1 Connecting the Dots Edward Randolph Director, Energy Division California Public Utilities...

19

1 Connecting the Dots Edward Randolph Director, Energy Division California Public Utilities Commission Date (example: April 26, 2012)

-

Upload

imogen-blake -

Category

Documents

-

view

213 -

download

0

Transcript of 1 Connecting the Dots Edward Randolph Director, Energy Division California Public Utilities...

1

Connecting the Dots

Edward RandolphDirector, Energy Division

California Public Utilities Commission

Date (example: April 26, 2012)

Connecting the Dots •Many different ways to connect the dots,

•Best to start at the point in time and explain how things built from there.

•So I will start at the year 1 AeC.

Move Back into Long Term Planning

• As part of unwinding the energy crisis the Legislature and the CPUC created a process for long term planning by the IOUs.

• This eventually became know as the Long Term Procurement Planning (LTPP).

• There have been changes overtime and will continue to change as we learn more and the needs of the gird change.

• Also eventually added Resource Adequacy to the mix

3

LTTP Today

• Open issues from the 2012 LTTP– SCE Track I Application– SCE Living pilot– SDG&E Carlsbad Application– SDG&E All source RFO/Application

4

LTPP Today

• 2014 LTPP

– Phase 1a -- Capacity and flexibility needs

– Phase 1b -- 2015 procurement Authorization

5

Resource Adequacy

• 2015 Compliance Year Proceeding to open this fall:– Should we unbundle system and flexible capacity?– Should/can we count curtailable renewable resources and if so,

how? – Should we change the allocation of flexible resource

requirements?

6

Then We Added Renewables

• Today Goal is 33% by 2020 with AB 327 setting that as a floor.– Current RPS Proceeding

• 2015 Procurement plans (based on compliance need not system need)

• RPS calculator (feeds back to needs and Transmission Planning in LTPP)

• Procurement Streamlining• RAM review (smaller non-DG procurement)• ReMAT (small DG)

7

RPS (well maybe)

• “Integration Adder” – or Total Resource Valuation. – Legislation requires valuation of integration

costs into Least Cost Best Fit.– Process was already underway – will entail

inputs from LTPP, RA, and RPS. – Could ultimately be used to value DR and EE.

8

Then Came Customer Generation

• California Solar Initiative & SGIP– Relates back to LTPP in RA by impact future

demand forecasts. – Relates to RPS IF customer sells RECs – but

otherwise doesn’t impact RPS.

• NEM 2.0

9

Then Came GHG(well it had been there for a while but we decide to reduce our production)

• Direct impact– Proceedings on cost allocation issues.

10

Then Came GHG(and a bunch of separate Programs to meet the goals. )

• Electric Vehicles • Utility role in infrastructure

• Vehicle to grid integration

• Demand Response– 2015 reauthorization

– Foundation policy issue to promote big increase

– Guidance for future portfolios

11

Then Came GHG(and a bunch of separate Programs to meet the goals.

• Energy Efficiency– Decision on 2015 funding mailed this week.– Next phases look at rolling portfolio and

program redesign issues.

12

Then Came the Future

• Distributed Resources Plan Proceeding– Establishes policies, procedures and rules for development of

Distribution Resources Plans• Phase 1: Aug – January, provide guidance for utility

Distribution Resources Plans (DRPs) required by AB 327 (Sec. 769)

• Phase 2: Commencing July 1, 2015, evaluate DRP filings and future investments in electric distribution infrastructure.

13

Then Came the Future

• Interconnection Reform

• Energy Storage

14

AND then There are Others….

• CEC IEPR

• CAISO TPP

• Joint Agency Steering Committee (JASC) (Padilla Letter)

15

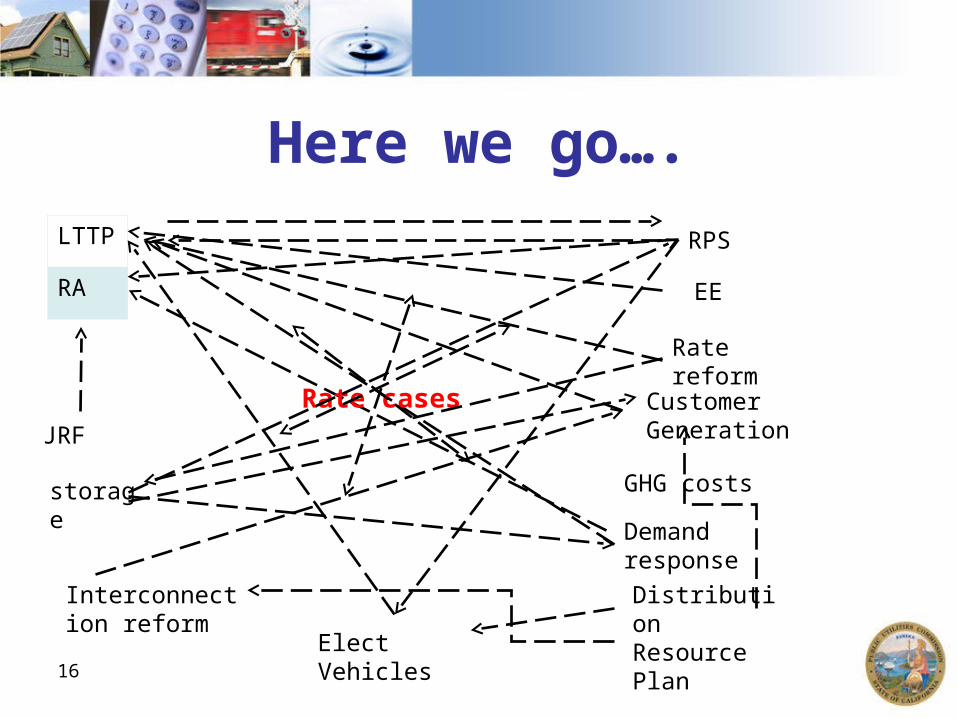

Here we go….LTTP

RA

16

RPS

Customer Generation

EE

Elect Vehicles

JRF

Distribution Resource Plan

Interconnection reform

GHG costs

Demand response

Rate reform

Rate cases

storage

What’s ahead?

• RADICALLY DIFFERENT?– All Source Procurement?– Clean Energy Standard?– Death of the special programs?

17

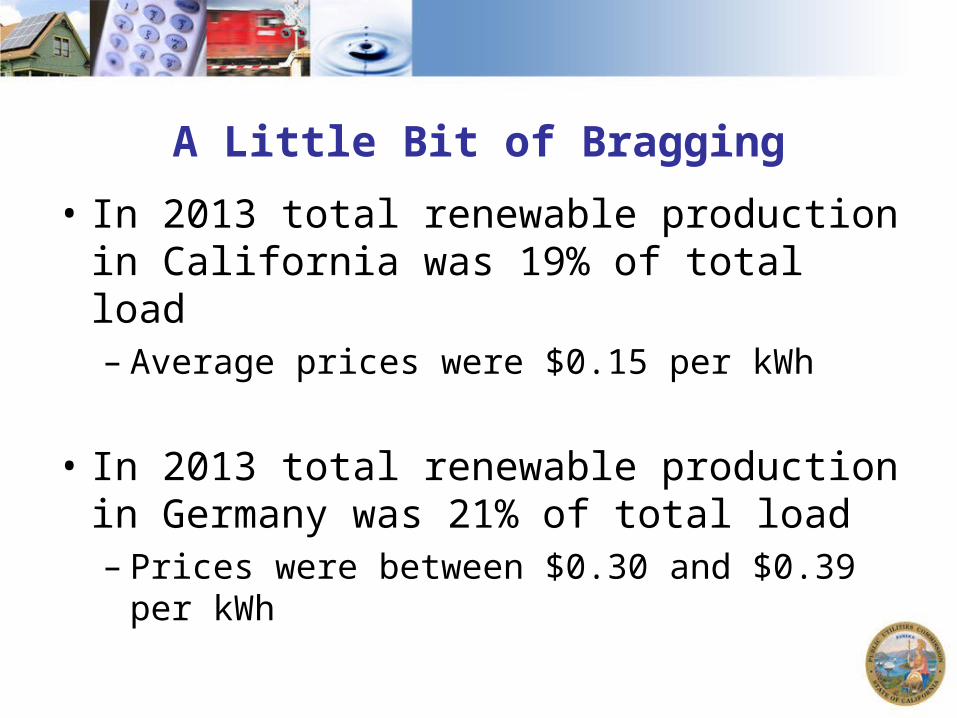

A Little Bit of Bragging

• In 2013 total renewable production in California was 19% of total load– Average prices were $0.15 per kWh

• In 2013 total renewable production in Germany was 21% of total load– Prices were between $0.30 and $0.39 per

kWh

Thank you!For Additional Information:

www.cpuc.ca.govwww.GoSolarCalifornia.ca.gov

www.CalPhoneInfo.com