03.12.04 PPT on Frauds.ppt - SIRC of ICAI onoonnon frauds in banking industry ddddetection, ,, ,...

26

PRESENTATION PRESENTATION PRESENTATION PRESENTATION ON ON ON ON FRAUDS IN BANKING INDUSTRY FRAUDS IN BANKING INDUSTRY FRAUDS IN BANKING INDUSTRY FRAUDS IN BANKING INDUSTRY D D DETECTION ETECTION ETECTION ETECTION, , , , C C CLASSIFICATION LASSIFICATION LASSIFICATION LASSIFICATION AND AND AND AND R R REPORTING EPORTING EPORTING EPORTING & & & DISCUSSION DISCUSSION DISCUSSION DISCUSSION OF OF OF OF CASE CASE CASE CASE STUDIES STUDIES STUDIES STUDIES By By By By CA.T.G.Sukumaran B.Com.,FCA,CAIIB

Transcript of 03.12.04 PPT on Frauds.ppt - SIRC of ICAI onoonnon frauds in banking industry ddddetection, ,, ,...

PRESENTATION PRESENTATION PRESENTATION PRESENTATION

ONONONON

FRAUDS IN BANKING INDUSTRYFRAUDS IN BANKING INDUSTRYFRAUDS IN BANKING INDUSTRYFRAUDS IN BANKING INDUSTRYDDDDETECTIONETECTIONETECTIONETECTION, , , , CCCCLASSIFICATIONLASSIFICATIONLASSIFICATIONLASSIFICATION ANDANDANDAND RRRREPORTINGEPORTINGEPORTINGEPORTING

&&&& DISCUSSIONDISCUSSIONDISCUSSIONDISCUSSION OFOFOFOF CASECASECASECASE STUDIESSTUDIESSTUDIESSTUDIES

ByByByBy

CA.T.G.SukumaranB.Com.,FCA,CAIIB

CONTENTS

� Various types of Frauds

� Causes and Concern

� Detection of Frauds

� Reporting of Frauds � Reporting of Frauds

� Fraud Risk and Risk mitigation

� Prevention and Control

� Role of Concurrent Auditors

� A few Case Studies in various departments of Banks

DEFINING ‘FRAUD’

In General – as per Contract Law

� A deception deliberately practiced in order to secure unfair or unlawful gain or causing loss to another party

In Banking as per RBI

� “..a deliberate act of omission or commission by any � “..a deliberate act of omission or commission by any person, carried out in the course of a banking

transaction or in the books of account maintained

manually or under computer system in banks, resulting

into wrongful gain to any person for a temporary period

or otherwise, with or without any monetary loss to the

bank.”

WWHYHY & HOW& HOW

Why fraud is committed� Motive mainly greed ,making effortless money

� Pressure due to commitment

� Opportunity caused by laxity /ignorance of colleagues

� Life style not commensurate with income

How fraud is committed:How fraud is committed:

1. Laxity in observance in the laid down systems and procedure by

operational staff and also by supervising staff.

2. Policies / Systems and procedures are not being followed

deliberately with malafide intention.

3. Lethargy, Negligence ,and ignorance

4. Misutilisation/overstepping of lending/discretionary powers in

credit dispensation etc.

TYPES OF FRAUDS

� INSIDER

Frauds by dishonest employee/s

� OUTSIDER

Customer/s or outsider/s

� BOTH COLLUDING

Clients in connivance with the Employees Clients in connivance with the Employees

Frauds reported can be broadly divided into two groups

Technology / operational -

More number of incidences but with lesser values

viz. credit card, ATM, inoperative accounts, etc.,

Advances related -

Accounting for major amount involved ,

but less number of accounts

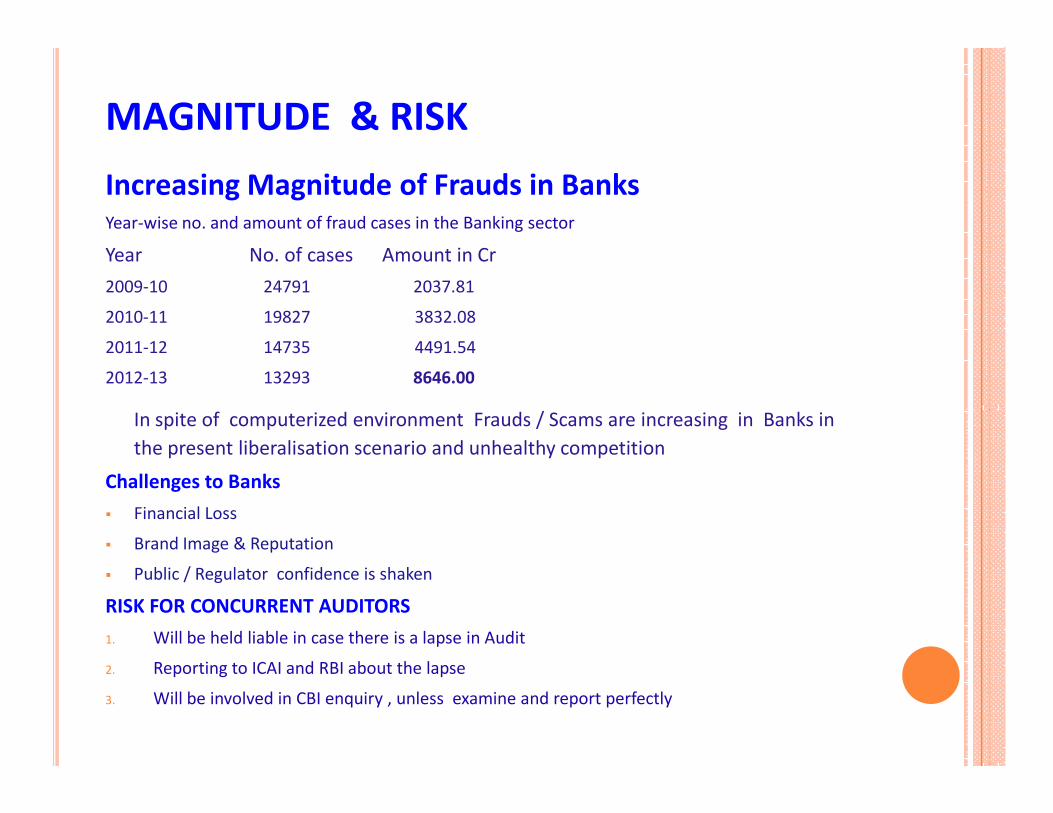

MAGNITUDE & RISK

Increasing Magnitude of Frauds in Banks Year-wise no. and amount of fraud cases in the Banking sector

Year No. of cases Amount in Cr

2009-10 24791 2037.81

2010-11 19827 3832.08

2011-12 14735 4491.54

2012-13 13293 8646.00

In spite of computerized environment Frauds / Scams are increasing in Banks in In spite of computerized environment Frauds / Scams are increasing in Banks in

the present liberalisation scenario and unhealthy competition

Challenges to Banks

� Financial Loss

� Brand Image & Reputation

� Public / Regulator confidence is shaken

RISK FOR CONCURRENT AUDITORS

1. Will be held liable in case there is a lapse in Audit

2. Reporting to ICAI and RBI about the lapse

3. Will be involved in CBI enquiry , unless examine and report perfectly

VARIOUS TYPES IF INSIDER INVOLVEMENT

� Misappropriation of Cash remitted by customers

� Intentional misposting to fraudster accounts

� Unauthorised withdrawal from deposit accounts through forged

instruments

� Passing fictitious entries in Books/System and manipulation of

records

� Theft of jewels pledged by the Customers� Theft of jewels pledged by the Customers

� Draw money using Limits not cancelled in system after repayment

� Misuse of Password sharing for transfer of funds to fraudster

accounts

� Misusing security forms like DDs , payorders, FD Receipts

� Misutilisation/overstepping of lending/discretionary powers, non-

observance of prescribed norms/ procedures in credit dispensation

VARIOUS TYPES OF OUTSIDER DEFRAUDING

� Fudging of financials /falsification of records

� Suppressing sundry creditors /over stating the sundry debtors

� Over valuing the stock to match DP with the credit limits.

� Arranging stocks in their godown only when bank comes for Inspection

� Collaterals lodged with the bank are inadequate or valueless.

� Hypothecated stocks are sold but the godown is set on fire to show loss of

stock is due to firestock is due to fire

� Taking loan from multiple banks with the same stocks

� Obtaining loan from forged/colour Xerox of documents

� Middle men availing overdrafts against fraudulent dischharge of Fixed

deposit Receipts

� Phishing ( anonymous e mail) , vishing ( voice), Smishing ( SMS) or

whaling ( targeting HNW clients) to elicit sensitive data in Hi Tech Banking

� Kite Flying / raising of accommodation bills in availing Bills Purchase

Facility

TYPES OF FRAUD BY

INSIDER / OUTSIDER COLLUSION

� Bribe / Commission for doing a favour to customer or credit decisions

� Over appraisal of Primary / collateral securities

� Unauthorised restructuring / extension

� Write off of recoverable amounts

� Advances sanctioned at the behest of top management

� Purchase of bills with out goods / cheques to accommodate the

borrower

� Disbursement of credit knowing diversion of funds

� Extending additional credit facility to prevent slippage of existing

facility into NPA

� Deliberately giving false credit rating to reduce Rate of Interest.

� Sanction of one time adhoc credit facilities to non-clients,

� Issue of letter of credit, bank guarantees without recording in branch

books

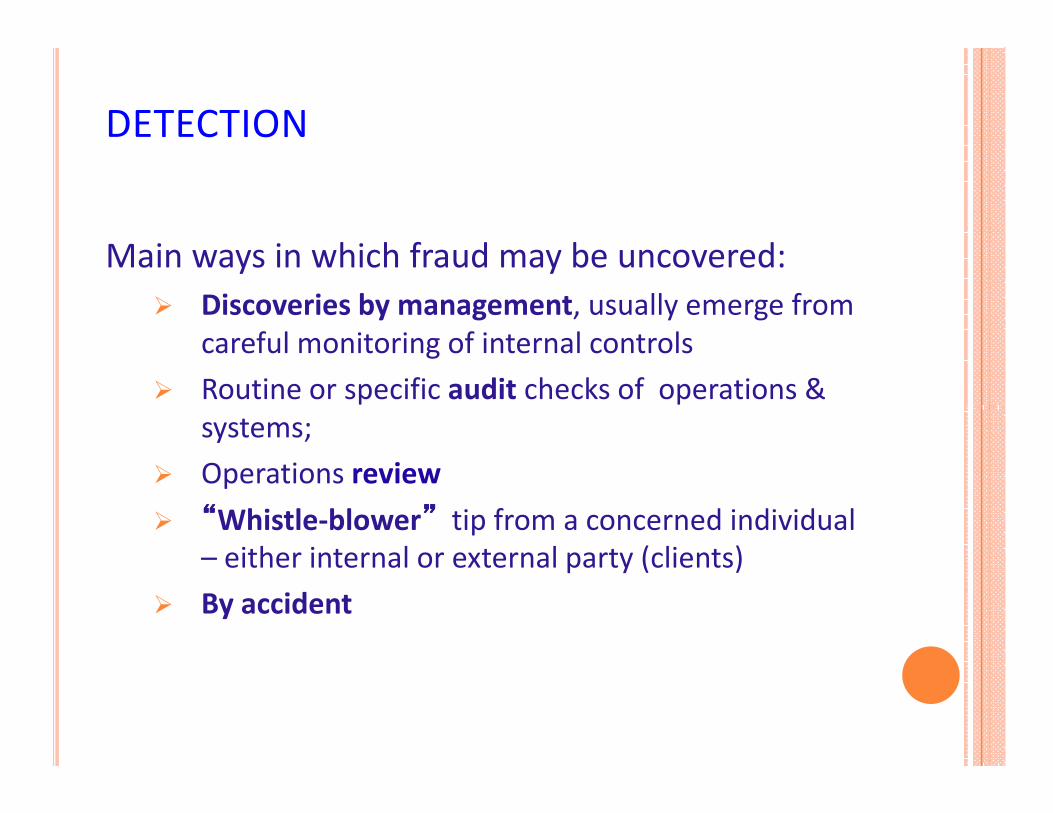

DETECTION

Main ways in which fraud may be uncovered:

� Discoveries by management, usually emerge from

careful monitoring of internal controls

� Routine or specific audit checks of operations &

systems;

� Operations review

� ““““Whistle-blower”””” tip from a concerned individual

– either internal or external party (clients)

� By accident

TIPS FOR DETECTION

� Check proper implementation of management controls

� Check for 100% compliance in sensitive / fraud prone areas

� Examine impersonal accounts ( direct GL Heads)

� Plug shortcuts evolved by branch functionaries

� Check KYC norms strictly in all account opening

� Check Suspicious Transaction Report , Cash Transaction Reports

� Check all large volume Transactions in the newly opened accounts � Check all large volume Transactions in the newly opened accounts

� No staff to sit in the same seat continuously i.e rotation of duty is

must

� Do documentation checks

� Do trend analysis, verify abnormal transactions

� Review properly-generated MIS reports

� competent, courageous, and efficient audit,

� Do field visits for asset verification

� Keep your eyes and ears open for observing what is happening in

the branch

DEPOSIT ACCOUNT FRAUDS

� Withdrawal from deposit accounts through forged

documents/instruments , mostly from inoperative accounts

� Transfer of funds to a fraudster account mostly fictitious through RTGS

/ NEFT

� The miscreant obtains/steals the cheque, materially alters the

particulars of cheques and presents over the counter for

payment/collection in the account with fake KYC documents

Payments of cheques under forged signatures, generally perpetrated � Payments of cheques under forged signatures, generally perpetrated

by the employees/partners/relatives of the account-holders.

� Daily deposit collections from traders & hawkers are not deposited next

working day

� Employee becomes joint account holder and withdraws the money.

� Manipulates the depositor’s Pass Book to conceal the facts

� Staff members including Branch Head indulging in fraudulent use of

cash deposited and concealing

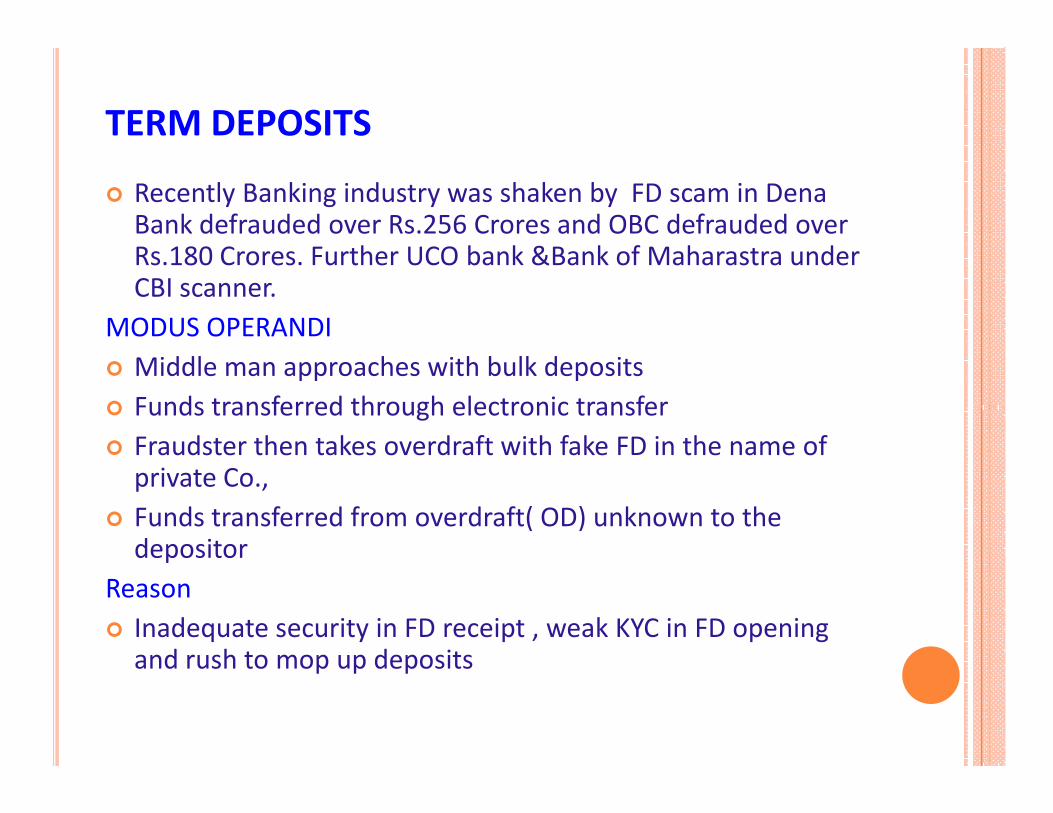

TERM DEPOSITS

� Recently Banking industry was shaken by FD scam in Dena Bank defrauded over Rs.256 Crores and OBC defrauded over Rs.180 Crores. Further UCO bank &Bank of Maharastra under CBI scanner.

MODUS OPERANDI

� Middle man approaches with bulk deposits

� Funds transferred through electronic transfer� Funds transferred through electronic transfer

� Fraudster then takes overdraft with fake FD in the name of private Co.,

� Funds transferred from overdraft( OD) unknown to the depositor

Reason

� Inadequate security in FD receipt , weak KYC in FD opening and rush to mop up deposits

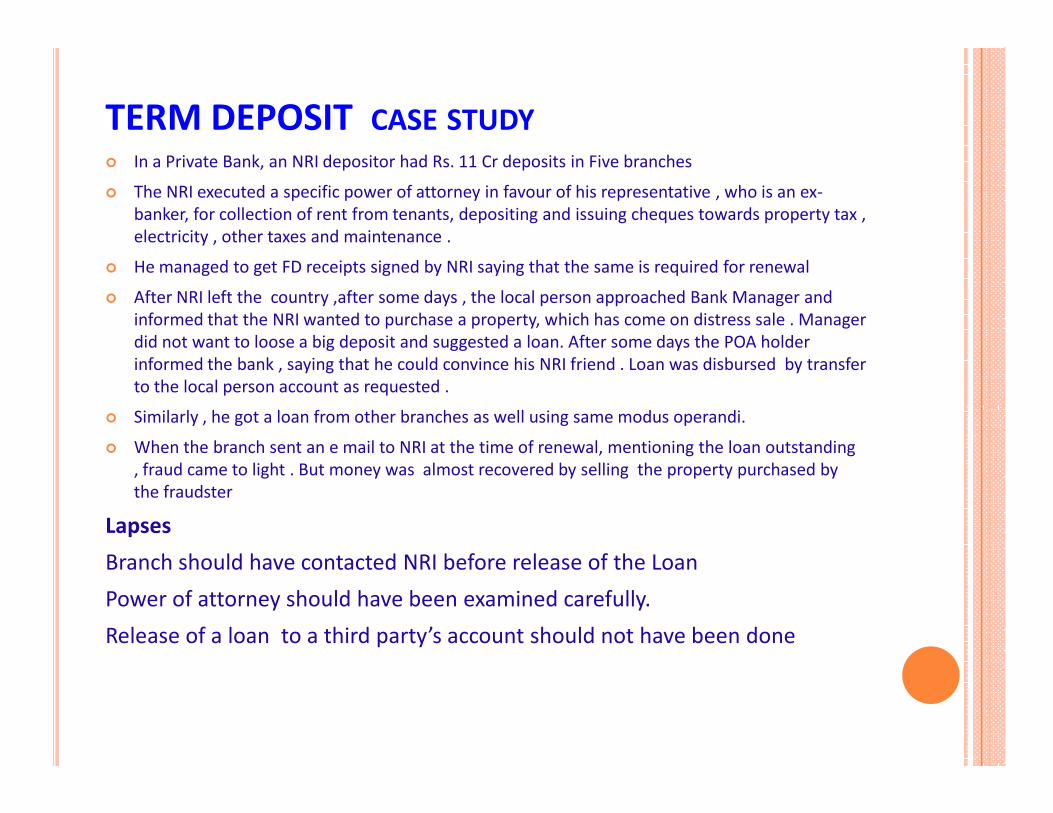

TERM DEPOSIT CASE STUDY

� In a Private Bank, an NRI depositor had Rs. 11 Cr deposits in Five branches

� The NRI executed a specific power of attorney in favour of his representative , who is an ex-

banker, for collection of rent from tenants, depositing and issuing cheques towards property tax ,

electricity , other taxes and maintenance .

� He managed to get FD receipts signed by NRI saying that the same is required for renewal

� After NRI left the country ,after some days , the local person approached Bank Manager and

informed that the NRI wanted to purchase a property, which has come on distress sale . Manager

did not want to loose a big deposit and suggested a loan. After some days the POA holder

informed the bank , saying that he could convince his NRI friend . Loan was disbursed by transfer

to the local person account as requested .

Similarly , he got a loan from other branches as well using same modus operandi.� Similarly , he got a loan from other branches as well using same modus operandi.

� When the branch sent an e mail to NRI at the time of renewal, mentioning the loan outstanding

, fraud came to light . But money was almost recovered by selling the property purchased by

the fraudster

Lapses

Branch should have contacted NRI before release of the Loan

Power of attorney should have been examined carefully.

Release of a loan to a third party’s account should not have been done

CHEQUES / BILLS PURCHASED

� Bogus or stolen railway receipts and Lorry receipts accompanied by

counterfeit bills are discounted.

� Fake bills with inflated value, drawn on sister concerns, are discounted.

� Genuine LRs and RRs are presented and got discounted from the bank but

the material is got released from the lorry godown/ railways on indemnity

bond.

� Bogus bills for worthless goods are discounted on the strength of dispatch � Bogus bills for worthless goods are discounted on the strength of dispatch

papers.

� Cheque purchase for huge amounts with out proper authority

� Kite flying / raising of accommodation bills

� Not crystallizing the bills remaining outstanding beyond due dates

� Bills purchased with out regular sanction limit or proper authority

� Bills remaining unrealized for a long period after due dates

FOREX

� LC devolvement (Importer not meeting the commitment in bills under LC

on due dates)

� Disbursement of Packing credit without verifying actual purchase of raw

material goods

� Fictitious buyer incase of export bills

� Purchase of bills with forged acceptance of LC by other banks

� Frequent overdue crystallization of bills

LC / PC / BP sanction with out authority � LC / PC / BP sanction with out authority

� Frequent request for extension of time ( Roll over ) for payment of bills

finance

� Not adhering to the stipulations in respect of ECGC cover such as payment

of premium and reporting of default in time

� Proper KYC in respect of opening of NRI accounts

� Monitoring huge inflow in NRE accounts and checking of huge transfers

from these accounts

� Inexperience of staff in this specialized operations

CASH & JEWEL LOANS

CASH

� Most sensitive Asset in Bank prone to fraud

� Misappropriation of Cash remitted and concealment

� Security lapses leading to decoity

� Shortage in cut / soiled notes

JEWEL LOANS JEWEL LOANS

� Appraiser defrauding

� Fake / stolen / less quality jewels

� Branch Head using pledged jewels to pledge with some other Banks

to raise money for his use

� Not adhering to key handling procedures

LOAN ACCOUNT FRAUDS

� Advance granted in haste or at the behest of top management or

any pressure or some consideration.

� False or incomplete credit information

� Lack of post disbursement supervision.

� End use not ensured / allowing diversion of funds

Mis-use / exceeding of discretionary powers by Managers/Officers� Mis-use / exceeding of discretionary powers by Managers/Officers

� Nomadic artisans obtain loans and vanish from the scene.

� Bogus firms appear everywhere and obtain loans.

� In connivance with the suppliers, machinery bills are inflated.

� Advance against hypothecation of inferior quality of goods,

overvaluation of stock

ADVANCES FRAUD --EXAMPLES

� In 2013-14 , advances against Fake documents amounts

to Rs 8734 Cr in Banks

� In Bank of Maharashtra , Rs. 3.70 Cr fraud in Vehicle

loans in a particular branch with out purchase of vehicle loans in a particular branch with out purchase of vehicle

in collusion with automobile dealer with fake bills

� Even in SHG , 3 women started fake trust and with

forged doc raised loans of Rs. 1.23 Cr

CREDIT FRAUDS – CASE STUDY

� In an advance to a business concern , balance sheet was fudged to

be healthy , Auditors signature was also forged . Even previous Bank

statement and opinion was forged

� Advance was released . Later after becoming NPA , the fraud came

to surface , when internal inspector found the contradiction in

opinion and bank statement

LAPSESLAPSES

� Concurrent Auditor was asked explanation , Then he could be

exonerated only due to the fact that document forging can not be

detected with naked eye

� Lapse on the Bank part here is that the statement , opinion of the

previous Bank was not verified with them

RETAIL LOAN FRAUD CASE

� A lady approached “A” branch of a Bank for Housing Loan for purchase of a Flat . In

this case she was asked to take legal opinion from bank’s panelled advocate . She

took the letter to advocate and got legal opinion with documents. in a cover

� Then she removed Original title deeds , put colour xerox and handed over to Bank ,

Loan was released

� Later she went to “ B “ branch of the same bank saying that legal opinion is taken

and there is delay in sanction by “ A “ branch . Then “B” branch released the loan for

same property

� The fraud came to light when she approached “C” branch and applied same trick.

� The branch manager got some doubt and telephoned to B Branch which happened

to be his previous branch and found that lady has obtained loan with colour xerox .

LAPSES

Omission to Obtain legal opinion by sending branch staff

Post sanction verification not done ,

Subsequent EC after SRO registration was not taken

B branch should have contacted A branch about delay

REPORTING AND INVESTIGATION

� Frauds as soon as detected should be informed to Top

management by a flash report

� Branch should Report to Vigilance department ( CVC)

� Depending on the amount involved , a complaint should

be lodged to Police , Crime Investigation dept of State or

CBI CBI

� Investigation will be initiated by the vigilance

department internally

� Delay in reporting due to hesitation and may

lead to further loss.

PREVENTION

� Minimize motivation to commit fraud:

� Hire and attract honest well-suited staff

� Provide reasonable and competitive staff remuneration

� Do employee lifestyle check

� Have suitable policies for fraud and dishonesty

� Close the window of opportunity to commit fraud:� Close the window of opportunity to commit fraud:

o Evaluate Bank’s Internal Control System effectiveness, its

policies and implementation, based on identified risk areas.

o Strictly follow the time tested procedures / guidelines

PRECAUTIONS TO BE TAKEN

BY CONCURRENT AUDITORS

� In case a fraud is committed in the branch and if there is a lapse on

the part of auditor , there is no protection

� Report only what is seen , not on Trust

� 100 % checking in fraud prone areas

� See what is happening around you and interact with staff to elicit

information

� Analyse large value Transaction in staff accounts and abnormal � Analyse large value Transaction in staff accounts and abnormal

Transactions in business accounts

� Be courageous in reporting , not to compromise

� Employ efficient Assistants

� Auditor should act as per instruction of Central Office and not be

guided by Branch information

� Give qualified reports , if not satisfied or not getting information

� Report by flash , once fraud is detected

CONSTRAINTS FOR CONCURRENT AUDITORS

� Auditors face time constraint as report insisted mostly first week of

the month

� Comparatively poor Remuneration

� Non co operation and no seriousness from Branch Officials

� Information / Returns / Documents not furnished in time

� Access to System disrupted often and not restored fast

� In experience of the Assistants

� In the present target oriented , competitive banking deviations are

high

� Incompetence of elderly staff and sub staff promotee in branches

to retrieve required information in the CBS Technology

� Considering the fraud risks , DOMOCLE’S SWORD IS HANGING

ABOVE

CONCLUSION

If financial systems and their large financial resources, drawn from

public money, are to be protected, the occurrence of fraud big and

small has to be stamped out

The role of insider in banking fraud, however, pernicious it may be,

is here to stay. considering the growing aspiration for effortless

money

For one detected case, there can be numerous instances, which

remain undetected.

Constant vigilance may reduce its frequency and magnitude, but

complete eradication is just not possible

“ Frauds can be prevented and controlled.”

THANK YOU