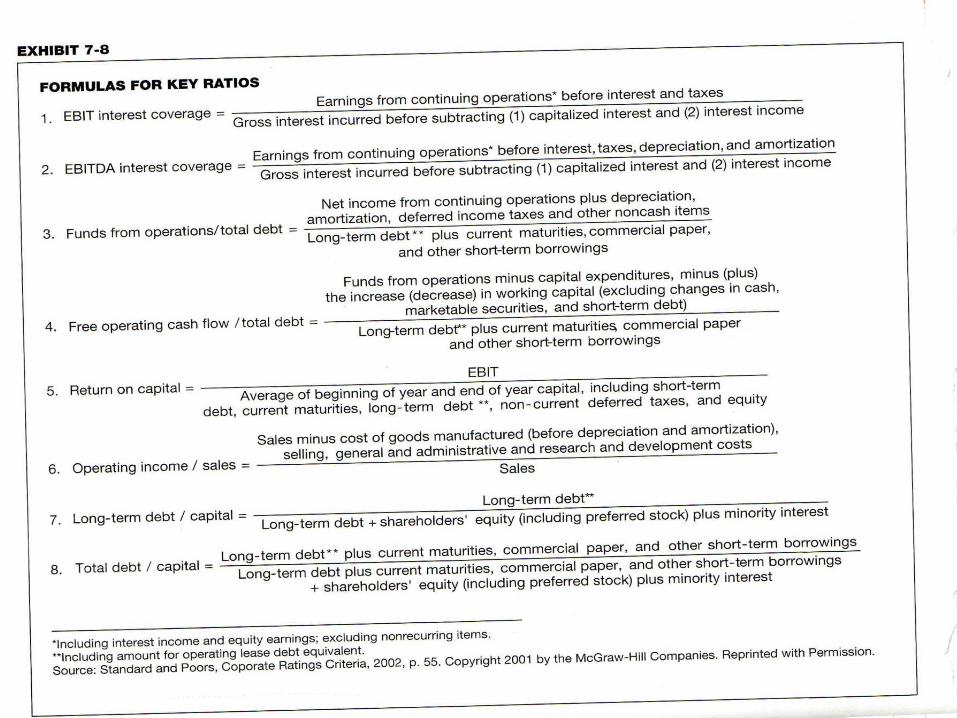

Standard & Poor’s rating method

1. EBIT interest coverage

2. EBITDA interest coverage

3. Funds from operations/Total debt %

4. Free operating cash flow/Total debt %

5. Return on capital %

6. Operating income/Sales

7. Long-term debt/Capital

8. Total debt/Capital

13

14

15

17

Financial distress

Financial distress can also be directly predicted.

18

Prediction of bankruptcy

Bankruptcy prediction models are used in the same way as the bond ratings prediction models.

Dependent variable is a dummy variable indicating whether or not the firm went bankrupt.

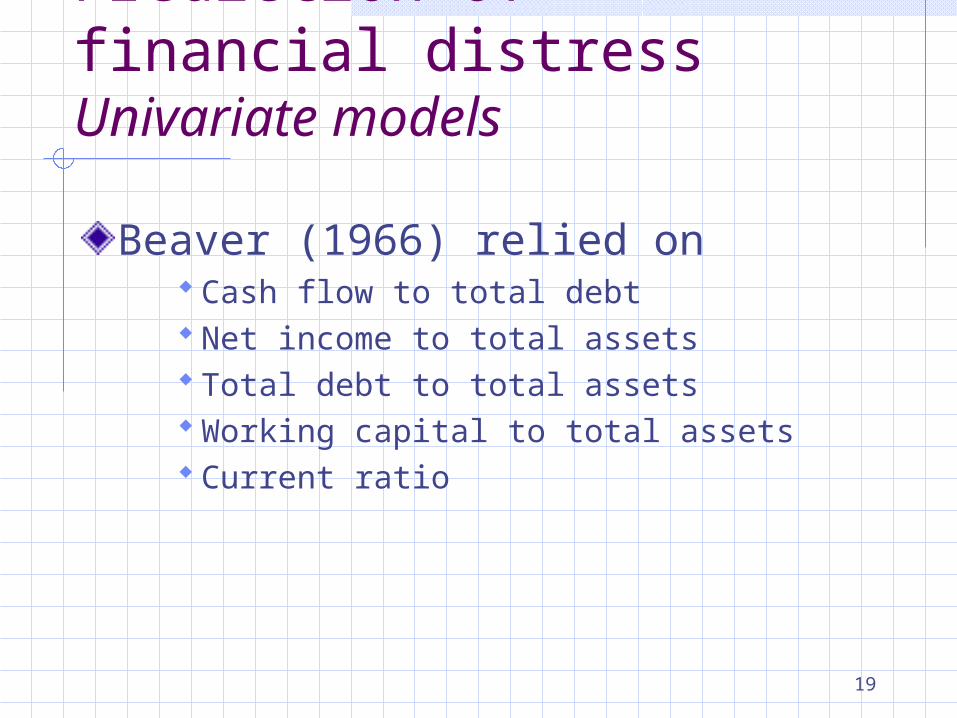

Beaver (1966) investigated the use of financial ratios in the bankruptcy prediction.

The results clearly indicate that values of the financial ratios differ between failed and non-failed firms.

19

Prediction of financial distressUnivariate models

Beaver (1966) relied on Cash flow to total debt Net income to total assets Total debt to total assets Working capital to total assets Current ratio

20

Example: Cash flow / total debt

-0.3

-0.2

-0.10

0.1

0.2

0.30.4

0.5

0.6

5 4 3 2 1

Years before failure

Nonfailedfirms

Failed firms

21

Example (cont.): Net income / total assets

-0.25

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

5 4 3 2 1

Years before failure

Nonfailedfirms

Failed firms

22

Example (cont.): Total debt / total assets

00.10.20.30.40.50.60.70.80.9

5 4 3 2 1

Years before failure

Failed firms

Nonfailedfirms

23

Example (cont.): Working capital / total assets

00.050.1

0.150.2

0.250.3

0.350.4

0.45

5 4 3 2 1

Years before failure

Nonfailedfirms

Failed firms

24

Example (cont.): Current ratio

0

0.5

1

1.5

2

2.5

3

3.5

4

5 4 3 2 1

Years before failure

Nonfailedfirms

failed firms

25

X1 = Working capital/Total assetsX2 = Retained earnings/Total assetsX3 = Earnings before interest and taxes/Total assetsX4 = Shareholders’ market value/Total liabilitiesX5 = Sales/Total assets

Z<1.81 implies a high probability of bankruptcyZ>2.99 implies a low probability of bankruptcy1.81<Z<2.99 implies an ambiguous area

Predicting Financial Distress

Altman Z-Score

1 2 3 4 5Z 1.2X 1.4X 3.3X 0.6X 1X

26

Prediction of financial distressMultivariate models

Altman Z-score (Current assets – current liabilities)/total assets Retained earnings/Total assets EBIT/Total assets Preferred and common stock market value/Book value of

liabilities Sales/Total assets

Nokia = 9.88Motorola = 1.71 (below the 2.99 nonbankrupt benchmark)

30

Motorola, Note 8Off-balance-sheet financing

“At December 31, 2001, future minimum lease obligations, net of minimum sublease rentals, for the next five years and beyond are as follows: 2002—$150 million; 2003—$117 million; 2004—$97 million; 2005—$76 million; 2006—$63 million; beyond—$90 million.”

•The present value of these payments, at 7%, is $484 million•Inclusion of these items increases debt by 5%

33

Nokia debt note detailOperating lease payments

Payments due Amount PV factor PV2002 254 € 0.9346 237 €2003 213 € 0.8734 186 €2004 178 € 0.8163 145 €2005 165 € 0.7629 126 €2006 162 € 0.7130 116 €

Beyond 274 € 0.6663 183 €993 €Total estimated liability

34

Elements of Free Operating Cash Flow

2001 Nokia (EURm) Motorola ($m)

EBITDA 5,735 (4,039)

Non-cash items 248 (2,273)

Fund from operations 5,983 (6,312)

Capital expenditures (1,041) (1,321)

Working capital change 978 1,527

Free operating cash flow 5,920 (6,106)

35

Debt Analysis Ratios

2001 2000 2001 2000EBIT interest coverage 37.11 31.91 (10.22) 2.97 EBITDA interest coverage 49.44 37.06 (6.26) 8.68 Funds from operations/Total debt 4.63 5.04 (0.58) 0.29 Free operating cash flow/Total debt 4.59 2.97 (0.56) (0.40) Return on end of year capital 0.31 0.50 (0.27) 0.04 Operating income/Sales 0.160 0.195 0.018 0.116 Long-term debt/Capital 0.085 0.066 0.421 0.238 Total debt/Capital 0.094 0.115 0.443 0.427

Nokia Motorola

36

38

More Recent Advances in Distress Prediction

RiskCalc

Market (Merton) Model

39

40

RiskCalc™

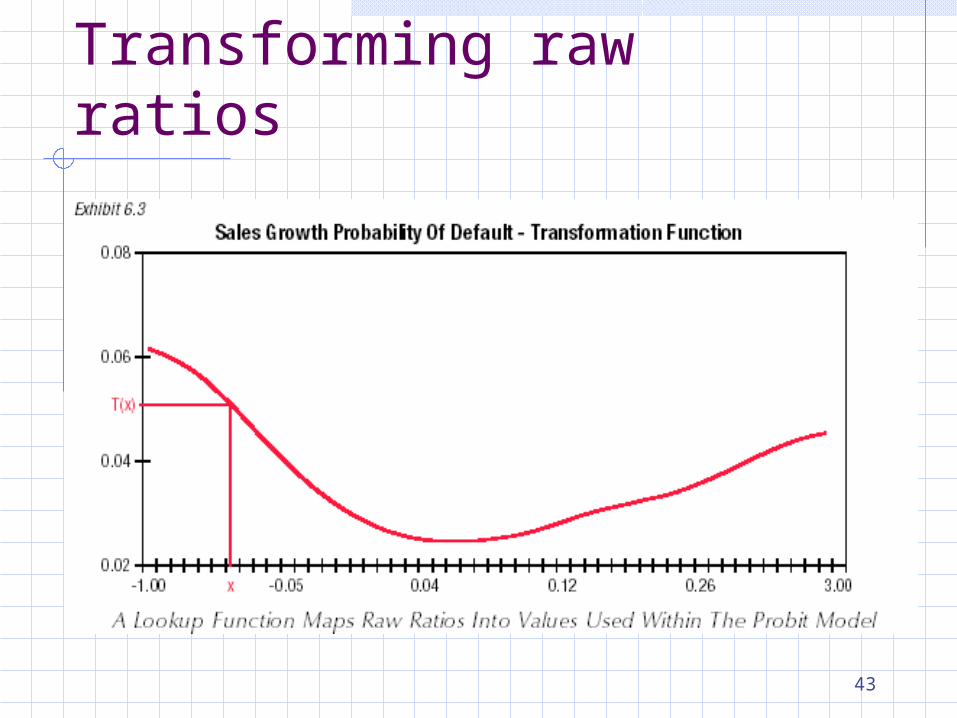

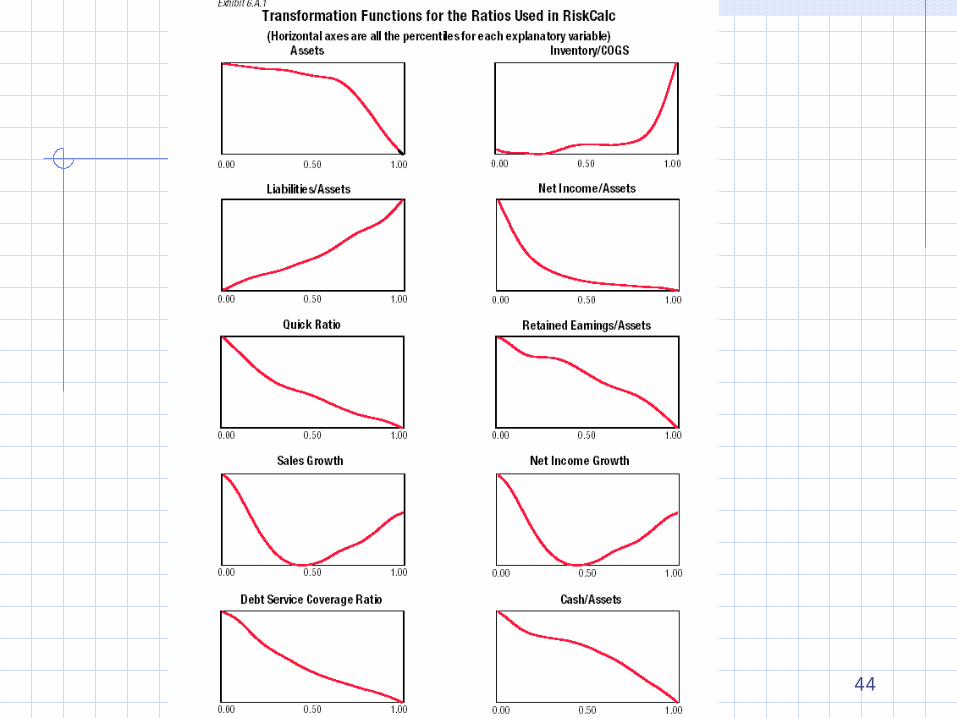

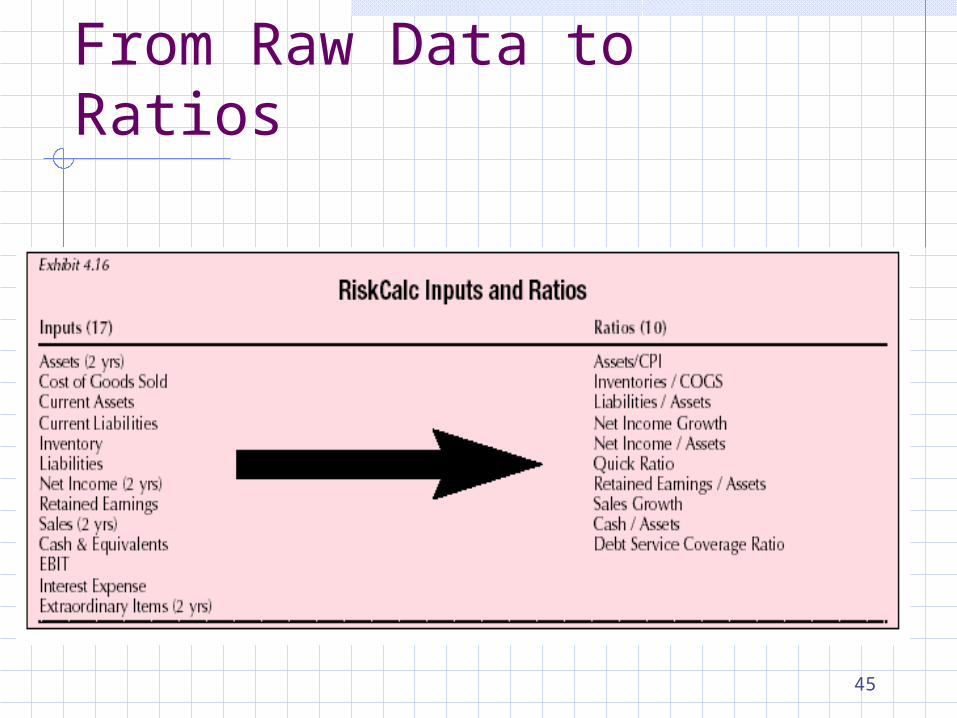

“The model's key advantage derives from Moody's unique and proprietary middle market private firm financial statement and default database (Credit Research Database), which comprises 28,104 companies and 1,604 defaults. Our main insights and conclusions are:…Comprehensive testing and validation suggest that RiskCalc's predictive power is superior to that of other publicly available benchmark models and is robust across non-financial industry sectors, and over time. RiskCalc™ was developed to achieve maximum predictive power with the smallest number of inputs. It requires just 10 financial ratios & indicators computed from 17 basic financial inputs. RiskCalc's predictive power derives, in part, from its meticulous transformation of input financial ratios….” Source: RiskCalc™ For Private Companies: Moody's Default Model , may 2000

41

43

Transforming raw ratios

44

45

From Raw Data to Ratios

46

Contribution of Factors

49

Market Model (Not required)

Banks can use the theory of option pricing to assess the credit risk of a corporate borrower

The probability of default is positively related to: the volatility of the firm’s stock the firm’s leverage

A model developed by KMV corporation is being widely used by banks for this purpose

50