09VWCMA056 NAINA LAZARUS

148

INDUSTRIAL TRAINING REPORT An Organizational Study of Bharti-AXA Life Insurance Co. Ltd. & Risk Analysis of Bharti-AXA Life Insurance ULIP Funds – A Study This Industrial Training Report is submitted in partial fulfillment of the requirements for the award of the Degree of MASTER OF BUSINESS ADMINISTRATION of BANGALORE UNIVERSITY This training has been undertaken by Naina Monica Pranesh Lazarus Reg. No. 09VWCMA056 Under the guidance and support of Poonam Nam Joshi M S Dilip Professor Agency Manager Alliance Business Academy Bharti-AXA Life Insurance ALLIANCE BUSINESS ACADEMY BANGALORE-560 076 1

-

Upload

nitesh-garodia -

Category

Documents

-

view

226 -

download

0

Transcript of 09VWCMA056 NAINA LAZARUS

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 1/147

INDUSTRIAL TRAINING REPORT

An Organizational Study of

Bharti-AXA Life Insurance Co. Ltd.

&

Risk Analysis of Bharti-AXA Life Insurance ULIP Funds – A Study

This Industrial Training Report is submitted in partial fulfillment of the requirements for the

award of the Degree of

MASTER OF BUSINESS ADMINISTRATION

of

BANGALORE UNIVERSITY

This training has been undertaken by

Naina Monica Pranesh Lazarus

Reg. No. 09VWCMA056

Under the guidance and support of

Poonam Nam Joshi M S Dilip

Professor Agency Manager

Alliance Business Academy Bharti-AXA Life Insurance

ALLIANCE BUSINESS ACADEMY

BANGALORE-560 076

1

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 2/147

Batch: 2009-2011

DECLARATION

I, Naina Lazarus, studying at Alliance Business Academy, hereby state that this

industrial training report titled “Risk Analysis of Bharti-AXA Life Insurance ULIP

Funds - A Study” carried out at Bharti-AXA Life Insurance Co. Ltd., is submitted in

partial fulfilment of the requirement of the MBA Program of Bangalore University, is

an original work carried out by me under the guidance and supervision of Poonam Nam

Joshi, faculty guide & M S Dilip, industry guide, and that the project or any part thereof

has not been previously submitted for a degree/diploma of any University/ Institution

elsewhere.

Date: 20th August 2010

Place: Bangalore

Naina Lazarus

Reg. No. 09VWCMA056

2

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 3/147

ACKNOWLEDGEMENT

The satisfaction that accompanies the successful completion of task would be incomplete

without the mention of the people who have made it possible and whose consent, guidance and

encouragement served as a guiding light for the completion of the study.

I would like to express my profound sense of gratitude to Prof. Sudhir Angur, President,

Alliance Business Academy for providing constant source of inspiration and the support to

conduct this research. I would also like to thank Prof. Prabhakaran and Prof. Rajasekhar for

providing constant source of inspiration and the support to conduct this research.

With a deep sense of gratitude, and indebtedness, I sincerely & whole-heartedly thank Mr. M S

Dilip (Agency Manager) and Mrs. Latha Balasubramanian (Branch Head), Bharti-AXA Life

Insurance Co. Ltd. for giving me an opportunity to conduct this study & for being a guiding

factor in all the steps of my internship and report, which has been a rewarding experience.

I would like to thank my guide, Prof. Poonam Nam Joshi and our program manager Prof.

Smitha Shenoy for their continuous guidance and support in bringing out this project.

I also express my deep gratitude to my family and friends, whose cooperation, wishes and help,

have made this project possible.

3

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 4/147

Naina Lazarus

TABLE OF CONTENTS

Chapter

No. Topic

Page

No.

EXECUTIVE SUMMARY

1 INDUSTRY PROFILE

1.1 Overview of the Indian Economy

1.2 Insurance Industry

2 COMPANY PROFILE

2.1 Introduction

2.2 Functional Departments

3 RESEARCH DESIGN

3.1 Statement of the Problem

3.2 Title of the Study

3.3 Objectives of the Study

4

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 5/147

3.4 Scope of the Study

3.5 Operational Definitions

3.6 Research Methodology

4 DATA ANALYSIS

4.1 Introduction

4.2 Analysis and interpretation

5 FINDINGS, SUGGESTIONS & CONCLUSION

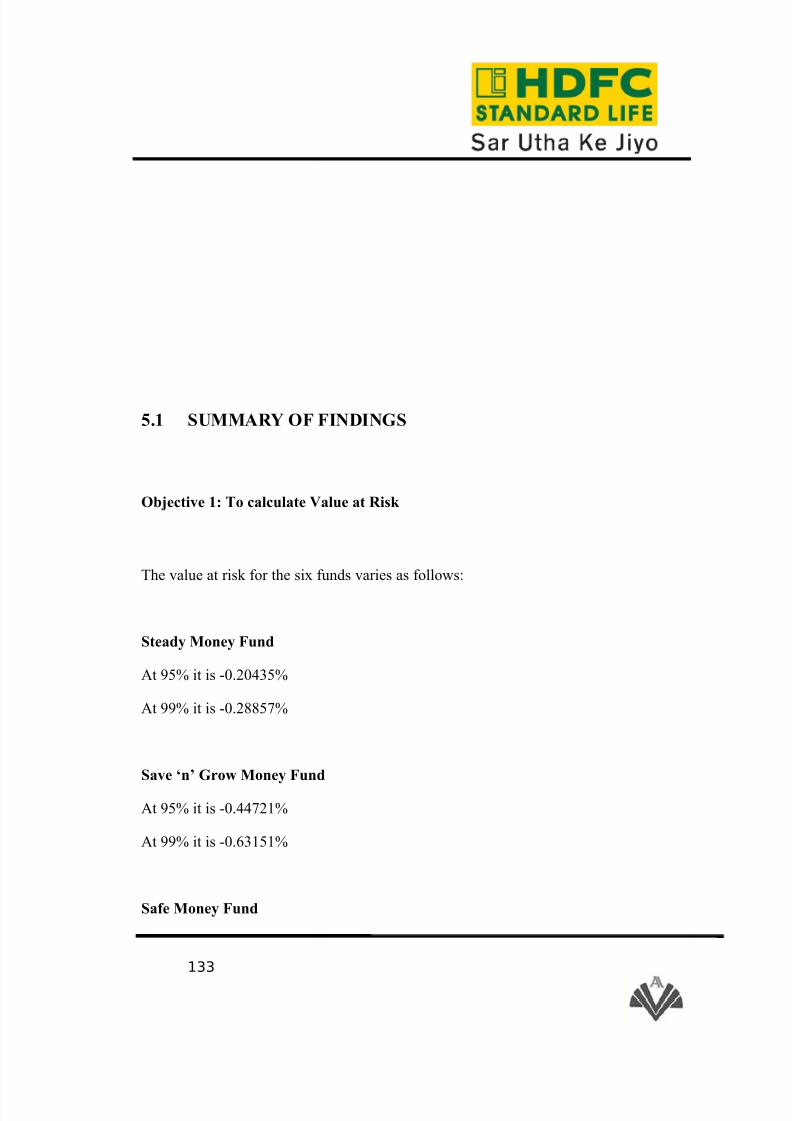

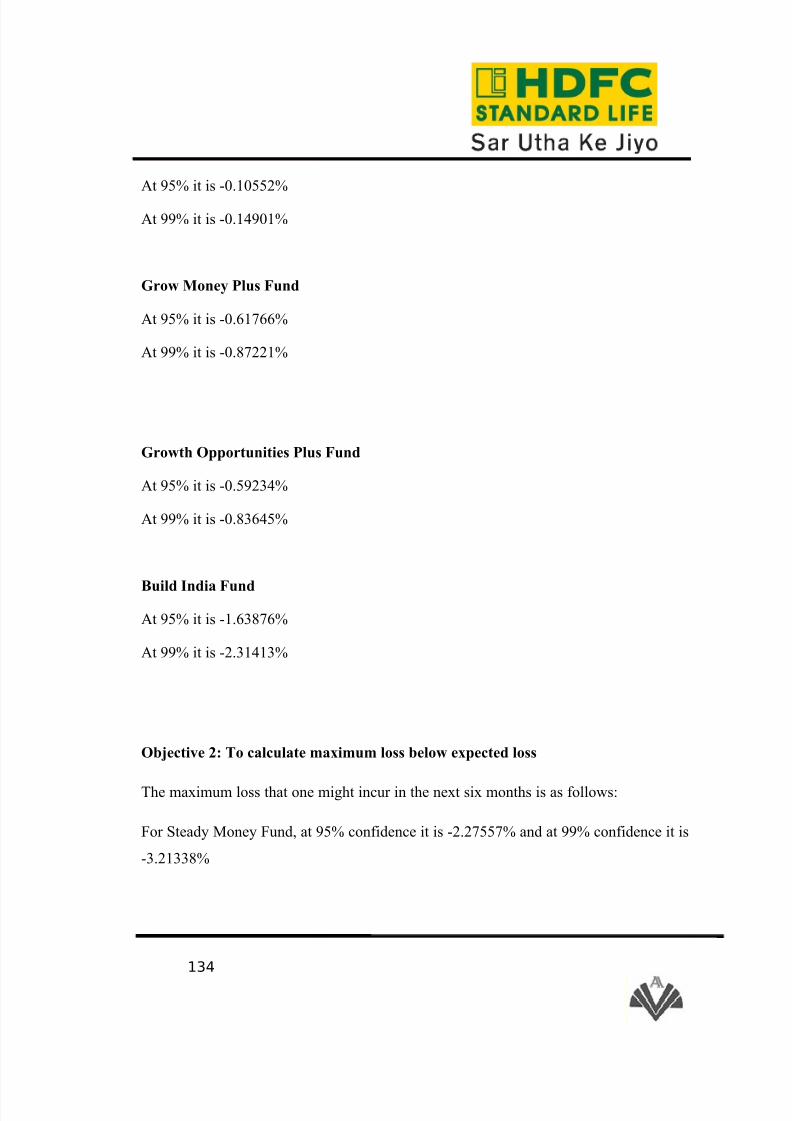

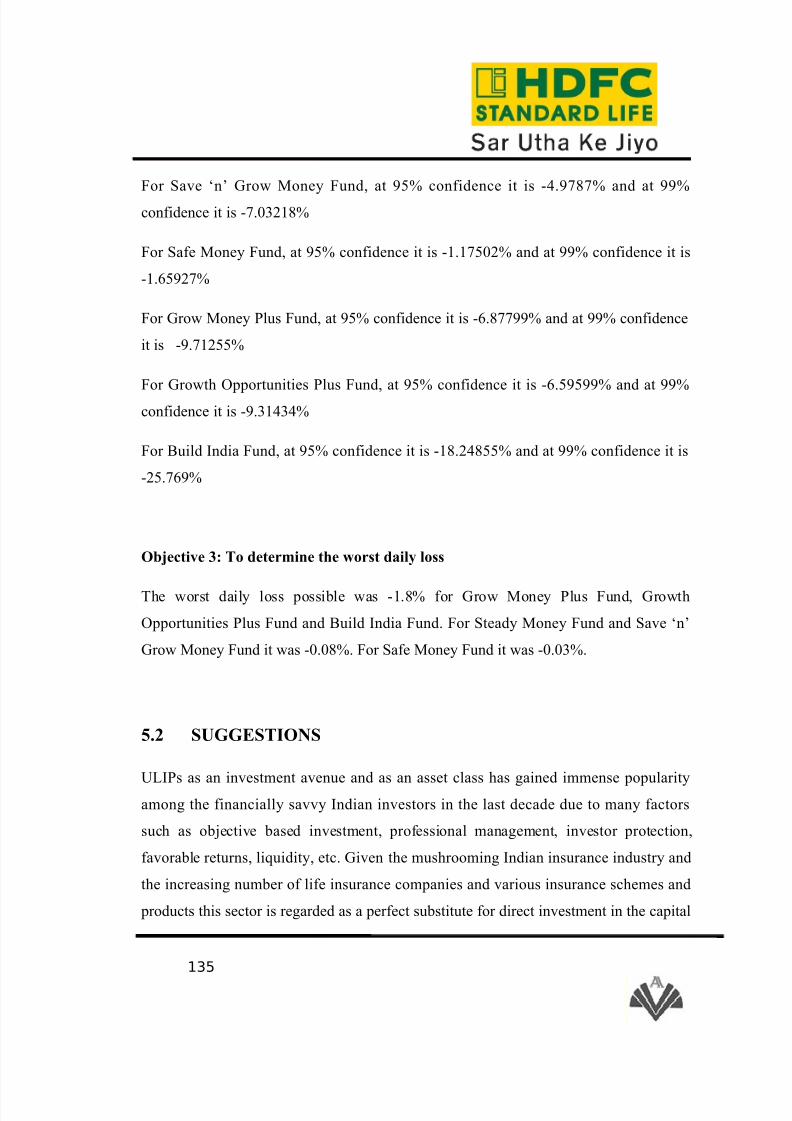

5.1 Summary of Findings

5.2 Suggestions

5.3Conclusion

MY LEARNING

BIBLIOGRAPHY

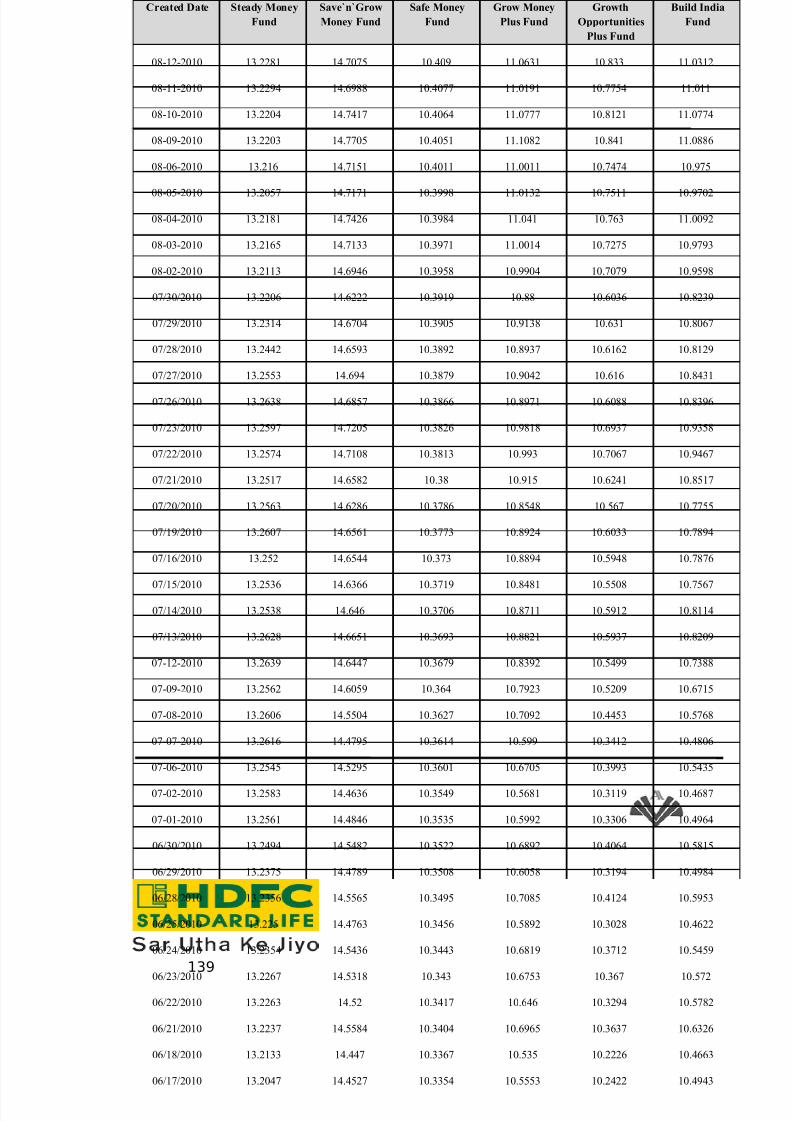

ANNEXURE

5

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 6/147

LIST OF TABLES

Sl. No. ParticularsPage

No.

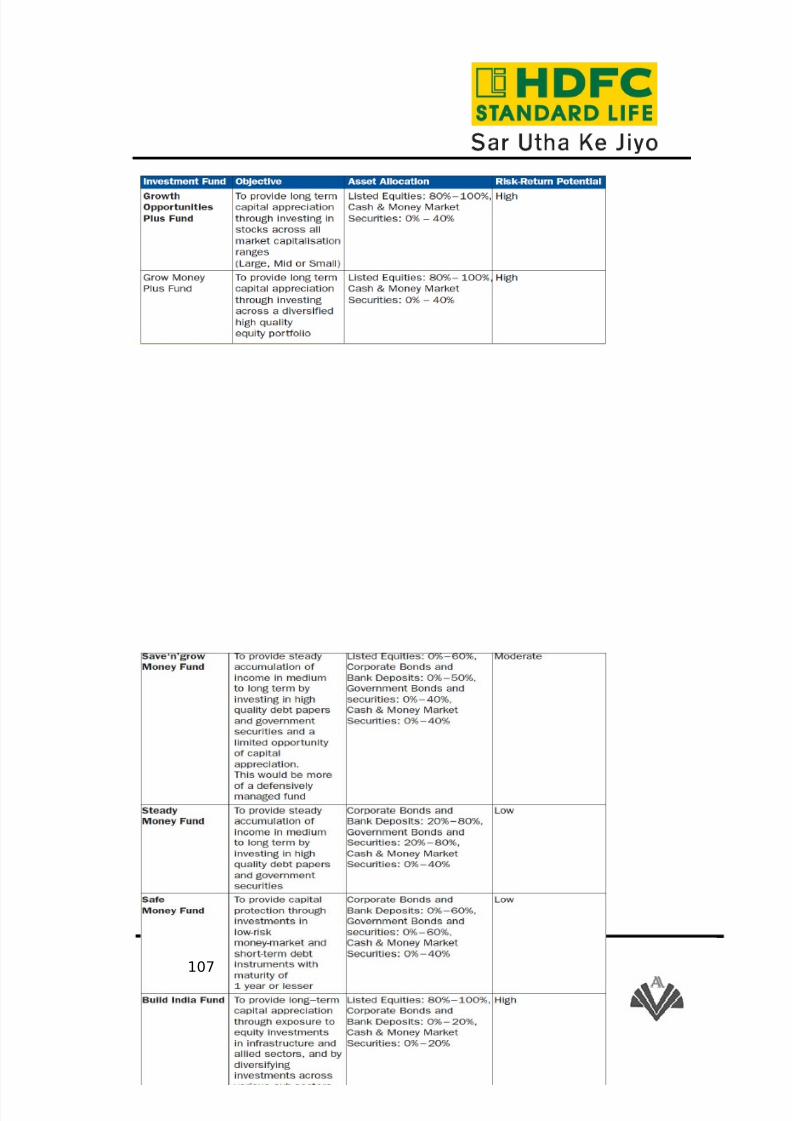

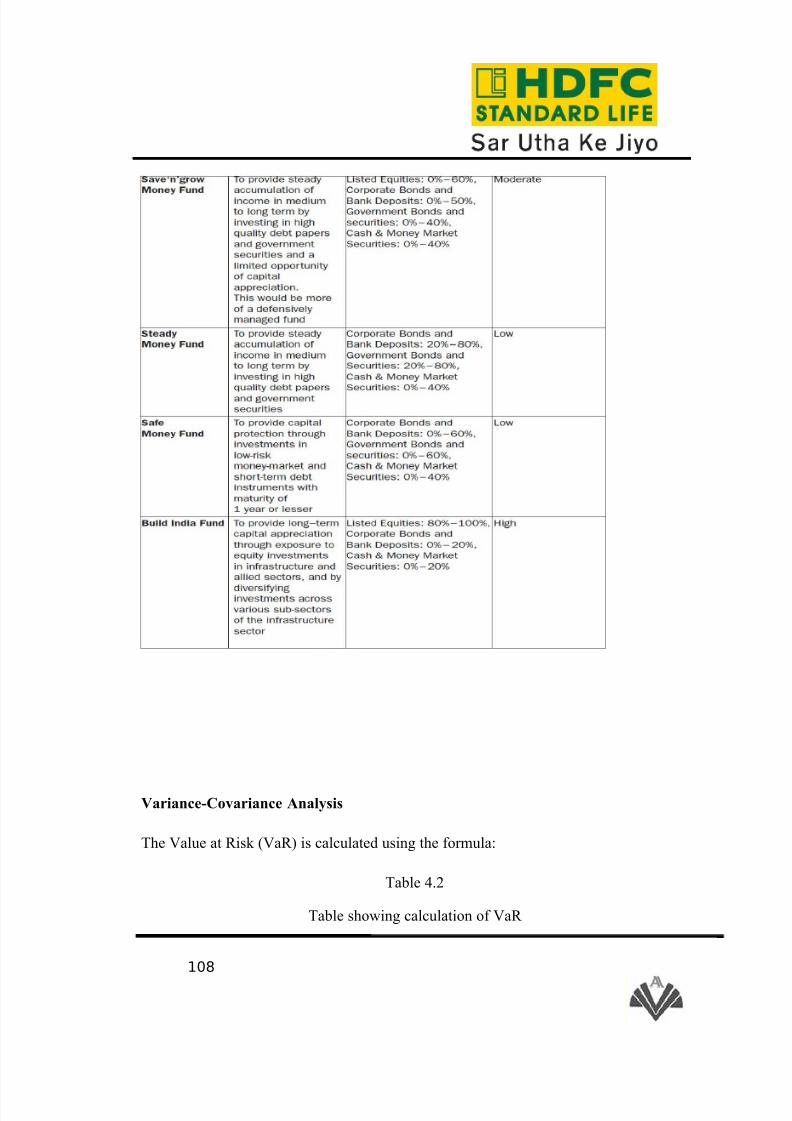

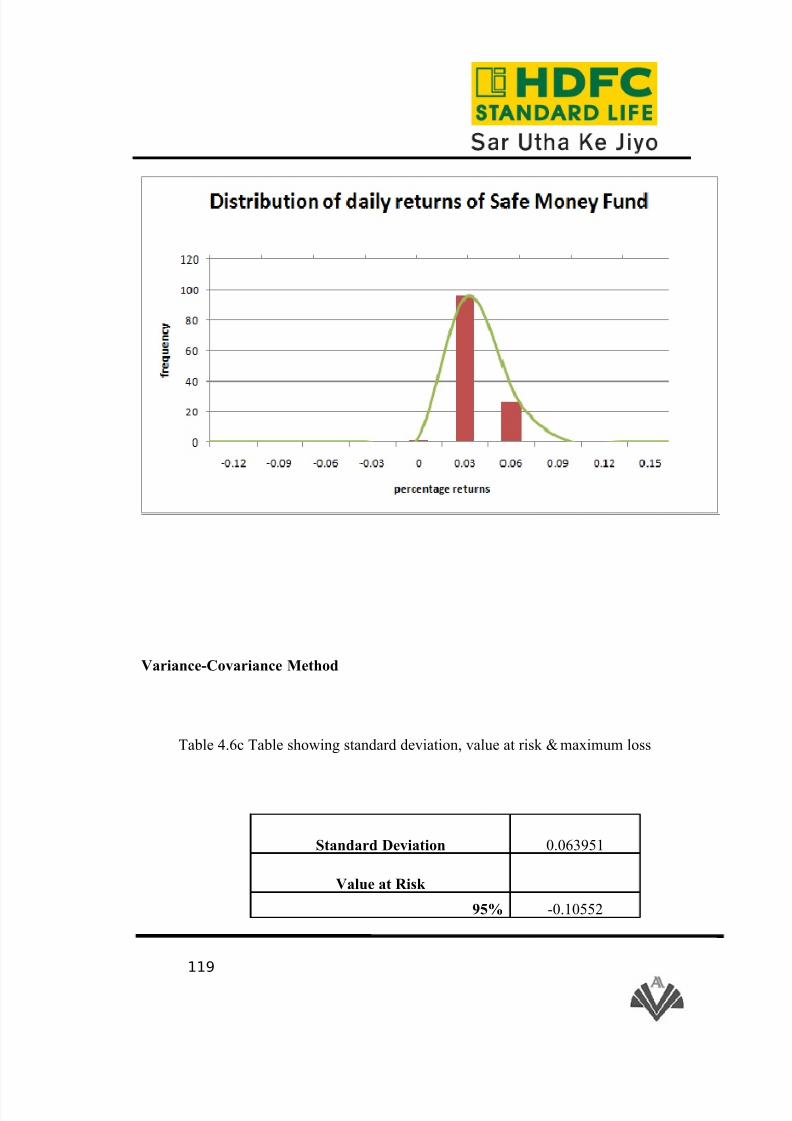

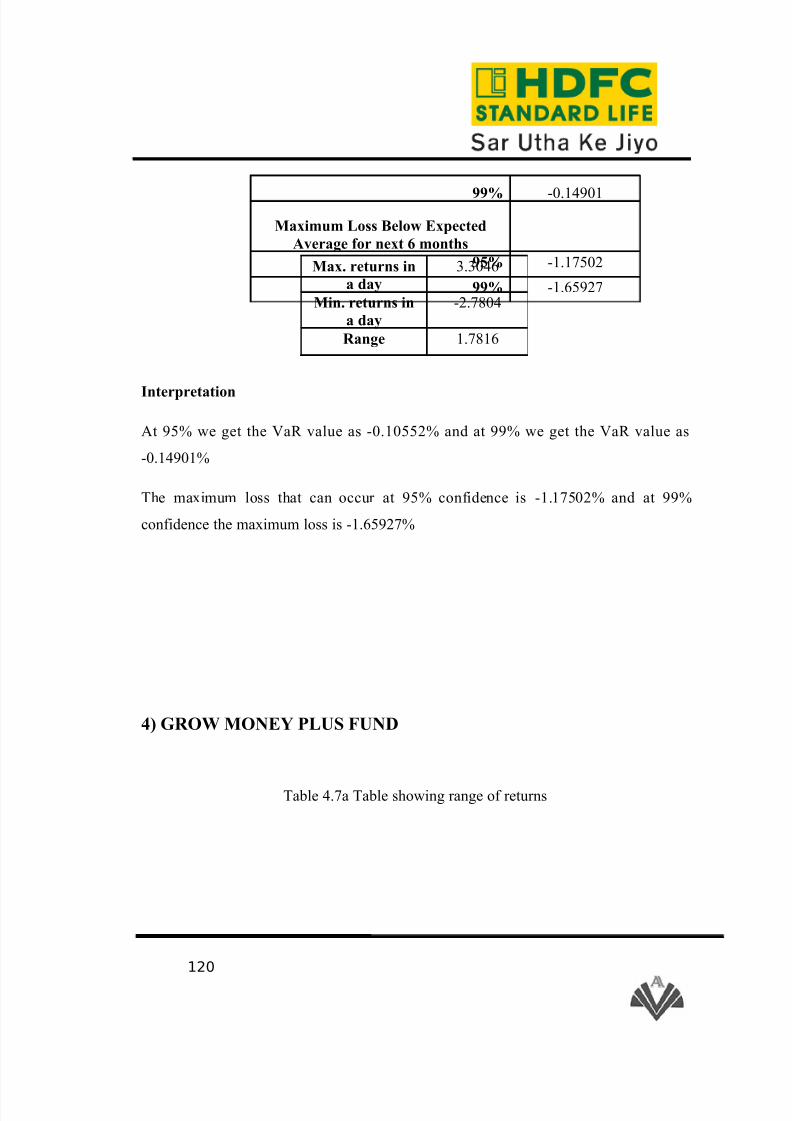

4.1 Table showing asset allocation & risk-return potential of the different funds

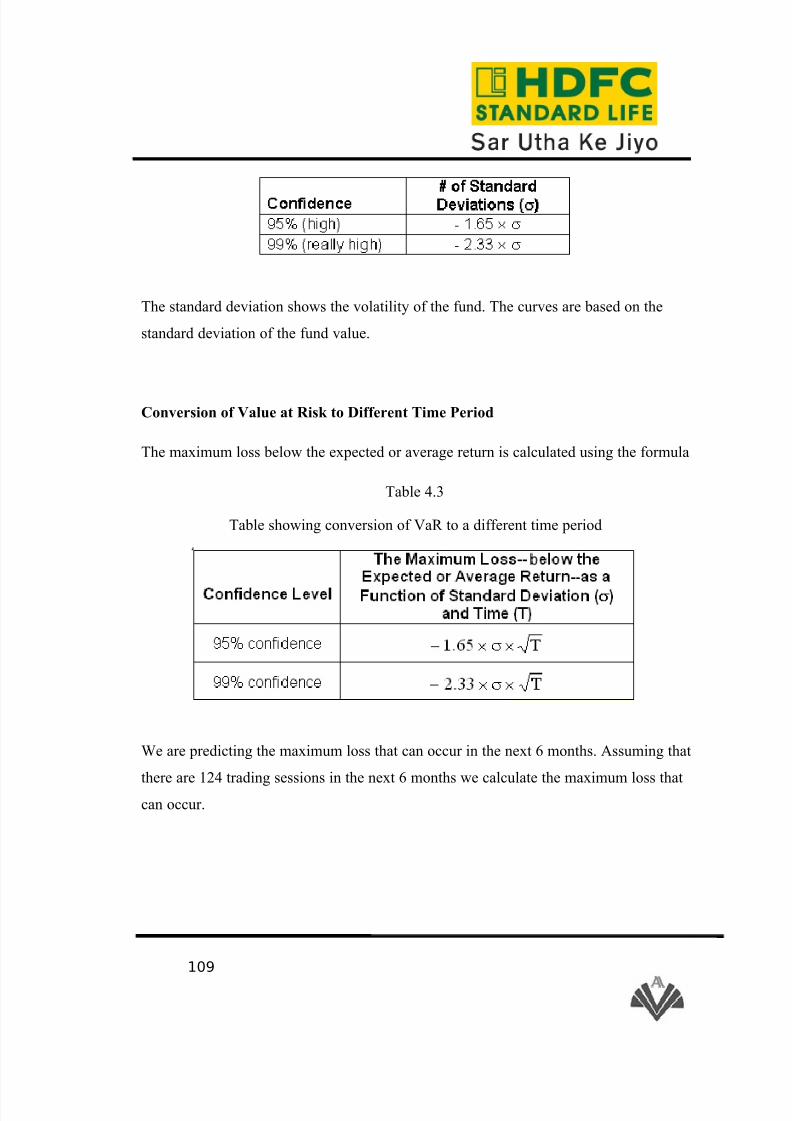

4.2 Table showing calculation of Value at Risk (VaR)

4.3 Table showing conversion of VaR to a different time period

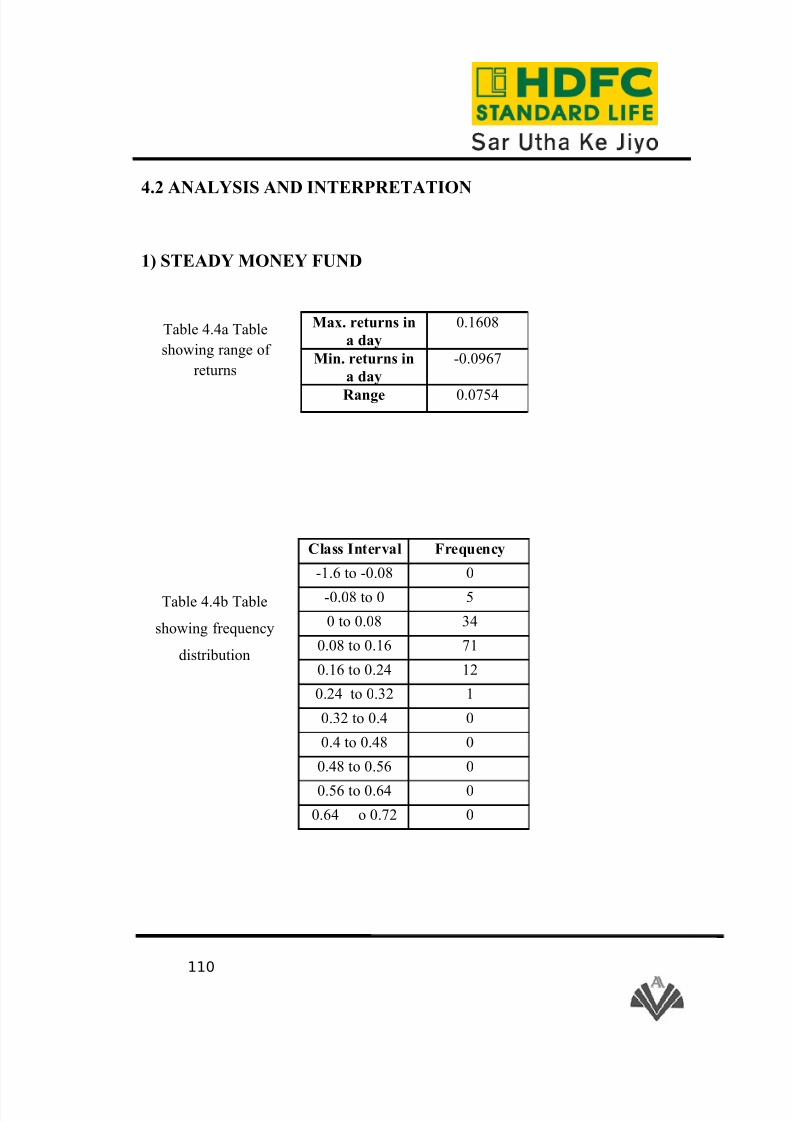

4.4a Table showing range of returns for Steady Money Fund

4.4b Table showing frequency distribution for Steady Money Fund

4.4c Table showing SD, VaR & maximum loss for Steady Money Fund

4.5a Table showing range of returns for Save ‘n’ Grow Money Fund

4.5b Table showing frequency distribution for Save ‘n’ Grow Money Fund

4.5c Table showing SD, VaR & maximum loss for Save ‘n’ Grow Money Fund

4.6a Table showing range of returns for Safe Money Fund

6

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 7/147

4.6b Table showing frequency distribution for Safe Money Fund

4.6c Table showing SD, VaR & maximum loss for Safe Money Fund

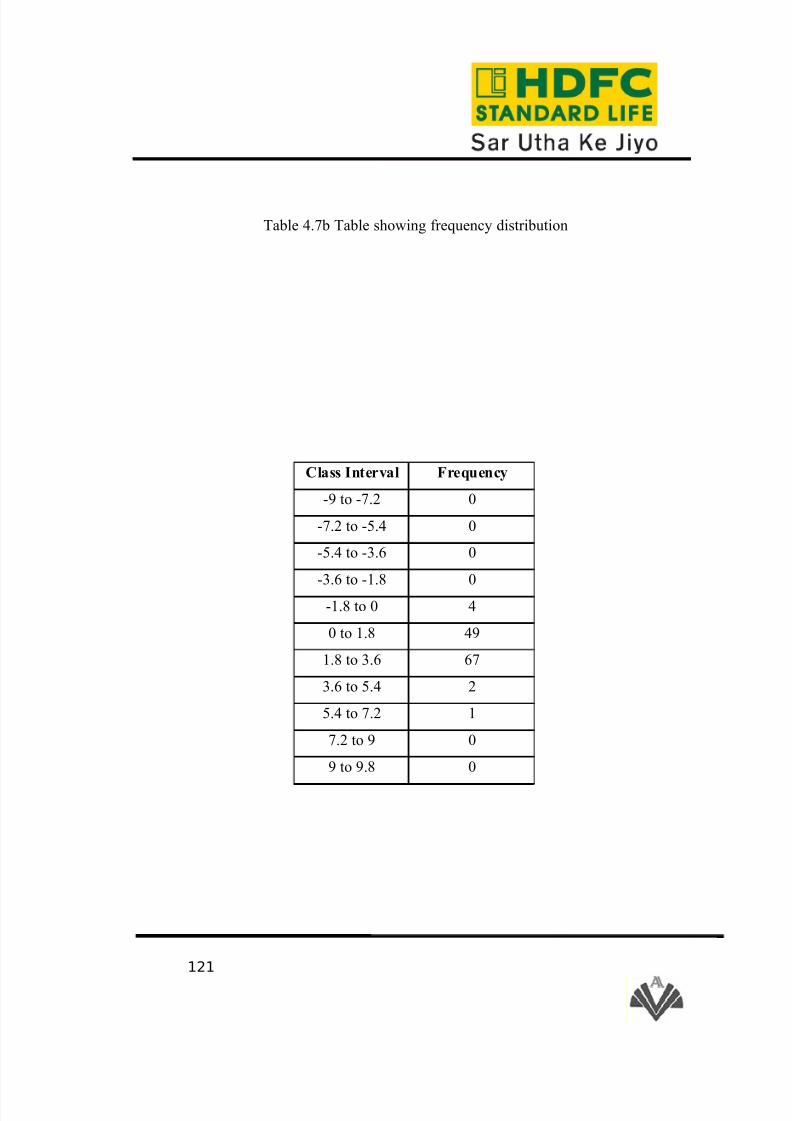

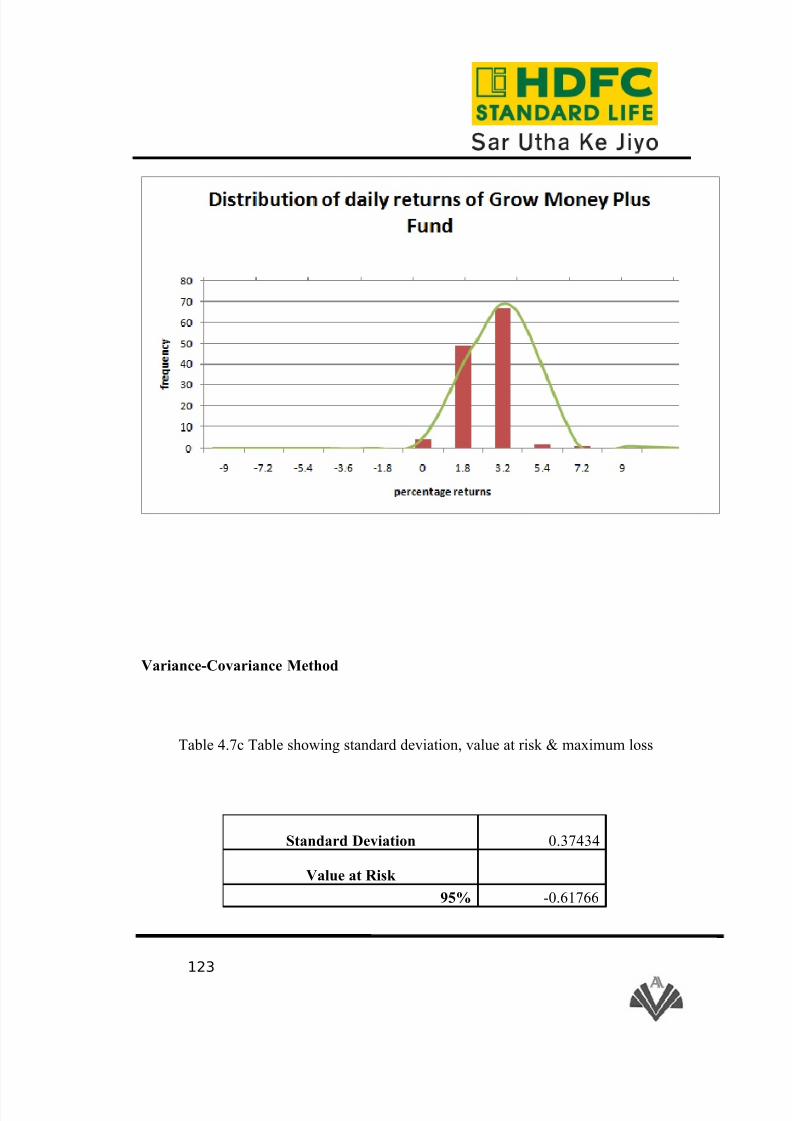

4.7a Table showing range of returns for Grow Money Plus Fund

4.7b Table showing frequency distribution for Grow Money Plus Fund

4.7c Table showing SD, VaR & maximum loss for Grow Money Plus Fund

4.8a Table showing range of returns for Growth Opportunities Plus Fund

4.8b Table showing frequency distribution for Growth Opportunities Plus Fund

4.8cTable showing SD, VaR & maximum loss for Growth Opportunities Plus

Fund

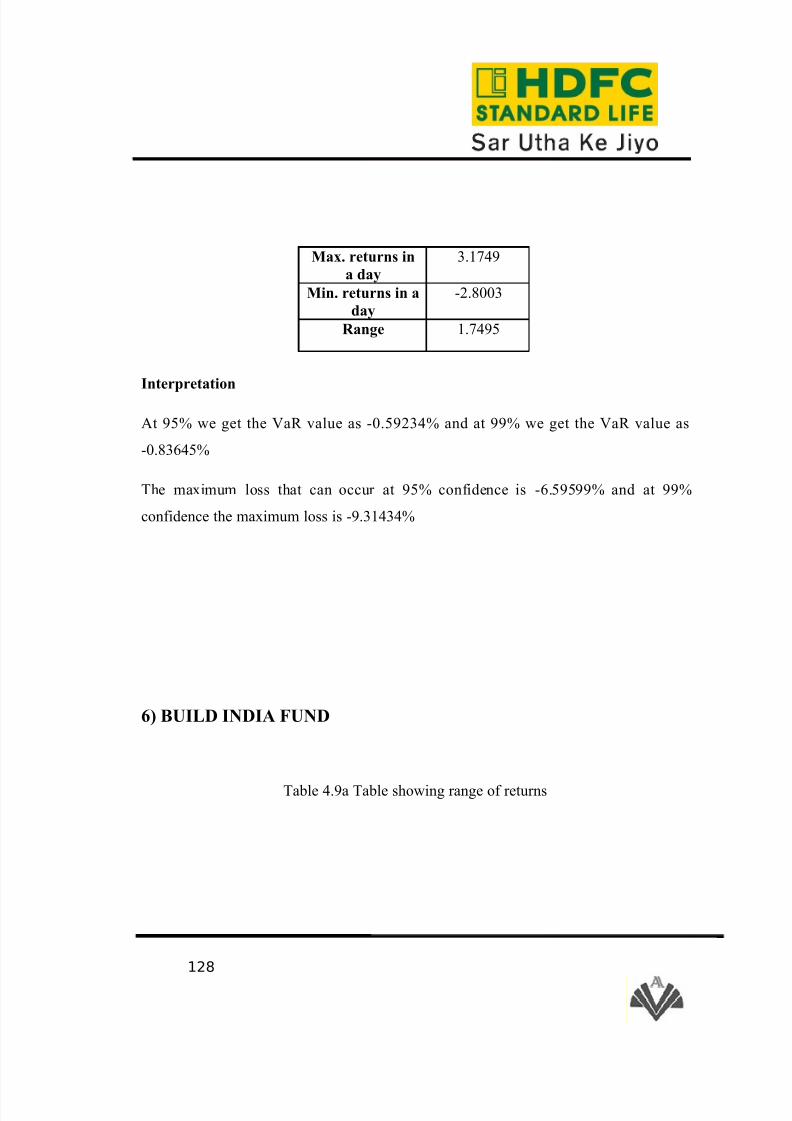

4.9a Table showing range of returns for Build India Fund

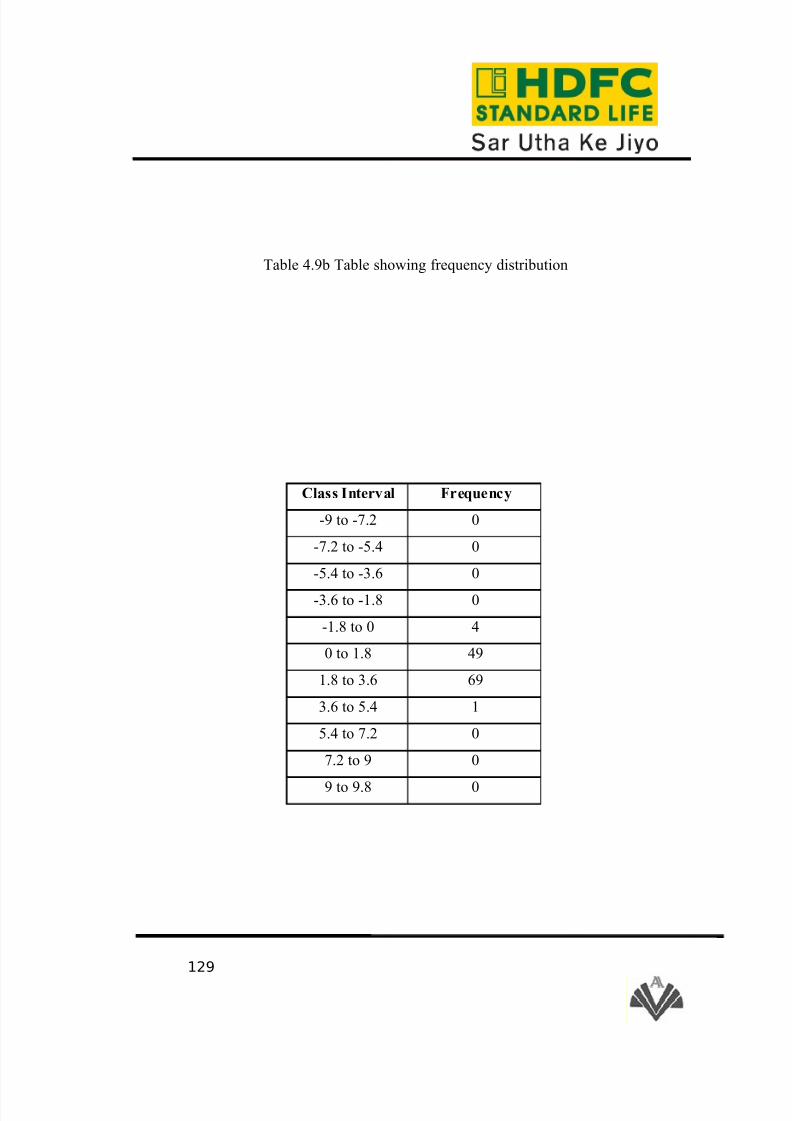

4.9b Table showing frequency distribution for Build India Fund

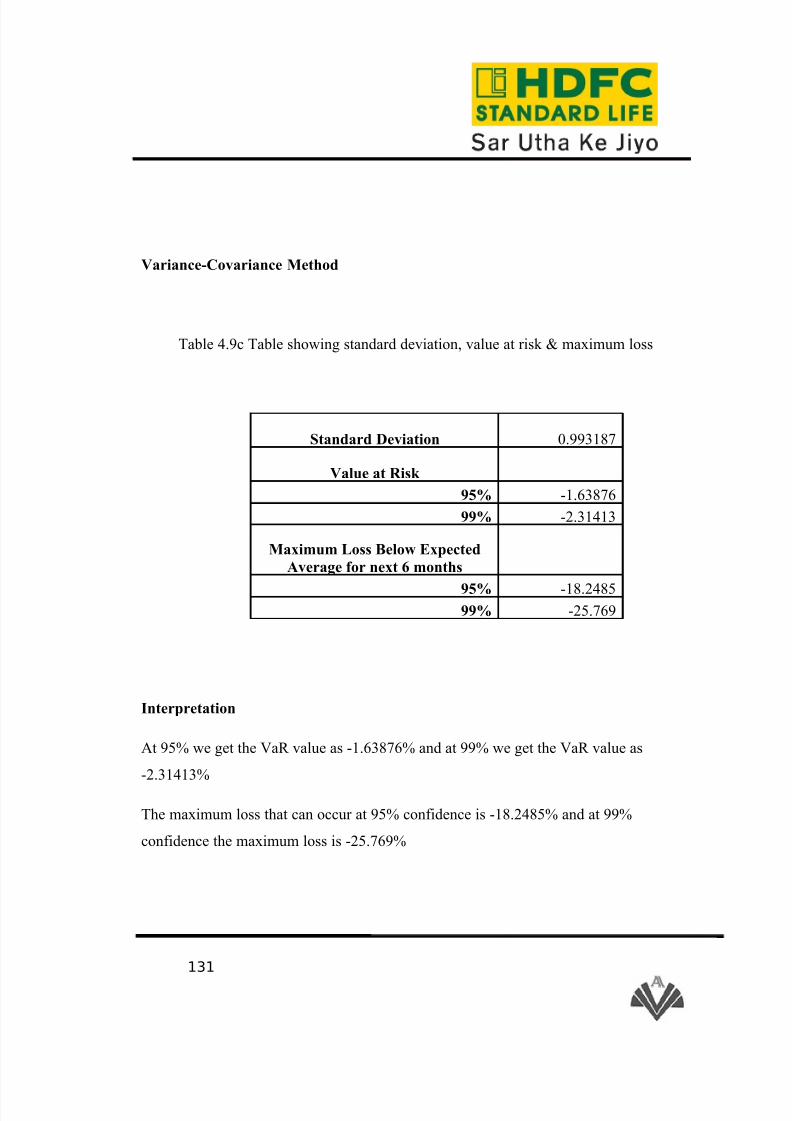

4.9c Table showing SD, VaR & maximum loss for Build India Fund

7

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 8/147

LIST OF CHARTS/GRAPHS

Sl.

No.

ParticularsPage

No.

1.1 Chart showing the market share of Life Insurance Companies in India

2.1 Chart showing the organisation structure

2.2 Chart showing the recruitment process

2.3 Chart showing the sales process

4.1 Graph showing the distribution of daily returns of Steady Money Fund

4.2Graph showing the distribution of daily returns of Save ‘n’ Grow Money

Fund

4.3 Graph showing the distribution of daily returns of Safe Money Fund

4.4 Graph showing the distribution of daily returns of Grow Money Plus Fund

4.5Graph showing the distribution of daily returns of Growth Opportunities

Plus Fund

8

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 9/147

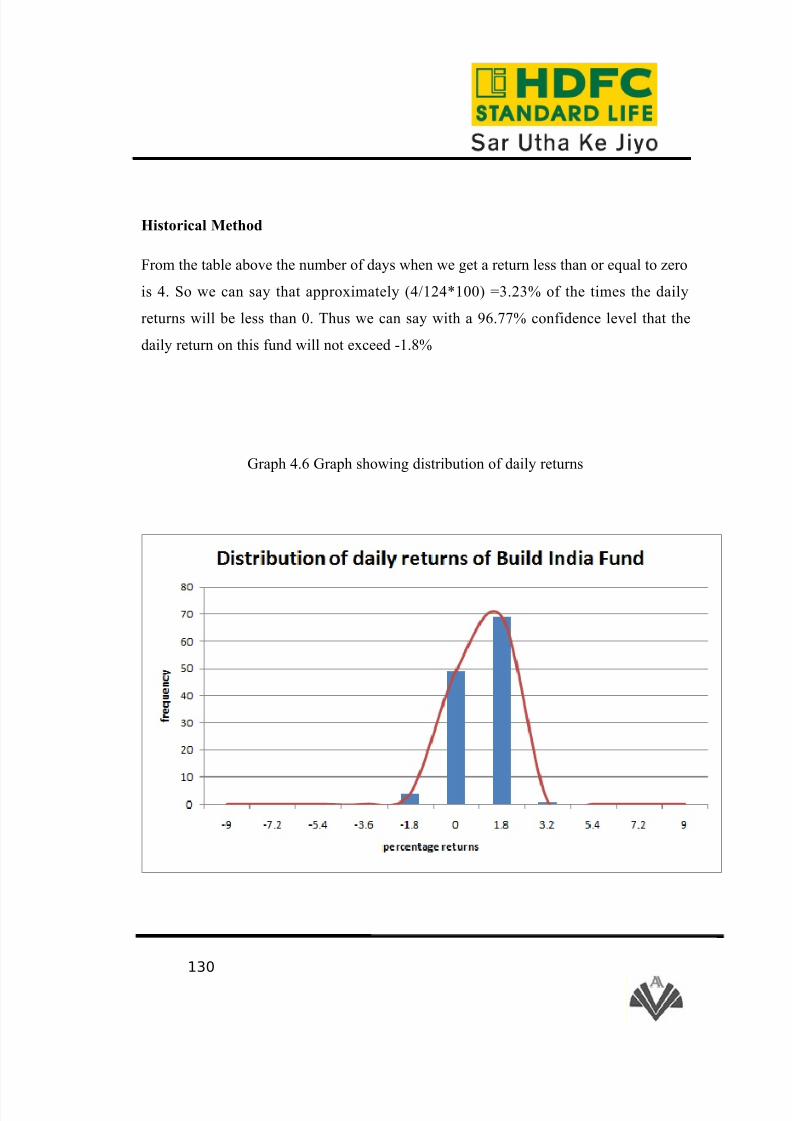

4.6 Graph showing the distribution of daily returns of Build India Fund

EXECUTIVE SUMMARY

The insurance companies, from a long time have been considered as a place where people pay

premium from a view point of its safety & earning returns over the premium paid after the

policy has matured. However, off late the role of insurance has widened. From a mere life

protection provider it has evolved into an institution which tries to meet different financial

requirements of customer. Investment is one such need. This report deals with the different

functions a life insurance company performs which act as a facilitator for investors. The study

is done keeping the policies of Bharti AXA Life in mind.

Bharti AXA Life Insurance Co. Ltd. is a joint venture between Bharti - one of India’s leading

business groups and AXA - global leader in financial protection and wealth management.

Bharti AXA Life Insurance has a 74% stake from Bharti and 26% stake of AXA in the joint

venture. In December 2006, the Company launched its operations in India. At present, it has

more than 5200 employees working over 12 states in the country. With the continuous

expansion, Bharti AXA Life Insurance is making itself proactive to cater to insurance and

wealth management needs of people.

In addition to the study on risk analysis of the ULIP funds, the study was conducted to

know the various functional areas of the organization. It included the study of various

departments, competitors, products of Bharti AXA Life Insurance. The stay in the

9

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 10/147

organization equipped with an in-depth knowledge of insurance as an investmentavenue, its benefits, restrictions, process and other aspects.

The study was an analytical study with a sample size of six different types of funds under Bharti

AXA ULIP plans. Out of this, three are equity funds, two are debt funds and remaining one is a

balanced fund. The data encompassing the performance of various funds was limited to six

months, from January to June 2010. So the study may not hold good for all the time.

The portfolio allocation, as well as sector-wise allocation had a great impact on performance of

the fund, be it an equity fund, a debt fund or a balanced fund. Descriptive statistics revealed that

the equity had the highest standard deviation, which means the risk involved is very high, thus

investment should be made with care in the equity. On the other hand, standard deviation of

debt and balanced funds was low, which means that both these instruments are safe to invest in.

The investment goals of the clients are varied and thus it is a challenge of the distribution

service to meet the investors expected returns irrespective of the market conditions. The

insurance companies should have a well-trained customer care cell for all the customer

grievances. Fund manager should be very careful about the asset allocation as it has a great

impact on the fund’s performance.

Lastly, since there has been an increase in the cost of living, investors should start saving early

so as to get maximum returns. An investor can easily achieve this, if right investment is made in

the right kind of funds thus ensuring that the right portfolio would help an investor to trade off

between risk and return.

10

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 11/147

CHAPTER 1

INDUSTRY PROFILE

11

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 12/147

1.1 OVERVIEW OF THE INDIAN ECONOMY

1.1.1 INTRODUCTION

India is an emerging economy and has witnessed unprecedented levels of economic

expansion. India, being a cost effective and labour intensive economy, has benefited

immensely from outsourcing of work from developed countries, and a strong

manufacturing and export oriented industrial framework. With the economic pace

picking up, global commodity prices have staged a comeback from their lows and

global trade has also seen healthy growth over the last two years.

There have been a number of causes behind growth of Indian economy in the last

couple of years. A number of market reforms have been instituted by the

Indian government and there has been significant amount of foreign direct investment

made in India. Much of this amount has been invested into several businesses including

knowledge process outsourcing industries. India’s foreign exchange reserves have gone

12

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 13/147

up in the last few years. Real estate sector as well as information technology industrieshave taken off. Capital markets are doing pretty well too.

Growing domestic demand and increased production have changed the Indian

economy.GDP has picked up, trade has become global and the services sector has led

change by throwing its gates open to outsourcing. India’s educated and English

speaking population became the biggest impetus that the economy needed. Trade has

risen by more than 375% since the adoption of the liberalization policies. All these

factors have contributed to the growth of the Indian economy.

1.1.2 INDIAN ECONOMIC INDICATORS

Indian economic indicators are pointing towards the country’s transition to a developed

economy.

a) GDP

India’s gross domestic product (purchasing power parity) was $3.561 trillion in 2009. It

was up from $3.344 trillion in 2008 and $3.113 trillion in 2007. India ranked fifth in the

world in terms of its purchasing power.

The official exchange rate GDP was $1.095 trillion in 2009 with per capita GDP at

$3,100. This was an increase from $2,900 in 2008 and $2,800 of 2007. However,

India’s world ranking was 164 due to its high variance in income and disparate wealth

distribution.

13

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 14/147

Real GDP growth was 6.5% in 2009, down from 7.4% and 9% in 2008 and 2007,respectively. The largest contribution towards GDP came from the services sector,

which contributed 58.4% of the total GDP. The industry sector contributed 25.8% and

agriculture added 15.8% to the GDP. Services kept its position as the biggest employer

as well for the huge workforce of 467 million people. Services employed 62.6%, while

industry generated 20% and agriculture pitched in 17.5% of the total jobs.

b) Inflation

Through a strict credit policy and stringent fiscal arrangements, India could somewhat

evade the recession. However, inflation has been a cause of concern. The 2009 figure

confirmed inflation at 10.7%, up from 8.3% in 2008. With industrial growth at 7.6% in

2009, India ranked as the twelve most progressive countries in the world.

c) FDI

The modern and liberalized Indian economy is a hotspot for FDI (foreign direct

investment). Every year the volume seems to grow larger and 2009 was no exception.

With FDI growing from $123.4 billion in 2008 to $161.3 billion in 2009, the Indian

economy has become the favourite spot for global investors to hedge their investments

and make profits in an economy where disposable income is rising steadily.

d) Core Infrastructure

Growth in the overall core infrastructure sector increased from 3.8% in October 2009 to

9.4% in January 2010, compared to the low growth of 2% achieved during the

14

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 15/147

corresponding months of the previous year. In January 2010, acceleration in growth wasseen in all the six core industry sectors.

e) Fiscal Trends

With an increase of 17%, the total expenditure incurred by the government grew from

$150 billion during the period April-January 2008-09 to $175 billion in the current

fiscal. In case of revenue receipts, the figures have also showed an increase of 5%

during the same period. As a result, the fiscal deficit increased moderately at the rate of

33% and went up from $58 billion to $77 billion during April-January 2009-10.

f) Foreign Investments

Foreign direct investment accumulated during the April-December period of 2009-10

stood at $26.5 billion, which was $2 billion higher than what was achieved previously.

Portfolio investments came in at $23.6 billion, compared to negative $11 billion in the

previous year. The rise in portfolio investments was particularly due to an increase in

FII investments.

g) Foreign Exchange Reserves

India's reserves as of March 2010 are at above $280 billion. In December 2009, the

forex was at $283.5 billion, increasing from $251 billion in April 2009. The forex, at

$283 billion, was less than the $286 billion achieved in the previous month of 2009.

15

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 16/147

The issues weighing down on the Indian economy are its unemployment rate and arather constant poverty rate. The unemployment rate grew in 2009 to 10.7% from

10.4% in 2008 and almost 25% of the population lives under the poverty line. In order

to combat this, the Indian administration is keen on encouraging privatization and

improving the employment scenario. Privatization will also attract FDI that can help in

structural improvements and thus trigger growth.

1.2 INSURANCE INDUSTRY

1.2.1 MEANING OF INSURANCE

Insurance is a form of risk management primarily used to hedge against the risk of a

contingent, uncertain loss. Insurance is defined as the equitable transfer of the risk of a

loss, from one entity to another, in exchange for payment.

Insurance is based on the law of large numbers. All who are exposed to a risk or a peril

contribute a relatively small sum to a common pool, which compensates the few who

suffer losses.

16

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 17/147

An insurer is a company selling the insurance; an insured or policyholder is the personor entity buying the insurance policy. The insurance rate is a factor used to determine

the amount to be charged for a certain amount of insurance coverage, called the

premium.

The transaction involves the insured assuming a guaranteed and known relatively small

loss in the form of payment to the insurer in exchange for the insurer's promise to

compensate insured in the case of a large, possibly devastating loss. The insured

receives a contract called the insurance policy which details the conditions and

circumstances under which the insured will be compensated.

TYPES OF INSURANCE

Insurance is generally classified into three main categories:

1. Life Insurance

2. Health Insurance

3. General Insurance

1.2.2 FUNCTIONS OF INSURANCE

a) PRIMARY FUNCTIONS

Providing protection – The elementary purpose of insurance is to allow security

against future risk, accidents and uncertainty. Insurance cannot arrest the risk from

taking place, but can for sure allow for the losses arising with the risk. Insurance is

in reality a protective cover against economic loss, by apportioning the risk with

others.

17

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 18/147

Collective risk bearing – Insurance is an instrument to share the financial loss. It isa medium through which few losses are divided among larger number of people. All

the insured add the premiums towards a fund, out of which the persons facing a

specific risk is paid.

Evaluating risk – Insurance fixes the likely volume of risk by assessing diverse

factors that give rise to risk. Risk is the basis for ascertaining the premium rate as

well.

Provide Certainty – Insurance is a device, which assists in changing uncertainty to

certainty.

b) SECONDARY FUNCTIONS

Preventing losses – Insurance warns individuals and businessmen to embraceappropriate device to prevent unfortunate aftermaths of risk by observing safety

instructions; installation of automatic sparkler or alarm systems, etc.

Covering larger risks with small capital – Insurance assuages the businessmen

from security investments. This is done by paying small amount of premium against

larger risks and dubiety.

Helps in the development of larger industries – Insurance provides an opportunityto develop to those larger industries which have more risks in their setting up.

c) OTHER FUNCTIONS

18

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 19/147

Is a savings and investment tool – Insurance is the best savings and investmentoption, restricting unnecessary expenses by the insured. Also to take the benefit of

income tax exemptions, people take up insurance as a good investment option.

Medium of earning foreign exchange – Being an international business, any

country can earn foreign exchange by way of issue of marine insurance policies and

a different other ways.

Risk Free trade – Insurance boosts exports insurance, making foreign trade risk free

with the help of different types of policies under marine insurance cover.

1.2.3 RISKS ASSOCIATED WITH INSURANCE SECTOR

As we all know Risk is the probability that a hazard will turn into a disaster.

Vulnerability and hazards are not dangerous, taken separately. But if they come

together, they become a risk or, in other words, the probability that a disaster will

happen.

TYPES OF RISKS

With regards to insurability, there are basically two categories of risks:

1. Speculative or Dynamic Risk

2. Pure or Static Risk

Speculative or Dynamic Risk

Speculative (dynamic) risk is a situation in which either profit OR loss is possible.

Examples of speculative risks are betting on a horse race, investing in stocks/bonds and

19

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 20/147

real estate. In the business level, in the daily conduct of its affairs, every businessestablishment faces decisions that entail an element of risk. The decision to venture

into a new market, purchase new equipments, diversify on the existing product line,

expand or contract areas of operations, commit more to advertising, borrow additional

capital, etc., carry risks inherent to the business. The outcome of such speculative risk

is either beneficial (profitable) or loss. Speculative risk is uninsurable.

Pure or Static Risk

The second category of risk is known as pure or static risk. Pure (static) risk is a

situation in which there are only the possibilities of loss or no loss, as oppose to loss or

profit with speculative risk. The only outcome of pure risks are adverse (in a loss) or

neutral (with no loss), never beneficial. Examples of pure risks include premature

death, occupational disability, catastrophic medical expenses, and damage to property

due to fire, lightning, or flood.

Types of Pure Risk

The major types of pure risk that are associated with great economic and financial

insecurity include:

1. Personal risk

2. Property risk

3. Liability risk

Personal risks are risks that directly affect an individual. They involve the possibility

of loss or reduction of income, of extra expenses, and the elimination of financial

20

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 21/147

assets.There are four major personal risks:

• Premature death

• Old age

• Poor health

• Unemployment

Premature death risk is defined as the risk of the death of the head of a household

with unfulfilled financial obligations. These can include dependents to support, a

mortgage to be paid off, or children to educate.

Old age is a risk of insufficient income during retirement. When older workers retire,

they lose their normal amount of earnings. Unless they have accumulated sufficient

assets from which to draw on, they would be facing a serious problem of economic

insecurity.

Risk of poor health includes both catastrophic medical bills and the loss of earned

income. The cost of health care has increased substantially in recent years. The loss of

income is another major cause of financial instability. In cases of severe long termdisability, there is a substantial loss of earned income, medical bills are incurred,

employee benefits may be lost, and savings depleted.

The risk of unemployment is another major threat to most families. Unemployment

can be the result of an industry cycle downswing, economic changes, seasonal factors

and frictions in the labour market. Regardless of the cause, unemployment can create

21

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 22/147

financial havoc in the average families by way of loss of income and employmentbenefits.

Property risk is the risk of having property damaged or loss from numerous perils.

Property loss can occur as a result of fire, lightning, windstorms, hail, and a number of

other causes.

Liability risks are another important type of pure risk that many people face. More than

ever, we are living in a litigious society. One can be sued for any frivolous reason. Onehas to defend himself when sued, even when the suit is without merit.

Nevertheless, risks can be reduced or managed. ‘Risk Management’ is an integrated

process that identifies, classifies, analyses & quantifies the financial impact of various

risks involved in running a business. It is a tool that recognizes the potential threats to

the business’s objectives and allows management to make informed decisions on the

appropriate course of action, be it to mitigate, transfer or allocate capital to the risk.

Risk management is not a new concept in life insurance and many of the basic

principles are as old as the insurance industry itself. The majority of companies already

have some form of risk management process in place. However, over recent years, there

has been significant progress in developing and formalizing these processes and even in

using them for regulatory purposes.

22

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 23/147

1.2.4 BENEFITS OF LIFE INSURANCE

Depending on its usage, life insurance gives various benefits. They are as follows:

• Income for Family Life: Insurance proceeds ensure a source of financial security for

your family to meet its household and living expenses.

• Payment of Debts: On the unfortunate death of the insured, the proceeds from a life

insurance policy can be used to meet outstanding debts such as mortgages, car loans or

charge account balances.

• Provide Education Funding For Children: The cash value of a whole life insurance

policy can be used to help accumulate funds for the higher education of insured’s

children.

• Equalize Inheritance: When an asset such as the family business passes on to family

members who are active in it, life insurance proceeds can be used to provide equal

assets to other family members Apart from these there are also Investment advantages

to the Insurance. While most investment options make a person’s money work harder,

they are no substitutes to life insurance. That's because when a person takes up a life

insurance policy, he enjoy the twin benefit of risk protection as well as returns on

savings.

• Life insurance enables a person to enjoy savings that guarantee full protection against

the risk of death of the insured. These long-term savings are made in an easy and

hassle-free manner because of low and convenient installments (or premiums).

23

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 24/147

• Life insurance also encourages 'forced thrift'. This means that the insured is made to

pay his/her premiums by saving his/her money, which he/she might not do in the

regular course of life.

• Some life insurance policies often allow insured to take loans against his policy,

should he require money to meet any unforeseen expenditure. What's more, some life

insurance policies also allow saving on taxes

1.2.5 BRIEF HISTORY OF INDIAN INSURANCE SECTOR

The insurance sector in India has completed all the facets of competition – from being

an open competitive market to being nationalized and then getting back to the form of a

liberalized market once again. The history of the insurance sector in India reveals that ithas witnessed complete dynamism for the past two centuries approximately.

I. IMPORTANT MILESTONES IN THE INDIAN LIFE INSURANCE

BUSINESS

With the establishment of the Oriental Life Insurance Company in Kolkata, the business

of Indian life insurance started in the year 1818.

1912: The Indian Life Assurance Companies Act came into force for regulating the life

insurance business.

1928: The Indian Insurance Companies Act was enacted for enabling the government to

collect statistical information on both life and non-life insurance businesses.

24

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 25/147

1938: The earlier legislation consolidated the Insurance Act with the aim of safeguarding the interests of the insuring public.

1956: 245 Indian and foreign insurers and provident societies were taken over by the

central government and they got nationalized. LIC was formed by an Act of Parliament,

viz. LIC Act, 1956. It started off with a capital of Rs. 5 crores and that too from the

Government of India.

II. IMPORTANT MILESTONES IN THE INDIAN GENERAL INSURANCE

BUSINESS

The history of general insurance business in India can be traced back to Triton

Insurance Company Ltd. (the first general insurance company) which was formed in the

year 1850 in Kolkata by the British.

1907: The Indian Mercantile Insurance Ltd. was set up which was the first company of

its type to transact all general insurance business.

1957: General Insurance Council, an arm of the Insurance Association of India, framed

a code of conduct for guaranteeing fair conduct and sound business patterns.

1968: The Insurance Act improved for regulating investments and set minimal solvency

levels and the Tariff Advisory Committee was set up.

1972: The General Insurance Business (Nationalization) Act, 1972 nationalized the

general insurance business in India. It was with effect from 1st January 1973.

107 insurers integrated and grouped into four companies, viz. the National Insurance

Company Ltd., the New India Assurance Company Ltd., the Oriental Insurance

25

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 26/147

Company Ltd. and the United India Insurance Company Ltd. GIC was incorporated as acompany.

1.2.6 INDIAN INSURANCE SECTOR REFORM

The formation of the Malhotra Committee in 1993 initiated reforms in the Indian

insurance sector. The aim of the Malhotra Committee was to assess the functionality of

the Indian insurance sector. This committee was also in charge of recommending the

future path of insurance in India.

The Malhotra Committee attempted to improve various aspects of the insurance sector,

making them more appropriate and effective for the Indian market.

The recommendations of the committee put stress on offering operational autonomy to

the insurance service providers and also suggested forming an independent regulatory

body.

In 1994, the committee submitted the report and some of the key recommendationsincluded:

1) Structure

• Government stake in the insurance Companies to be brought down to 50%.

• Government should take over the holdings of GIC and its subsidiaries so that

these subsidiaries can act as independent corporations.

• All the insurance companies should be given greater freedom to operate.

26

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 27/147

2) Competition

• Private Companies with a minimum paid up capital of Rs.1bn should be allowed

to enter the industry.

• No Company should deal in both Life and General Insurance through a single

entity.

• Foreign companies may be allowed to enter the industry in collaboration with

the domestic companies.

• Postal Life Insurance should be allowed to operate in the rural market.

• Only One State Level Life Insurance Company should be allowed to operate in

each state.

3) Regulatory Body

• The Insurance Act should be changed.

• An Insurance Regulatory body should be set up.

• Controller of Insurance (Currently a part from the Finance Ministry) should be

made independent.

4) Investments

• Mandatory Investments of LIC Life Fund in government securities to be

reduced from 75% to 50%.

• GIC and its subsidiaries are not to hold more than 5% in any company (There

current holdings to be brought down to this level over a period of time).

5) Customer Service

• LIC should pay interest on delays in payments beyond 30 days.

• Insurance companies must be encouraged to set up unit linked pension plans.

27

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 28/147

•

Computerisation of operations and updating of technology to be carried out inthe insurance industry The committee emphasized that in order to improve the

customer services and increase the coverage of the insurance industry should be

opened up to competition.

But at the same time, the committee felt the need to exercise caution as any failure on

the part of new players could ruin the public confidence in the industry. Hence, it was

decided to allow competition in a limited way by stipulating the minimum capital

requirement of Rs.100 crores. The committee felt the need to provide greater autonomy

to insurance companies in order to improve their performance and enable them to act as

independent companies with economic motives. For this purpose, it had proposed

setting up an independent regulatory body.

1.2.7 MAJOR POLICY CHANGES

Insurance sector has been opened up for competition from Indian private insurance

companies with the enactment of Insurance Regulatory and Development Authority

Act, 1999 (IRDA Act). As per the provisions of IRDA Act, 1999, Insurance Regulatory

and Development Authority (IRDA) was established on 19th April 2000 to protect the

interests of holder of insurance policy and to regulate, promote and ensure orderly

growth of the insurance industry. IRDA Act 1999 paved the way for the entry of private

players into the insurance market which was hitherto the exclusive privilege of public

sector insurance companies/ corporations. Under the new dispensation Indian insurance

companies in private sector were permitted to operate in India with the following

conditions:

• Company is formed and registered under the Companies Act, 1956;

28

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 29/147

•

The aggregate holdings of equity shares by a foreign company, either by itself or through its subsidiary companies or its nominees, do not exceed 26%, paid up

equity capital of such Indian insurance company;

• The company's sole purpose is to carry on life insurance business or general

insurance business or reinsurance business.

• The minimum paid up equity capital for life or general insurance business is

Rs.100 crores.

• The minimum paid up equity capital for carrying on reinsurance business has

been prescribed as Rs.200 crores.

1.2.8 IRDA

The Insurance Regulatory and Development Authority Act of 1999 brought aboutseveral crucial policy changes in the insurance sector of India. It led to the formation of

the Insurance Regulatory and Development Authority (IRDA) in 2000. The Authority

has its Head Quarters at Hyderabad.

The Authority is a ten-member team consisting of

a. Chairman; b. five whole-time members; c. four part-time members

All these positions are appointed by the Government of India.

The goals of the IRDA are to safeguard the interests of insurance policyholders, as well

as to initiate different policy measures to help sustain growth in the Indian insurance

sector.

29

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 30/147

The Authority has notified 27 Regulations on various issues which include Registrationof insurers, Regulation on insurance agents, Solvency Margin, Re-insurance, Obligation

of Insurers to Rural and Social sector, Investment and Accounting Procedure,

Protection of policy holders' interest etc. Applications were invited by the Authority

with effect from 15th August, 2000 for issue of the Certificate of Registration to both

life and non-life insurers. In 2010, the Government of India ruled that the Unit Linked

Insurance Plans (ULIPs) will be governed by IRDA, and not the market regulator

Securities and Exchange Board of India

Section 14 of IRDA Act, 1999 lays down the duties, powers and functions of IRDA.

Subject to the provisions of this Act and any other law for the time being in force, the

Authority shall have the duty to regulate, promote and ensure orderly growth of the

insurance business and re-insurance business.

DUTIES, POWERS AND FUNCTIONS OF IRDA

Section 14 of IRDA Act, 1999 lays down the duties, powers and functions of IRDA

1. Subject to the provisions of this Act and any other law for the time being

in force, the Authority shall have the duty to regulate, promote and ensure

orderly growth of the insurance business and re-insurance business.

2. Without prejudice to the generality of the provisions contained in sub-

section (1), the powers and functions of the Authority shall include,

1. issue to the applicant a certificate of registration, renew, modify,

withdraw, suspend or cancel such registration;

2. protection of the interests of the policy holders in matters

concerning assigning of policy, nomination by policy holders, insurable

30

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 31/147

interest, settlement of insurance claim, surrender value of policy andother terms and conditions of contracts of insurance;

3. specifying requisite qualifications, code of conduct and practical

training for intermediary or insurance intermediaries and agents;

4. specifying the code of conduct for surveyors and loss assessors;

5. promoting efficiency in the conduct of insurance business;

6. promoting and regulating professional organisations connected

with the insurance and re-insurance business;

7. levying fees and other charges for carrying out the purposes of

this Act;

8. calling for information from, undertaking inspection of,

conducting enquiries and investigations including audit of the insurers,

intermediaries, insurance intermediaries and other organisations

connected with the insurance business;

9. control and regulation of the rates, advantages, terms and

conditions that may be offered by insurers in respect of general

insurance business not so controlled and regulated by the Tariff Advisory Committee under section 64U of the Insurance Act, 1938 (4

of 1938);

10. specifying the form and manner in which books of account shall

be maintained and statement of accounts shall be rendered by insurers

and other insurance intermediaries;

11. regulating investment of funds by insurance companies;

12. regulating maintenance of margin of solvency;

13. adjudication of disputes between insurers and intermediaries or insurance intermediaries;

14. supervising the functioning of the Tariff Advisory Committee;

15. specifying the percentage of premium income of the insurer to

finance schemes for promoting and regulating professional

organisations referred to in clause (f);

31

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 32/147

16. specifying the percentage of life insurance business and generalinsurance business to be undertaken by the insurer in the rural or social

sector; and

17. exercising such other powers as may be prescribed

1.2.9 PRESENT SCENARIO OF THE INDUSTRY

The US$ 41-billion Indian life insurance industry is considered the fifth largest

life insurance market, and growing at a rapid pace of 32-34 per cent annually,

according to the Life Insurance Council.

Life Insurance Corporation of India (LIC) registered an 83 per cent increase in

new business income in March 2010, while private players posted a 47 per cent

growth in new business premium.

Moreover, according to IRDA, insurers sold 10.55 million new policies in 2009-

10 with LIC selling 8.52 million and private companies 2.03 million policies. At

the end of March 2010, LIC held 65 per cent market share in terms of new

business income collection with the private sector contributing the remaining 35

per cent share in 2009-10.

According to IRDA, total premium collected in 2009-10 was US$ 24.64 billion,

an increase of 25.46 per cent over US$ 19.64 billion collected in 2008-09.

A growth of 18 per cent is expected in total premium income and is likely to

cross the US$ 64.93 billion mark.

India insurance is a flourishing industry, with several national and international players

competing and growing at rapid rates. Thanks to reforms and the easing of policy

regulations, the Indian insurance sector been allowed to flourish, and as Indians become

32

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 33/147

more familiar with different insurance products, this growth can only increase, with theperiod from 2010 - 2015 projected to be the 'Golden Age' for the Indian insurance

industry.

Indian insurance companies offer a comprehensive range of insurance plans, a range

that is growing as the economy matures and the wealth of the middle classes increases.

The most common types include: term life policies, endowment policies, joint life

policies, whole life policies, loan cover term assurance policies, unit-linked insurance

plans, group insurance policies, pension plans, and annuities. General insurance plans

are also available to cover motor insurance, home insurance, travel insurance and health

insurance.

Due to the growing demand for insurance, more and more insurance companies are now

emerging in the Indian insurance sector. With the opening up of the economy, several

international leaders in the insurance sector are trying to venture into the India

insurance industry.

a. MARKET OVERVIEW

• The insurance industry in India is at an early stage with low penetration

and high potential.

• The total premium of the insurance industry has grown at a CAGR of

24.6 per cent from 2002–03 to 2008–09 to reach US$ 52.6 billion in

2008–09.

• The number of insurance players has increased from four and eight in

life and non-life sectors, respectively, in 2000 to 23 and 22, respectively,

as on January 2010.

b. GROWTH DRIVERS

33

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 34/147

• There is a high demand for insurance products due to a growing middleclass, increasing working population, rising household savings and

increasing purchasing power.

• Penetration levels set to increase

• The increasing literacy rate, especially in rural India, has spread

awareness about the need for insurance.

• Between 2006 and 2026, the working population (25–60 years) is

expected to increase from 675.8 million to 795.5 million giving rise to a

favourable market for insurance companies.

• Projected per capita GDP is expected to increase from US$ 380.8 in

2000–2001 to US$ 2,097.5 in 2026, reflecting higher disposable income.

• Favourable government and regulatory initiatives are expected to

increase the contribution of the insurance industry to the overall

economic development of the country.

c. OPPORTUNITIES

• High potential demand for insurance products

• Since more than two-thirds of India’s population lives in rural areas, micro-

insurance is seen as the most suitable aid to reach the poor and socially-

disadvantaged sections of society.

• Favourable demographics, fast progression of medical technology and

increasing demand for better healthcare have facilitated a high growth in health

insurance.

• Growing demand for Indian insurance offshoring business

34

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 35/147

•

Total revenues from Indian offshore insurance business process outsourcing(BPO) services are estimated to have increased from US$ 367 million in 2002–

03, US$ 790 million in 2006–07 to US$ 2 billion by 2009–2010.

• Employment is expected to more than double from 41,600 in 2005–06 to around

100,500 in 2009–2010

• Rising demand from semi-urban and rural population for micro-insurance

products

• The industry is also promoting micro-insurance as a viable business opportunity

and integrating the same with the poverty alleviation programmes of various

state governments.

• Poor insurance literacy and awareness, high transaction costs, inadequate

regulations and inadequate understanding of client needs and expectations have

restricted demand for micro-insurance products.

• However, with the development of rural health insurance regulations and

growing awareness about micro-insurance products, focus of many private

players has shifted to these areas.

1.2.10 INDIAN INSURANCE INDUSTRY - CHALLENGES

1. NEW COMERS

With more companies coming up every day, and the growing demand of the industry

makes the market very competitive. Until and unless the existing companies make a

mark and create their very own brand name it would be quite tough to sustain their

35

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 36/147

position in the market. There is also a probability of big companies taking over the newemerging companies.

2. SUPPLIER POWER

The people providing capital act as big terror as opportunity always lies in the big hands

and they can any day tempt good insurer from small companies to their own company.

3. BUYER POWER

Individuals never stand a chance in front of big corporate sectors as they dominate the

insurance industries with high potential of negotiation power.

4. PRESENCE OF SUBSTITUTES

The insurance industry is full of options and the large insurance companies offer the

same services as others, be it in any sector - home, commercial, auto, health or life.

Other key challenges include retention of talent, no benchmarks available for costing

and outdated risk tables and global level challenges like climate change, terrorism,

regulatory intervention, inflation, legal risks etc.

1.2.11 INDIAN INSURANCE INDUSTRY – GROWTH

36

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 37/147

OUTLOOK

Rising affluence is expected to increase the insurable population significantly by

2015. By then, 100 million people are estimated to be added to the working

population.

The India insurance sector is likely to put its foot forward towards more

competition with growing importance and recognition.

The Indian Insurance market is expected to be around US$52 billion

by 2010

Expected CAGR of over 30% p.a.

POTENTIAL OF THE INDUSTRY

o Largely untapped market with 17% of the world’s population

o Nearly 80% of the Indian population is without Life, Health and Non-life

insurance

o Strong economic growth with increase in affluence and rising risk awareness

leading to rapid growth in the insurance sector

o Innovative products such as Unit Linked Insurance Policies are likely to drive

future industry growth

o Investment opportunities exist in both life and non-life segments

o Total estimated investment opportunity of US$14-15 billion

37

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 38/147

POTENTIAL OF LIFE INSURANCE BUSINESS

• India’s life insurance market has grown rapidly over the past six years, with new

business premiums growing at over 40% per year.

• The premium income of India’s life insurance market is set to double by 2012

on better penetration and higher incomes.

• Insurance penetration in India is currently about 4% of its GDP, much lower

than the developed market level of 6-9%. It could rise to 5.1-6.2 by 2012 in

tandem with the country’s demographic profile.

• In several segments of the population, the penetration is lower than potential.

For example, in urban areas, the penetration of life insurance in the mass market

is about 65%, and it’s considerably less in the low-income unbanked segment.

In rural areas, life insurance penetration in the banked segment is estimated to

be about 40%, while it is marginal at best in the unbanked segment.

• The total premium could go up to $80-100 billion by 2012 from the present $40

billion as higher per capita income increases per capita insurance intensity.

• The average household premium will rise to Rs 3,000-4,100 from the current Rs

1,300 as will penetration by the existing and new players.

• Considering the world’s largest population and an annual growth rate of nearly 7

per cent, India offers great opportunities for insurers.

• US based online insurance company ebix.com plans to enter the Indian market

following deregulation of its insurance sector.

38

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 39/147

• Online insurer ebix.com’s expansion into India is a major step for the companyto become a global supplier of internet-based insurance tools for consumers and

insurance professionals.

• In a diverse country such as India it is imperative that a universal insurance

infrastructure be created to maximize efficiency in the insurance industry.

• Online insurer ebix.com can offer the Indian market a business-to-consumer

internet portal where consumers have more choice while purchasing insuranceand an internet-based agency management system that will help agents work

more efficiently with multiple carriers.

• Foreign holding in Indian insurance companies is limited to 26 per cent. The

government wants to increase the cap to 49 percent, but its communist allies

oppose such a move.

• The market is moving beyond single-premium policies and unit linked insurance

products which are easier to sell.

• The agency model is the dominant sales channel accounting for more than 85

per cent of fresh premiums but overall inactivity and attrition is much higher at

50-55 per cent than the global average of 25 per cent.

• Opportunities include health insurance and pensions, the report said; adding

only 1.5-2 per cent of total healthcare expenditure in India was currently

covered by insurance.

PENETRATION- LOWER THAN POTENTIAL

39

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 40/147

• Management consultancy firm McKinsey has forecast that India’s life insuranceindustry will be double in the next five years from $40 billion to $80-100 billion

in 2012. This growth would improve the level of insurance penetration from

5.1% of gross domestic product to 6.2% in 2010-2012.

• The Indian life insurance industry could witness a rise in the insurance sector

premiums between 5.1% and 6.2% of GDP in 2012, from the current 4.1%.

Total market premiums are likely to more than double during this period, from

about $40 billion to $80-100 billion. This implies a higher annual growth in new

business annual premium equivalent (APE) of 19% to 23% from 2007 to 2012.

• The large part of the growth would come from second- and third-tier cities and

small towns. Based on MGI forecasts, 26 tier-II cities with population greater

than one million and 33 tier-III towns with the population of more than 5 lakh

will account for 25% of the middle class and newly bankable class in 2025.

Over 5,000 tier-IV small towns will account for as much as 40% of these two

classes in 2025.

• However, if an insurer decided to be a niche player and concentrated on metros

and their suburbs, they will have a big market, since 60% of the very rich

(annual income over Rs 10 lakh) would be concentrated in the top eight cities.

Although these consumers will be highly accessible, players will have to reckon

with intense competition that is only going to increase and extend to other

segments as well.

1.2.12 PEST ANALYSIS

40

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 41/147

PEST analysis of any industry sector investigates the important factors that are affectingthe industry and influencing the companies operating in that sector. PEST is an

acronym for political, economic, social and technological analysis. Political factors

include government policies relating to the industry, tax policies, laws and regulations,

trade restrictions and tariffs etc. The economic factors relate to changes in the wider

economy such as economic growth, interest rates, exchange rates and inflation rate, etc.

Social factors often look at the cultural aspects and include health consciousness,

population growth rate, age distribution, changes in tastes and buying patterns, etc. The

technological factors relate to the application of new inventions and ideas such as R&D

activity, automation, technology incentives and the rate of technological change.

1) POLITICAL FACTORS

Increased service tax on premium

5% discount on corporate premium

Hike in FDI limit

Pricing control in general insurance

Favourable regulation for rural insurance

2) ECONOMIC FACTORS

Increase in Gross Domestic Savings

41

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 42/147

Increased economic activities

Interest rates

Inflation rate

3) SOCIAL FACTORS

Low insurance coverage

Rise in elderly population

Changing Indian perception

Growth of Islamic insurance

Increase in lifestyle diseases

Level of education

Level of earnings

4) TECHNOLOGICAL FACTORS

Automation of processes

Increase in CRM solutions

42

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 43/147

Internet driven information era

Business Process Monitoring (BPM)

1.2.13 LIFE INSURANCE COMPANIES IN INDIA

1) Life Insurer in Public Sector

Life Insurance Corporation of India

2) Life Insurers in Private Sector

SBI Life Insurance

Metlife India Life Insurance

ICICI Prudential Life Insurance

Bajaj Allianz Life

Max New York Life Insurance

Sahara Life Insurance

Tata AIG Life

HDFC Standard Life

Birla Sunlife

Kotak Life Insurance

43

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 44/147

Aviva Life Insurance

Reliance Life Insurance

ING Vysya Life Insurance

Shriram Life Insurance

Bharti AXA Life Insurance Co Ltd

Future Generali Life Insurance Co Ltd

IDBI Fortis Life Insurance

AEGON Religare Life Insurance

DLF Pramerica Life Insurance

Canara HSBC Oriental Bank of Commerce Life Insurance

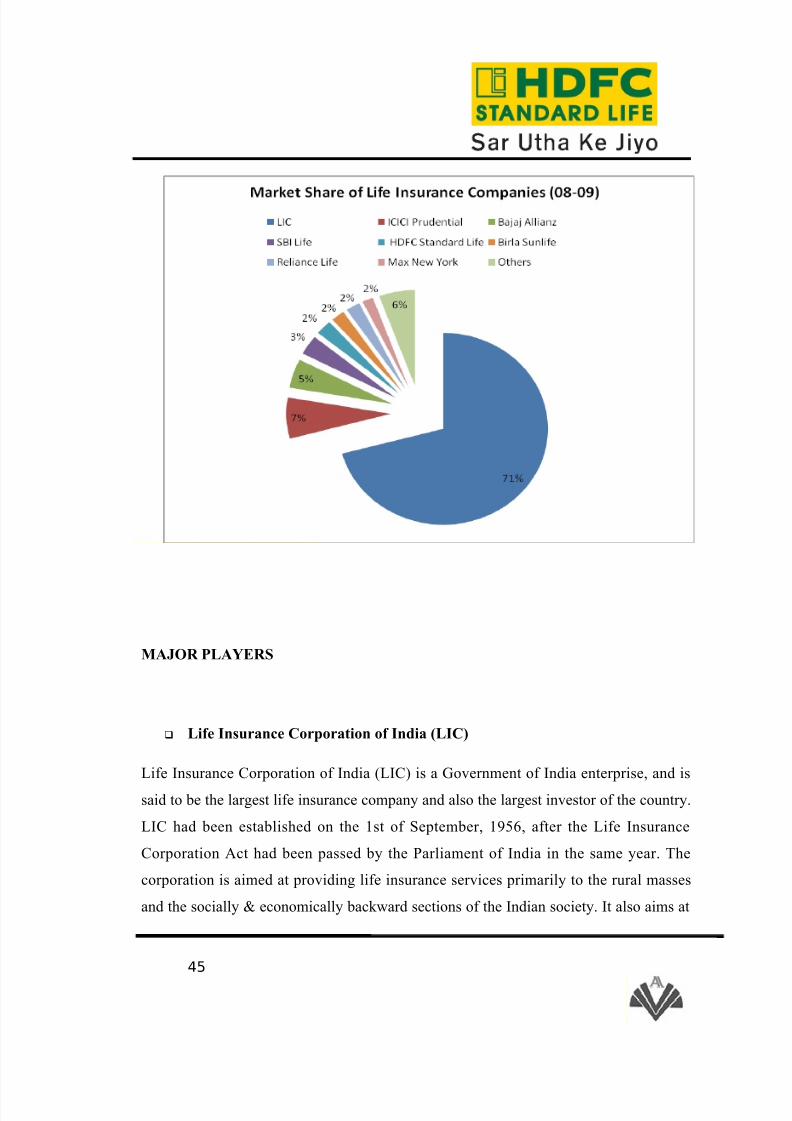

Chart 1.1

Chart showing market share of life insurance companies

44

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 45/147

MAJOR PLAYERS

Life Insurance Corporation of India (LIC)

Life Insurance Corporation of India (LIC) is a Government of India enterprise, and is

said to be the largest life insurance company and also the largest investor of the country.

LIC had been established on the 1st of September, 1956, after the Life Insurance

Corporation Act had been passed by the Parliament of India in the same year. The

corporation is aimed at providing life insurance services primarily to the rural masses

and the socially & economically backward sections of the Indian society. It also aims at

45

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 46/147

promoting the people for saving their money, and offers attractive savings featuresalong with various insurance policies.

HDFC Standard Life Insurance

Established on 14th August 2000, HDFC Standard Life Insurance Co. Ltd. is a joint

venture between Housing Development Finance Corporation Limited (HDFC Limited)

- India's leading housing finance institution, and a Group Company of the Standard Life

Plc, UK. The Company is one of leading private insurance companies, offering a range

of individual and group insurance solutions, in India. Being a joint venture of top

financial services groups, HDFC Standard Life has adequate financial expertise to

manage long-term investments safely and resourcefully.

Bajaj Allianz

Bajaj Allianz Life Insurance Co. Ltd. is a joint venture between Allianz SE, one of the

world's largest insurance companies, and Bajaj Finserv. Allianz SE is a leading

insurance corporation globally and one of the largest asset managers in the world, that

manage assets worth over a Trillion. With over 115 years of financial experience,

Allianz SE is present in over 70 countries around the world. Bajaj Allianz is into both

life insurance and general insurance. Today, Bajaj Allianz is one of India's leading and

fastest growing insurance companies. Currently, it has presence in more than 550

locations with over 60,000 Insurance Consultants.

ICICI Prudential Life Insurance

46

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 47/147

ICICI Prudential Life Insurance Company is a joint venture between ICICI Bank, whichis one of India's foremost financial services companies, and Prudential plc, which is a

leading international financial services group headquartered in the United Kingdom.

ICICI Prudential began the operations in December 2000. Today, this company has

over 2100 branches, which include 1,116 micro-offices, over 290,000 advisors and 18

banc assurance partners.

Max New York Life Insurance

Max New York Life Insurance Company Limited is a joint venture between Max India

Limited, which is a one of India's leading multi-business corporate, and New York Life

International, which is a Fortune 100 company & global expert in life insurance. Max

New York Life Insurance started its commercial operations in India in 2001. It is the

first life insurance company in India to be awarded the IS0 9001:2000 certification. The

company has around 133 offices all over the country.

Reliance Life Insurance

Reliance Life Insurance Company Limited is a part of Reliance Capital Ltd., a part of

Reliance - Anil Dhirubhai Ambani Group. Reliance Capital is one of India's leading

private sector financial services companies, which ranks among the top 3 private sector

financial services and banking companies. Reliance Life Insurance is not only one of

India's fastest growing life insurance companies, but also counts among the top 4

private sector insurers. In just 2 years, the Company has crossed the mark of 1.7 Million

policies.

47

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 48/147

SBI Life Insurance

SBI Life Insurance offers a slew of products designed for various segments of society.

These include money back products, pension products, protection cum savings

products, and unit linked products. All these products cater to various requirements of

its end users.

Birla Sun Life Insurance

Birla Sun Life Insurance Co. Ltd. is a joint venture between Aditya Birla Group, an

Indian multinational corporation, and Sun Life Financial Inc, a leading global insurance

company. Birla Sun Life Insurance is distinguished as the first company in the sector of

financial solutions to begin Business Continuity Plan. This insurance company has

pioneered the unique Unit Linked Life Insurance Solutions in India. Within 4 years of

its launch, BSLI became one of the leading players in the industry of Private Life

Insurance Scheme.

48

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 49/147

CHAPTER 2

COMPANY PROFILE

2.1 INTRODUCTION

Bharti AXA Life Insurance Co. Ltd. is a joint venture between Bharti - one of India’s

leading business groups with interests in telecom, agri business and retail, and AXA -

49

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 50/147

global leader in financial protection and wealth management. AXA's operations arediverse geographically, with major operations in Western Europe, North America and

the Asia/Pacific area. It also has operations in Australia, New Zealand, Hong Kong,

Singapore, Indonesia, Philippines, Thailand, China, India and Malaysia.

Bharti AXA Life Insurance has a 74% stake from Bharti and 26% stake of AXA in the

joint venture. In December 2006, the Company launched its operations in India. At

present, it has more than 5200 employees working over 12 states in the country. With

the continuous expansion, Bharti AXA Life Insurance is making itself proactive to cater

to insurance and wealth management needs of people.

2.1.1 PROMOTERS

1) BHARTI ENTERPRISES

Bharti Enterprises is one of India’s leading business groups with operations in over 21

countries across the globe with interests in telecom, financial services, retail, fresh and

processed foods, and real estate.

Bharti started its telecom services business by launching mobile services in Delhi

(India) in 1995. Bharti Airtel, the group's' flagship company, has emerged as one of the

top telecom companies in the world and is amongst the top five wireless operators in

the world. Through its global telecom operations Bharti group has presence in 21

countries across Asia, Africa and Europe - India, Sri Lanka, Bangladesh, Jersey,

Guernsey, Seychelles, Burkina Faso, Chad, Congo Brazzaville, Democratic Republic of

Congo, Gabon, Ghana, Kenya, Madagascar, Malawi, Niger, Nigeria, Sierra Leone,

50

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 51/147

Tanzania, Uganda, and Zambia.

Over the past few years, the group has diversified into emerging business areas in the

fast expanding Indian economy. With a vision to build India's finest conglomerate by

2020 the group has forayed into the retail sector by opening retail stores in multiple

formats - small and medium - as well establishing large scale cash & carry stores to

serve institutional customers and other retailers. The group offers a complete portfolio

of financial services - life insurance, general insurance and asset management - to

customers across India. Bharti also serves customers through its fresh and processed

foods business. The group has growing interests in other areas such as telecom

software, real estate, training and capacity building, and distribution of telecom/IT

products.

Partnerships

Over the years some of biggest names in international business have partnered Bharti.

Currently, Singtel, IBM, Ericsson, Nokia Siemens and Alcatel-Lucent are key partners

in telecom. Walmart is Bharti's partner for its cash & carry venture. Axa Group is the

partner for the financial services business and Del Monte Pacific for the processed

foods division.

Vision

To build India's finest conglomerate by 2020.

51

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 52/147

Values

Empowerment

Entrepreneurship

Transparency

Impact

Flexibility

GROUP COMPANIES

i. Bharti Airtel

Bharti Airtel Limited is a leading emerging market telecom services provider with

operations in 18 countries across Asia and Africa. The company is structured into four

strategic business units - Mobile, Telemedia, Enterprise and Digital TV. The mobile

business offers services across 18 countries in Asia and Africa. The Telemedia business

provides broadband, IPTV and telephone services across India. The Enterprise business

provides end-to-end telecom solutions to corporate customers and national and

international long distance services to carriers. The Digital TV business provides DTH

services across India. All these services are provided under the Airtel brand.

ii. Bharti Infratel Limited

Bharti Infratel Limited is amongst India's leading telecom passive infrastructure service

providers. The company deploys, owns and manages telecom towers and

communication structures, for various mobile operators across 18 states of India. It has

a vast footprint of over 30,000+ towers and holds a 42% take in Indus Towers Ltd - a

Joint Venture between Bharti Infratel, Vodafone & Idea Cellular - that has the

52

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 53/147

distinction of being the world's largest tower company. Bharti Infratel has not onlypioneered the passive infrastructure space in the Indian telecom sector, but has also

continued to lead the industry in developing and providing innovative solutions and

setting service delivery benchmarks.

iii. Bharti Realty Limited

Bharti Realty Limited is a young, vibrant and dynamic realty company with expanding

interests in commercial, retail and residential real estate. It has grown from strength to

strength, constructing and managing over ten top of the line facilities for Bharti group

companies and third party clients. Spurred by its accomplished success and acquired

expertise, Bharti Realty Limited has now forayed into developing quality commercial

real estate in the central business district (CBD) areas of metropolitan cities, retail real

estate in the up-market localities of metropolitan cities and in a few prominent cities of

Punjab, and high end residential real estate in the Delhi NCR region, Mumbai and

Bangalore.

iv. Beetel Teletech Limited

Beetel Teletech Limited is a sales and distribution company with focus on emerging

markets of SAARC, Middle East, Africa, Latin America and is engaged into

distribution & marketing of wide range of products that include Smart Phones, High

quality cordless phones, Modems, Audio / video conferencing products, Free To Air Set

Top Boxes, Fixed Cellular Phones & Fixed Wireless Terminals.

v. Comviva

Comviva is a global player in offering mobile solutions beyond VAS. With an extensive

portfolio of products and solutions that encompass content, commerce and community-

related offerings, Comviva enables mobile operators to offer services that enrich users’

53

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 54/147

lives. Comviva enhances operator efficiencies and revenue performance by addingvalue at every stage of the customer lifecycle – from prepaid subscription and etop-up

to customer care, and from real-time promotions and loyalty management to billing

solutions. Comviva has extensive expertise in delivering and managing mobile

solutions that extend beyond VAS, powering solutions to mobile operators in more than

80 countries worldwide and reaching over 550 million subscribers globally.

vi. Jersey Airtel and Guernsey Airtel

Jersey Airtel and Guernsey Airtel are subsidiaries of Bharti group and offer mobile

services on the islands of Jersey and Guernsey respectively in the Channel Islands

(Europe). All services are offered under the Airtel-Vodafone brand under a partnership

to bring a range of Vodafone global products together with other exciting services from

Bharti to customers in Jersey and Guernsey.

vii. Centum Learning Limited

Centum Learning Limited provides end-to-end learning and skill-building solutions that

enhance business performance to Bharti Group and several large corporates. Centum

Learning has received the Gold Award for "Excellence in Training" at the World HRD

Congress, 2010 and has been adjudged as one of the ' Top 15 Emerging Leaders in

Training Outsourcing' 2009 Worldwide. Centum Learning provides industry oriented

employability programmes through a network of 130 Centum Learning Centers spread

across 90 cities. It has also launched a new education initiative, Centum U – Institute

of Management & Creative Studies which offers UG and PG programmes in association

with world renowned institutions.

viii. Bharti Walmart

54

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 55/147

Bharti Walmart is a B2B joint venture between Bharti Enterprises and Walmart for wholesale cash & carry and back-end supply chain management operations in India to

serve small retailers, manufacturers, institutions and farmers. The Company operates

Cash & Carry stores under the Best Price Modern Wholesale brand. A typical cash-and-

carry store stands between 50,000 and 100,000 square feet and sells a wide range of

fresh, frozen and chilled foods, fruits and vegetables, dry groceries, personal and home

care, hotel and restaurant supplies, clothing, office supplies and other general

merchandise items.

ix. Bharti Retail

Bharti Retail is a wholly owned subsidiary of Bharti Enterprises. The Company

operates easyday neighborhood stores and compact hypermarket stores called easyday

Market. Bharti Retail provides consumers a wide range of good quality products at

affordable prices. easyday stores are a one stop shop that cater to every family's day-to-

day needs. Merchandise at easyday Market stores include apparels, home furnishings,appliances, mobile phones, meat shop, general merchandise, fruits and vegetables

among others.

x. Bharti AXA Life Insurance

Bharti AXA Life Insurance is a joint venture between Bharti and AXA Group.The

company launched national operations in December 2006. Today, Bharti AXA Life has

a national footprint of distributors trained to provide quality financial advice and

insurance solutions to the large Indian customer base. Bharti AXA Life offers a range

of innovative products and services that cater to specific insurance and wealth

management needs of customers.

xi. Bharti AXA General Insurance

55

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 56/147

Bharti AXA General Insurance is a joint venture between Bharti Group and AXAGroup. The company is one of the fastest growing in the general insurance segment and

is the first in the industry to receive dual certifications of ISO 9001:2008 & 27001:2005

within the a year of launching operations. The company offers an extensive product

range for retail, rural and commercial clients with cashless facilities in over 4000

hospitals and 1600 garages as well as 24/7 multi-modal claims registration.

xii. Bharti AXA Investment Managers

Bharti AXA Investment Managers Private Limited is a joint venture between Bharti and

the AXA Group. With a presence in more than 34 locations across the country within

one year of the launch, Bharti AXA Investment Managers boasts one of the largest

footprints for any AMC in the country during launch. This indicates the retail focus of

the AMC. With best practices brought in from world leaders in financial protection,

Bharti AXA Investment Managers aim to be an aggressive player in the Indian Asset

Management Industry.

xiii. Indus Towers

Indus Towers, a JV between Vodafone Essar (42%), Bharti Group (42%) and Aditya

Birla Telecom Limited (16%) and is India’s leading mobile towers company. The

company, which operates in 16 telecom circles across India, provides services to all

telecom operators and other wireless service providers such as as broadcasters and

broadband service providers on non-discriminatory basis.

xiv. FieldFresh Foods Pvt. Ltd

56

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 57/147

FieldFresh Foods Pvt. Ltd, a joint venture company between Bharti Enterprises and DelMonte Pacific Ltd. The company offers branded FieldFresh fruits & vegetables across

India and international markets, including Europe and the Middle East. The company

produces markets and distributes farm fresh products. FieldFresh Foods Pvt. Ltd, aims

to become one of the most trusted provider of premium quality fresh farm products,

processed foods and beverages.

2) AXA GROUP

AXA Group is a worldwide leader in Financial Protection. AXA’s operations are

diverse geographically, with major operations in Europe, North America and the

Asia/Pacific area. In 2009, total revenues amounted to Euro 90.1 billion and total

revenues underlying earnings to Euro 3.9 billion. AXA had Euro 1,014 billion in assets

under its management as of December 31, 2009.

AXA is a French global insurance group headquartered in Paris. AXA is a

conglomerate of independently run business, operated according to the laws and

regulations of many different countries.

The AXA group of companies are engaged in life, health and other forms of insurance,

as well as investment management. The AXA group operates primarily in Western

Europe, North America and the Asia Pacific region and the Middle East.

57

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 58/147

The AXA Group encompasses five operating business segments: Life & Savings,Property & Casualty, International Insurance (including reinsurance), Asset

Management and Other Financial Services.

AXA ranks as the 73rd largest company in the world (based on revenue) on the

2009 Fortune Global 500 list.

In the financial markets, AXA is positioned as a global leader in Financial Protection

with:

•96 million clients worldwide

•216 095 employees 400,000 individual shareholders

•90.1 billion euros in revenues

Commitments

AXA aspired to do business responsibly, and to build trust-based relationships with its

stakeholders:

♦ Clients: Consistently deliver efficient local service and adapted solutions, while

adhering to the highest standards of professional conduct.

♦ Shareholders: Create lasting value by achieving operating performance that

ranks among the best in the industry, and provide transparency financial

information.

♦ Employees: Ensure professional fulfilment by offering a supportive and

respectful workplace where people are empowered and the continuous

development of competencies is encouraged.

58

8/7/2019 09VWCMA056 NAINA LAZARUS

http://slidepdf.com/reader/full/09vwcma056-naina-lazarus 59/147

♦ Suppliers: Maintain excellent supplier relationships by adhering to a set of clearly defined procurement guidelines and promoting ongoing dialogue.

♦ Community: Act as a responsible corporate citizen by sharing our professional

expertise with the community and sponsoring philanthropic initiatives.