1 Access regulation and incentives for investment in alternative broadband infrastructure* Harald...

33

1 Access regulation and incentives for investment in alternative broadband infrastructure* Harald Gruber Presentation for REGULATION AND COMPETITION SEMINAR SERIES 07 UPF, the Comisión del Mercado de las Telecomunicaciones (CMT) and the Barcelona Graduate School of Economics Barcelona, 17 December 2007 *The opinions expressed are of the author and need not necessarily reflect those of the EIB.

-

date post

20-Dec-2015 -

Category

Documents

-

view

222 -

download

1

Transcript of 1 Access regulation and incentives for investment in alternative broadband infrastructure* Harald...

1

Access regulation and incentives for investment in alternative broadband infrastructure*

Harald GruberPresentation for

REGULATION AND COMPETITION SEMINAR SERIES 07

UPF, the Comisión del Mercado de las Telecomunicaciones (CMT) and the Barcelona Graduate School of Economics

Barcelona, 17 December 2007

*The opinions expressed are of the author and need not necessarily reflect those of the EIB.

2

Outline

• Sector overview

• Fixed line access regulation

• Investment incentives

• Alternative regulatory scenarios

• Conclusion

3

Past drivers for investment and growth

• Technology– Cost reduction– Performance increase

• Regulatory change– Liberalisation– Changes in market structure

4

EU Commission, 2007

5

EU Commission, 2007

6

EU Commission, 2007

7

EU Commission, 2007

8

Fixed line market

• Slow revenue growth:– Pressure on tariffs– Switch to flat fees– Fixed-mobile substitution

• Pressures on profit margins• Increasing role of data/broadband revenues• Customer access as key revenue source• Persistence of ex ante regulation

9

Fixed line broadband regulation

• Bottleneck in local loop access• Regulatory remedy: open access at cost based

prices:– Service based competition: bitstream, resale

– Facility based competition: Full LLU, shared access

• Asymmetric access regulation of DSL (unbundling) vs. cable modem

10

EU Commission, 2007

11

Ladder of investment theory

• Short term goal of service based competition– Resale– Bitstream

• Long term goal of facility based competition– Shared access– Full local loop unbundling

12

EU wholesale access line availability

20

03

20

04

20

05

20

06

Full ULLShared access

Bitstream access

Resale

0

5000

10000

15000K

lin

es

European Commission, 2007

13

EU DSL wholesale access types

European Commission, 2007

0%

10%

20%

30%

40%

50%

60%

2003 2004 2005 2006

Facility based

Service based

14

Investment incentives

• Increasing investment profile for new entrants.

• Investment effect on incumbent uncertain

15

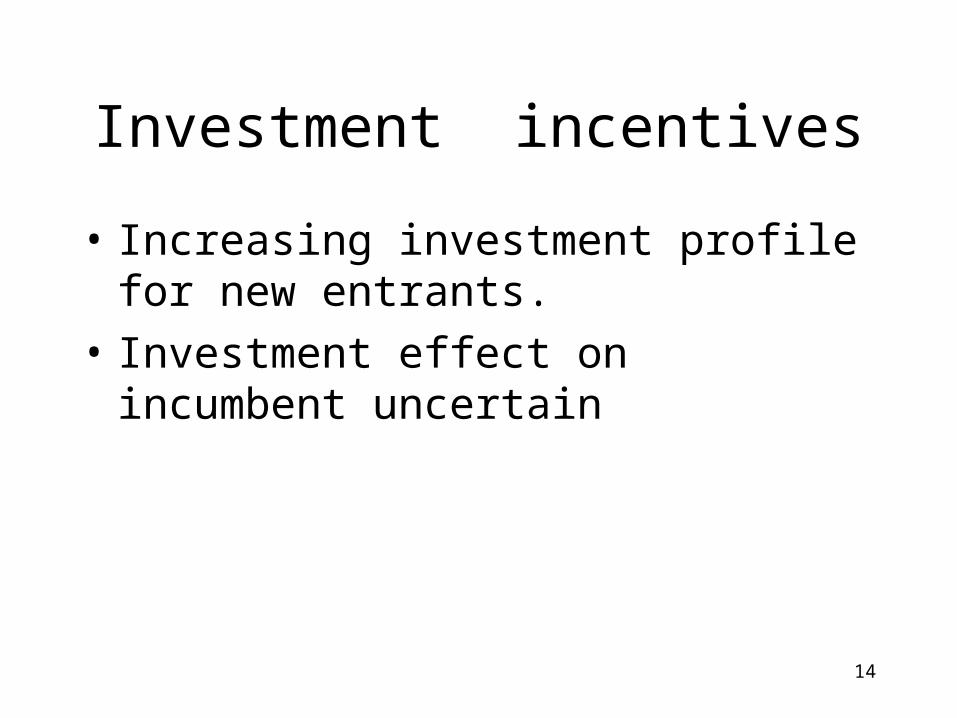

New entrants' market shares in EU

0%

5%

10%

15%

20%

25%

30%

35%

2002 2003 2004

Lines (DSL)

Investment (fixedlines)

Source: EU Commission, LE

Investment ladder without investment?

16

Issues for future investment incentives

• Does next generation access (NGA) require less investment or are investment incentives diminished?

• Is unbundling complement or substitute for new entrants’/incumbents’ investment?

• Incentives for alternative platforms seem reduced (see Waverman et. al, 2007)

17

Role of facility based competition in driving NGA investment

• There is empirical evidence (for US) that inter-platform competition has significant positive effects on diffusion of broadband

• Change in regulatory approach in the US

• Evidence for positive relationship between investment and platform competition

18

Shares of broadband access types in the EU

0%10%20%30%40%50%60%70%80%90%

2003 2004 2005

DSL

Cable modem

Other

Source: European Commission

EU is moving away from platform competition

19

European Commission, 2007

20

Vertical separation as remedy for SMP

• Additional tool proposed: functional separation: separate business units within company

• Analogy with UK, but BT created Openreach on voluntary basis

• Ofcom: no relevance for investment incentives

• Is it creating investment incentives?

21

Source : ARCEP, OTA

Evolution of full unbundling

0500 000

1 000 0001 500 000

2 000 0002 500 0003 000 0003 500 000

janv-05 juil-05 janv-06 juil-06 janv-07 juil-07

France

UK

22

Reservations about functional separation

• Risk of monopoly & persistence of ex ante regulation

• Risk of irreversibility• Investment incentives:

– does not internalise market interdependencies– hold up problem– lack of incentives for quality

• What is the prospect for infrastructure competition

23

Further issues

• Functional separation may not be enough• Structural separation: creation of distinct legal

entitity with different ownership structure • Case of eircom: voluntary structural separation

driven by financial rating considerations• Unclear whether solves lack of investment issue

24

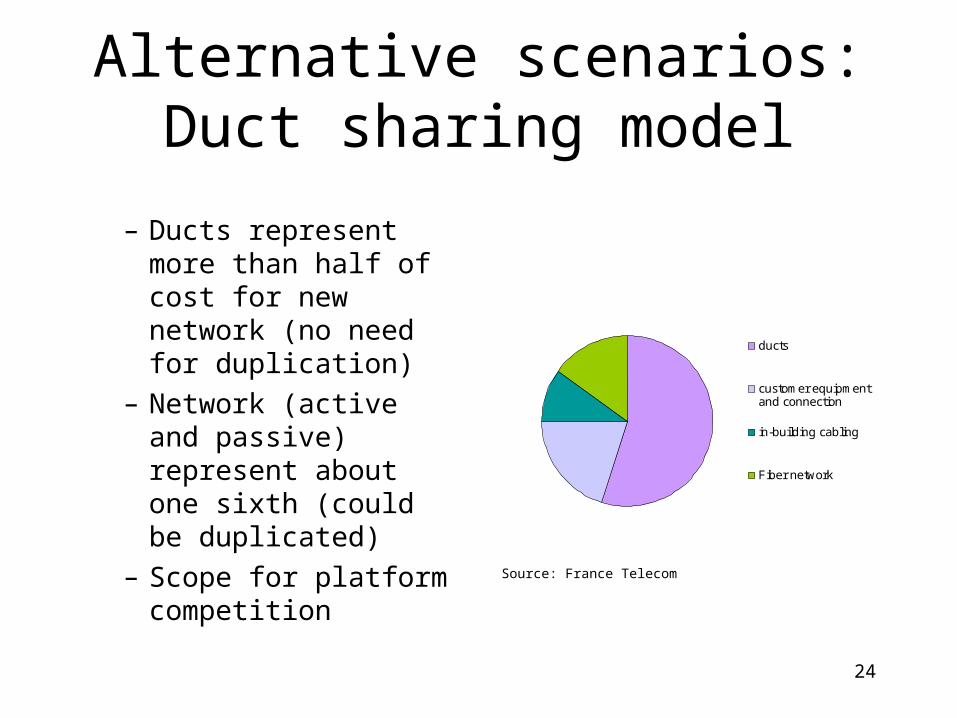

Alternative scenarios:Duct sharing model

– Ducts represent more than half of cost for new network (no need for duplication)

– Network (active and passive) represent about one sixth (could be duplicated)

– Scope for platform competition

ducts

customer equipmentand connection

in-building cabling

Fiber network

Source: France Telecom

25

Alternative scenarios: Unregulated platform competition

– Possible where at least two platforms (DSL+cable) exist already

– Example of the Netherlands

26

Share of broadband platforms

0%

20%

40%

60%

80%

100%

Other

Cable

DSL

Source: OECD

27

Alternative scenarios: Regional regulation

– Regional regulation: regulate only areas with single platform

28

Platform competition

• May not be feasible to the same degree for all EU countries because of absence of cable networks

• Look for alternatives, e.g. radio based technologies– Wimax– HSDPA

• Scope for issuing spectrum licenses (digital dividend)

29

South Korea: Broadband access, by type

0%

10%

20%

30%

40%

50%

60%

70%

2002 2003 2004 2005

DSL

Cable

Other

A counterexample

Source: OECD

30

Cost comparisons

• FTTx investment/subs. in the order of € 1100-1500

• DSL investment/subs. for triple play €200-500

• So investment for NGA are potentially very large

31

Regulatory challenges

• Encourage more investment• What to do with countries with single platform ?• Consider non-uniform regulation across EU?

– Mandatory unbundling (possibly limited time horizon) for countries without alternatives to DSL

– Deregulation in countries with platform competition

32

Investment patterns

Invest

Not Invest

Incumbent New entrant Incumbent New entrant Incumbent New entrant

33

Conclusion

• Regulation has strong effects on investment behaviour– Incumbents– New entrants

• Regulation should not represent a permanent claim on incumbents assets

• Stimulation of facility based competition