99SSP_Template · Web viewThis document is intended for informational purposes only. ...

Upload

sydney-youngCategory

view

213download

0

112/2013

UCSB Human Resources, Benefits

This presentation is intended for communication purposes only. Please see the At Your Service website (http://atyourservice.ucop.edu) and plan documents for complete information.

Medical Plan Comparison

2

Topics

• Medical Plan Design 101• Medical Plan Comparisons

◊ Residence requirements◊ Choice of physician◊ Cost of care & prescription drugs◊ Out of Pocket Maximum◊ Health Savings Account◊ Behavioral Health

3

What is your priority?

• Cost to enroll – monthly premium

• Cost of care ◊ Predictable, low cost copays◊ Pay a % of each service

• Choice of providers◊ HMO medical group physicians◊ PPO preferred network or any provider

• Effort to manage – coordinating care &

bills

Medical Plan Design 101

HMOPPOPLUS

5

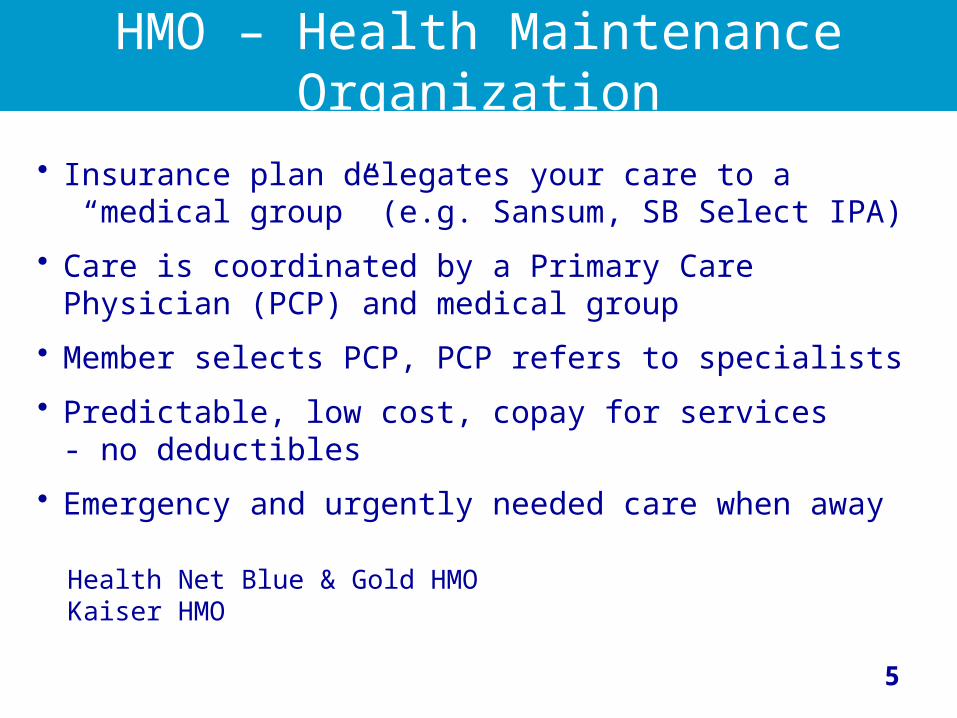

HMO – Health Maintenance Organization

• Insurance plan delegates your care to a “medical group” (e.g. Sansum, SB Select IPA)

• Care is coordinated by a Primary Care Physician (PCP) and medical group

• Member selects PCP, PCP refers to specialists

• Predictable, low cost, copay for services - no deductibles

• Emergency and urgently needed care when away

Health Net Blue & Gold HMOKaiser HMO

6

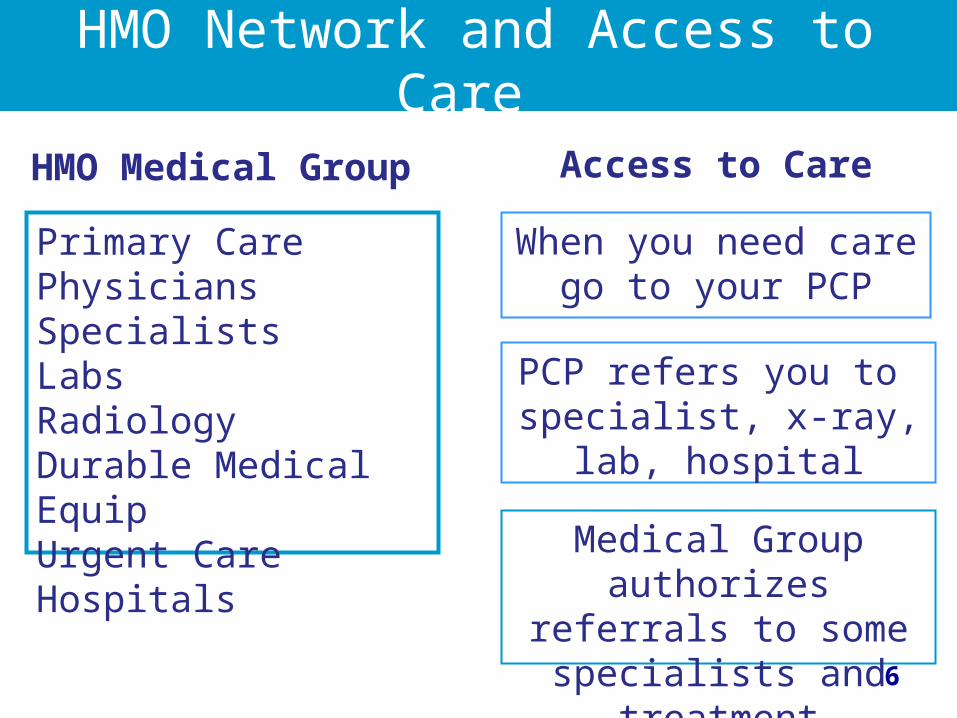

HMO Network and Access to Care

Primary Care PhysiciansSpecialistsLabsRadiologyDurable Medical EquipUrgent CareHospitals

When you need care go to your PCP

PCP refers you to specialist, x-ray, lab,

hospital

HMO Medical Group

Medical Group authorizes referrals to some specialists and

treatment

Access to Care

7

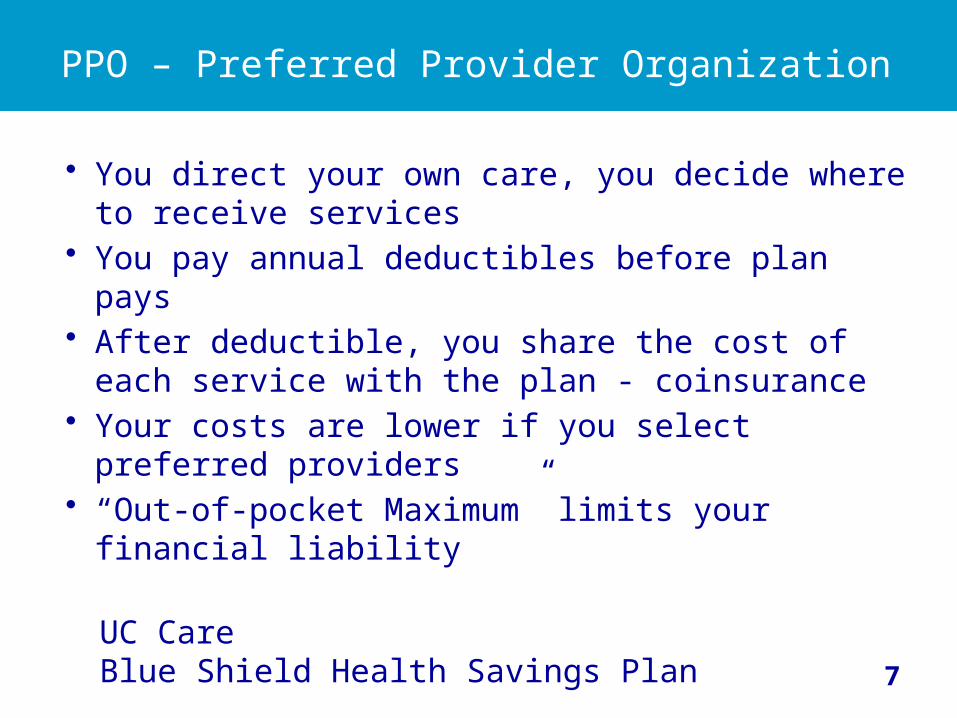

PPO – Preferred Provider Organization

• You direct your own care, you decide where to receive services

• You pay annual deductibles before plan pays• After deductible, you share the cost of each

service with the plan - coinsurance• Your costs are lower if you select preferred

providers• “Out-of-pocket Maximum” limits your

financial liability

UC Care Blue Shield Health Savings Plan

8

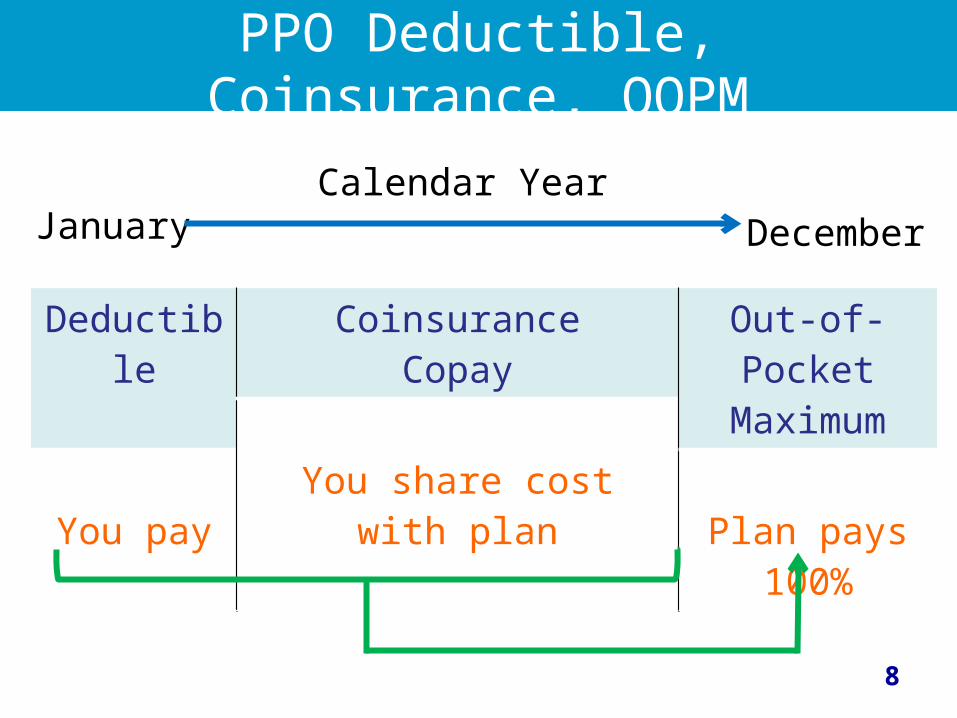

PPO Deductible, Coinsurance, OOPM

JanuaryCalendar Year

December

Deductible

You pay

CoinsuranceCopay

You share cost with plan

Out-of-Pocket

Maximum

Plan pays 100%

9

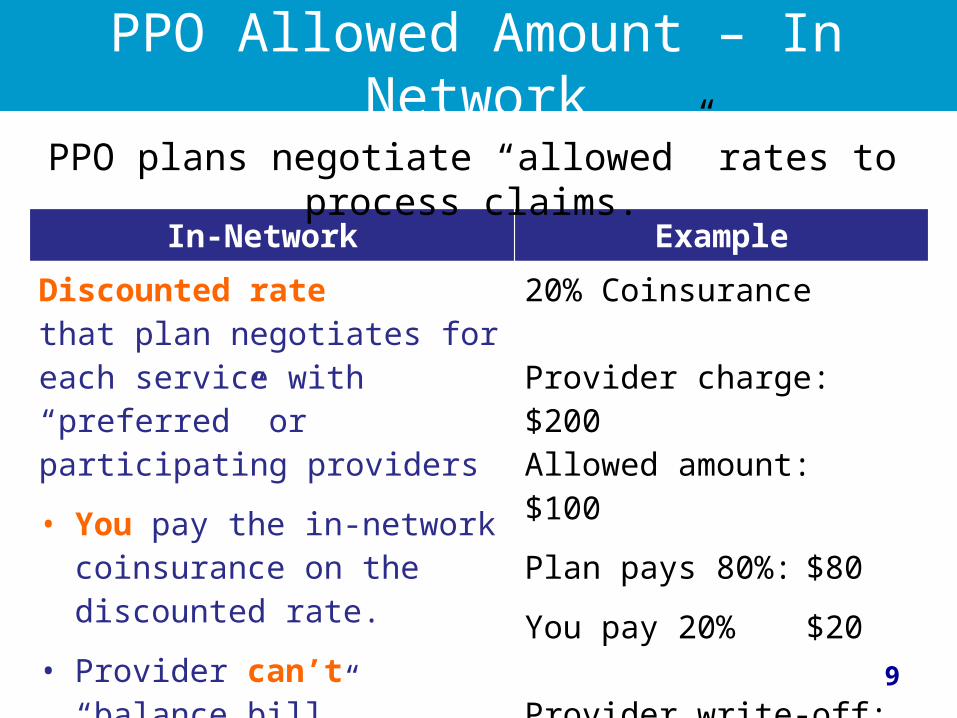

PPO Allowed Amount – In Network

In-Network Example

Discounted rate that plan negotiates for each service with “preferred” or participating providers

• You pay the in-network coinsurance on the discounted rate.

• Provider can’t “balance bill”

20% Coinsurance

Provider charge: $200Allowed amount: $100

Plan pays 80%: $80

You pay 20% $20

Provider write-off:$100

PPO plans negotiate “allowed” rates to process claims.

10

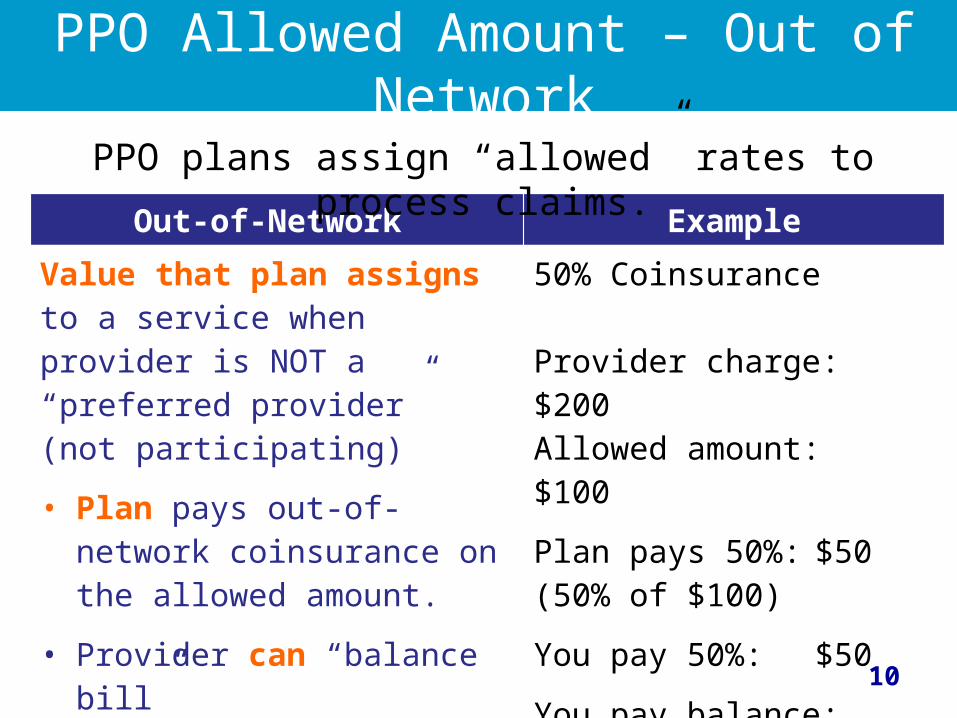

PPO Allowed Amount – Out of Network

Out-of-Network Example

Value that plan assigns to a service when provider is NOT a “preferred provider” (not participating)

• Plan pays out-of-network coinsurance on the allowed amount.

• Provider can “balance bill”

50% Coinsurance

Provider charge: $200Allowed amount: $100

Plan pays 50%: $50(50% of $100)

You pay 50%: $50

You pay balance: $100

PPO plans assign “allowed” rates to process claims.

11

PPO Claims, EOBs & Bills

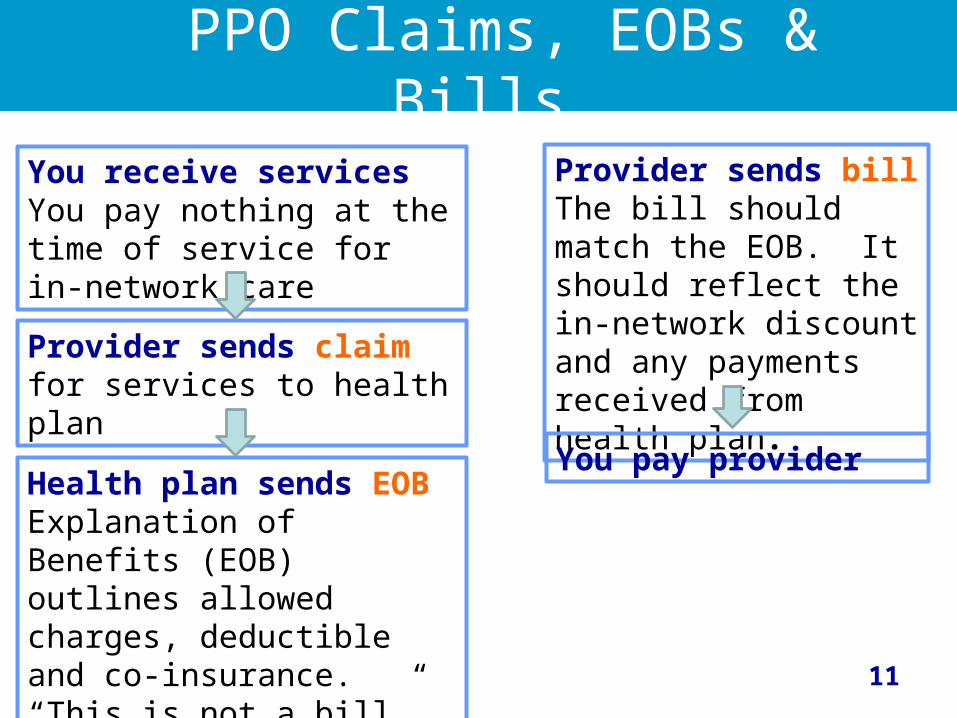

You receive servicesYou pay nothing at the time of service for in-network care

Provider sends claim for services to health plan

Health plan sends EOBExplanation of Benefits (EOB) outlines allowed charges, deductible and co-insurance. “This is not a bill”.

Provider sends billThe bill should match the EOB. It should reflect the in-network discount and any payments received from health plan.

You pay provider

12

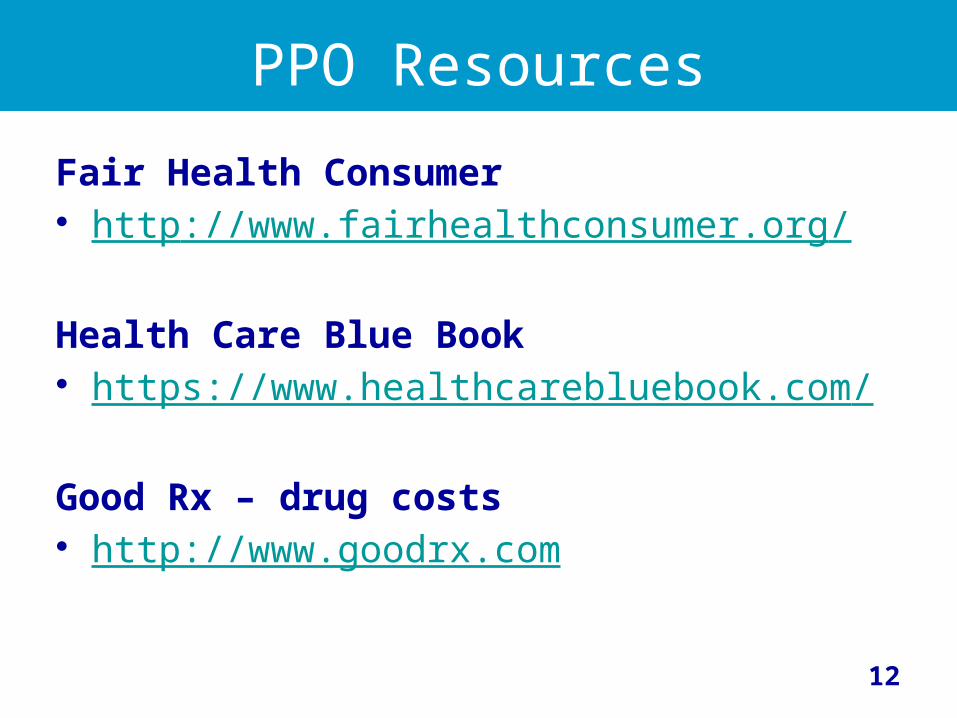

PPO Resources

Fair Health Consumer• http://www.fairhealthconsumer.org/

Health Care Blue Book• https://www.healthcarebluebook.com/

Good Rx – drug costs• http://www.goodrx.com

13

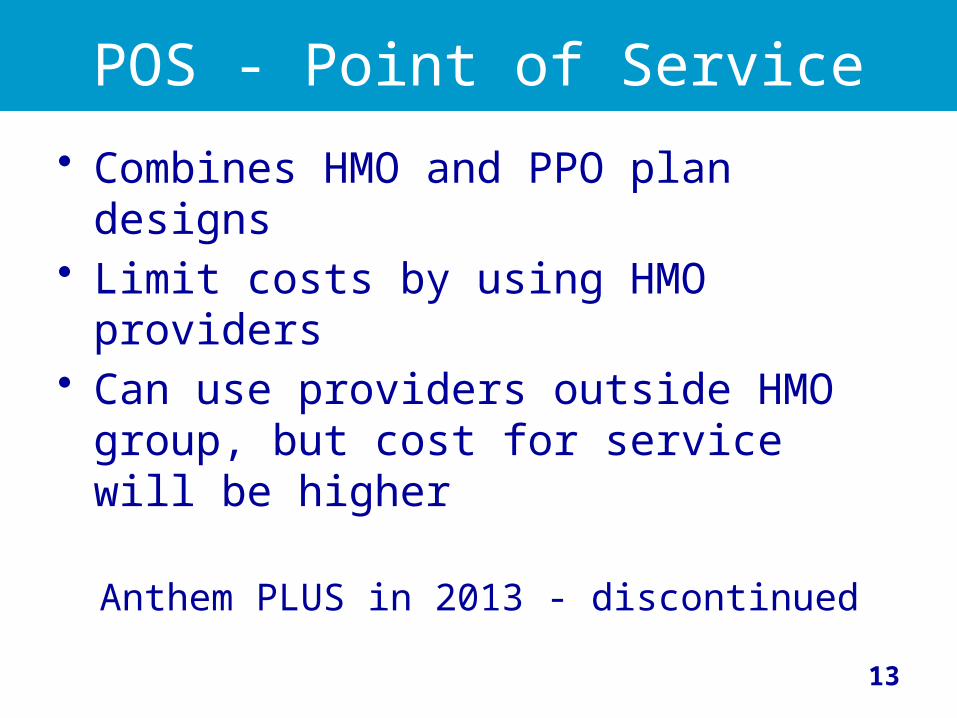

POS - Point of Service

• Combines HMO and PPO plan designs• Limit costs by using HMO providers• Can use providers outside HMO

group, but cost for service will be higher

Anthem PLUS in 2013 - discontinued

14

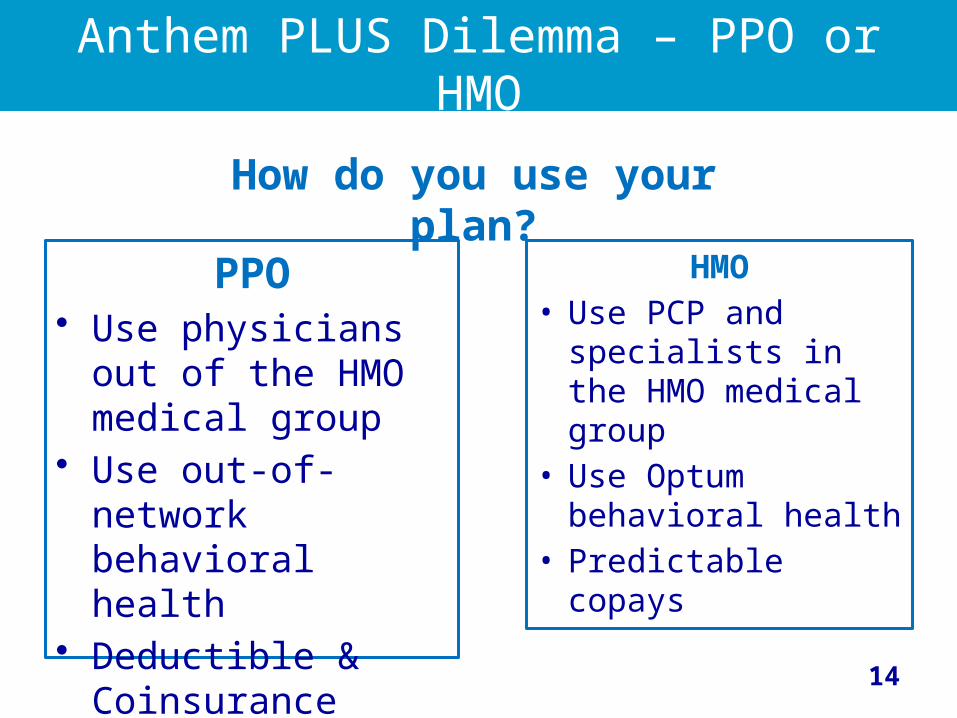

Anthem PLUS Dilemma – PPO or HMO

PPO• Use physicians out

of the HMO medical group

• Use out-of-network behavioral health

• Deductible & Coinsurance

HMO• Use PCP and

specialists in the HMO medical group

• Use Optum behavioral health

• Predictable copays

How do you use your plan?

2014 Medical Plans

Health Net Blue & Gold HMOKaiser HMO

UC CareBlue Shield Health Savings Plan

Core

16

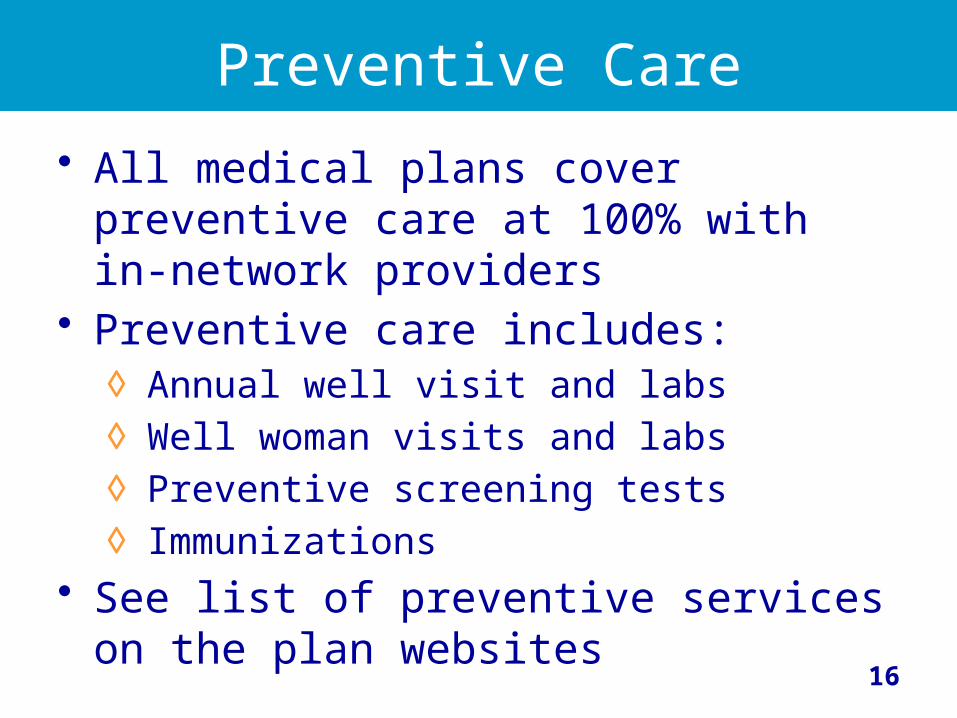

Preventive Care

• All medical plans cover preventive care at 100% with in-network providers

• Preventive care includes:◊ Annual well visit and labs◊ Well woman visits and labs◊ Preventive screening tests◊ Immunizations

• See list of preventive services on the plan websites

17

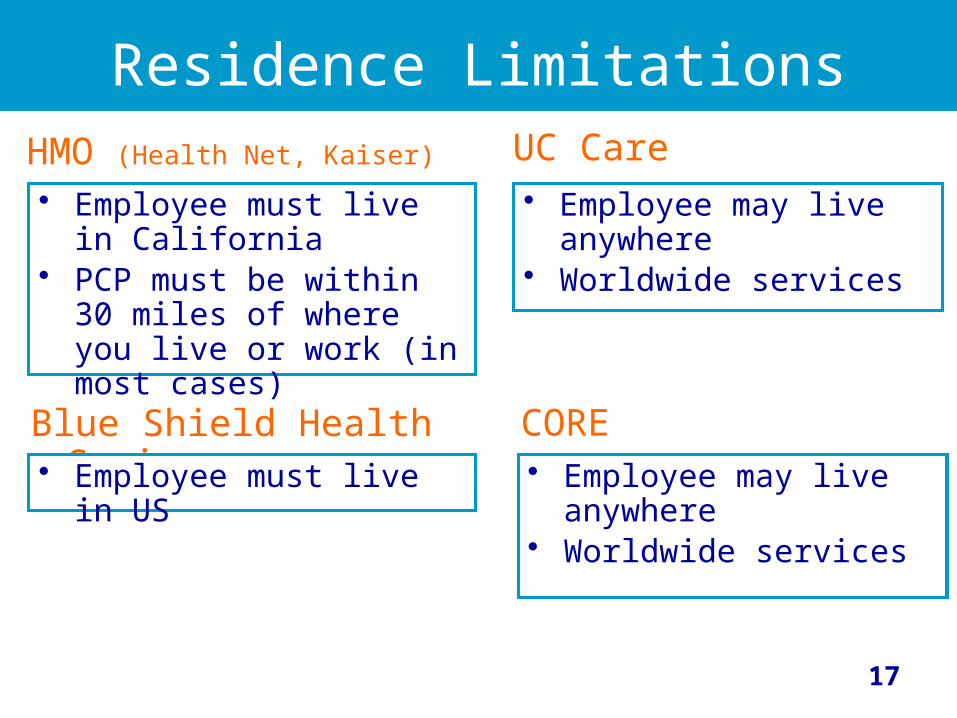

Residence LimitationsHMO (Health Net, Kaiser)

• Employee must live in California

• PCP must be within 30 miles of where you live or work (in most cases)

Blue Shield Health Savings• Employee must live in US

• Employee may live anywhere

• Worldwide services

CORE

UC Care

• Employee may live anywhere

• Worldwide services

• Employee may live anywhere

• Worldwide services

18

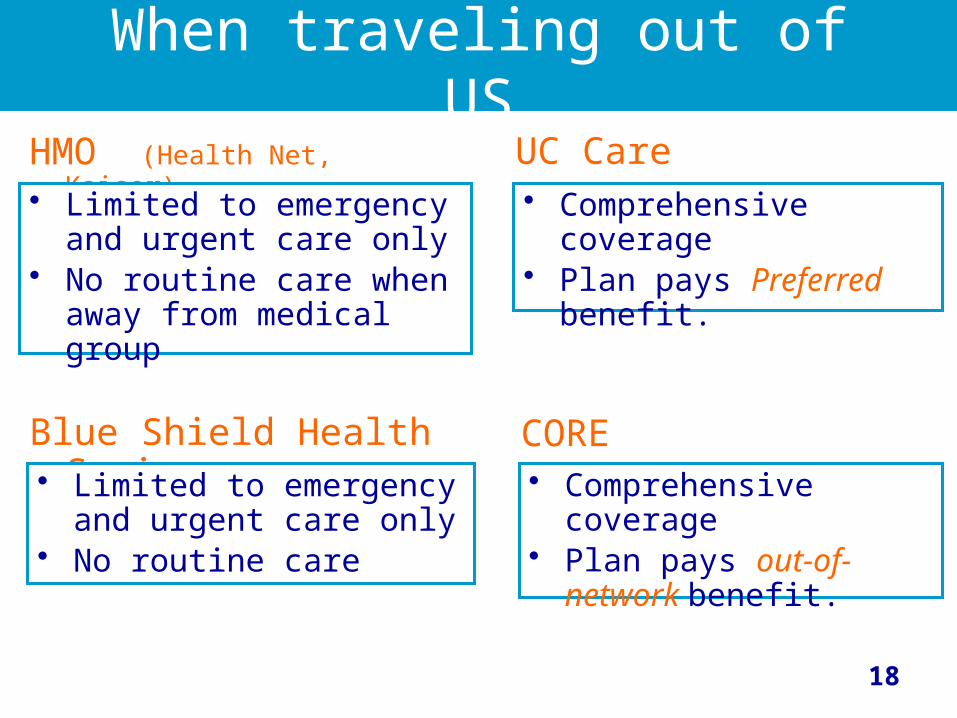

When traveling out of USHMO (Health Net, Kaiser)

• Limited to emergency and urgent care only

• No routine care when away from medical group

Blue Shield Health Savings• Limited to emergency and urgent care only

• No routine care

• Comprehensive coverage

• Plan pays Preferred benefit.

CORE

UC Care

• Comprehensive coverage

• Plan pays out-of-network benefit.

19

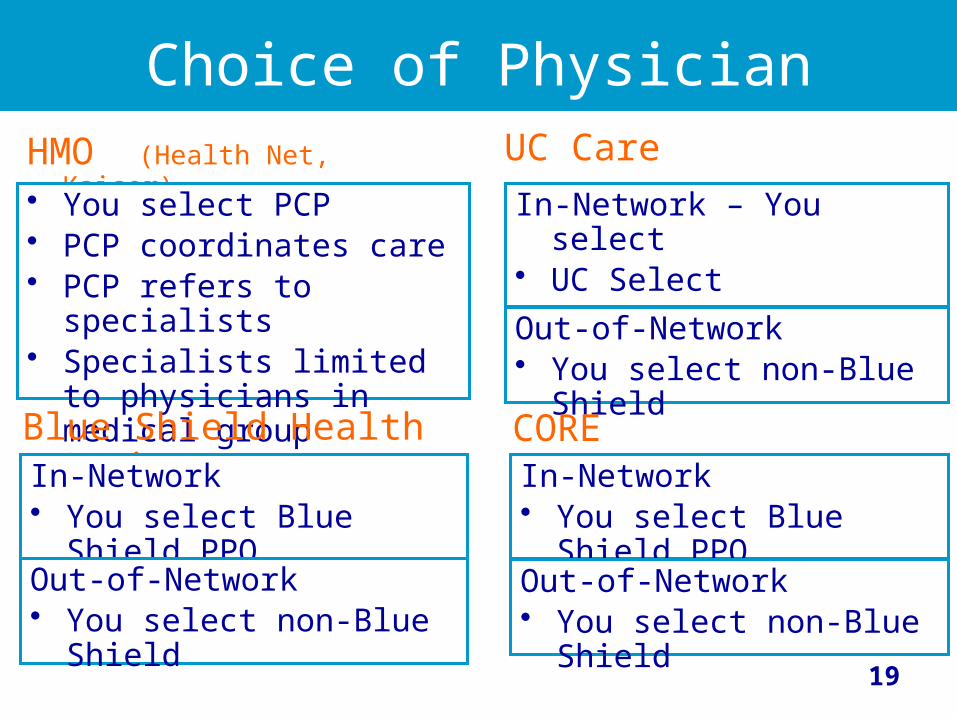

Choice of PhysicianHMO (Health Net,

Kaiser)• You select PCP• PCP coordinates care• PCP refers to specialists• Specialists limited to

physicians in medical group

Blue Shield Health SavingIn-Network

• You select Blue Shield PPO

Out-of-Network• You select non-Blue

Shield

In-Network – You select• UC Select• Blue Shield Preferred

PPOOut-of-Network• You select non-Blue

ShieldCORE

UC Care

In-Network • You select Blue Shield

PPOOut-of-Network• You select non-Blue

Shield

20

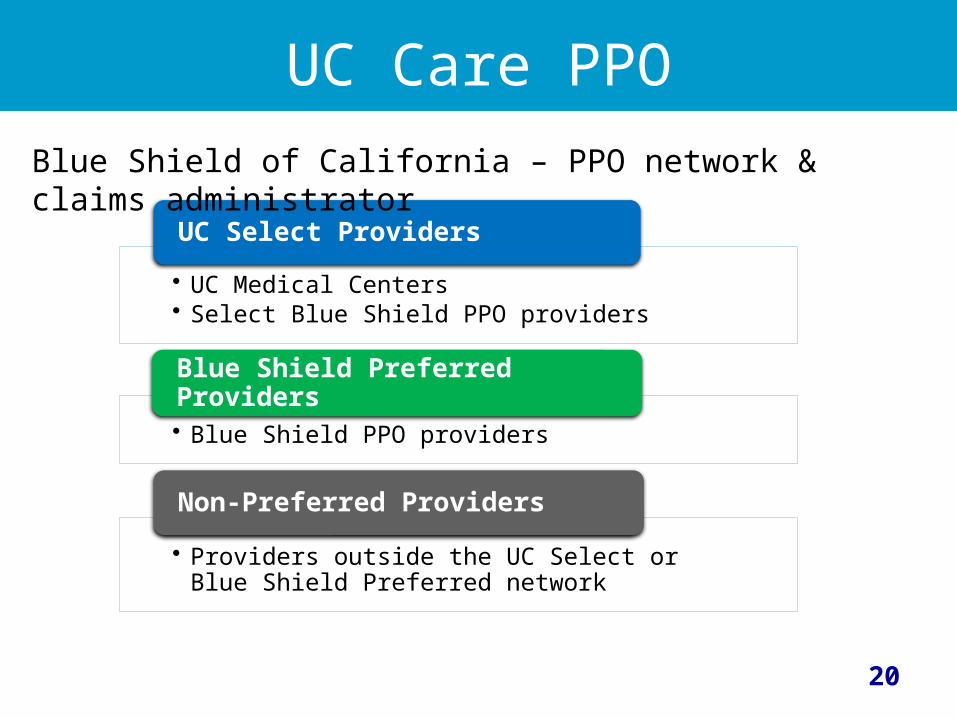

UC Care PPO

• UC Medical Centers• Select Blue Shield PPO providers

UC Select Providers

• Blue Shield PPO providers

Blue Shield Preferred Providers

• Providers outside the UC Select or Blue Shield Preferred network

Non-Preferred Providers

Blue Shield of California – PPO network & claims administrator

21

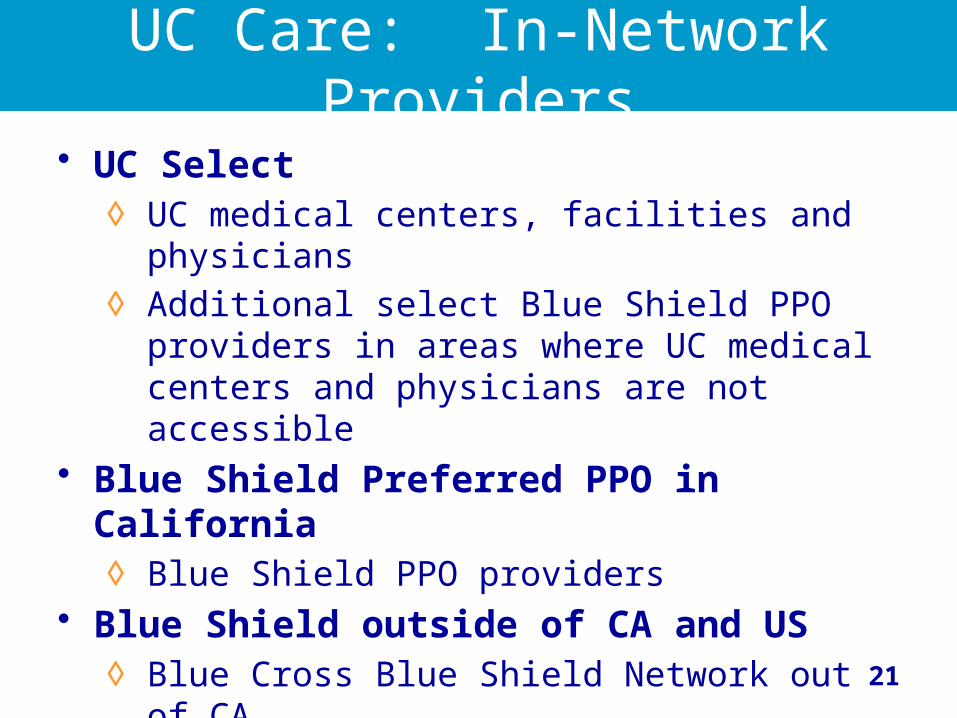

UC Care: In-Network Providers

• UC Select ◊ UC medical centers, facilities and

physicians◊ Additional select Blue Shield PPO providers

in areas where UC medical centers and physicians are not accessible

• Blue Shield Preferred PPO in California◊ Blue Shield PPO providers

• Blue Shield outside of CA and US◊ Blue Cross Blue Shield Network out of CA◊ BlueCard Network out of US

22

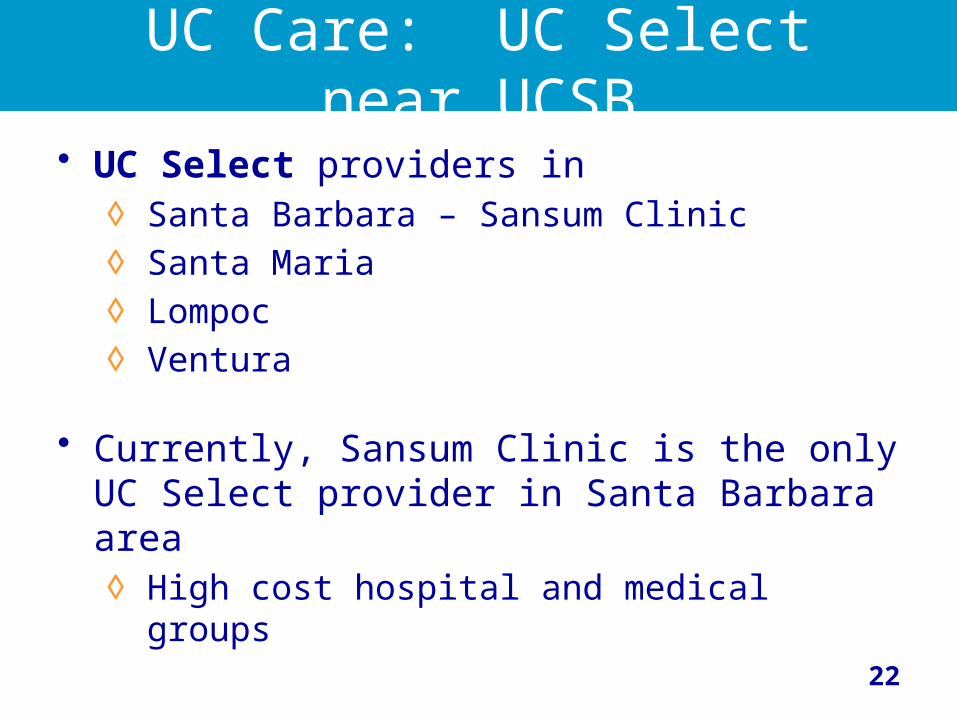

UC Care: UC Select near UCSB

• UC Select providers in◊ Santa Barbara – Sansum Clinic ◊ Santa Maria◊ Lompoc◊ Ventura

• Currently, Sansum Clinic is the only UC Select provider in Santa Barbara area◊ High cost hospital and medical groups

23

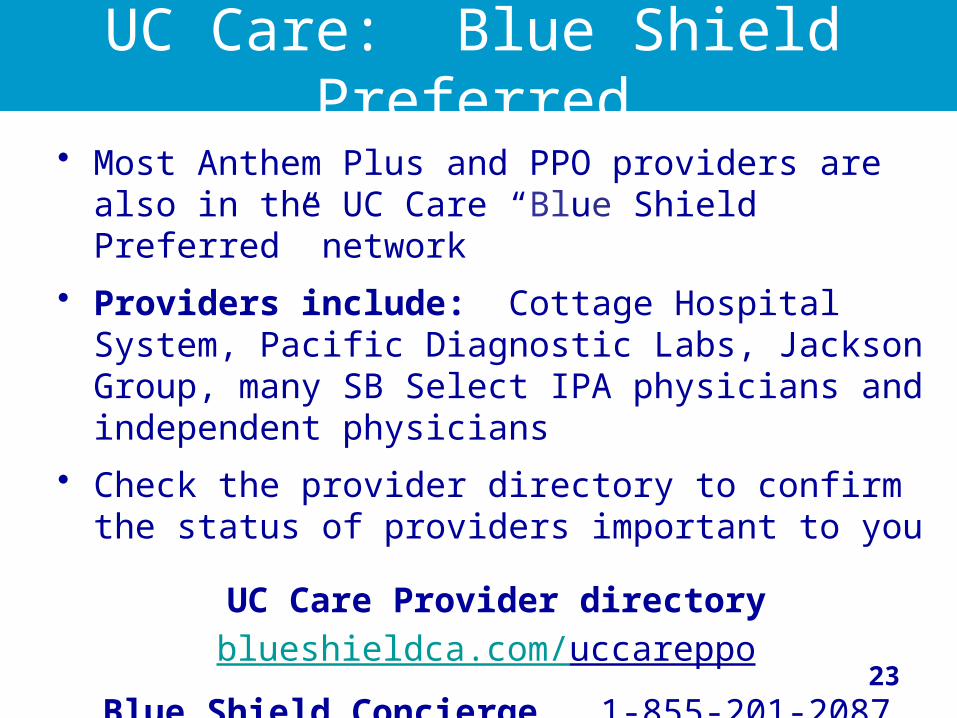

UC Care: Blue Shield Preferred

• Most Anthem Plus and PPO providers are also in the UC Care “Blue Shield Preferred” network

• Providers include: Cottage Hospital System, Pacific Diagnostic Labs, Jackson Group, many SB Select IPA physicians and independent physicians

• Check the provider directory to confirm the status of providers important to you

UC Care Provider directoryblueshieldca.com/uccareppo

Blue Shield Concierge 1-855-201-2087

24

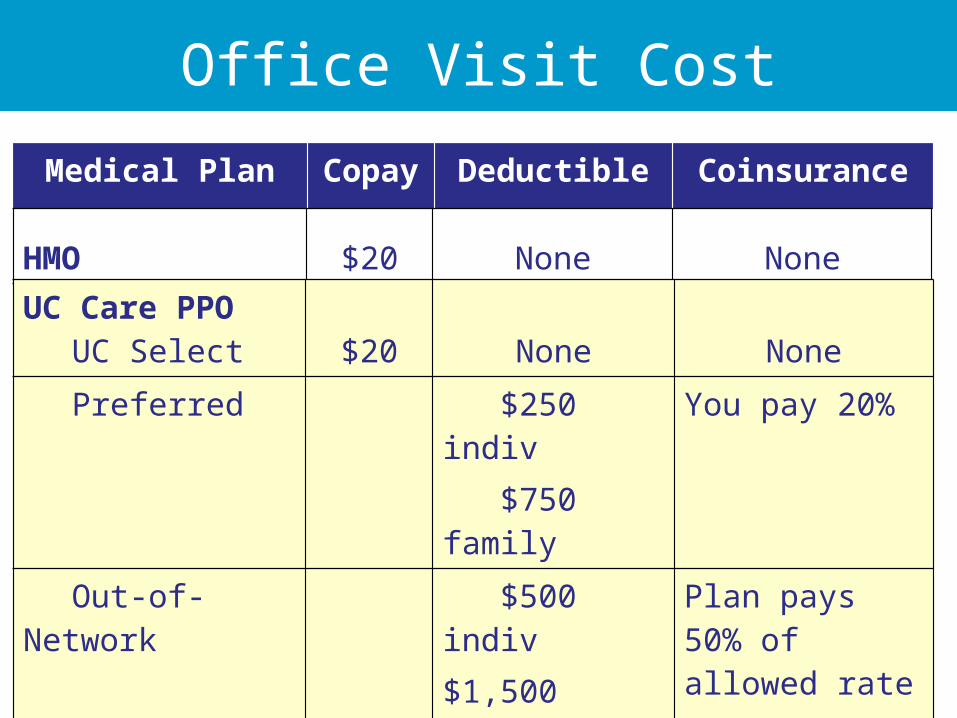

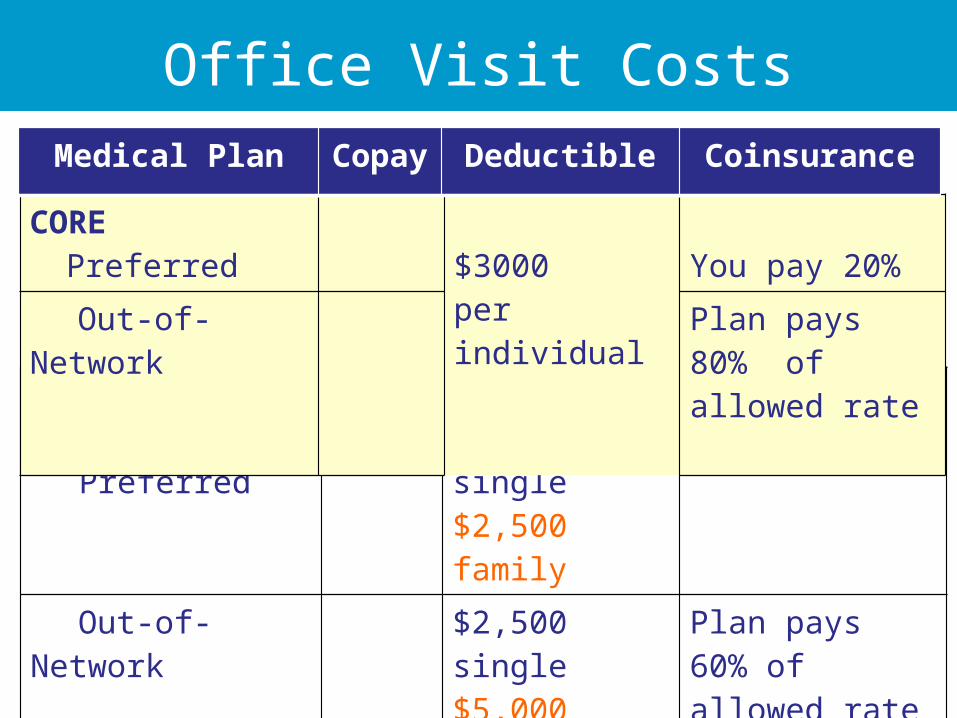

Office Visit Cost

Medical Plan Copay

Deductible Coinsurance

HMO $20 None None

UC Care PPOUC Select $20 None None

Preferred $250 indiv $750 family

You pay 20%

Out-of-Network

$500 indiv$1,500 family

Plan pays 50% of allowed rate

You pay balance

25

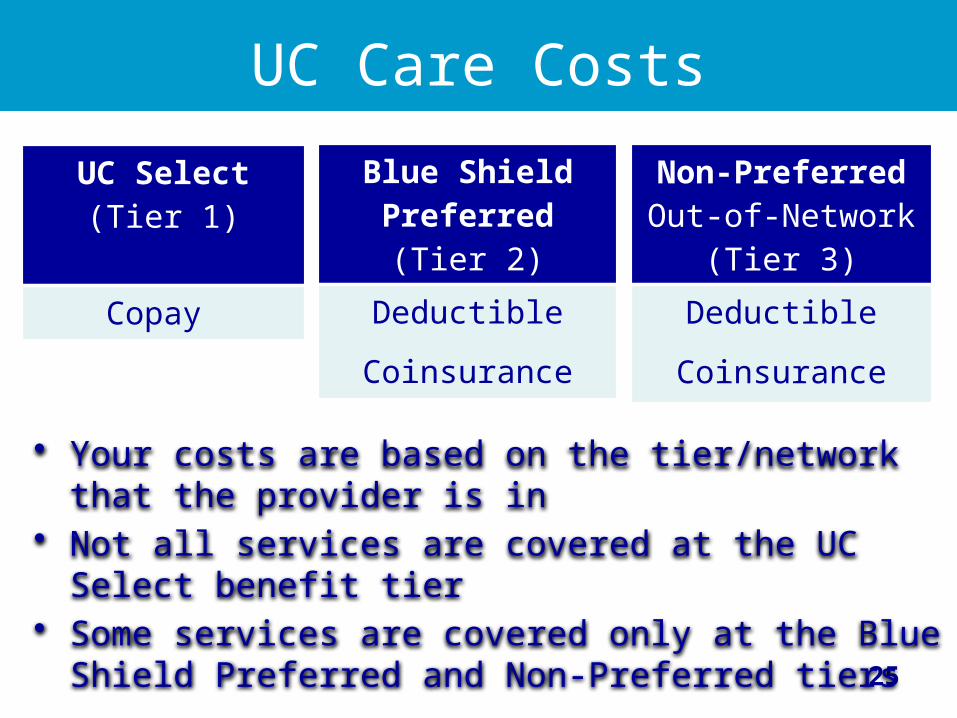

UC Care Costs

UC Select(Tier 1)

Copay

Blue ShieldPreferred

(Tier 2)

Deductible

Coinsurance

Non-PreferredOut-of-Network

(Tier 3)

Deductible

Coinsurance

• Your costs are based on the tier/network that the provider is in

• Not all services are covered at the UC Select benefit tier

• Some services are covered only at the Blue Shield Preferred and Non-Preferred tiers

26

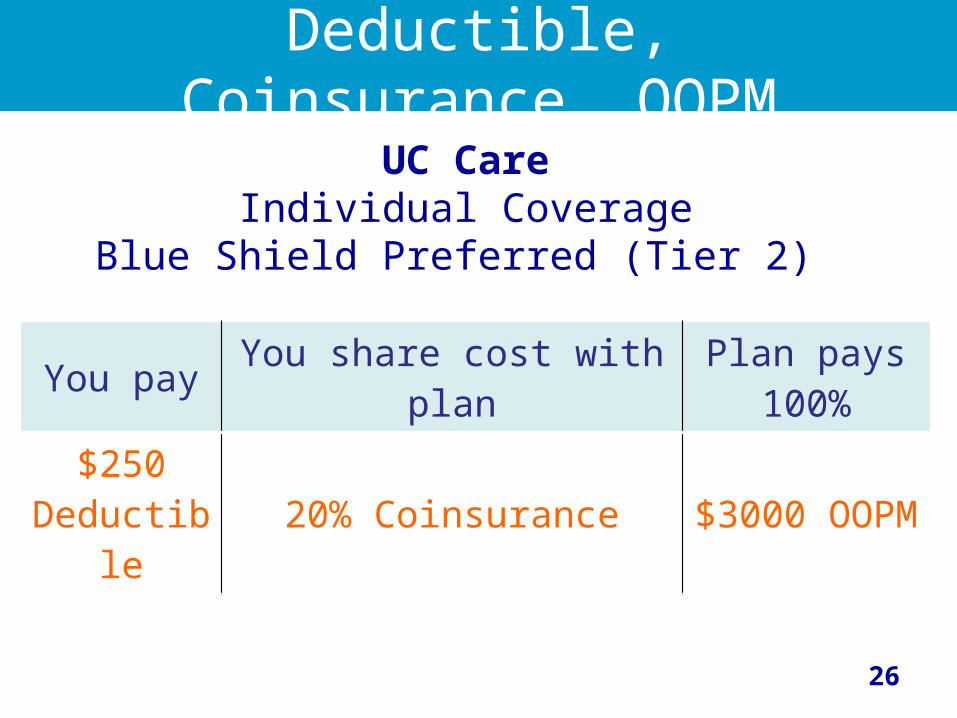

Deductible, Coinsurance, OOPM

You pay You share cost with plan

Plan pays100%

$250Deductibl

e20% Coinsurance $3000

OOPM

UC CareIndividual Coverage

Blue Shield Preferred (Tier 2)

27

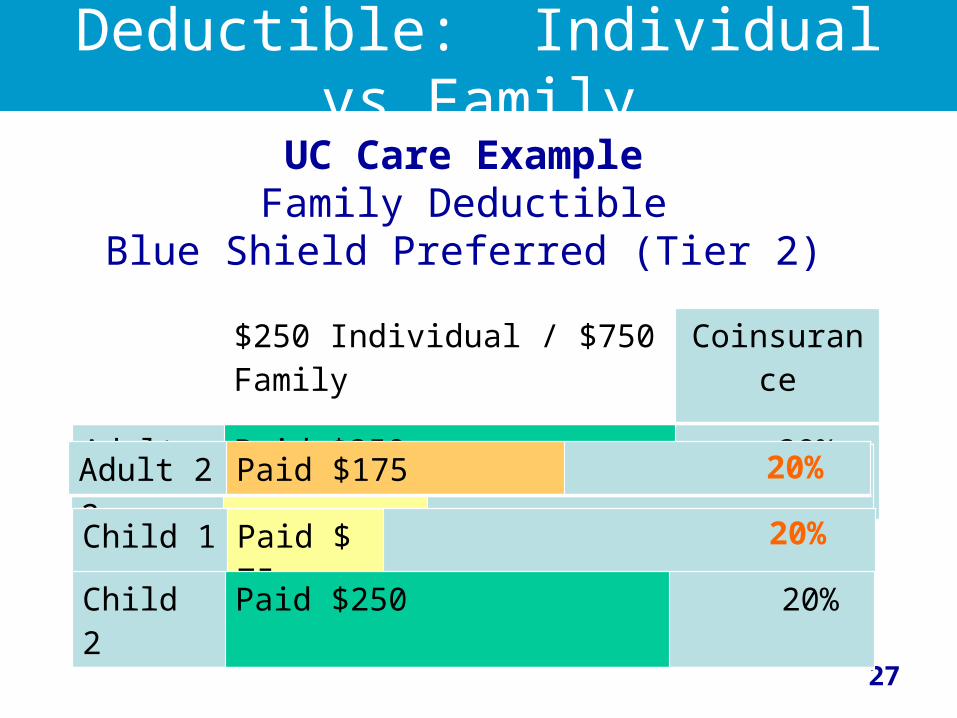

Deductible: Individual vs Family

$250 Individual / $750 Family

Coinsurance

Adult 1 Paid $250 20%Adult 2 Paid $100

Child 1 Paid $ 75

Child 2 Paid $250 20%

Adult 2 Paid $175 20%

20%

UC Care ExampleFamily Deductible

Blue Shield Preferred (Tier 2)

Office Visit Costs

28

Blue Shield HSP

Preferred$1,250 single$2,500 family

You pay 20%

Out-of-Network

$2,500 single$5,000 family

Plan pays 60% of allowed rate

Full family deductible must be met before plan shares cost

COREPreferred

$3000 per individual

You pay 20%

Out-of-Network

Plan pays 80% of allowed rate

Medical Plan Copay

Deductible Coinsurance

29

Deductible, Coinsurance, OOPM

You pay You share cost with plan

Plan pays100%

$1250Deductibl

e20% Coinsurance $4000

OOPM

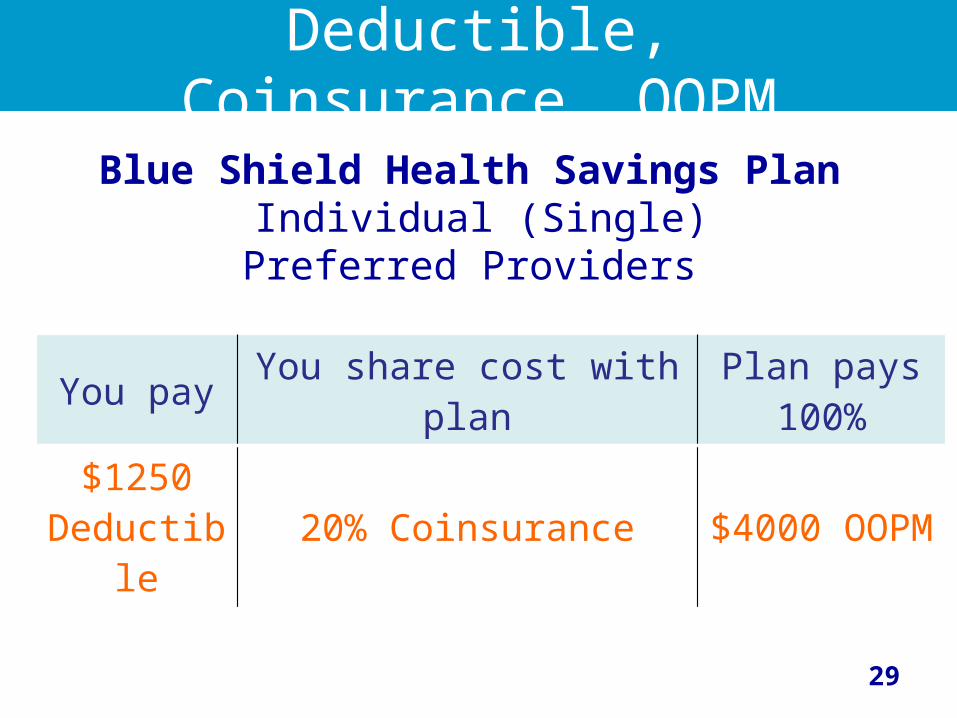

Blue Shield Health Savings Plan Individual (Single)

Preferred Providers

30

Deductible, Coinsurance, OOPM

You pay You share cost with plan

Plan pays100%

$2500Deductibl

e20% Coinsurance $6400

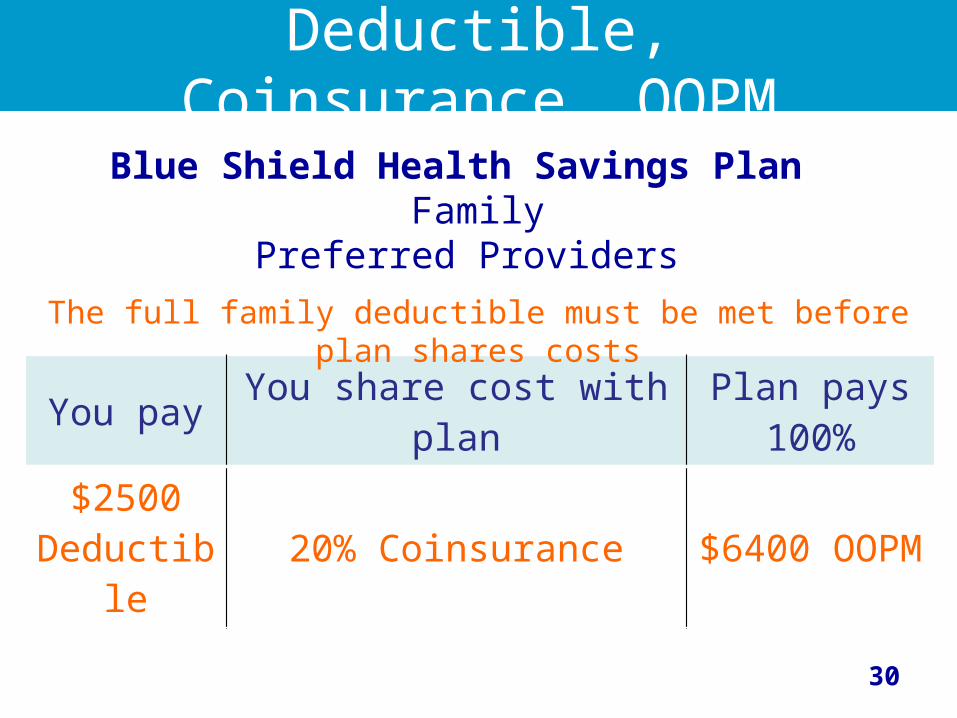

OOPM

Blue Shield Health Savings Plan Family

Preferred Providers

The full family deductible must be met before plan shares costs

31

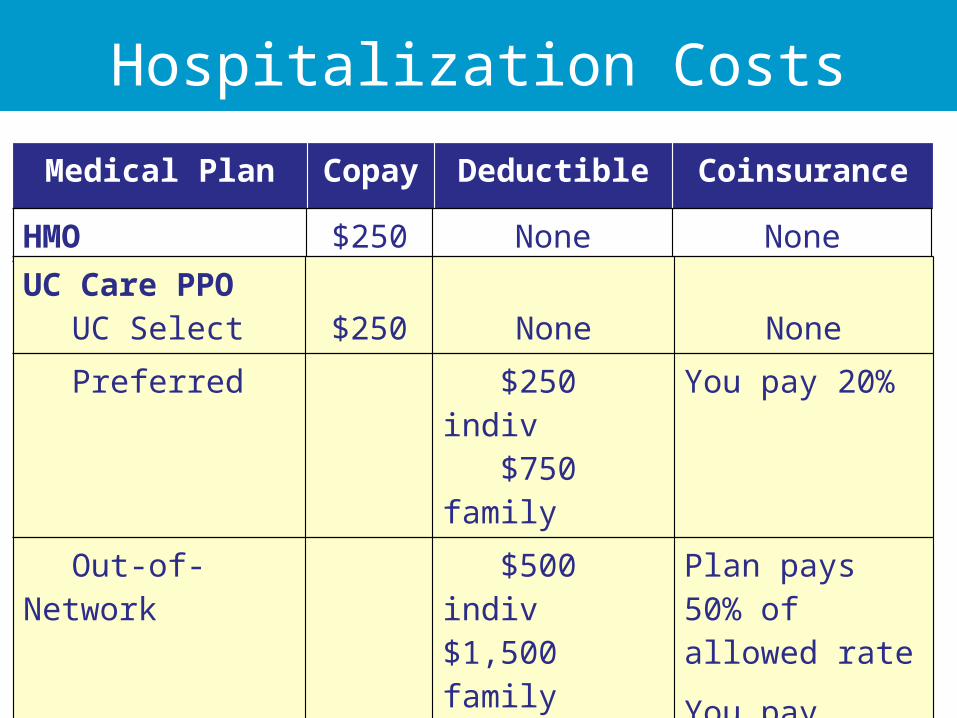

Hospitalization Costs

Medical Plan Copay

Deductible Coinsurance

HMO $250 None None

UC Care PPOUC Select $250 None None

Preferred $250 indiv $750 family

You pay 20%

Out-of-Network

$500 indiv$1,500 family

Plan pays 50% of allowed rate

You pay balance

Hospitalization Costs

32

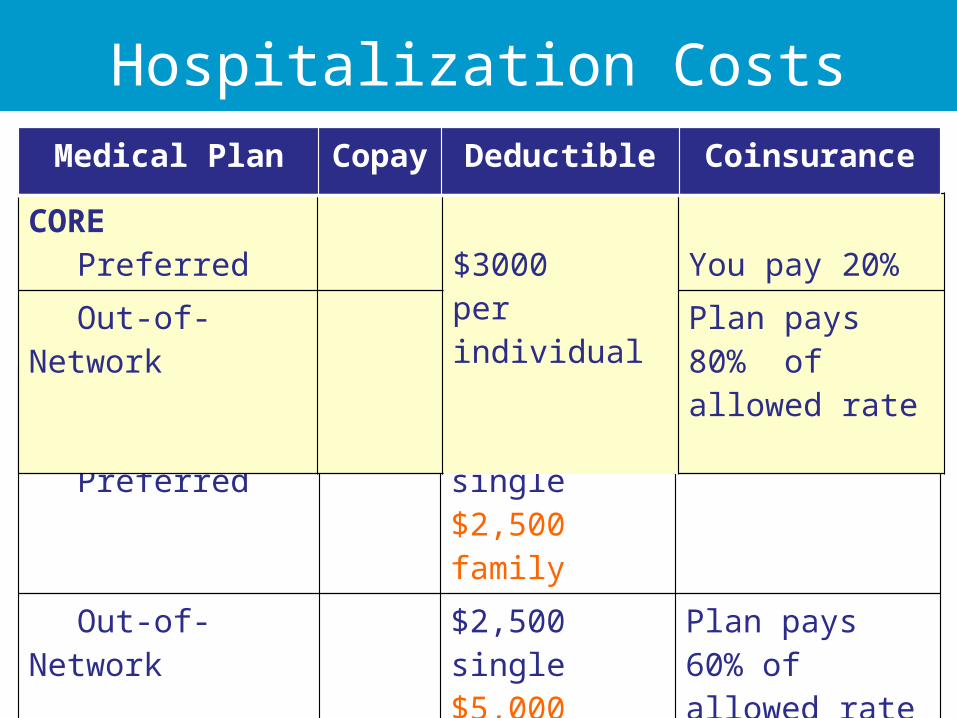

Blue Shield HSP

Preferred$1,250 single$2,500 family

You pay 20%

Out-of-Network

$2,500 single$5,000 family

Plan pays 60% of allowed rate

Full family deductible must be met before plan shares cost

COREPreferred

$3000 per individual

You pay 20%

Out-of-Network

Plan pays 80% of allowed rate

Medical Plan Copay

Deductible Coinsurance

33

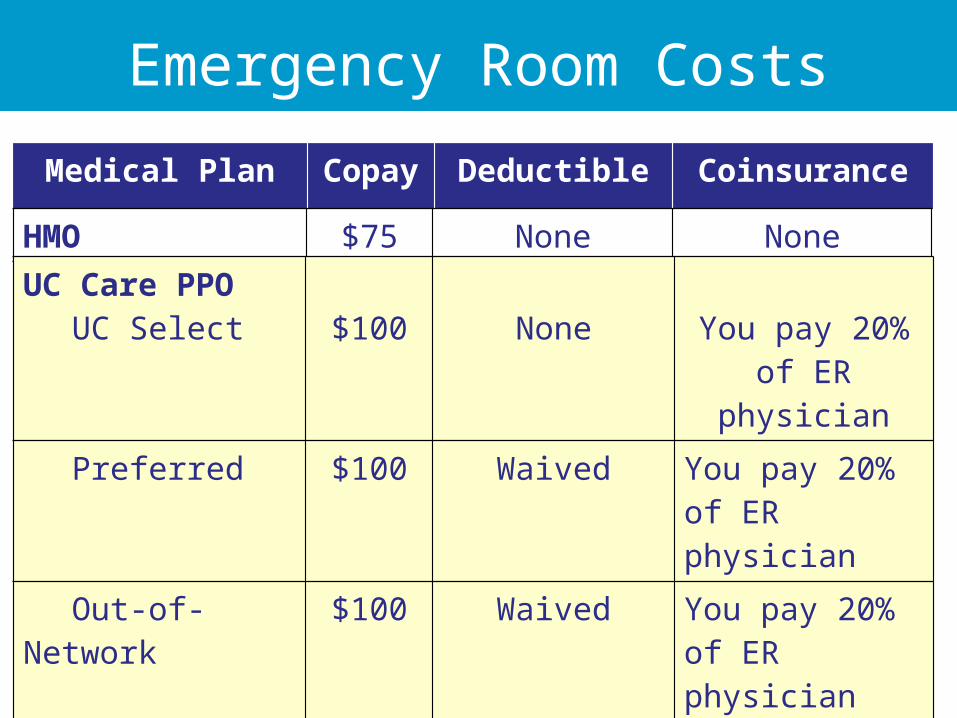

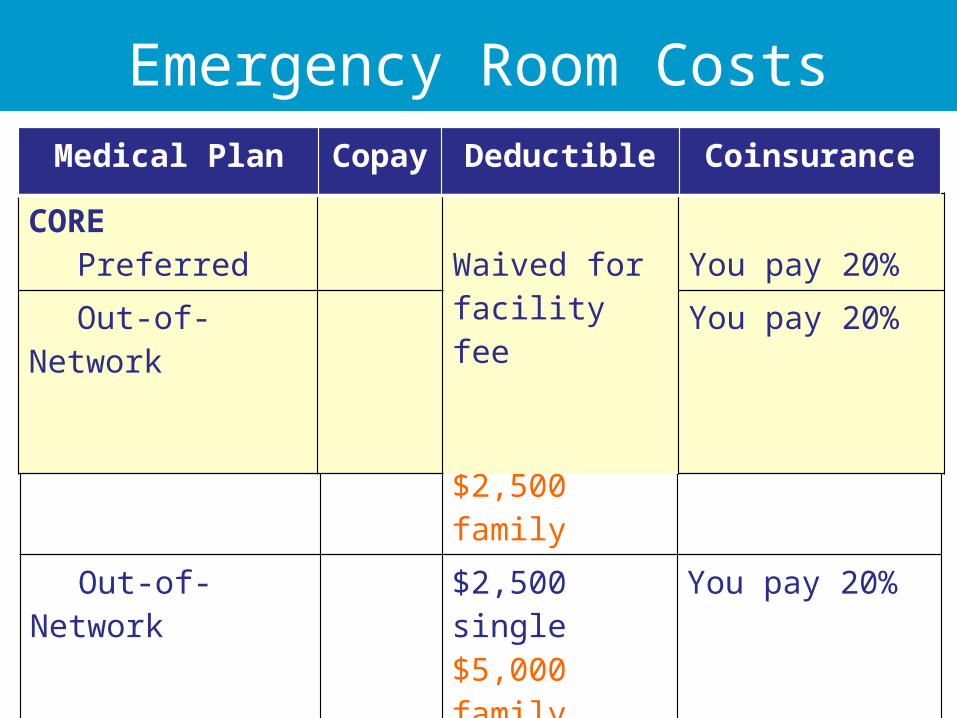

Emergency Room Costs

Medical Plan Copay

Deductible Coinsurance

HMO $75 None None

UC Care PPOUC Select $100 None You pay 20%

of ER physician

Preferred $100 Waived You pay 20% of ER physician

Out-of-Network

$100 Waived You pay 20% of ER physician

Emergency Room Costs

34

Blue Shield HSP

Preferred$1,250 single$2,500 family

You pay 20%

Out-of-Network

$2,500 single$5,000 family

You pay 20%

Full family deductible must be met before plan shares cost

COREPreferred

Waived for facility fee

You pay 20%

Out-of-Network

You pay 20%

Medical Plan Copay

Deductible Coinsurance

35

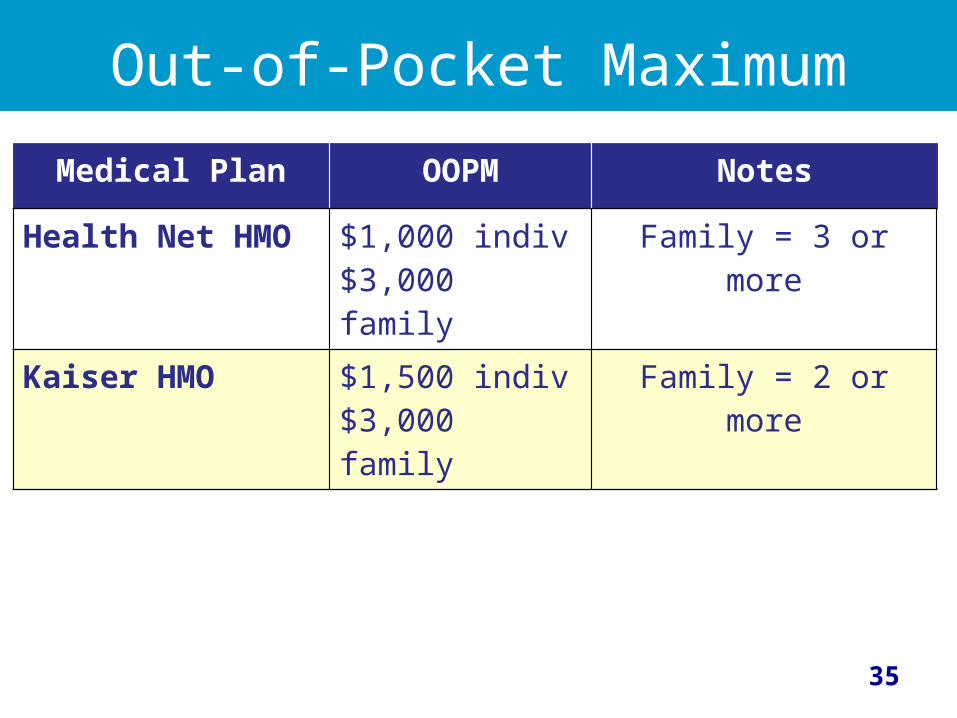

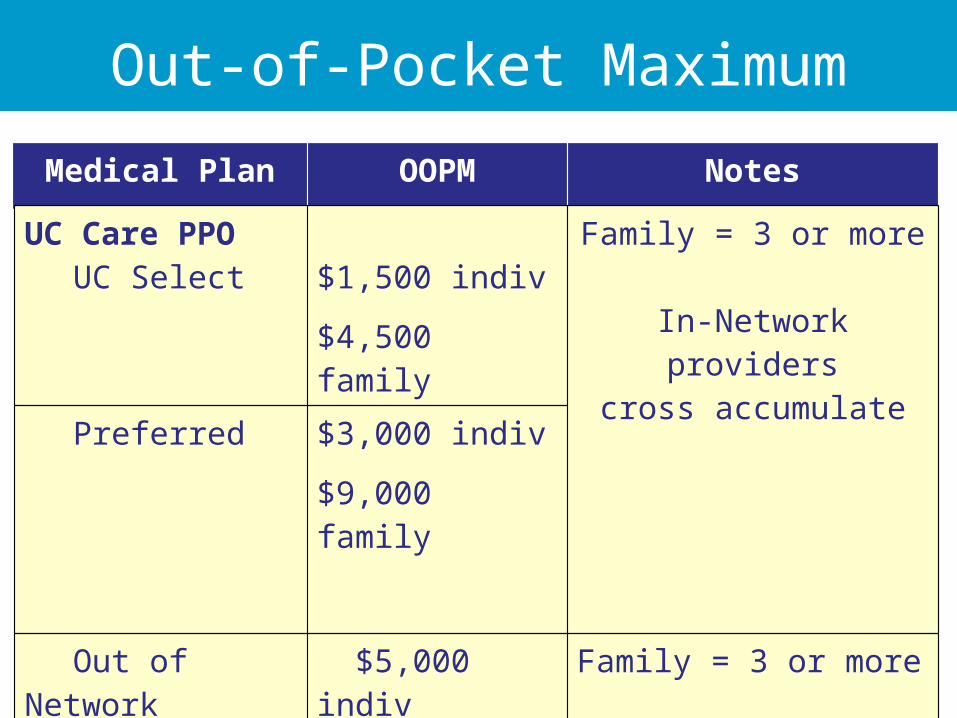

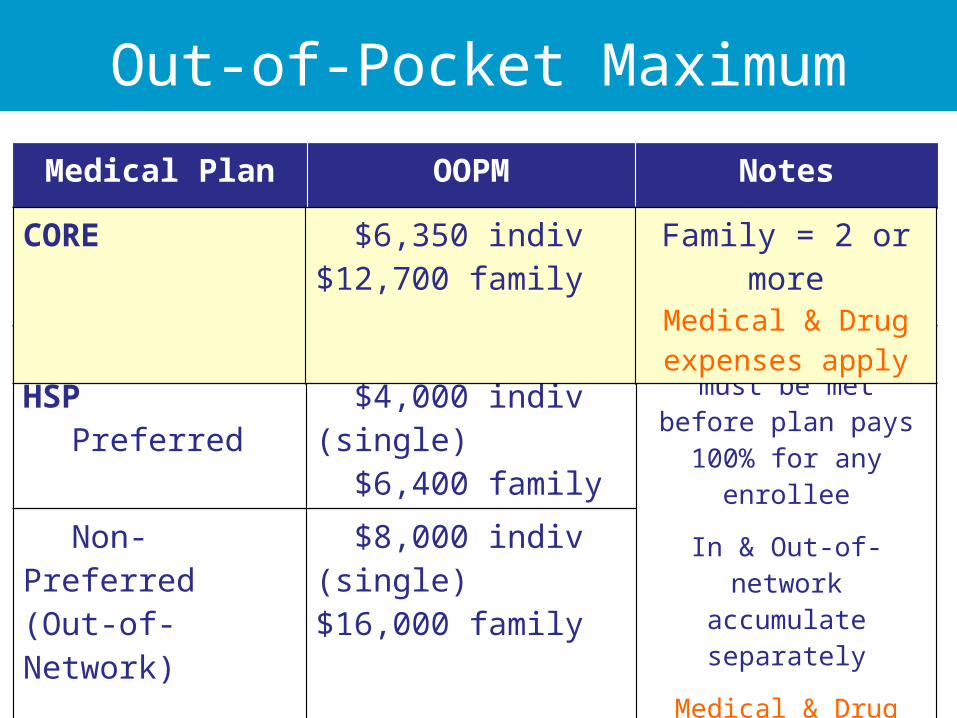

Out-of-Pocket Maximum

Medical Plan OOPM Notes

Health Net HMO $1,000 indiv$3,000 family

Family = 3 or more

Kaiser HMO $1,500 indiv$3,000 family

Family = 2 or more

36

Out-of-Pocket Maximum

Medical Plan OOPM Notes

UC Care PPOUC Select $1,500 indiv

$4,500 family

Family = 3 or more

In-Network providerscross accumulate

Preferred $3,000 indiv

$9,000 family

Out of Network

$5,000 indiv

$15,000 family

Family = 3 or more

Out-of-network accumulates separately

37

Out-of-Pocket Maximum

Medical Plan OOPM Notes

Blue Shield HSP

Preferred $4,000 indiv (single) $6,400 family

Full family OOPM must be met before plan pays 100% for

any enrollee

In & Out-of-network accumulate separately

Medical & Drug expenses apply

Non-Preferred(Out-of-Network)

$8,000 indiv (single)$16,000 family

CORE $6,350 indiv$12,700 family

Family = 2 or more

Medical & Drug expenses apply

38

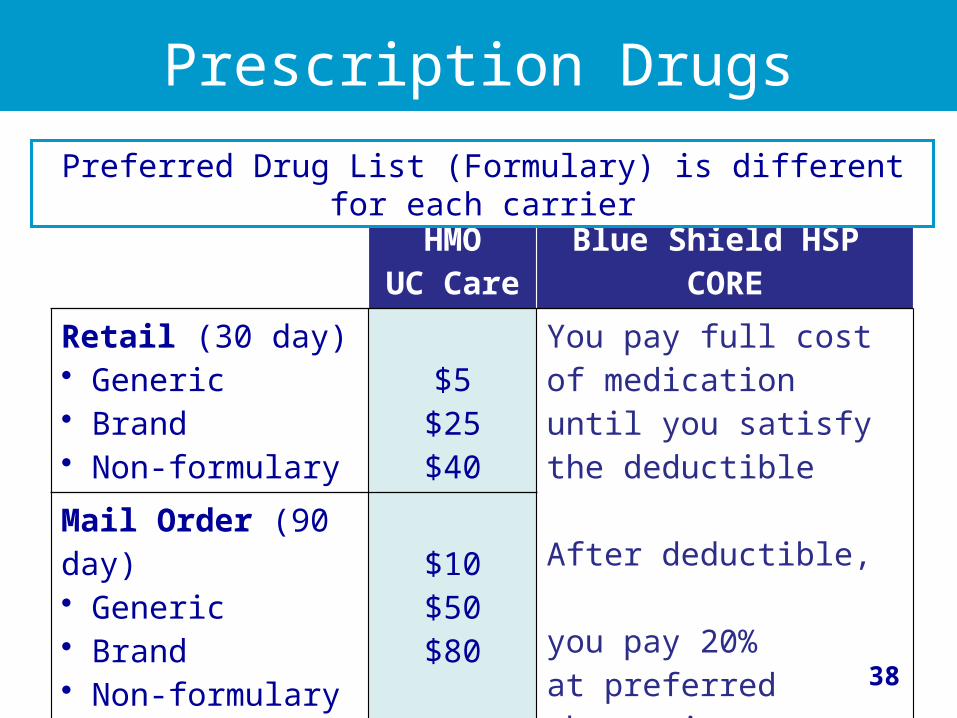

Prescription Drugs

HMOUC Care

Blue Shield HSP CORE

Retail (30 day)• Generic• Brand• Non-formulary

$5$25$40

You pay full cost of medication until you satisfy the deductible

After deductible, you pay 20% at preferred pharmacies

Mail Order (90 day) • Generic• Brand• Non-formulary

$10$50$80

Preferred Drug List (Formulary) is different for each carrier

39

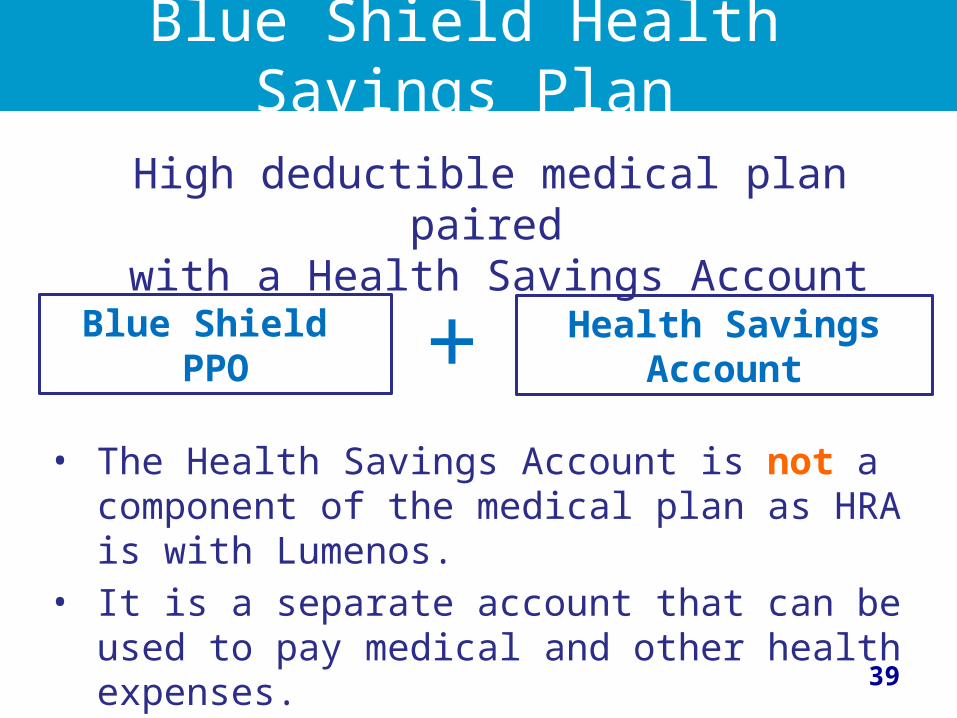

Blue Shield Health Savings Plan

Blue Shield PPO +

High deductible medical plan paired with a Health Savings Account

Health Savings Account

• The Health Savings Account is not a component of the medical plan as HRA is with Lumenos.

• It is a separate account that can be used to pay medical and other health expenses.

40

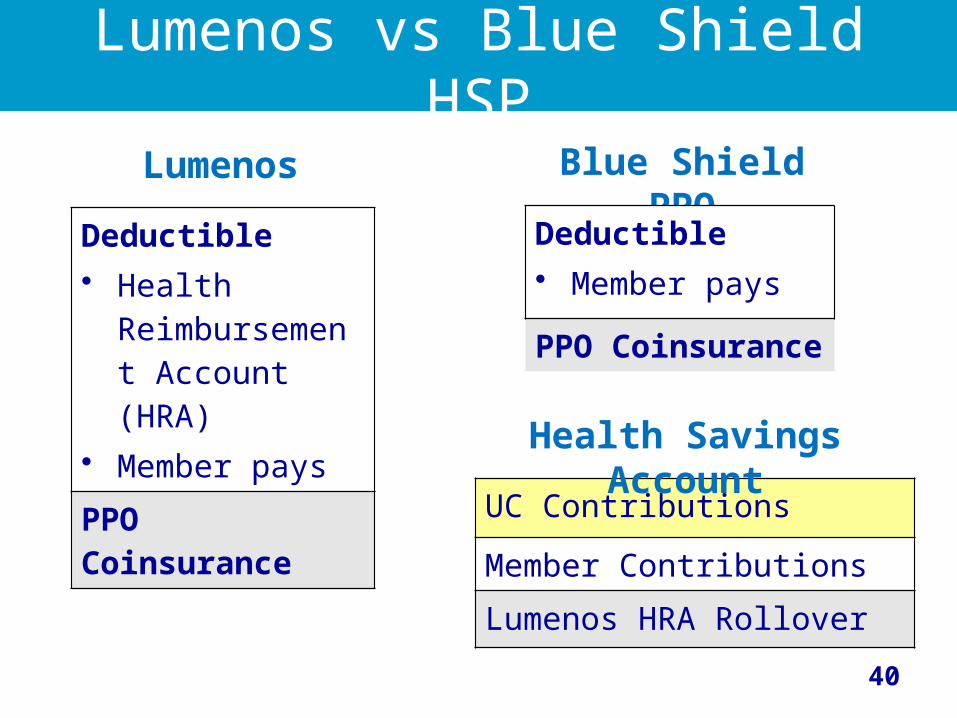

Lumenos vs Blue Shield HSP

Deductible Health

Reimbursement Account (HRA)

Member pays

PPO Coinsurance

Lumenos Blue Shield PPO

Deductible Member pays

PPO Coinsurance

UC Contributions

Member Contributions

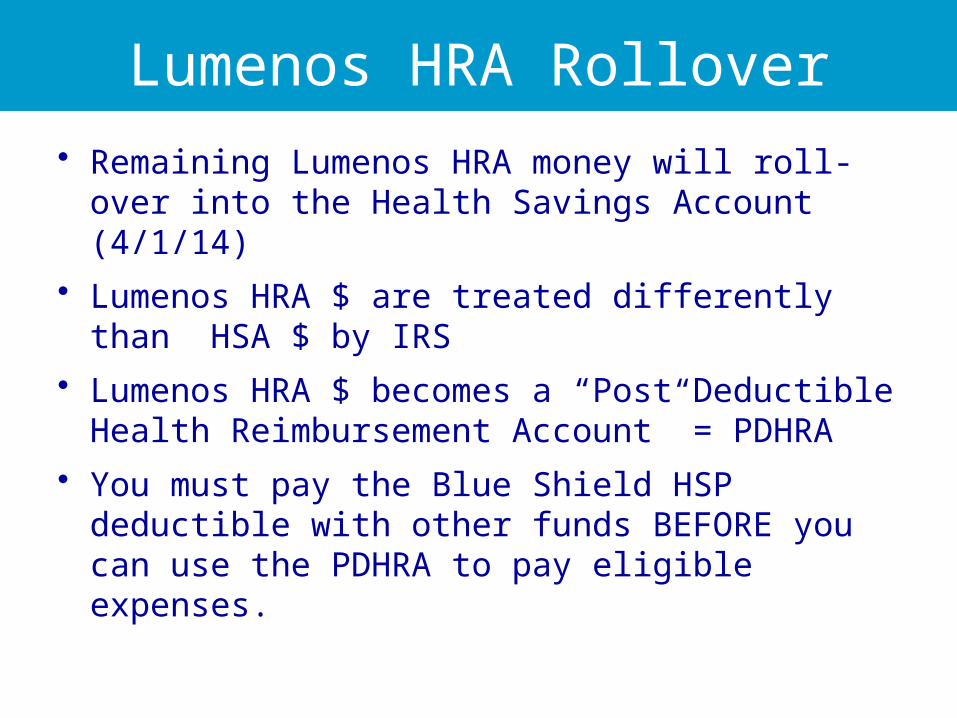

Lumenos HRA Rollover

Health Savings Account

Lumenos HRA Rollover• Remaining Lumenos HRA money will roll-over

into the Health Savings Account (4/1/14)• Lumenos HRA $ are treated differently than

HSA $ by IRS• Lumenos HRA $ becomes a “Post Deductible

Health Reimbursement Account” = PDHRA• You must pay the Blue Shield HSP deductible

with other funds BEFORE you can use the PDHRA to pay eligible expenses.

42

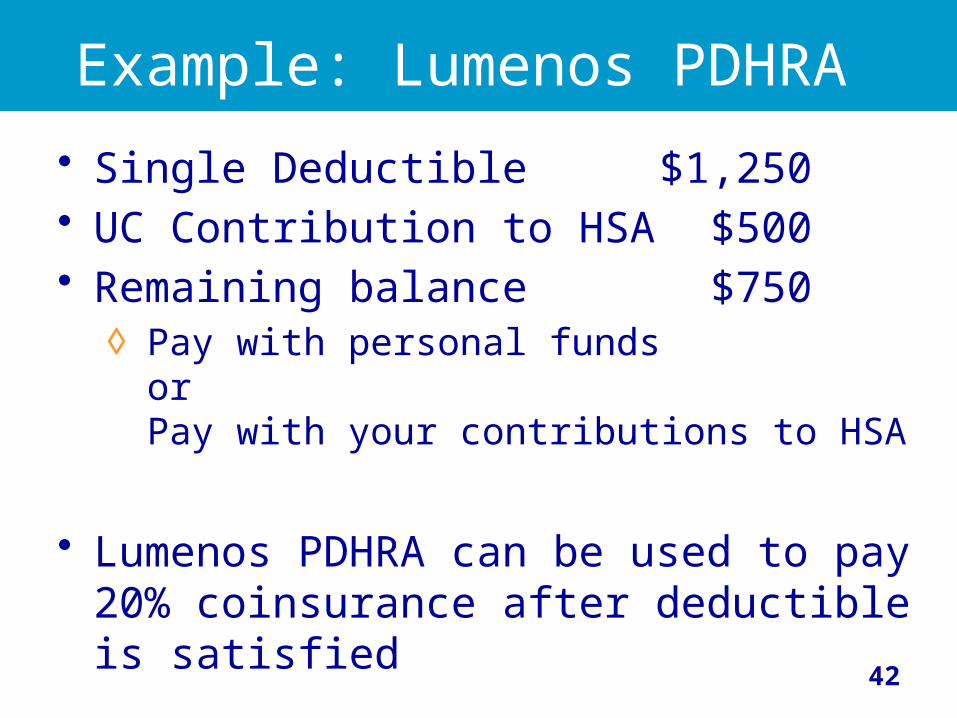

Example: Lumenos PDHRA

• Single Deductible $1,250• UC Contribution to HSA $500• Remaining balance $750

◊ Pay with personal fundsorPay with your contributions to HSA

• Lumenos PDHRA can be used to pay 20% coinsurance after deductible is satisfied

43

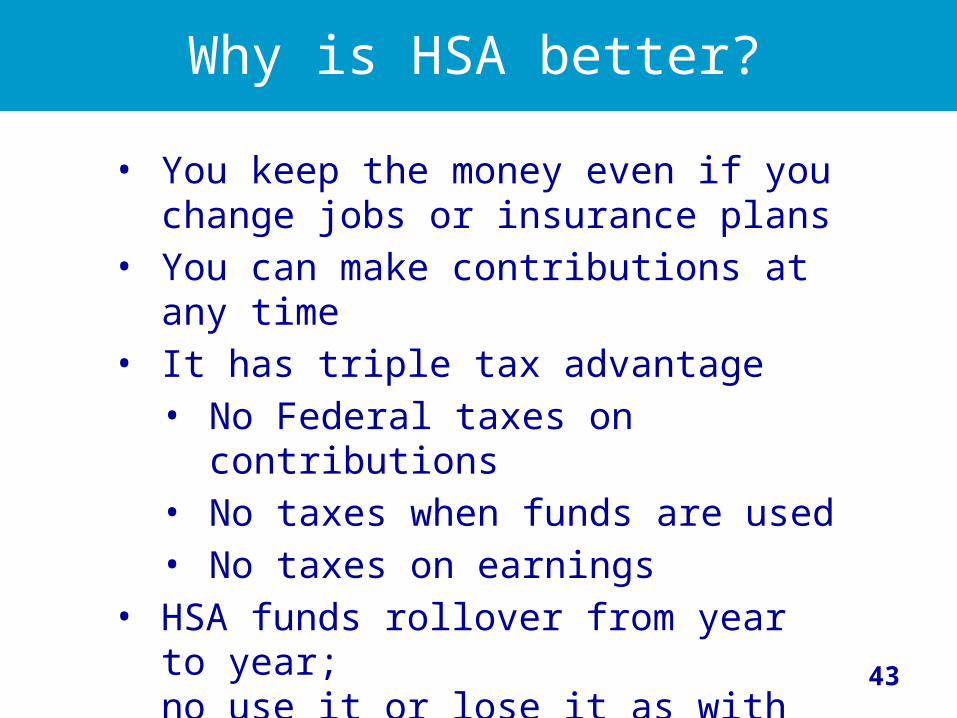

Why is HSA better?

• You keep the money even if you change jobs or insurance plans

• You can make contributions at any time

• It has triple tax advantage • No Federal taxes on contributions • No taxes when funds are used• No taxes on earnings

• HSA funds rollover from year to year; no use it or lose it as with Health FSA

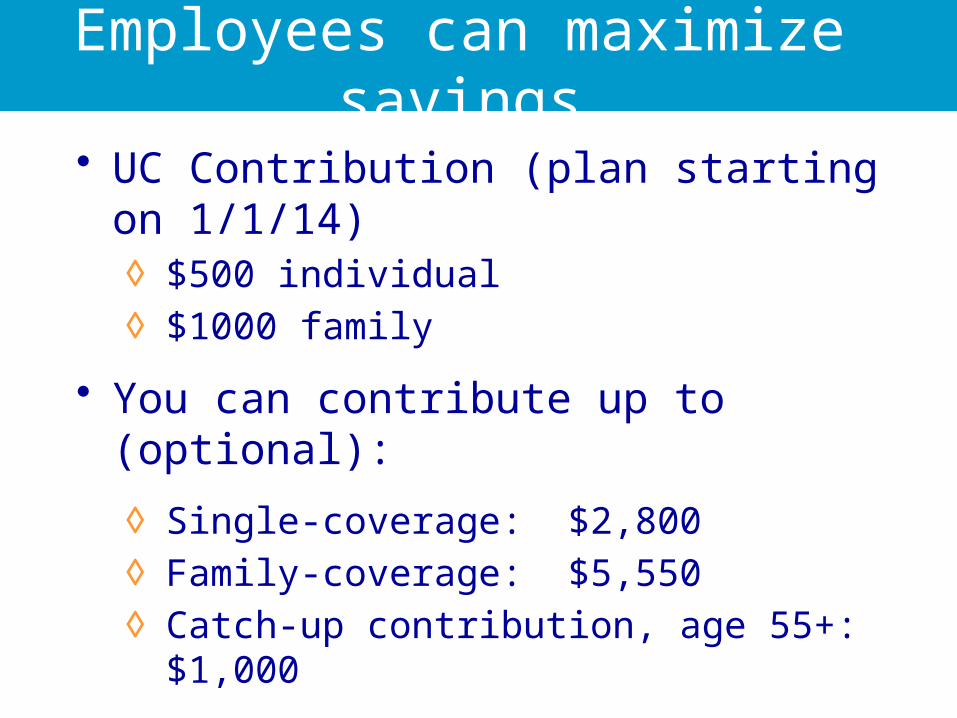

Employees can maximize savings

• UC Contribution (plan starting on 1/1/14) ◊ $500 individual ◊ $1000 family

• You can contribute up to (optional):

◊ Single-coverage: $2,800◊ Family-coverage: $5,550◊ Catch-up contribution, age 55+:

$1,000

Tip: Contribute the money you would have put in your Health FSA.

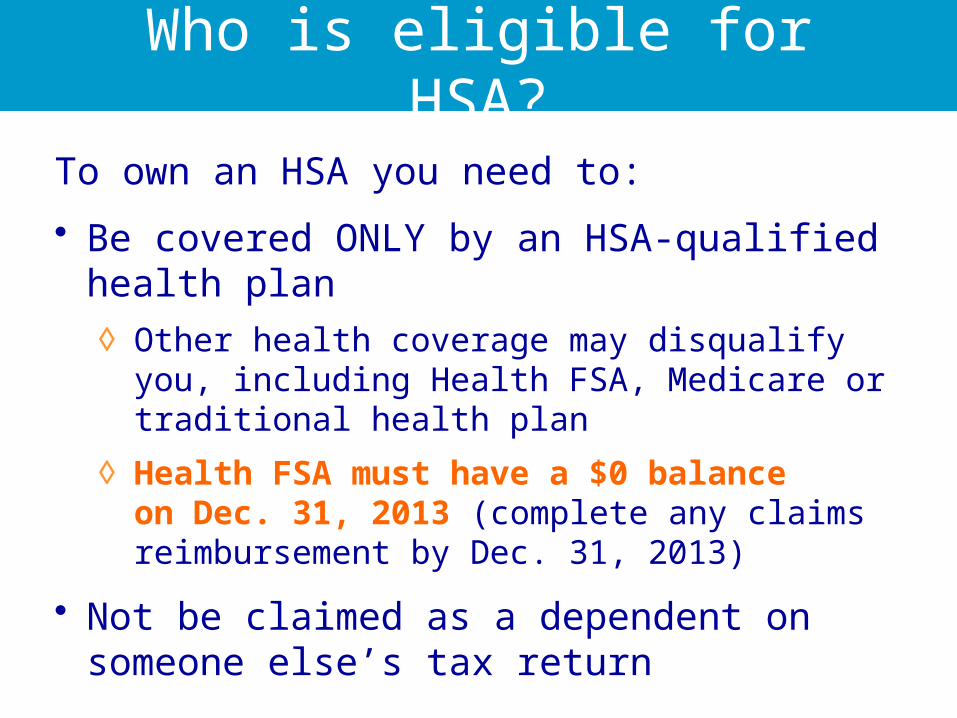

Who is eligible for HSA?

To own an HSA you need to:

• Be covered ONLY by an HSA-qualified health plan◊ Other health coverage may disqualify you,

including Health FSA, Medicare or traditional health plan

◊ Health FSA must have a $0 balance on Dec. 31, 2013 (complete any claims reimbursement by Dec. 31, 2013)

• Not be claimed as a dependent on someone else’s tax return

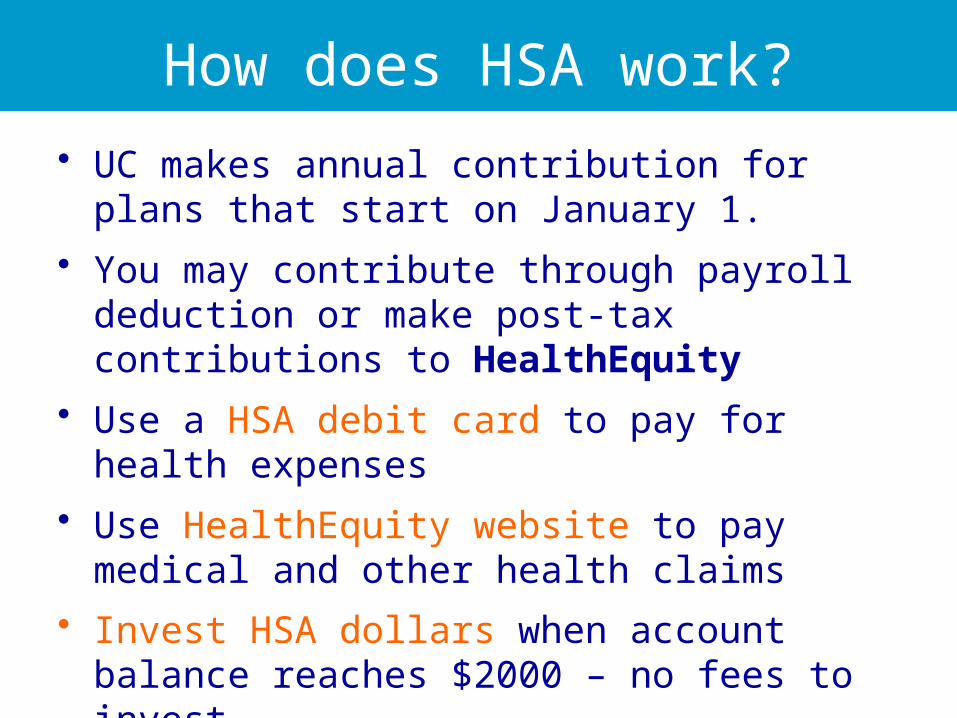

How does HSA work?

• UC makes annual contribution for plans that start on January 1.

• You may contribute through payroll deduction or make post-tax contributions to HealthEquity

• Use a HSA debit card to pay for health expenses

• Use HealthEquity website to pay medical and other health claims

• Invest HSA dollars when account balance reaches $2000 – no fees to invest

47

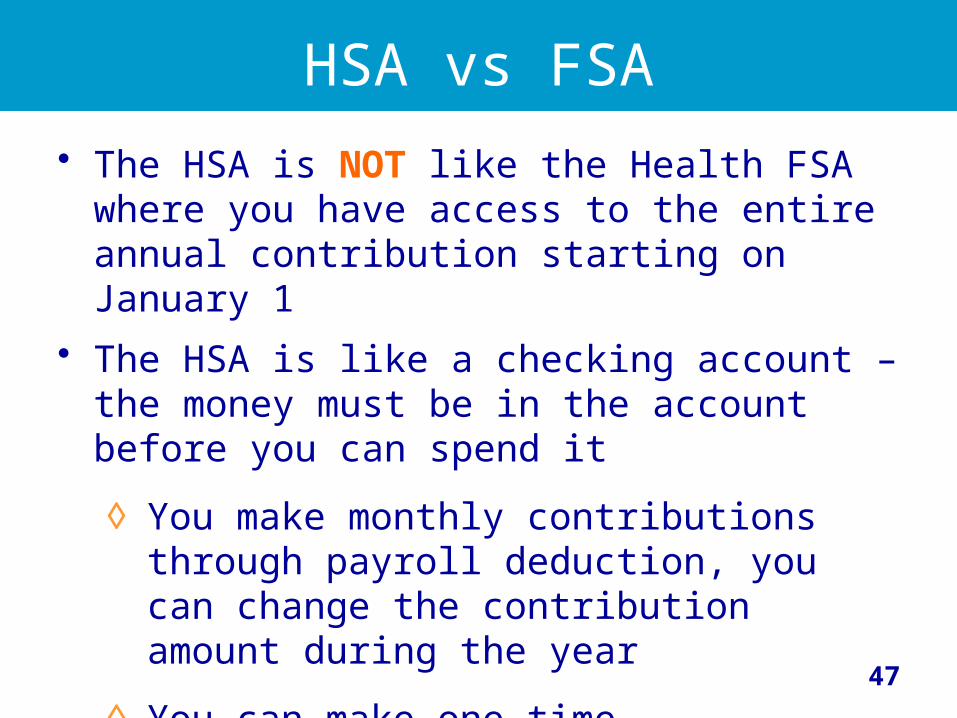

HSA vs FSA

• The HSA is NOT like the Health FSA where you have access to the entire annual contribution starting on January 1

• The HSA is like a checking account – the money must be in the account before you can spend it

◊ You make monthly contributions through payroll deduction, you can change the contribution amount during the year

◊ You can make one time contributions through Health Equity

48

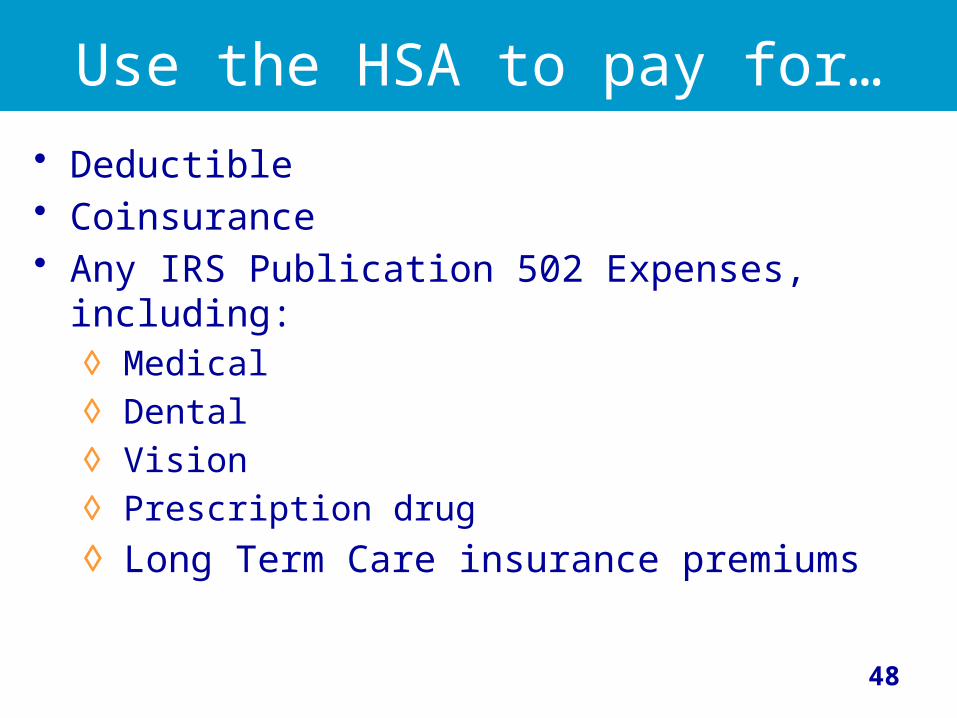

Use the HSA to pay for…

• Deductible• Coinsurance• Any IRS Publication 502 Expenses, including:

◊ Medical◊ Dental◊ Vision◊ Prescription drug◊ Long Term Care insurance premiums

49

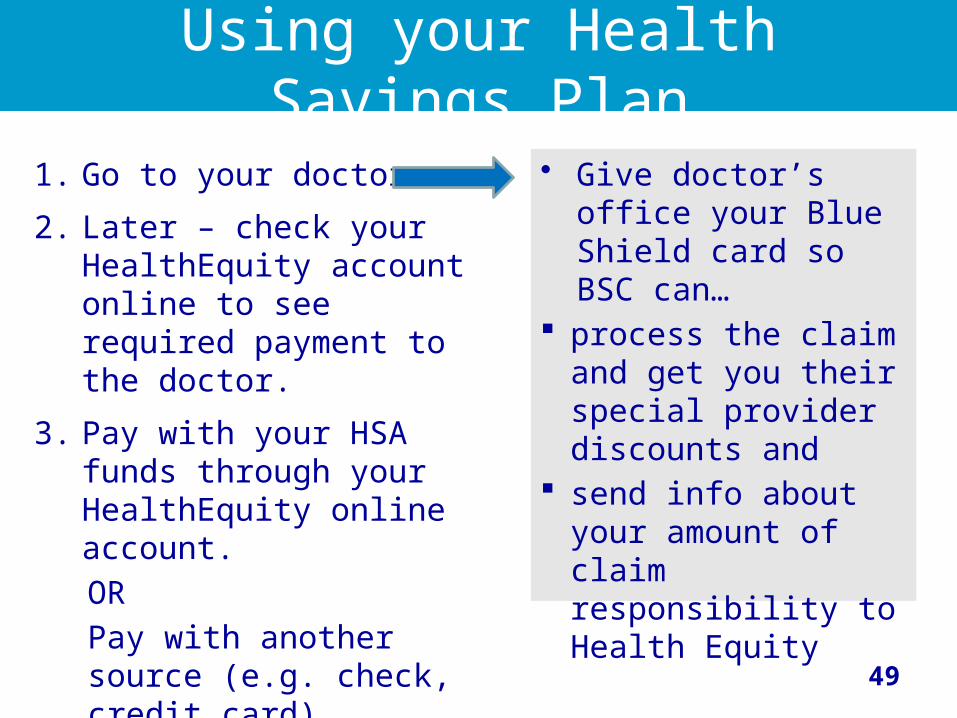

Using your Health Savings Plan

1. Go to your doctor.

2. Later – check your HealthEquity account online to see required payment to the doctor.

3. Pay with your HSA funds through your HealthEquity online account.ORPay with another source (e.g. check, credit card)

• Give doctor’s office your Blue Shield card so BSC can…

process the claim and get you their special provider discounts and

send info about your amount of claim responsibility to Health Equity

For more information

HealthEquity Member Services is available every hour of every day

Call the Blue Shield/UC dedicated line 1.855.201.8375

say“Health Savings Account”

www.healthequity.com/ed/uc

www.blueshieldca.com/uc

51

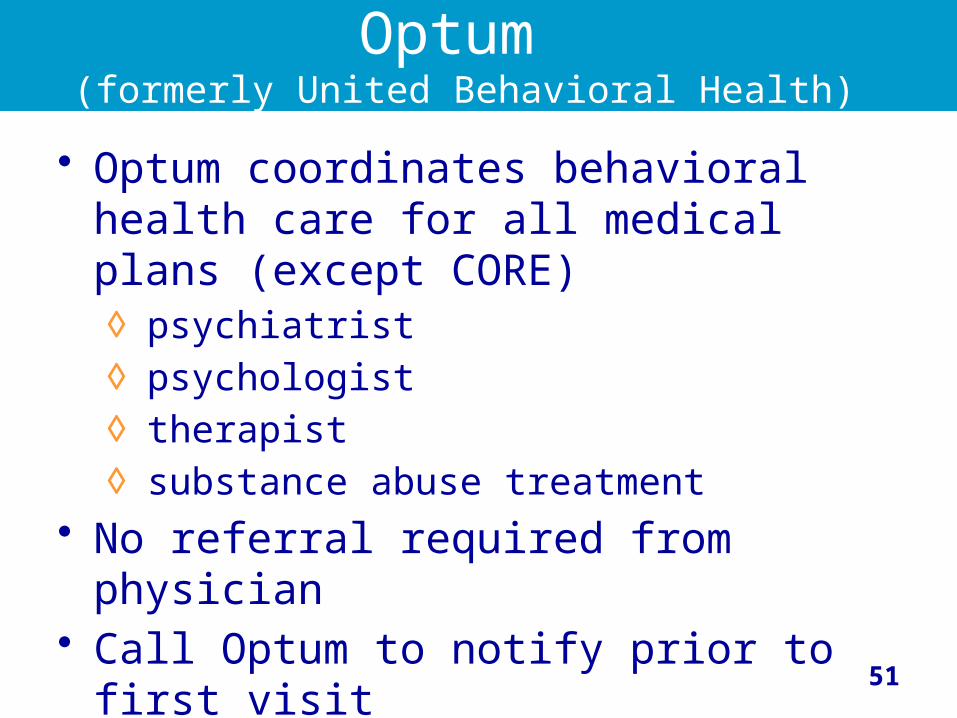

Optum (formerly United Behavioral Health)

• Optum coordinates behavioral health care for all medical plans (except CORE)◊ psychiatrist◊ psychologist◊ therapist◊ substance abuse treatment

• No referral required from physician• Call Optum to notify prior to first visit

52

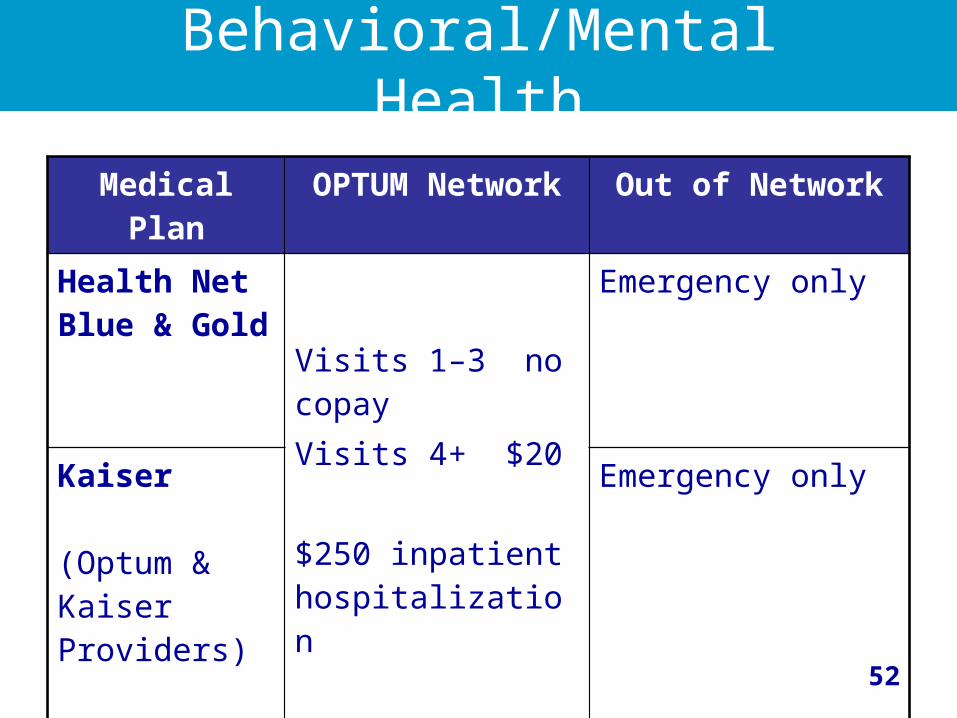

Behavioral/Mental Health

Medical Plan

OPTUM Network

Out of Network

Health Net Blue & Gold

Visits 1–3 no copayVisits 4+ $20

$250 inpatient hospitalization

Emergency only

Kaiser

(Optum & Kaiser Providers)

Emergency only

53

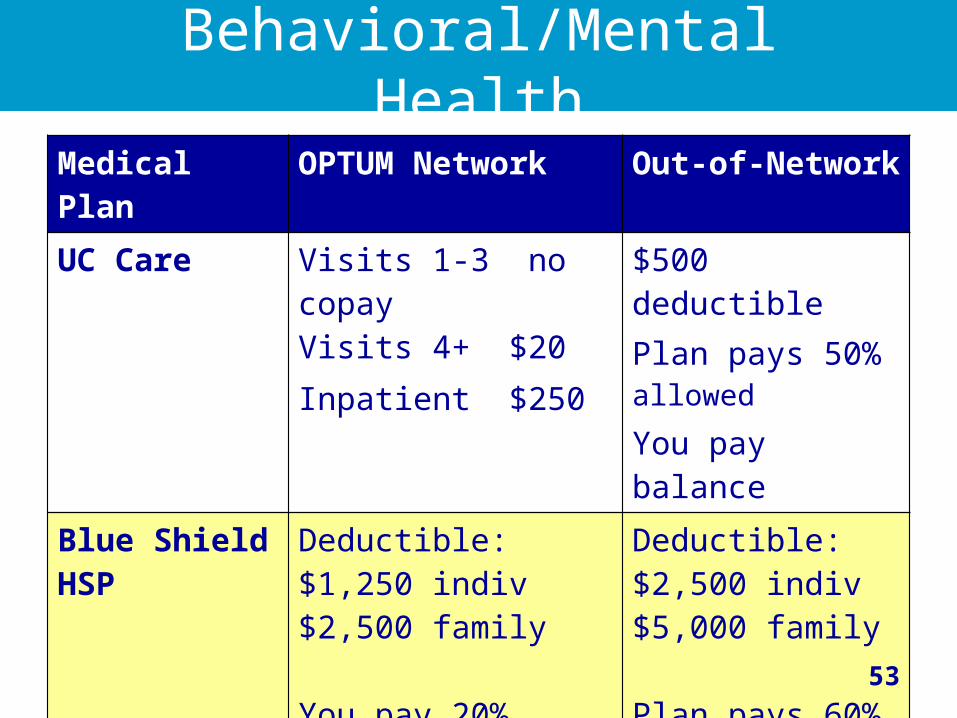

Behavioral/Mental HealthMedical Plan

OPTUM Network Out-of-Network

UC Care Visits 1-3 no copayVisits 4+ $20Inpatient $250

$500 deductiblePlan pays 50% allowed

You pay balance

Blue Shield HSP

Deductible:$1,250 indiv $2,500 family

You pay 20%

Deductible:$2,500 indiv$5,000 family

Plan pays 60% allowedYou pay balance

54

Behavioral/Mental Health

Medical Plan

Blue Shield Network

Out of Network

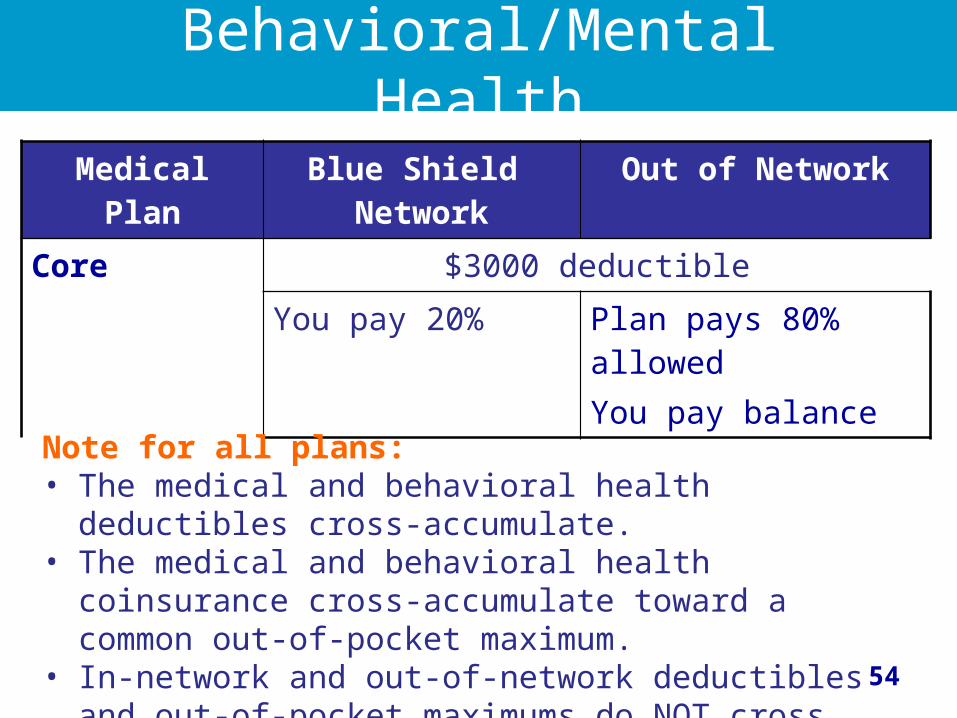

Core $3000 deductible

You pay 20% Plan pays 80% allowedYou pay balance

Note for all plans:• The medical and behavioral health deductibles cross-

accumulate.• The medical and behavioral health coinsurance cross-

accumulate toward a common out-of-pocket maximum.• In-network and out-of-network deductibles and out-of-

pocket maximums do NOT cross accumulate.

55

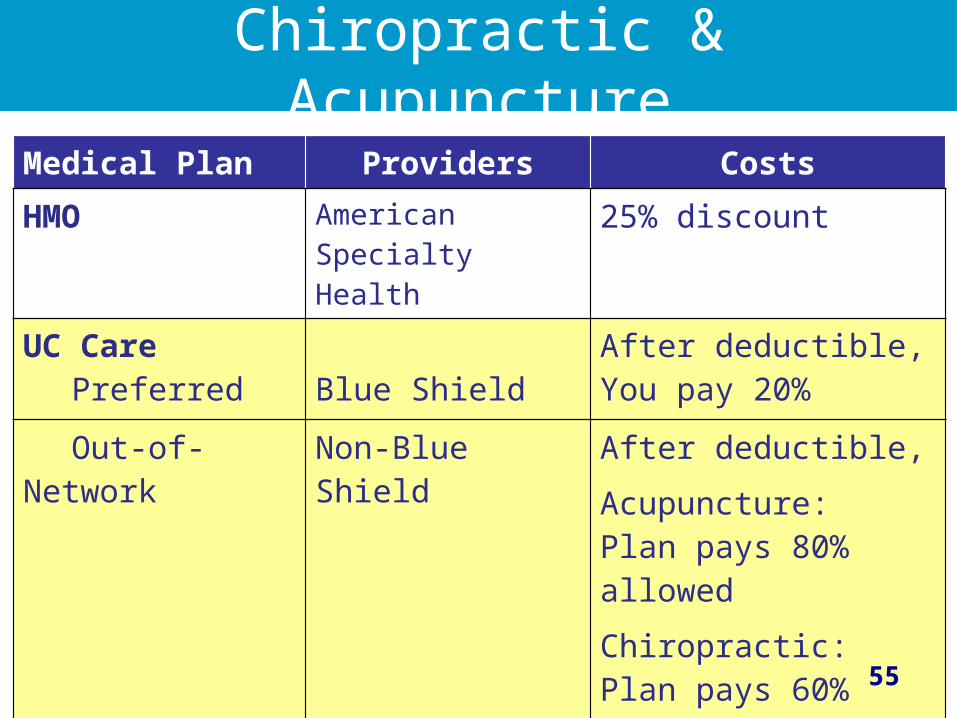

Chiropractic & AcupunctureMedical Plan Providers Costs

HMO American Specialty Health

25% discount

UC Care Preferred Blue Shield

After deductible,You pay 20%

Out-of-Network

Non-Blue Shield After deductible,

Acupuncture:Plan pays 80% allowed

Chiropractic:Plan pays 60% allowed

Note: Benefit is limited to 24 visits per calendar year combined for Acupuncture and Chiropractic visits

56

Chiropractic & AcupunctureMedical Plan Providers Costs

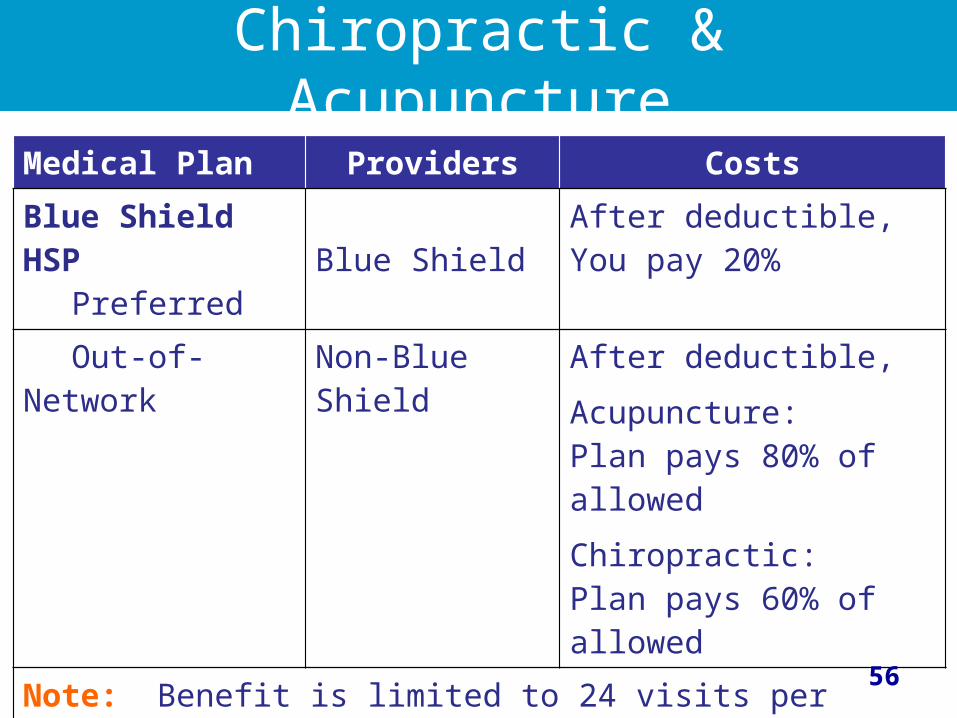

Blue Shield HSP

PreferredBlue Shield

After deductible,You pay 20%

Out-of-Network

Non-Blue Shield

After deductible,

Acupuncture:Plan pays 80% of allowed

Chiropractic:Plan pays 60% of allowed

Note: Benefit is limited to 24 visits per calendar year combined for Acupuncture and Chiropractic visits

57

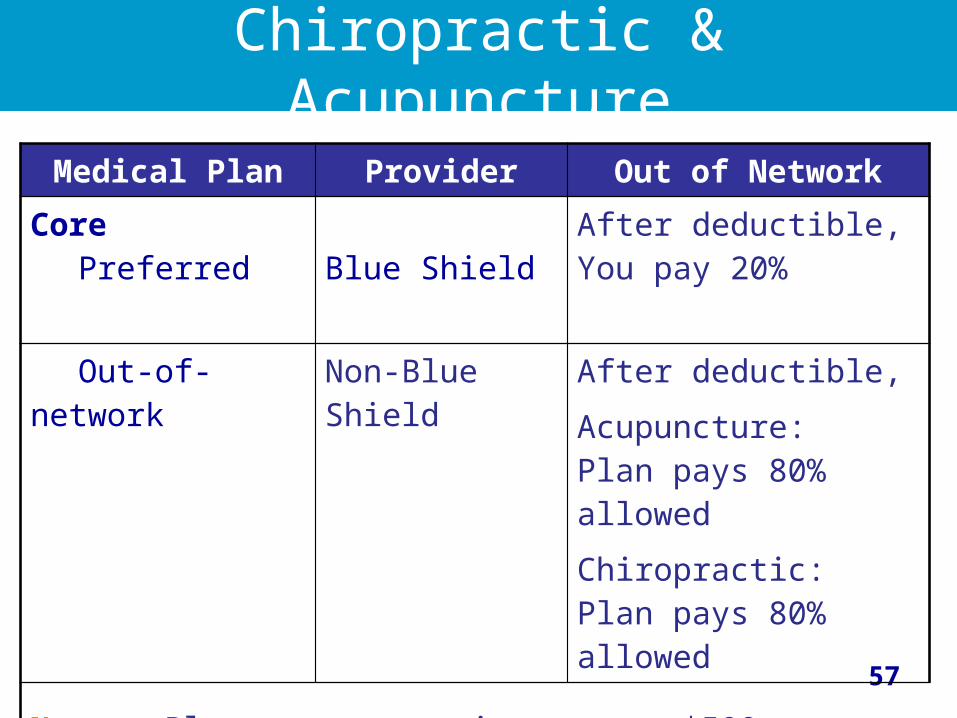

Chiropractic & Acupuncture

Medical Plan Provider Out of Network

CorePreferred Blue Shield

After deductible,You pay 20%

Out-of-network

Non-Blue Shield

After deductible,

Acupuncture:Plan pays 80% allowed

Chiropractic:Plan pays 80% allowed

Note: Plan payment maximum up to $500 per calendar year

58

http://atyourservice.ucop.edu/oe

• Resources◊ Plan contacts◊ Plan rates

• Medical Plans◊ Benefit summaries◊ Links to plan websites◊ Links to provider directories

• Other plans◊ Dental, vision, FSA

59