1-1 Accounting, Fifth Edition 1 Fall 2015 INTRODUCTION TO FINANCIAL STATEMENTS.

27

1-1 Accounting, Fifth Edition 1 Fall 2015 INTRODUCTION TO FINANCIAL STATEMENTS

-

Upload

easter-marsh -

Category

Documents

-

view

219 -

download

2

Transcript of 1-1 Accounting, Fifth Edition 1 Fall 2015 INTRODUCTION TO FINANCIAL STATEMENTS.

1-1 Accounting, Fifth Edition

1Fall 2015

INTRODUCTION TO FINANCIAL STATEMENTS

1-2

Forms of Business OrganizationForms of Business OrganizationForms of Business OrganizationForms of Business Organization

1-3

Users and Uses of Financial InformationUsers and Uses of Financial InformationUsers and Uses of Financial InformationUsers and Uses of Financial Information

LO 2

Internal Users

1-4

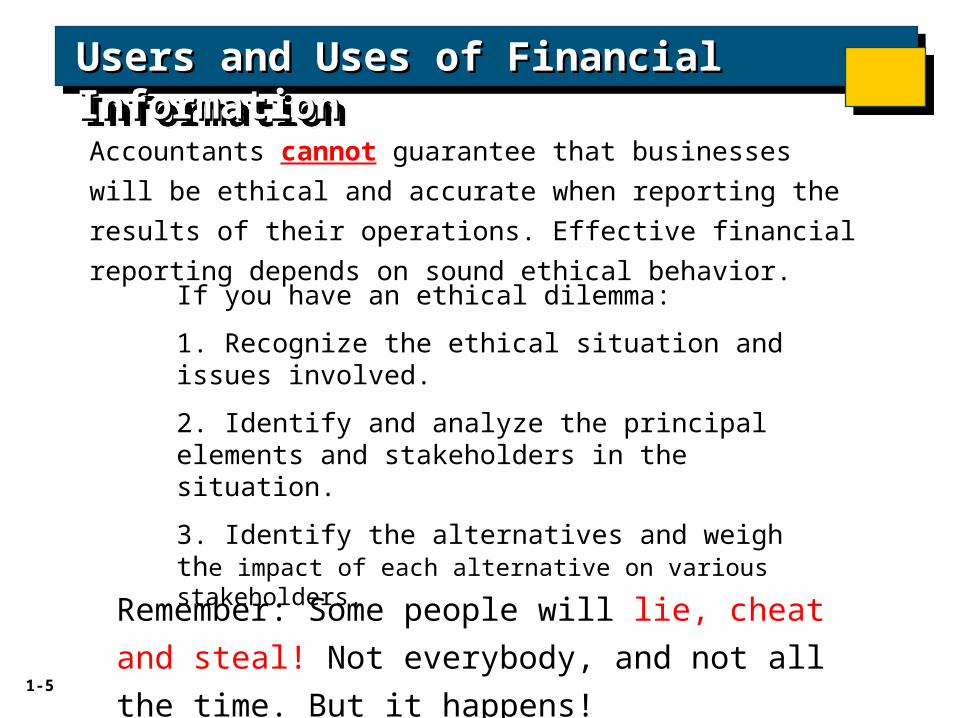

Users and Uses of Financial InformationUsers and Uses of Financial InformationUsers and Uses of Financial InformationUsers and Uses of Financial Information

LO 2

External Users

Regulatory Agencies How much does Lowes or Walmart owe the IRS?

1-5

Users and Uses of Financial InformationUsers and Uses of Financial InformationUsers and Uses of Financial InformationUsers and Uses of Financial Information

Remember: Some people will lie, cheat and steal!

Not everybody, and not all the time. But it happens!

Accountants cannot guarantee that businesses will be ethical

and accurate when reporting the results of their operations.

Effective financial reporting depends on sound ethical behavior.

If you have an ethical dilemma:

1. Recognize the ethical situation and issues involved.

2. Identify and analyze the principal elements and stakeholders in the situation.

3. Identify the alternatives and weigh the impact of each alternative on various stakeholders.

1-6

Businesses are involved in 3 types of activity. The Acct. Information System (AIS) tracks of these activities in the

Balance Sheet and Income Statement

Business ActivitiesBusiness ActivitiesBusiness ActivitiesBusiness Activities

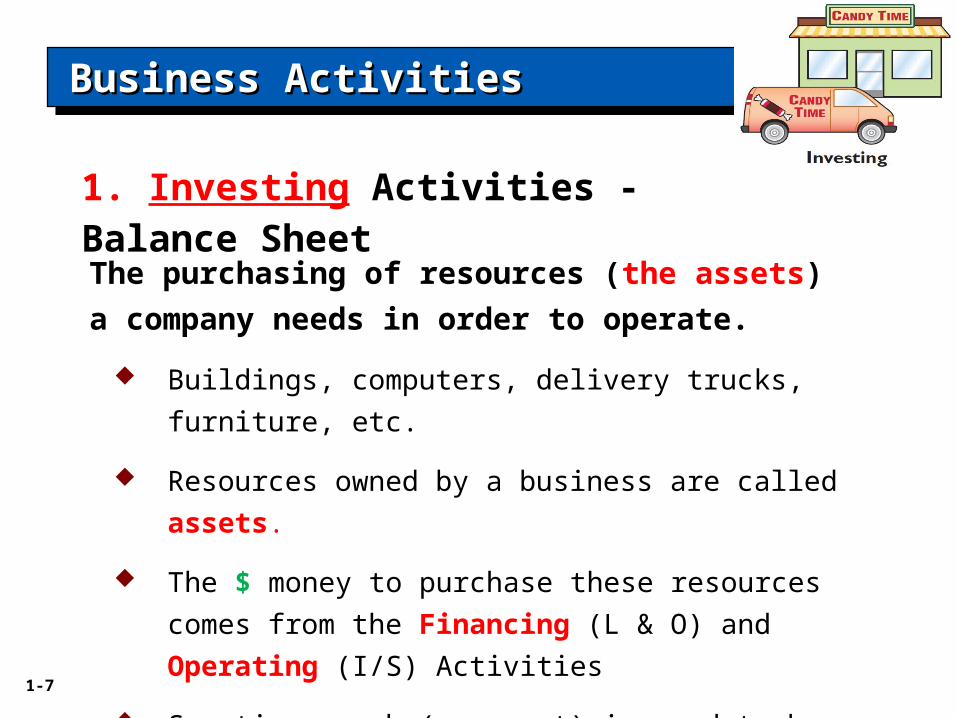

1. Investing 2. Financing Activities

AssetsL

3. Operating Activities

S/E

Rev- Exp = NI

1-7

1. Investing Activities - Balance Sheet

The purchasing of resources (the assets) a

company needs in order to operate.

Buildings, computers, delivery trucks, furniture, etc.

Resources owned by a business are called assets.

The $ money to purchase these resources comes from

the Financing (L & O) and Operating (I/S) Activities

Sometimes cash (an asset) is used to buy other assets

Business ActivitiesBusiness ActivitiesBusiness ActivitiesBusiness Activities

1-8

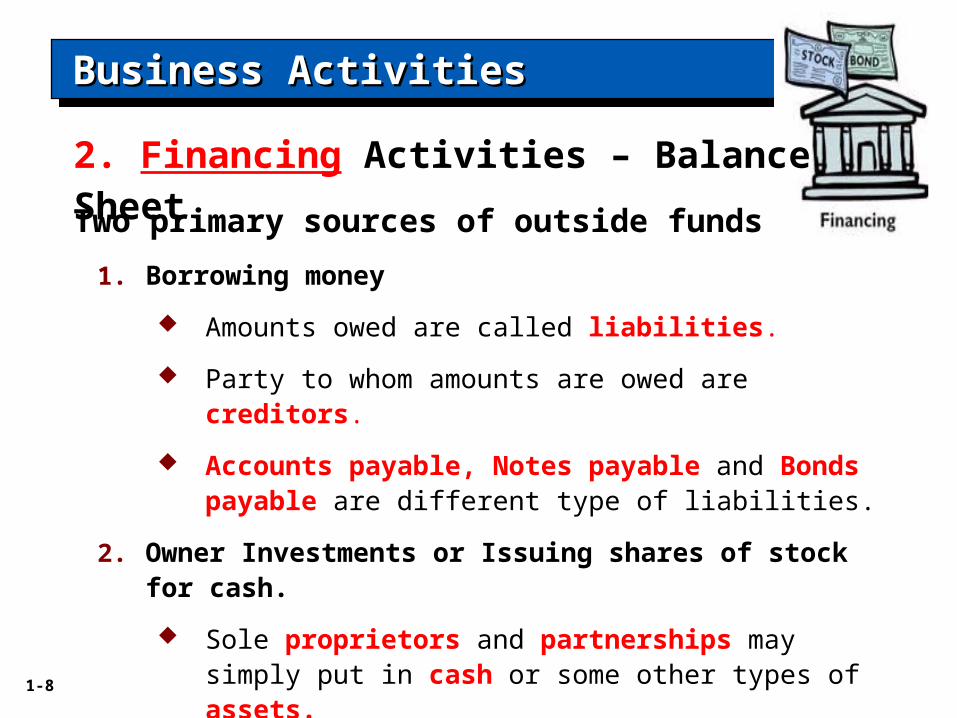

Two primary sources of outside funds are:

1. Borrowing money

Amounts owed are called liabilities.

Party to whom amounts are owed are creditors.

Accounts payable, Notes payable and Bonds payable are different type of liabilities.

2. Owner Investments or Issuing shares of stock for cash.

Sole proprietors and partnerships may simply put in cash or some other types of assets.

Payments to stockholders are called dividends.

Business ActivitiesBusiness ActivitiesBusiness ActivitiesBusiness Activities

2. Financing Activities – Balance Sheet

1-9

3. Operating Activities – Income Statement

Once a business has the assets it needs, it can begin

its operations and start earning money.

Revenues - Amounts earned from the sale of goods or

services performed (e.g., selling T-shirts = sales

revenue, mowing lawns = service revenue, others might

include interest revenue).

Inventory – Goods available for sale to customers.

Accounts receivable - Right to receive money from a

customer, in the future, as the result of a sale or service.

Business ActivitiesBusiness ActivitiesBusiness ActivitiesBusiness Activities

1-10

3. Operating Activities (continued)

Expenses - cost of assets consumed or services used - cost of

goods sold, administrative, selling, marketing, and tax expenses.

Liabilities arising from expenses include accounts payable,

interest payable, wages payable, sales taxes payable, and

income taxes payable.

Net income – when revenues exceed expenses (7 - 3 = +4)

Net loss – when expenses exceed revenues (4 – 6 = -2)

If you make money you’re “in the black”

If you lose money you’re “in the red.”

“Black Friday” is when a business finally makes a profit

Business ActivitiesBusiness ActivitiesBusiness ActivitiesBusiness Activities

1-11

Income Statement(Earnings)

Companies prepare 4 financial statements from the summarized accounting data - in this order!

Companies prepare 4 financial statements from the summarized accounting data - in this order!

Statement of Cash Flows

Retained Earnings

Statement(Any

Dividends?)

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

Balance Sheet

A small business for a sole proprietor or partnership may need only the I/S and B/S!

A small business for a sole proprietor or partnership may need only the I/S and B/S!

1-12

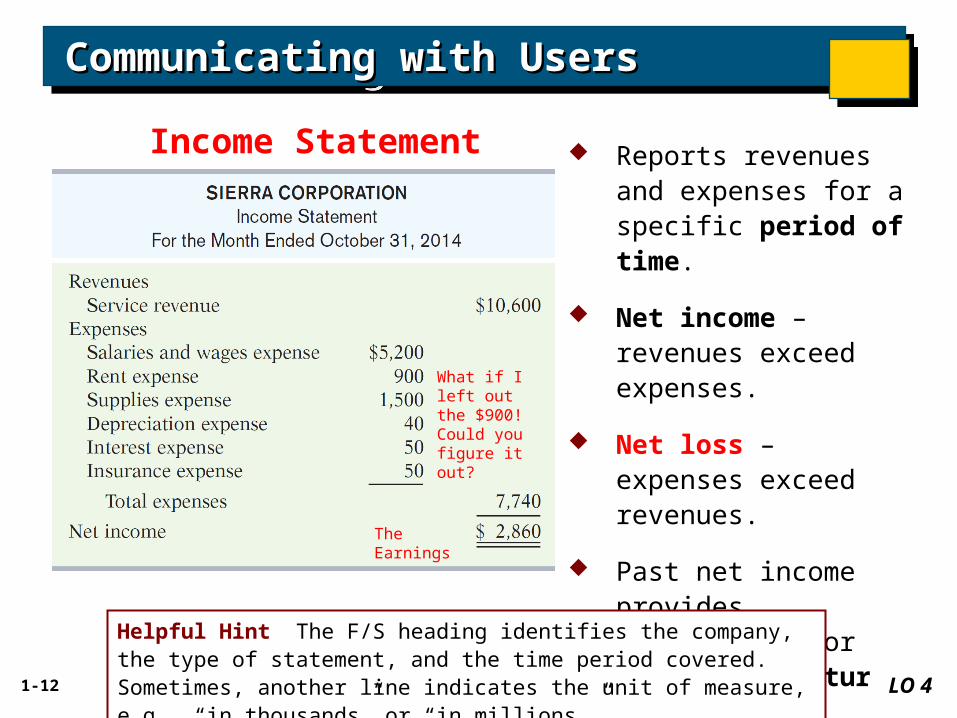

Reports revenues and expenses for a specific period of time.

Net income – revenues exceed expenses.

Net loss – expenses exceed revenues.

Past net income provides information for predicting future net income.

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

LO 4

Income Statement

Helpful Hint The F/S heading identifies the company, the type of statement, and the time period covered. Sometimes, another line indicates the unit of measure, e.g., “in thousands” or “in millions.”

What if I left out the $900! Could you figure it out?

The Earnings

1-13

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

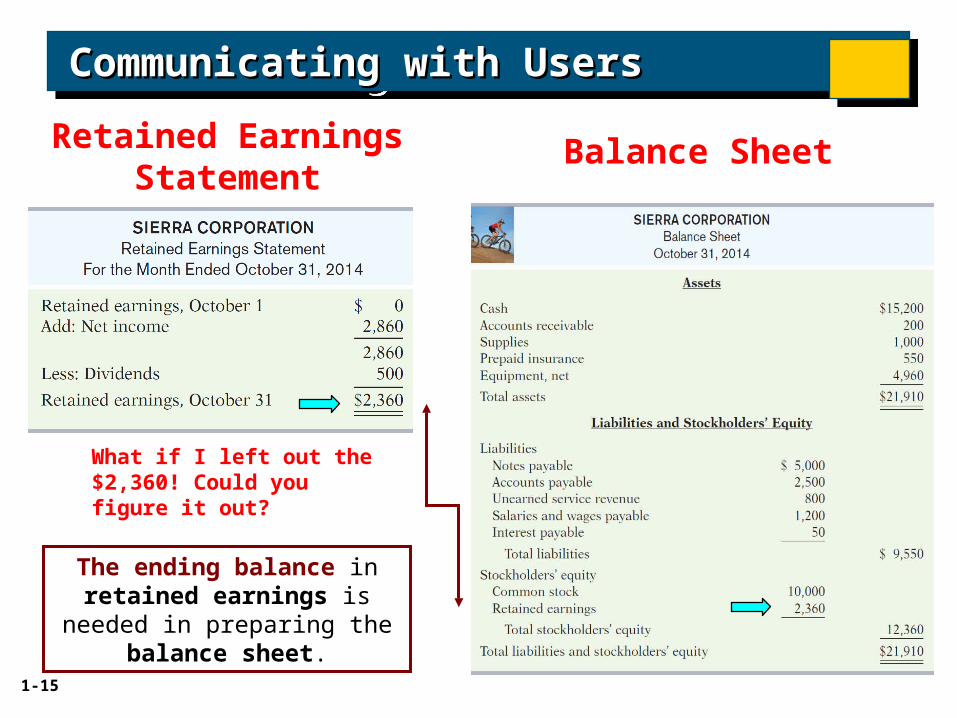

Retained Earnings Statement

Net income is needed to determine the ending balance in

retained earnings.

Income Statement

What if I left out the $500! Could you figure it out?

1-14

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

Statement shows amounts and

causes of changes in retained

earnings during the period.

Time period is the same as

that covered by the income

statement.

Users can evaluate dividend

payment practices. The R/E

statement is the only place

where we’ll see “dividends.”

Retained Earnings Statement

Helpful Hint The heading of this statement identifies the company, the type of statement, and the time period covered by the statement.

1-15

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

Retained Earnings Statement

The ending balance in retained earnings is needed in preparing the balance sheet.

Balance Sheet

What if I left out the $2,360! Could you figure it out?

1-16

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

Balance Sheet Reports assets and claims

to assets at a specific

point in time.

Assets = Liabilities +

Stockholders’ Equity.

Lists assets first, followed

by liabilities and

stockholders’ equity.

Helpful Hint The heading of a balance sheet must identify the company, the statement, and the date.

1-17

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

Balance Sheet Statement of Cash Flows

Remember the 3 types of business activities!

1-18

Where did cash come

from during the

period?

How was cash used

during the period?

What was the change

in the cash balance

during the period?

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

Statement of Cash Flows

LO 5

Helpful Hint The heading identifies the company, the type of statement, and the time period covered by the statement. Negative numbers are shown in parentheses.

Remember the 3 types of business activities!

1-19

U.S. companies that are publicly traded, meaning they sell their

stocks to the public (e.g., on the NYSE) and report to the Securities &

Exchange Commission, must provide shareholders with an annual

report.

The annual report always includes:

The Financial statements (already discussed)

Managements’ discussion and analysis (MD&A).

Notes to the F/S (footnotes/disclosures).

The Independent Auditor's report (The Auditor’s Opinion)

Elements of an Annual ReportElements of an Annual ReportElements of an Annual ReportElements of an Annual Report

1-20

Managements’ Discussion and Analysis

MD&A discusses 1. the company’s ability to pay near-term obligations,

2. its ability to fund operations and expansion, and 3. the results of

operations. Management must highlight favorable and/or unfavorable

trends and identify significant events and uncertainties affecting these

three factors.

Elements of an Annual ReportElements of an Annual ReportElements of an Annual ReportElements of an Annual Report

1-21

Elements of an Annual ReportElements of an Annual ReportElements of an Annual ReportElements of an Annual Report

Notes to the Financial Statements

Clarify the F/S and provide additional detail.

Notes are essential to understanding a company’s operating

performance and financial position and are a required part of

the annual report (sometimes called footnotes or disclosures)

LO 6

1-22

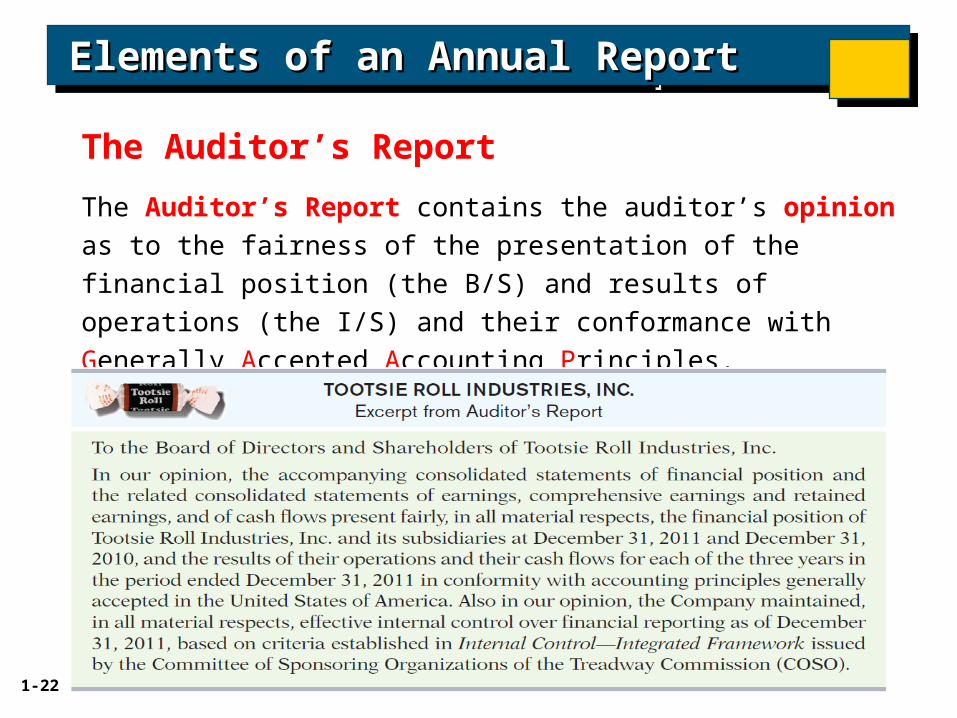

The Auditor’s Report

Elements of an Annual ReportElements of an Annual ReportElements of an Annual ReportElements of an Annual Report

The Auditor’s Report contains the auditor’s opinion as to the

fairness of the presentation of the financial position (the B/S) and

results of operations (the I/S) and their conformance with Generally

Accepted Accounting Principles.

1-23

In choosing the organizational form for your outdoor guide

service, you should consider the pros and cons of each. Identify each of the following

organizational characteristics with the organizational form or forms with which it is

associated.

1. Easier to raise funds.

2. Simple to establish.

3. No personal legal liability.

4. Tax advantages.

5. Easier to transfer ownership.

1. Corporation.

2. Sole proprietorship and partnership.

3. Corporation.

4. Sole proprietorship and partnership.

5. Corporation.

Solution

1-24

State whether each of the following items is most closely

associated with the management discussion and analysis (MD&A), the notes to

the financial statements, or the auditor’s report.

1. Descriptions of significant accounting policies.

2. Unqualified opinion.

3. Explanations of uncertainties and contingencies.

4. Description of ability to fund operations and expansion.

5. Description of results of operations.

6. Certified public accountant (CPA).

1. Notes.

2. Auditor’s report.

3. Notes.

4. MD&A.

5. MD&A.

6. Auditor’s report.

Solution

1-25

1. Cost of renting property.

2. Truck purchased.

3. Notes payable.

4. Issuance of ownership shares.

5. Amount earned from providing service.

6. Amounts owed to suppliers.

1. Expense.

2. Asset.

3. Liabilities.

4. Common stock.

5. Revenue.

6. Liabilities.

Solution

Classify each item as an asset, liability, common stock,

revenue, or expense.

1-26

Net income will result during a time period when:

a. assets exceed liabilities.

b. assets exceed revenues.

c. expenses exceed revenues.

d. revenues exceed expenses.

Review Question

Communicating with UsersCommunicating with UsersCommunicating with UsersCommunicating with Users

1-27

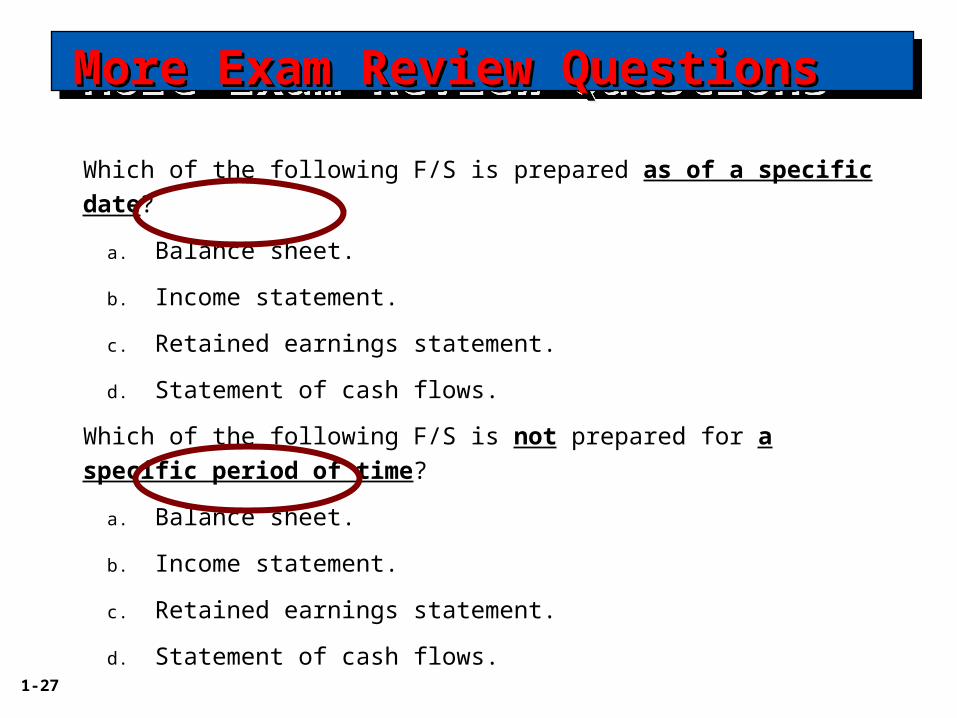

Which of the following F/S is prepared as of a specific date?

a. Balance sheet.

b. Income statement.

c. Retained earnings statement.

d. Statement of cash flows.

More Exam Review QuestionsMore Exam Review QuestionsMore Exam Review QuestionsMore Exam Review Questions

Which of the following F/S is not prepared for a specific period of time?

a. Balance sheet.

b. Income statement.

c. Retained earnings statement.

d. Statement of cash flows.