1 A presentation for the Institute of Certified Public Accountants of Kenya during the International...

36

1 A presentation for the Institute of Certified Public Accountants of Kenya during the International Public Sector Accounting Standards, IPSAS’s Workshop 7 th & 8 th April 2011 Laico Regency Hotel, Nairobi. Chachi S. Francis,MBA (Free State), BSc (Nairobi) Corporate Governance In the Public Sector

-

Upload

maud-shields -

Category

Documents

-

view

219 -

download

0

Transcript of 1 A presentation for the Institute of Certified Public Accountants of Kenya during the International...

1

A presentation for theInstitute of Certified Public Accountants of Kenya

during theInternational Public Sector Accounting Standards, IPSAS’s Workshop

7th & 8th April 2011 Laico Regency Hotel, Nairobi.

Chachi S. Francis,MBA (Free State), BSc (Nairobi)

Corporate Governance

In the

Public Sector

2

Definitions

• Corporate:– Involving or shared by all members of a group.– Connected with a corporation.

• Corporation:– An organization that is recognised by law as a single unit. – A legal person (in law).

• Govern:– To control or influence somebody/something or how something

happens.

• Governance:– The activity of controlling a country/organisation.

3

contd…definitions• Transform:

– Change the form/appearance of something.

• Transformation:

– The process by which the form/appearance of a thing is changed.

• Q: in your day to day work:

–what are the inputs? Outputs?

–Who are your stakeholders? What are their interest?

4

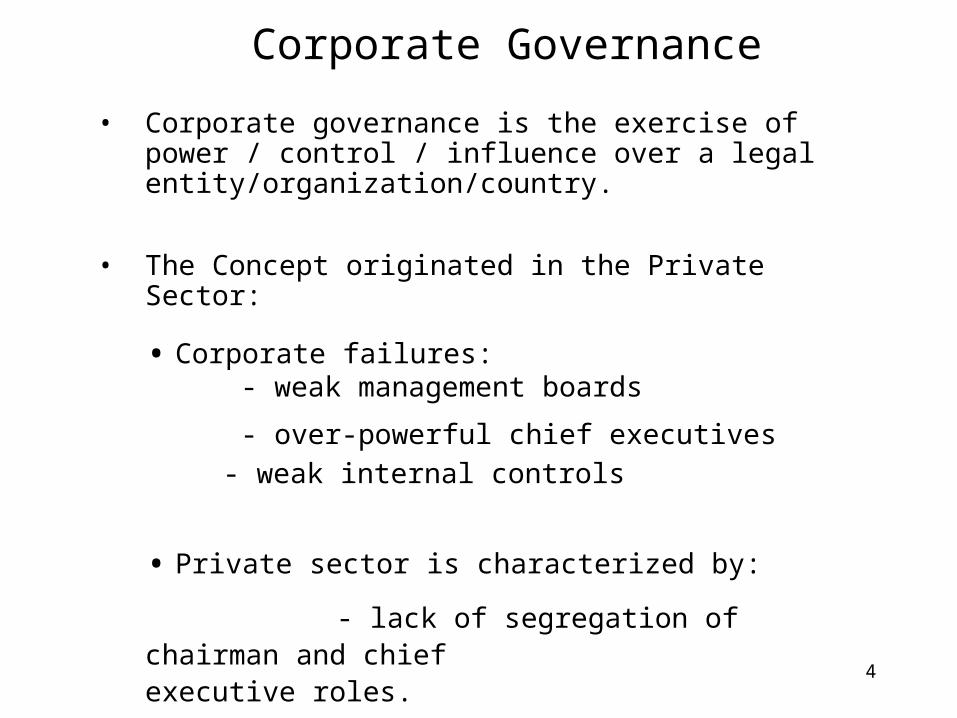

Corporate Governance

• Corporate governance is the exercise of power / control / influence over a legal entity/organization/country.

• The Concept originated in the Private Sector:

• Corporate failures:- weak management boards

- over-powerful chief executives

- weak internal controls

• Private sector is characterized by:

- lack of segregation of chairman and chief executive roles.

- lack of audit committee/internal audit functions

- weak control/override of controls.

5

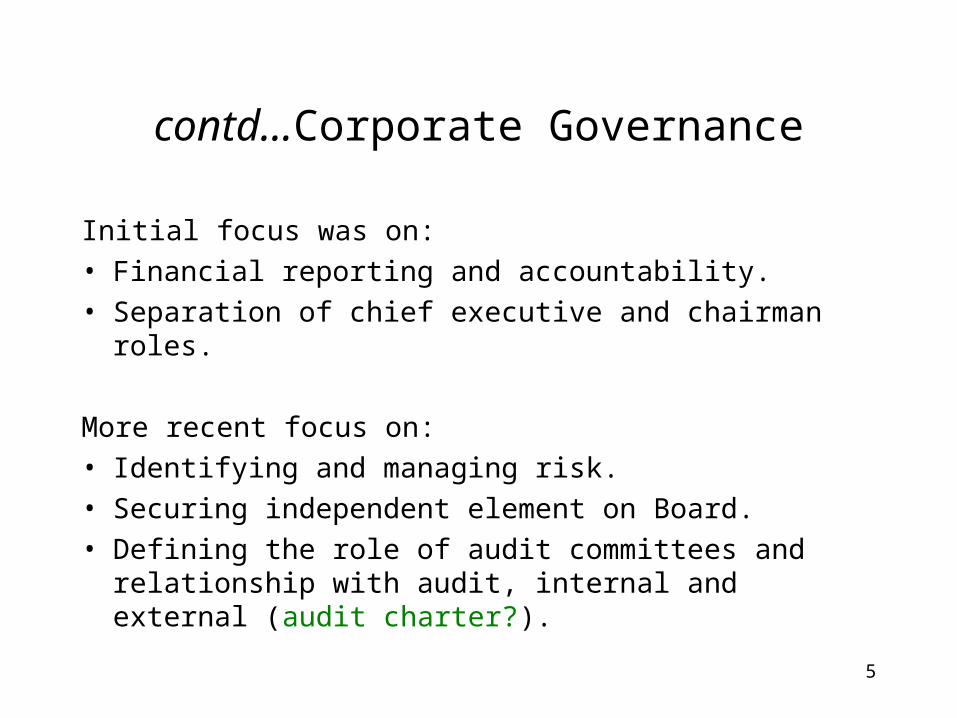

contd…Corporate Governance

Initial focus was on:• Financial reporting and accountability.• Separation of chief executive and chairman roles.

More recent focus on:• Identifying and managing risk.• Securing independent element on Board.• Defining the role of audit committees and relationship

with audit, internal and external (audit charter?).

66

Corporate Governance

Factors influencing corporate governance:

• Is there an issue about concentration of power?

• Is there clarity about about reporting to stakeholders?

• Is there clarity about accountability? Indeed what is meant by accountability?

• Is there an issue of risk and if so how well is it managed?

• Is there need for an independent element to review executive management and to liase with audit?

7

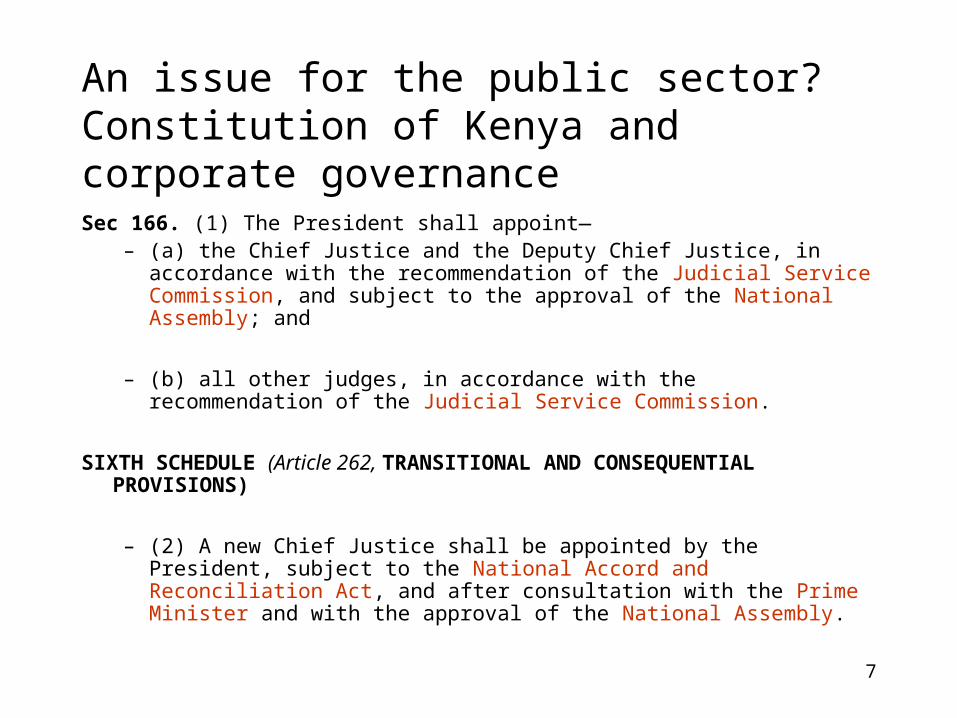

An issue for the public sector?Constitution of Kenya and corporate governance

Sec 166. (1) The President shall appoint—– (a) the Chief Justice and the Deputy Chief Justice, in

accordance with the recommendation of the Judicial Service Commission, and subject to the approval of the National Assembly; and

– (b) all other judges, in accordance with the recommendation of the Judicial Service Commission.

SIXTH SCHEDULE (Article 262, TRANSITIONAL AND CONSEQUENTIAL PROVISIONS)

– (2) A new Chief Justice shall be appointed by the President, subject to the National Accord and Reconciliation Act, and after consultation with the Prime Minister and with the approval of the National Assembly.

8

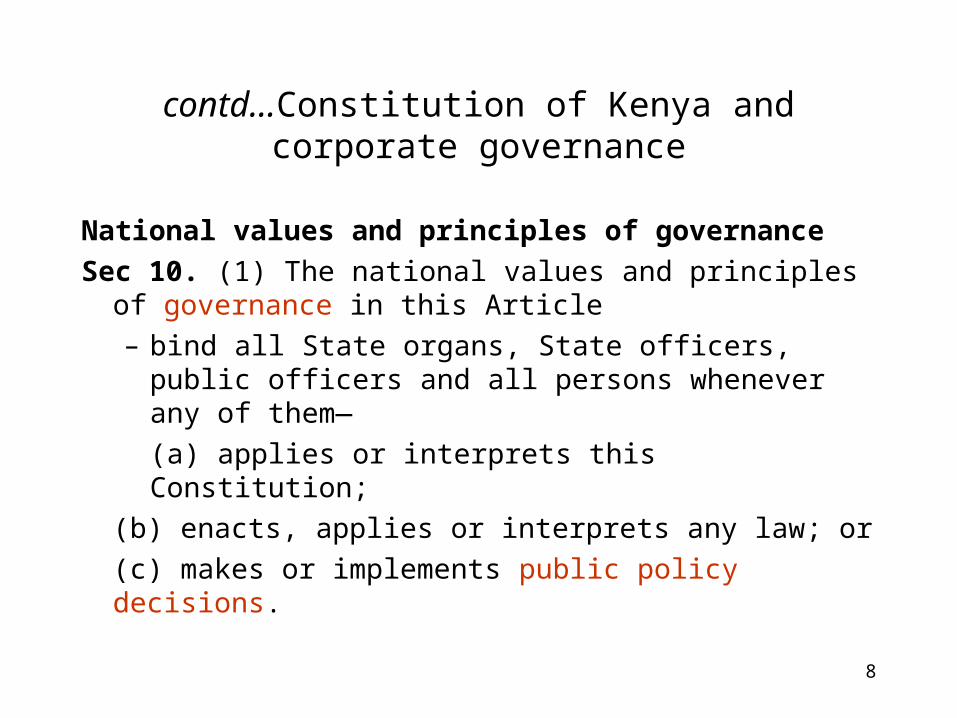

contd…Constitution of Kenya and corporate governance

National values and principles of governanceSec 10. (1) The national values and principles of

governance in this Article– bind all State organs, State officers, public officers

and all persons whenever any of them—(a) applies or interprets this Constitution;

(b) enacts, applies or interprets any law; or(c) makes or implements public policy

decisions.

9

National values

(2) The national values and principles of governance include –

a)patriotism, national unity, sharing and devolution ofpower, the rule of law, democracy and participation ofthe people;

(b) human dignity, equity, social justice, inclusiveness,equality, human rights, non-discrimination and

protection of the marginalised;

(c) good governance, integrity, transparency andaccountability; and

(d) sustainable development.

10

Bill of rights

20 (3) In applying a provision of the Bill of Rights, a court shall —(b) adopt the interpretation that most favours the enforcement of a right or fundamental freedom.

21 (4) In interpreting the Bill of Rights, a court, tribunal or other authority shall promote —(a) the values that underlie an open and democratic society……

1111

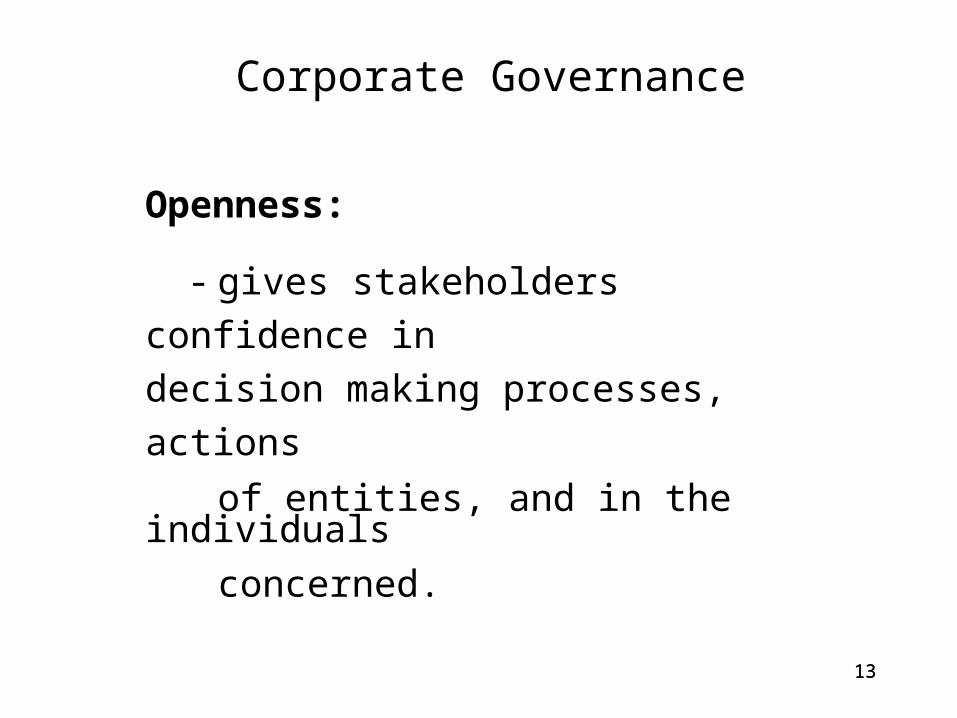

Corporate Governance

Public Sector Definition:

“The system by which organisations are directed and controlled”

Underlying this definition are three principles:

- Openness

- Integrity

- Accountability

12

Objective of IPSAs

• IPSAs aim to:

– improve the quality of general purpose financial reporting by public sector entities, leading to better informed assessments of the resource allocation decisions made by governments, thereby increasing transparency and accountability.

1313

Corporate Governance

Openness:

- gives stakeholders confidence in

decision making processes, actions

of entities, and in the individuals

concerned.

1414

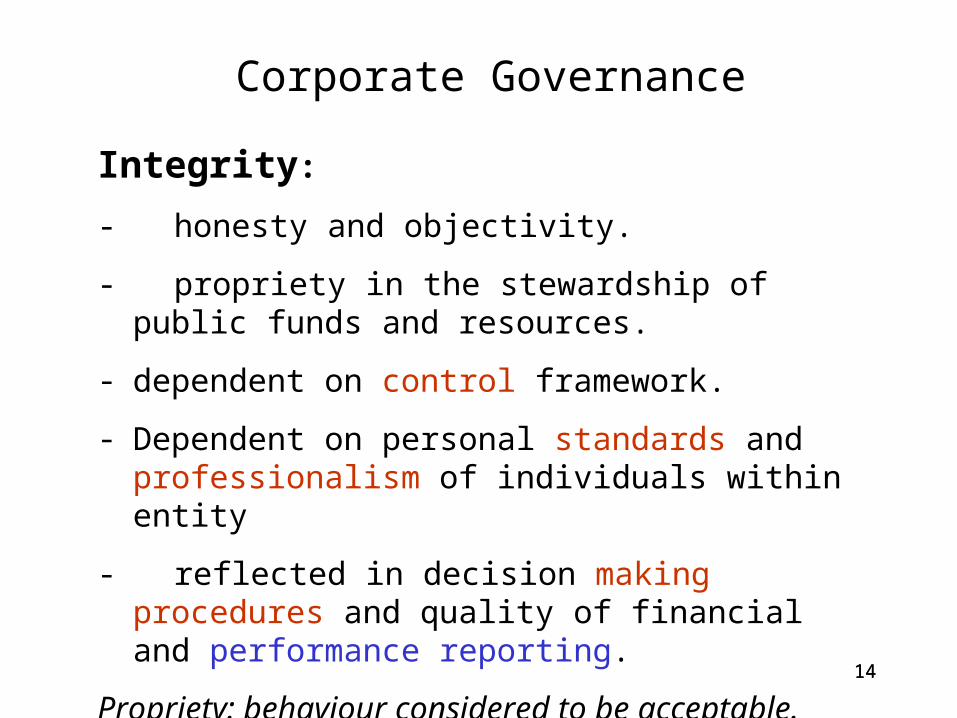

Corporate Governance

Integrity:

- honesty and objectivity.

- propriety in the stewardship of public funds and resources.

- dependent on control framework.

- Dependent on personal standards and professionalism of individuals within entity

- reflected in decision making procedures and quality of financial and performance reporting.

Propriety: behaviour considered to be acceptable.

1515

Corporate Governance

Accountability:

- process whereby entities and individuals within them are responsible for their decisions and actions, including stewardship of public funds and performance

- achieved though clarity of responsibilities and roles

1616

Corporate Governance principles

These principles are reflected in four “dimensions” of public sector governance:

- standards of behaviour (Balance of

Power and Authority)

- organisational structures and processes

- control

- external reporting

1717

Standards of corporate governance/ Balance of Power

There should be a governing body of a Public Sector Entity with:

Chairperson of the Governing body (e.g. Board of Directors / Governors / Trustees,

Non-executive Members of Governing body.

Executive Management. Organisation leaders determine values and standards. Organisation should publish formal code of conduct. Code of conduct should cover: probity and propriety,

selflessness, objectivity, honesty. Relationships – actual or potential conflicts of interest

including political interests to be disclosed. Gifts, hospitality and entertainment controlled to ensure

‘no undue influence’.

18

Structures and processes

Board

CEO

Stakeholders

Public

Shareholders

Other RegulatorsPPOA, ERB, KACC,

etc etc etc

Auditor

19

contd…structure and processes

• Clear policy on hiring and removal (of staff, directors, contractors).

• Clarity of roles of shareholders, BOD, management. • Clear qualification requirements.• Clarity of remunerations.• Clear code of conduct and made available to all

persons involved (staff, directors etc).• Clarity of Board schedule of meetings, reporting, etc.• Clarity of corporate social responsibility interventions.

2020

Control

Risk Management

• Internal Audit

• Audit Committees

• Internal Control

• Budgeting, Financial Management, Training.

• Identify nature and extent of major risks.

• Review of past risks.

• Identify new risks arising from new objectives and activities.

• Anticipate future risks and changes to risk.

• Assess ability to reduce incidence of risk.

2121

External Reporting

Annual Reporting including:

Use of Appropriate Accounting Standards.

Performance against targets.

External Audit.

Statement of aims and objectives.

Commentary on the accounts and performance.

Statement of compliance with relevant codes.

2222

Role of the governing body- defines the vision, mission and long-term objectives

within policy and resource framework.

- oversees delivery of planned results.

- appoints senior management

- approves and adopts annual report, including financial statements.

- ensures there is an effective system of internal control.

- oversees the processes of risk management

2323

Chairpersonseparate from Chief Executive

• preferably independent (non-executive).

• provides leadership and cohesion.

• ensures there is an effective process for reviewing performance of governing body (Board assessment).

• ensures that the governing body has adequate support and information.

• ensures that the business of the governing body is undertaken efficiently and on a timely basis.

2424

Audit Committee

• At highest level of the organisation

• Is independent of executive management.

• Is a sub-committee of governing body.

• Membership confined to non-executives.

• Chairman to be other than chairman of board

• Meetings normally attended by Finance officer, internal auditor and external auditors.

• Have authority to investigate any matter.

2525

Audit Committee’s Terms of Reference• May also known as the Audit Charter.

• General roles include:

• oversight over management’s responsibility for effectiveness of internal control system.

• review adequacy of policies and practices for ensuring compliance with regulations, policies, etc.

• review adequacy of internal audit resources.

• recommend/approve appointment/removal of head of internal audit.

• review activities and programme of internal audit, and co-ordination with external audit.

• oversee entity’s relationship with external auditor.

26

Trends in corporate governance in the public sector

Now considered a serious issue in the public sector because of concerns about:

• Excessive confidentiality in decision making.• Avoiding influence of special interests?• Inefficiency in public expenditure.

Now greater demand for:• Openness and accountability in government, with• Greater willingness to challenge decisions.

27

Control of public money (Constitution of Kenya)

A state organ may be denied funds only for a serious material breach or persistent material breaches.

However, a decision to stop the transfer of funds:

• may not stop the transfer of more than fifty per cent of funds due to a county government.

• shall not stop the transfer of funds for more than sixty days; and

• will require the approval of both houses of parliament within thirty days or else the decision lapses.

28

Controller of Budget and Auditor General

The new constitution of Kenya separates the functions of:“Controller of Budget”; and“Auditor General.

Q: What are the implications if both positions were to be held by one person?

29

Controller of Budget

Role of The Controller of Budget:

to oversee the implementation of the budgets of the national and county governments by authorising withdrawals from public funds.

to submit to each House of Parliament a report on the implementation of the budgets of the national and county governments every four months.

30

Auditor General

The Auditor-General:

may audit and report on the accounts of any entity that is funded from public funds.

Submits audit reports to Parliament or county assembly.

To be audited by a professionally qualified accountant appointed by Parliament.

31

Parliament/county assembly

Parliament or the county assembly shall, within 3 months after receiving an audit report, debate and consider the report and take appropriate action.

32

The link to globalization

• Globalisation:– The process by which regional economies, societies, and cultures

have become integrated through a global network of political ideas, communication, transportation, trade, technology, culture etc.

• In essence, the world has become a global village and hence the evolution of uniformity/standards:– Air travel safety standards– IT / Telecommunication standards (computers, mobiles etc).– Radiation standards (X-rays, transceivers, scanners etc).– Financial standards (IFRS, IPSAs etc).– Audit standards (IAS).– Etc

• The UN system has adopted IPSAs.

33

Benefits of corporate governance1. The separation of ownership and control.

2. Alignment of the interests of the organization, shareholders , board, employees as well as the community in which the organization operates.

3. Protection of organizations as they are important to the welfare of individuals-

a) They create jobs, generate income and income tax.

b) They produce a wide variety of goods and services.

c) They provide mechanisms for savings and investments.

4. Creation of efficient organizations.

5. Environmentally and socially responsible corporate organizations.

6. Promotes competitiveness.

7. Gives confidence to investors.

34

Parting shot

The primary responsibility for ensuring that Good Corporate Governance prevails in an institution lies with the BOARD of DIRECTORS of the corporate body.

35

SummaryDo we agree:

• Corporate governance is an issue for the public sector?

• There is a link with efficiency/effectiveness?• About the standards that should be covered?• That there will be effects upon the organisation?• About the impacts on reporting and control?• That personal behaviour has to be covered?

Overall, will raising the standards of corporate governance lead to better public services?

36

Further reading• Garratt, B. (ed.). 2003. Developing Strategic Thought: A Collection of the Best Thinking on

Business Strategy. London: Profile Books.• Peters, T. 2003. Re-imagine! Business Excellence in a Disruptive Age,. London: Dorling Kindersley.• Noel Hepworth, 2003. Corporate Governance in the Public Sector, CEF Conference, Slovenia.• Wikimedia Foundation, Inc. 2011, International Public Sector Accounting Standards, retrieved 4th

April 2011, from www.wikipedia.org.• Wikimedia Foundation, Inc. 2011, Globalization, retrieved 4th April 2011, from www.wikipedia.org.• International Federation of Accountants. International Public Sector Accounting Standards Board,

retrieved 4th April 2011, from www.ifac.org.• Commonwealth of Australia. 2009. Corporate Governance: Handbook for the board: 5 Useful

guides and checklists, retrieved 4th April 2011, from www.w3.org.• United Nations Development Programme. 2009. Orientation Session on International Public Sector

Accounting Standards (IPSAS).• David Woodward,2004. Corporate Governance in the Public Sector. European Internal Audit

Conference.• Eudora Koranteng. 2004. Corporate Governance. Ghana.

Thank [email protected]