02 July 2021 1QFY22E Results Preview Information Technology

12

02 July 2021 1QFY22E Results Preview Information Technology HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters Strong momentum continues Strong deal momentum (both pipeline and large deal bookings), broad- based industry-vertical trends towards digital transformation, positive cyclical indicators in product development/engineering services and consulting, accelerated hiring, and improving alignment with hyperscalers/SaaS indicate continuity of momentum for the sector (coverage universe). Tier-1 IT is expected to deliver 4% QoQ (3% organic) and 20% YoY (base impact) revenue growth. In comparison, mid-tier IT is expected to post 3.5% QoQ (range of -3.6% to +5.9% QoQ) with larger mid-tier averaging >4.5% QoQ. Margin will be impacted by wage increases, increase in sub-contracting/attrition, offset partly by operating leverage and FX/offshoring. Deal wins (TCS-Proximus, Ericsson, Alcatel-Lucent, Virgin Atlantic; INFY-BP, Archrock, RXR, Britvic; HCLT-Hitachi ABB; WPRO-Levi Strauss, Bristol Water; LTI-Hoist Finance) remained strong in 1QFY22. Acquisition volumes continued in 1Q (WPRO-Ampion; TECHM- DigitalOnUs, Eventus; LTI-Cuelogic; PSYS-Sureline Systems select assets; MTCL-NxT Digital; ZENT-M3bi) to augment capabilities in cybersecurity, DevOps, product development and analytics. We believe that the elevated supply-side pressure is transient and will normalise over the next 1-2 quarters. Revenue outperformance led by WPRO, TELX, PSYS and MTCL: In 1QFY22E, we expect WPRO to lead the growth at 9.4% QoQ in USD terms helped by Capco acquisition (630bps QoQ), followed by TCS with 3.6% QoQ growth supported by uptick in deals. INFY/HCLT/ TECHM are expected to post 3.5/2.2/2%. Within mid-tiers, TELX/PSYS/MTCL to report growth at 5.9/5.4/5.3% QoQ (USD terms). LTI, MPHL and LTTS are expected to post 3.9%, 3.5% and 3.5% QoQ growth, while CYL will lag at -3.6% QoQ due to decline in DLM business. In terms of margin, WPRO is expected to underperform operationally (Capco integration & partial wage increase impact) within tier-1s and TELX within mid tiers (one-time payout impact of - 550bps). Margins during the quarter are impacted due to wage hike and promotion cycle for most companies. Key monitorables: (1) Revenue guidance: INFY (expected to increase by 100bps)/HCLT (unchanged at >10% CC) for FY22, WPRO (2.5-3% for 2Q) and LTTS (100bps increase expected); (2) Progression/regression in large deal pipeline and bookings; (3) Attrition & sub-contracting and commentary on supply-side factors; (4) Pricing and delivery-mix outlook; (5) Core verticals’ performance and outlook. Maintain positive outlook: We roll over valuations to Jun-23E and raise target multiples for most of the companies in our coverage universe (except WPRO and CYL) to reflect greater visibility/longevity of growth. Our positive stance on the sector remains premised on the longevity of high growth (and strong balance sheet), supported by large deal wins. While mid-tier IT valuations have hit escape velocity (sustainable), driven by strong business momentum (both absolute and relative to tier-1), broadly risk-reward is favourable for tier-1s. Preferred picks are Infosys, HCL Tech, Mphasis and Sonata. Company CMP* (INR) RECO TP (INR) TCS 3,342 ADD 3,750 Infosys 1,560 BUY 1,730 Wipro 539 ADD 575 HCL Tech 986 BUY 1,185 TechM 1,085 BUY 1,270 LTI 4,017 ADD 4,520 Mindtree 2,581 ADD 2,670 Mphasis 2,172 BUY 2,680 LTTS 2,893 REDUCE 2,680 Tata Elxsi 4,244 ADD 4,165 Persistent 2,960 ADD 3,160 Cyient 886 ADD 915 Zensar^ 325 BUY 375 Sonata 755 BUY 805 Mastek 2,230 BUY 2,460 *CMP as on 1 st Jul 2021 Apurva Prasad [email protected] +91-22-6171-7327 Amit Chandra [email protected] +91-22-6171-7345 Vinesh Vala [email protected] +91-22-6171-7332 TCS INFY WPRO HCLT TECHM LTI MTCL MPHL LTTS TELX PSYS CYL ZENT SSOF MAST 5 10 15 20 25 30 35 40 45 10 15 20 25 30 P/E (x) FY23E EPS CAGR % (FY21-24E)

Transcript of 02 July 2021 1QFY22E Results Preview Information Technology

02 July 2021 1QFY22E Results Preview

Information Technology

HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters

Strong momentum continues Strong deal momentum (both pipeline and large deal bookings), broad-

based industry-vertical trends towards digital transformation, positive

cyclical indicators in product development/engineering services and

consulting, accelerated hiring, and improving alignment with

hyperscalers/SaaS indicate continuity of momentum for the sector

(coverage universe). Tier-1 IT is expected to deliver 4% QoQ (3%

organic) and 20% YoY (base impact) revenue growth. In comparison,

mid-tier IT is expected to post 3.5% QoQ (range of -3.6% to +5.9% QoQ)

with larger mid-tier averaging >4.5% QoQ. Margin will be impacted by

wage increases, increase in sub-contracting/attrition, offset partly by

operating leverage and FX/offshoring.

Deal wins (TCS-Proximus, Ericsson, Alcatel-Lucent, Virgin Atlantic;

INFY-BP, Archrock, RXR, Britvic; HCLT-Hitachi ABB; WPRO-Levi

Strauss, Bristol Water; LTI-Hoist Finance) remained strong in 1QFY22.

Acquisition volumes continued in 1Q (WPRO-Ampion; TECHM-

DigitalOnUs, Eventus; LTI-Cuelogic; PSYS-Sureline Systems select

assets; MTCL-NxT Digital; ZENT-M3bi) to augment capabilities in

cybersecurity, DevOps, product development and analytics. We believe

that the elevated supply-side pressure is transient and will normalise

over the next 1-2 quarters.

Revenue outperformance led by WPRO, TELX, PSYS and MTCL: In

1QFY22E, we expect WPRO to lead the growth at 9.4% QoQ in USD

terms helped by Capco acquisition (630bps QoQ), followed by TCS

with 3.6% QoQ growth supported by uptick in deals. INFY/HCLT/

TECHM are expected to post 3.5/2.2/2%. Within mid-tiers,

TELX/PSYS/MTCL to report growth at 5.9/5.4/5.3% QoQ (USD terms).

LTI, MPHL and LTTS are expected to post 3.9%, 3.5% and 3.5% QoQ

growth, while CYL will lag at -3.6% QoQ due to decline in DLM

business. In terms of margin, WPRO is expected to underperform

operationally (Capco integration & partial wage increase impact)

within tier-1s and TELX within mid tiers (one-time payout impact of -

550bps). Margins during the quarter are impacted due to wage hike

and promotion cycle for most companies.

Key monitorables: (1) Revenue guidance: INFY (expected to increase

by 100bps)/HCLT (unchanged at >10% CC) for FY22, WPRO (2.5-3%

for 2Q) and LTTS (100bps increase expected); (2)

Progression/regression in large deal pipeline and bookings; (3)

Attrition & sub-contracting and commentary on supply-side factors;

(4) Pricing and delivery-mix outlook; (5) Core verticals’ performance

and outlook.

Maintain positive outlook: We roll over valuations to Jun-23E and

raise target multiples for most of the companies in our coverage

universe (except WPRO and CYL) to reflect greater visibility/longevity

of growth. Our positive stance on the sector remains premised on the

longevity of high growth (and strong balance sheet), supported by

large deal wins. While mid-tier IT valuations have hit escape velocity

(sustainable), driven by strong business momentum (both absolute

and relative to tier-1), broadly risk-reward is favourable for tier-1s.

Preferred picks are Infosys, HCL Tech, Mphasis and Sonata.

Company CMP*

(INR) RECO

TP

(INR)

TCS 3,342 ADD 3,750

Infosys 1,560 BUY 1,730

Wipro 539 ADD 575

HCL Tech 986 BUY 1,185

TechM 1,085 BUY 1,270

LTI 4,017 ADD 4,520

Mindtree 2,581 ADD 2,670

Mphasis 2,172 BUY 2,680

LTTS 2,893 REDUCE 2,680

Tata Elxsi 4,244 ADD 4,165

Persistent 2,960 ADD 3,160

Cyient 886 ADD 915

Zensar^ 325 BUY 375

Sonata 755 BUY 805

Mastek 2,230 BUY 2,460

*CMP as on 1st Jul 2021

Apurva Prasad

+91-22-6171-7327

Amit Chandra

+91-22-6171-7345

Vinesh Vala [email protected]

+91-22-6171-7332

TCSINFY

WPRO

HCLTTECHM

LTIMTCL

MPHL

LTTS

TELX

PSYS

CYL

ZENT

SSOF

MAST

5

10

15

20

25

30

35

40

45

10 15 20 25 30

P/E

(x

) F

Y2

3E

EPS CAGR % (FY21-24E)

Page | 2

1QFY22E Results Preview

IT Services: 1QFY22E Quarterly Financial Summary

Company

Net Sales (USD mn) Net Sales (INR bn) EBIT (INR bn) EBIT Margin (%) APAT (INR bn) Adj. EPS (INR)

1Q

FY22E

QoQ

(%)

YoY

(%)

1Q

FY22E

QoQ

(%)

YoY

(%)

1Q

FY22E

QoQ

(%)

YoY

(%)

1Q

FY22E

QoQ

(bps)

YoY

(bps)

1Q

FY22E

QoQ

(%)

YoY

(%)

1Q

FY22E

4Q

FY21

1Q

FY21

TCS 6,204 3.6 22.6 457.26 4.6 19.3 118.43 0.9 30.9 25.9 -95 229 93.77 1.4 33.8 25.3 25.0 18.9

Infosys 3,738 3.5 19.8 275.52 4.7 16.4 65.88 2.3 22.8 23.9 -56 124 52.10 2.6 23.1 12.4 12.1 10.1

Wipro 2,354 9.4 22.5 178.05 9.6 19.4 32.56 -2.2 27.0 18.3 -220 109 28.84 -3.0 20.6 5.1 5.2 4.2

HCLT 2,754 2.2 16.9 202.99 3.3 13.8 41.51 4.3 13.4 20.5 19 -6 32.86 10.9 12.3 12.1 10.9 10.8

Tech M 1,356 2.0 12.3 99.96 2.7 9.8 15.09 -5.9 64.6 15.1 -138 503 12.20 7.8 25.5 13.9 12.9 11.1

Tier-1 IT 16,408 4.0 20.1 1,213.77 5.0 16.9 273.48 1.0 26.9 22.5 -89 178 219.77 2.8 25.4

L&T

Infotech 465 3.9 19.1 34.27 4.8 16.2 5.71 -9.8 11.1 16.7 -270 -76 4.60 -8.5 10.4 26.4 28.8 23.9

Mindtree 304 5.3 19.9 22.37 6.1 17.2 4.06 3.7 54.7 18.1 -41 440 3.30 3.9 54.8 20.0 19.3 12.9

Mphasis 354 3.5 16.0 26.11 3.4 14.1 4.13 1.8 15.2 15.8 -25 15 3.28 3.6 19.4 17.6 17.0 14.8

L&T Tech 204 3.5 19.6 15.07 4.6 16.4 2.28 -4.7 45.4 15.1 -148 302 1.94 -0.2 65.6 18.6 18.6 11.2

Tata Elxsi 75 5.9 42.5 5.56 7.2 38.7 1.42 -9.5 73.2 25.5 -471 508 1.14 -1.4 64.8 18.2 18.5 11.1

Persistent 161 5.4 23.0 11.88 6.7 19.8 1.57 7.1 52.4 13.2 5 283 1.53 10.7 69.5 20.0 18.0 11.8

Cyient 144 -3.6 10.6 10.65 -2.6 7.4 1.23 -10.8 141.4 11.6 -107 643 0.98 -11.4 20.7 8.9 10.1 7.4

Zensar 124 3.4 -0.7 9.16 4.5 -3.4 1.26 -2.6 29.2 13.8 -100 348 0.95 5.5 31.2 4.2 4.0 3.2

Sonata 44 1.0 21.2 12.11 12.6 27.1 0.95 1.7 40.4 7.9 -84 74 0.77 -6.8 55.1 7.4 8.0 4.8

Mastek 69 4.5 35.5 5.07 5.0 31.4 0.99 3.3 74.0 19.5 -33 477 0.69 13.2 69.6 24.1 21.3 14.2

Mid-Tier IT 1,946 3.5 18.1 152.24 5.0 16.1 23.60 -2.9 34.9 15.5 -125 216 19.18 -0.6 34.6

Aggregate 18,353 3.9 19.9 1,366.01 5.0 16.8 297.08 0.7 27.5 21.7 -93 182 238.95 2.5 26.1

Source: HSIE Research, Wipro USD Rev is IT services, Sonata USD rev is IITS, Wipro includes inorganic growth of 630bps QoQ & TECHM includes

inorganic growth of 50bps QoQ

USD revenue QoQ growth trend

Source: HSIE Research, Wipro includes inorganic growth of 630bps QoQ & TECHM includes inorganic

growth of 50bps QoQ

Sequential USD revenue growth

Companies 1QFY22E

QoQ (%)

2Q-4QFY22E

Implied CQGR (%)

1Q-4QFY23E

Implied CQGR (%) Companies

1QFY22E

QoQ (%)

2Q-4QFY22E

Implied CQGR (%)

1Q-4QFY23E

Implied CQGR (%)

TCS 3.6 2.6 2.6 L&T Tech 3.5 3.1 3.7

Infosys 3.5 3.5 2.9 Tata Elxsi 5.9 4.8 4.6

Wipro 9.4 3.1 2.4 Persistent 5.4 4.7 4.5

HCLT 2.2 2.5 2.6 Cyient -3.6 5.0 2.6

Tech M 2.0 2.7 2.6 Zensar 3.4 2.9 2.9

L&T Infotech 3.9 4.1 4.0 Sonata 1.0 4.3 4.0

Mindtree 5.3 3.7 3.6 Mastek 4.5 2.2 4.8

Mphasis 3.5 3.5 3.2

Source: HSIE Research

3.6 3.5

9.4

2.2 2.03.9

5.33.5 3.5

5.9 5.4

-3.6

3.4

1.0

4.5

-6.0-4.0-2.00.02.04.06.08.0

10.012.0

TC

S

Info

sys

Wip

ro

HC

LT

Tec

h M

L&

T I

nfo

tech

Min

dtr

ee

Mp

has

is

L&

T T

ech

Tat

a E

lxsi

Per

sist

ent

Cy

ien

t

Zen

sar

So

nat

a

Mas

tek

Page | 3

1QFY22E Results Preview

IT Services: valuation metrics

Company MCap

(INR bn)

CMP

(INR)

TP

(INR) RECO

EPS (INR) P/E (x) RoE (%) USD Rev

CAGR%

FY21-24E

EPS

CAGR%

FY21-24E FY21 FY22E FY23E FY24E FY21 FY22E FY23E FY24E FY21 FY22E FY23E FY24E

TCS 12,360 3,342 3,750 ADD 90.2 107.5 122.1 135.4 37.1 31.1 27.4 24.7 39.1 44.5 47.1 48.2 12.3 14.5

Infosys 6,633 1,560 1,730 BUY 46.2 52.4 59.9 67.0 33.8 29.8 26.0 23.3 27.3 30.0 34.3 35.1 13.1 13.2

Wipro 2,980 539 575 ADD 19.5 21.8 25.1 28.6 27.6 24.7 21.5 18.8 19.4 20.7 21.4 21.9 14.0 13.6

HCL Tech 2,674 986 1,185 BUY 45.9 49.7 57.4 64.5 21.5 19.8 17.2 15.3 22.4 21.2 21.9 21.9 11.1 12.0

TechM 1,048 1,085 1,270 BUY 51.1 59.2 68.7 75.9 21.2 18.3 15.8 14.3 19.3 20.1 21.4 21.6 10.7 14.1

Tier-1 IT Median

27.6 24.7 21.5 18.8 22.4 21.2 21.9 21.9 12.3 13.6

LTI 699 4,017 4,520 ADD 111.3 121.9 149.4 176.3 36.1 32.9 26.9 22.8 29.8 26.6 27.4 27.3 17.3 16.6

Mindtree 425 2,581 2,670 ADD 70.3 81.1 91.6 106.9 36.7 31.8 28.2 24.1 29.7 28.2 26.8 26.5 16.6 15.0

Mphasis 405 2,172 2,680 BUY 65.3 75.0 91.2 112.6 33.3 29.0 23.8 19.3 19.7 20.4 22.3 24.5 14.2 19.9

L&T Tech 302 2,893 2,680 REDUCE 60.1 81.5 97.5 118.8 48.2 35.5 29.7 24.3 20.1 22.6 23.1 24.0 15.2 25.5

Tata Elxsi 264 4,244 4,165 ADD 59.1 80.1 99.4 120.3 71.8 53.0 42.7 35.3 30.1 35.1 36.9 35.9 23.5 26.7

Persistent 226 2,960 3,160 ADD 59.0 83.3 101.4 118.5 50.2 35.6 29.2 25.0 17.4 21.1 22.1 22.2 19.9 26.2

Cyient 97 886 915 ADD 33.8 40.1 50.2 52.9 26.2 22.1 17.7 16.8 13.5 14.4 16.6 16.2 12.2 16.1

Zensar 74 325 375 BUY 15.3 16.8 19.8 24.1 21.2 19.3 16.4 13.5 15.7 15.2 16.3 18.0 9.2 16.3

Sonata 78 755 805 BUY 25.6 31.8 38.6 45.5 29.5 23.8 19.5 16.6 33.7 34.0 35.9 36.5 17.0 21.1

Mastek 64 2,230 2,460 BUY 73.5 93.2 117.5 139.5 30.3 23.9 19.0 16.0 25.4 27.7 28.3 27.3 17.3 23.8

Mid-Tier IT AVG

38.4 30.7 25.3 21.3 23.5 24.5 25.6 25.8 16.2 20.7

Mid-Tier IT Median 34.7 30.4 25.4 21.0 22.7 24.6 25.0 25.5 16.8 20.5

Source: HSIE Research, CMP as on 1st Jul 2021

Global IT Peers: valuation metrics

Company MCap

(USD bn)

CMP

(USD)

TP

RECO

EPS (USD) P/E (x) RoE (%) USD Rev

CAGR%

FY21-24E

EPS

CAGR%

FY21-24E FY21 FY22E FY23E FY24E FY21 FY22E FY23E FY24E FY21 FY22E FY23E FY24E

Accenture 196.5 295 NA NR 8.8 9.9 10.8 12.7 33.4 29.7 27.3 23.1 31.2 30.5 29.0 32.3 8.2 8.7

Cognizant 36.5 69 NA NR 3.4 4.0 4.4 4.8 20.3 17.4 15.9 14.5 12.7 16.5 16.7 15.0 10.0 9.7

Capgemini^ 27.3 162 NA NR 7.3 7.7 8.7 9.9 22.2 21.1 18.6 16.4 13.2 18.7 19.1 18.7 9.5 13.6

EPAM 28.8 511 NA NR 6.3 7.8 9.6 12.3 80.6 65.9 53.4 41.6 18.3 19.5 21.3 21.2 40.0 25.8

Globant 9.1 219 NA NR 2.5 3.4 4.0 4.6 89.5 64.7 54.7 47.6 8.2 13.0 12.4 NA 44.3 16.5

TietoEVRY^ 3.2 27 NA NR 2.2 2.3 2.5 2.6 12.4 11.8 10.7 10.1 5.7 15.0 15.1 15.6 3.2 8.1

Global IT AVG

43.0 35.1 30.1 25.6 14.9 18.9 18.9 20.5 19.2 13.7

Global IT Median

27.8 25.4 23.0 19.8 13.0 17.6 17.9 18.7 9.8 11.7

Source: Bloomberg Consensus, HSIE Research, CMP as on 1st Jul 2021, ^ in EUR

Page | 4

1QFY22E Results Preview

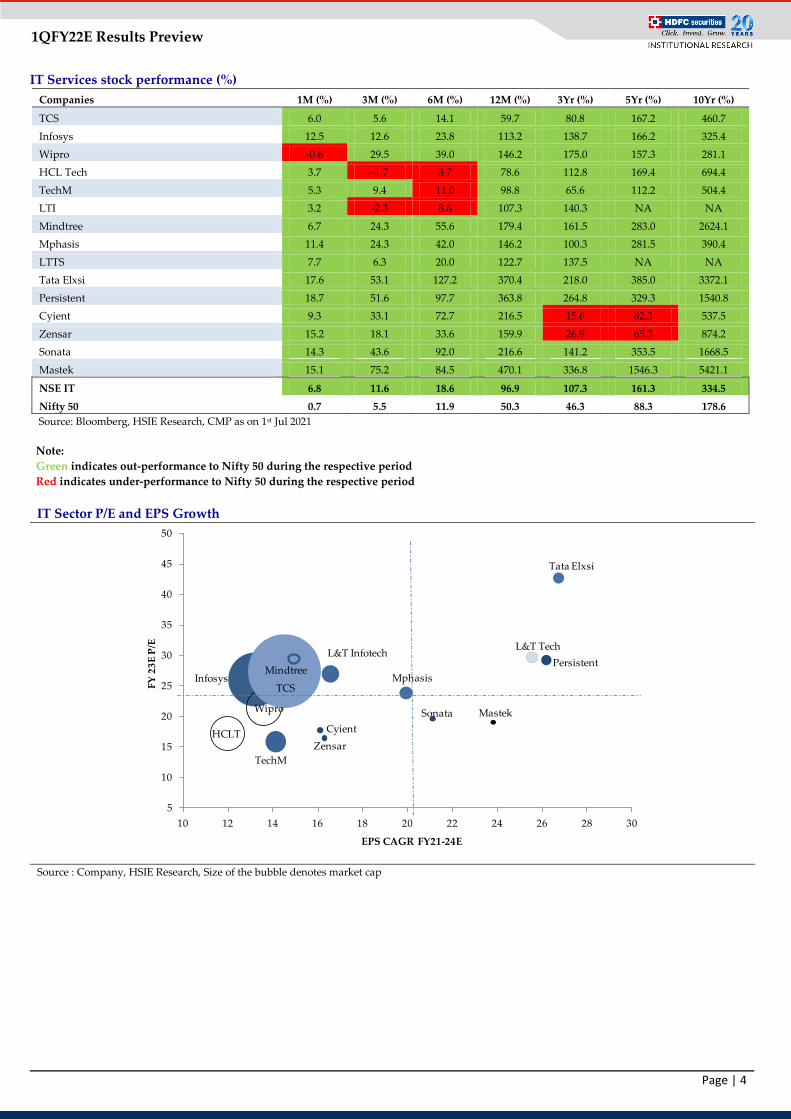

IT Services stock performance (%)

Companies 1M (%) 3M (%) 6M (%) 12M (%) 3Yr (%) 5Yr (%) 10Yr (%)

TCS 6.0 5.6 14.1 59.7 80.8 167.2 460.7

Infosys 12.5 12.6 23.8 113.2 138.7 166.2 325.4

Wipro -0.6 29.5 39.0 146.2 175.0 157.3 281.1

HCL Tech 3.7 -1.7 3.7 78.6 112.8 169.4 694.4

TechM 5.3 9.4 11.0 98.8 65.6 112.2 504.4

LTI 3.2 -2.3 8.6 107.3 140.3 NA NA

Mindtree 6.7 24.3 55.6 179.4 161.5 283.0 2624.1

Mphasis 11.4 24.3 42.0 146.2 100.3 281.5 390.4

LTTS 7.7 6.3 20.0 122.7 137.5 NA NA

Tata Elxsi 17.6 53.1 127.2 370.4 218.0 385.0 3372.1

Persistent 18.7 51.6 97.7 363.8 264.8 329.3 1540.8

Cyient 9.3 33.1 72.7 216.5 15.6 82.3 537.5

Zensar 15.2 18.1 33.6 159.9 26.9 65.3 874.2

Sonata 14.3 43.6 92.0 216.6 141.2 353.5 1668.5

Mastek 15.1 75.2 84.5 470.1 336.8 1546.3 5421.1

NSE IT 6.8 11.6 18.6 96.9 107.3 161.3 334.5

Nifty 50 0.7 5.5 11.9 50.3 46.3 88.3 178.6

Source: Bloomberg, HSIE Research, CMP as on 1st Jul 2021

Note:

Green indicates out-performance to Nifty 50 during the respective period

Red indicates under-performance to Nifty 50 during the respective period

IT Sector P/E and EPS Growth

Source : Company, HSIE Research, Size of the bubble denotes market cap

Infosys

Wipro

HCLT

TechM

L&T Infotech

MphasisMindtree

L&T Tech

Cyient

TCS

Persistent

Zensar

Sonata Mastek

Tata Elxsi

5

10

15

20

25

30

35

40

45

50

10 12 14 16 18 20 22 24 26 28 30

FY

23

E P

/E

EPS CAGR FY21-24E

Page | 5

1QFY22E Results Preview

Change in estimates

IT Services

Company

Revenue USD Mn

(NEW) Change (%) EBIT % (NEW) Change (bps) EPS (INR) NEW Change (%)

FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E

TCS 25,833 28,674 0.5% 0.6% 26.4 26.9 0 -59 107.5 122.1 0.7% -1.5%

Infosys 15,835 17,819 0.0% -0.1% 23.2 23.4 -44 -78 52.4 59.9 -0.9% -2.6%

Wipro 9,893 10,978 0.1% 0.5% 18.0 18.5 -12 -1 21.8 25.1 -0.5% 0.6%

HCL Tech 11,445 12,678 -0.3% -0.3% 20.2 20.3 -32 -21 49.7 57.4 -1.5% -1.3%

Tech Mahindra 5,633 6,240 0.1% 0.5% 15.0 15.6 -21 14 59.2 68.7 -1.8% 1.0%

LTI 1,976 2,322 0.8% 0.7% 17.5 17.8 -113 -155 121.9 149.4 -5.8% -7.8%

Mindtree 1,286 1,489 2.2% 4.5% 17.3 16.8 -72 -74 81.1 91.6 -1.8% -0.2%

Mphasis 1,491 1,701 1.3% 2.1% 16.0 16.7 -47 -9 75.0 91.2 -1.4% 1.4%

LTTS 857 984 1.3% 2.7% 16.0 16.8 -39 -29 81.5 97.5 -1.5% 0.8%

Tata Elxsi 325 390 2.3% 4.1% 26.2 26.7 91 -9 80.1 99.4 5.8% 3.6%

Persistent 692 828 2.7% 5.9% 13.4 13.8 22 -33 83.3 101.4 5.8% 3.5%

Cyient 620 702 -1.1% -0.3% 12.4 13.2 11 22 40.1 50.2 0.6% 1.4%

Zensar 518 580 0.8% 2.6% 13.4 14.0 -40 11 16.8 19.8 -2.0% 3.7%

Sonata 190 221 -0.3% 1.1% 7.9 8.0 4 -1 31.8 38.6 2.0% 1.7%

Mastek 284 332 2.5% 3.4% 18.0 18.7 28 37 93.2 117.5 3.7% 5.8%

Source: Company, HSIE Research

Companies M-cap

(INR bn)

CMP

(INR)

TP Old

(INR)

New TP

(INR) Old Rating

New

Rating

Old

multiple

(x)

New

multiple

(x)

5Y Avg (x) 10Y Avg

(x)

TCS* 12,360 3,342 3,470 3,750 ADD ADD 28 30 22 21

Infosys* 6,633 1,560 1,540 1,730 BUY BUY 25 28 18 17

Wipro 2,980 539 550 575 ADD ADD 22 22 16 15

HCL Tech* 2,674 986 1,045 1,185 BUY BUY 18 20 14 14

Tech Mahindra* 1,048 1,085 1,160 1,270 BUY BUY 17 18 14 13

LTI* 699 4,017 4,210 4,520 ADD ADD 26 28 19 NA

Mindtree* 425 2,581 2,200 2,670 ADD ADD 24 28 19 16

Mphasis* 405 2,172 1,980 2,680 BUY BUY 22 28 16 14

LTTS* 302 2,893 2,320 2,680 REDUCE REDUCE 24 26 21 NA

Tata Elxsi* 264 4,244 3,450 4,165 ADD ADD 36 40 20 18

Persistent* 226 2,960 2,450 3,160 ADD ADD 25 30 16 14

Cyient 97 886 890 915 ADD ADD 18 18 13 12

Zensar*^ 74 325 305 375 ADD BUY 16 18 13 10

Sonata* 78 755 685 805 BUY BUY 18 20 12 9

Mastek* 64 2,230 2,000 2,460 BUY BUY 18 20 12 8

Source: HSIE Research, * PE multiple increased, TP based on Jun-23E EPS, CMP as on 1st Jul 2021, ^Rating upgraded

Page | 6

1QFY22E Results Preview

IT Sector USD Revenue Growth (% YoY) IT Sector USD Revenue Growth (% QoQ)

Source: Company, HSIE Research

Source: Company, HSIE Research

IT Sector EBIT Margin Trend (%) IT Sector EBIT Margin Change (QoQ bps)

Source: Company, HSIE Research

Source: Company, HSIE Research

IT Sector Aggregate Revenue growth and Margin trend Tier 1 Revenue growth and Margin trend

Source: Company, HSIE Research

Source: Company, HSIE Research

2.4

%

2.2

%

2.4

%

1.2

%

2.0

%

1.9

%

-1.5

%

-6.2

%

5.9

%

4.9

%

3.8

%

3.9

%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

E

7.2 7.9 7.7

6.9

1.915.8 11.3 10.1

21.621.1

21.6

20.7

22.9 22.5 22.823.0

18.5

19.5

20.5

21.5

22.5

23.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

E

FY

23

E

FY

24

E

USD Revenue Growth % EBIT Margin % (RHS)

8.2

%

8.7

%

8.0

%

8.4

%

8.0

%

7.7

%

3.6

%

-3.9

% -0.2

%

2.7

% 8.2

%

19

.9%

-10%

-5%

0%

5%

10%

15%

20%

25%

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

E

21.1 21.3

20.519.1

20.0

20.3

20.0

19.9

22.3

23.222.7

21.7

17

18

19

20

21

22

23

24

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

E

76

19

-85

-13

7

89

26

-24

-11

24

0

87

-51

-93

-200

-150

-100

-50

0

50

100

150

200

250

300

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

E

7.2 8.4 8.5

6.9

1.9 15.9 11.8 10.6

20.8

20.3

20.9

20.0

22.2

21.822.2

22.4

18.5

19.0

19.5

20.0

20.5

21.0

21.5

22.0

22.5

23.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

E

FY

23

E

FY

24

E

USD Revenue Growth % EBIT Margin % (RHS)

Page | 7

1QFY22E Results Preview

Currency movements

Favourable movement of USD-INR (1.2% QoQ)

Cross-currency impact was flat in 1QFY22 as compared to positive impact in the prior quarter

USD-INR Trend GBP-USD Trend

Source: NSE, Bloomberg, HSIE Research

Source: NSE, Bloomberg, HSIE Research

EUR-USD Trend AUD-USD Trend

Source: NSE, Bloomberg, HSIE Research Source: NSE, Bloomberg, HSIE Research

64

.5

64

.3 64

.7

64

.3

67

.0

70

.0 72

.1

70

.5

69

.6 70

.4 71

.2 72

.3

75

.9

74

.4

73

.8

72

.9 73

.7

(6)

(4)

(2)

0

2

4

6

60.0

62.0

64.0

66.0

68.0

70.0

72.0

74.0

76.0

78.0

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

USD-INR Average Change QoQ % - RHS

1.2

8

1.3

1

1.3

3 1.3

9

1.3

6

1.3

0

1.2

9

1.3

0

1.2

9

1.2

3 1.2

9

1.2

8

1.2

4 1.2

9

1.3

2 1.3

8

1.4

0

(6)

(4)

(2)

0

2

4

6

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

GBP-USD Average Change QoQ % - RHS

1.1

0

1.1

8

1.1

8

1.2

3

1.1

9

1.1

6

1.1

4

1.1

4

1.1

2

1.1

1

1.1

1

1.1

0

1.1

0

1.1

7 1.1

9

1.2

1 1.2

1

(4)

(2)

0

2

4

6

8

1.00

1.05

1.10

1.15

1.20

1.25

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

EUR-USD Average Change QoQ % - RHS

0.7

5

0.7

9

0.7

7 0.7

9

0.7

6

0.7

3

0.7

2

0.7

1

0.7

0

0.6

9

0.6

8

0.6

6

0.6

6

0.7

2

0.7

3

0.7

7

0.7

7

(6)

(4)

(2)

0

2

4

6

8

10

0.60

0.65

0.70

0.75

0.80

0.85

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

AUD-USD Average Change QoQ % - RHS

Page | 8

1QFY22E Results Preview

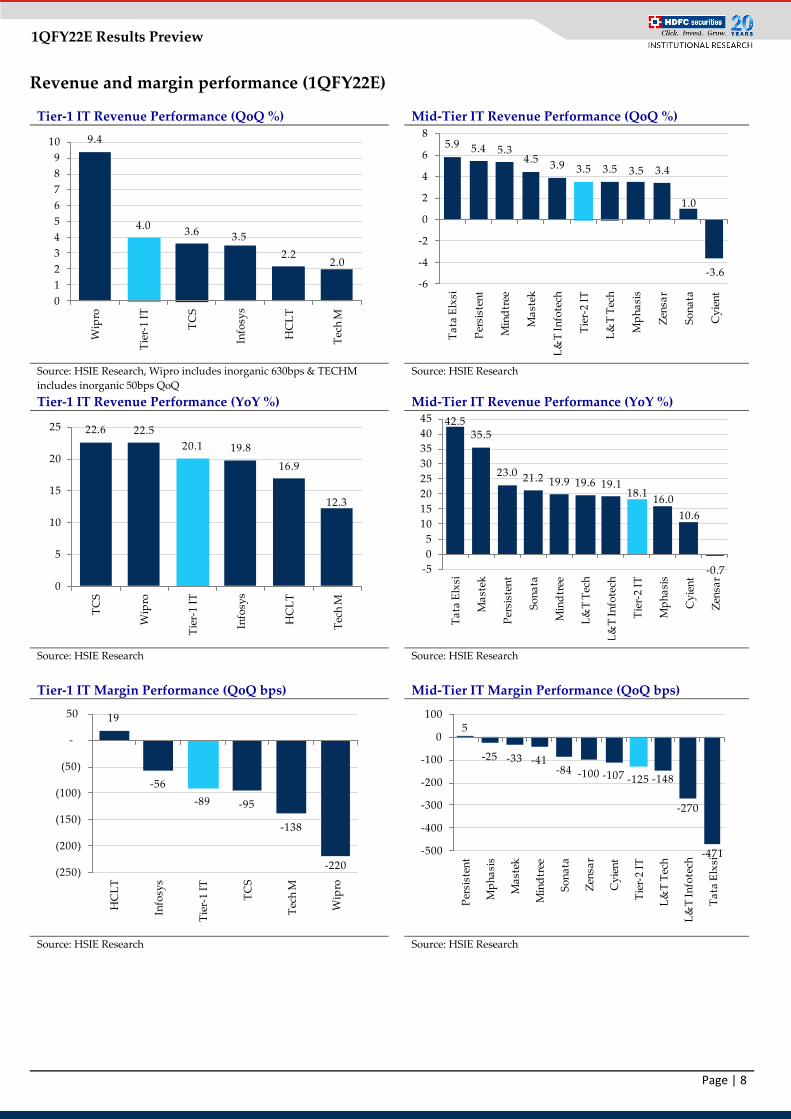

Revenue and margin performance (1QFY22E)

Tier-1 IT Revenue Performance (QoQ %) Mid-Tier IT Revenue Performance (QoQ %)

Source: HSIE Research, Wipro includes inorganic 630bps & TECHM

includes inorganic 50bps QoQ

Source: HSIE Research

Tier-1 IT Revenue Performance (YoY %) Mid-Tier IT Revenue Performance (YoY %)

Source: HSIE Research Source: HSIE Research

Tier-1 IT Margin Performance (QoQ bps)

Mid-Tier IT Margin Performance (QoQ bps)

Source: HSIE Research Source: HSIE Research

9.4

4.03.6 3.5

2.22.0

0

1

2

3

4

5

6

7

8

9

10

Wip

ro

Tie

r-1

IT

TC

S

Info

sys

HC

LT

Tec

h M

5.9 5.4 5.34.5

3.9 3.5 3.5 3.5 3.4

1.0

-3.6-6

-4

-2

0

2

4

6

8

Ta

ta E

lxsi

Per

sist

ent

Min

dtr

ee

Ma

stek

L&

T I

nfo

tech

Tie

r-2

IT

L&

T T

ech

Mp

ha

sis

Zen

sar

So

na

ta

Cy

ien

t

22.6 22.5

20.1 19.8

16.9

12.3

0

5

10

15

20

25

TC

S

Wip

ro

Tie

r-1

IT

Info

sys

HC

LT

Tec

h M

42.535.5

23.0 21.2 19.9 19.6 19.118.1

16.0

10.6

-0.7-5

0

5

10

15

20

25

30

35

40

45

Ta

ta E

lxsi

Ma

stek

Per

sist

ent

So

na

ta

Min

dtr

ee

L&

T T

ech

L&

T I

nfo

tech

Tie

r-2

IT

Mp

ha

sis

Cy

ien

t

Zen

sar

19

-56

-89 -95

-138

-220(250)

(200)

(150)

(100)

(50)

-

50

HC

LT

Info

sys

Tie

r-1

IT

TC

S

Tec

h M

Wip

ro

5

-25 -33 -41-84 -100 -107 -125 -148

-270

-471-500

-400

-300

-200

-100

0

100

Per

sist

ent

Mp

ha

sis

Ma

stek

Min

dtr

ee

So

na

ta

Zen

sar

Cy

ien

t

Tie

r-2

IT

L&

T T

ech

L&

T I

nfo

tech

Ta

ta E

lxsi

Page | 9

1QFY22E Results Preview

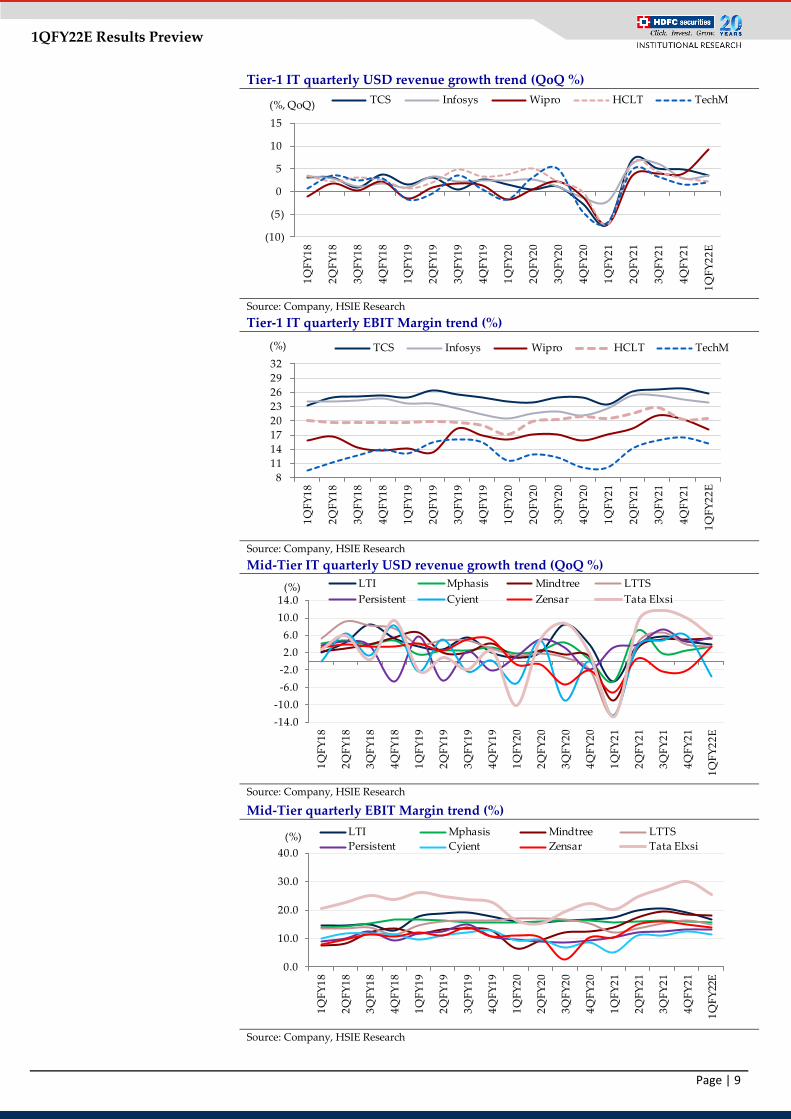

Tier-1 IT quarterly USD revenue growth trend (QoQ %)

Source: Company, HSIE Research

Tier-1 IT quarterly EBIT Margin trend (%)

Source: Company, HSIE Research

Mid-Tier IT quarterly USD revenue growth trend (QoQ %)

Source: Company, HSIE Research

Mid-Tier quarterly EBIT Margin trend (%)

Source: Company, HSIE Research

(10)

(5)

0

5

10

15

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

E

TCS Infosys Wipro HCLT TechM(%, QoQ)

8

11

14

17

20

23

26

29

32

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

E

TCS Infosys Wipro HCLT TechM(%)

-14.0

-10.0

-6.0

-2.0

2.0

6.0

10.0

14.0

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22

E

LTI Mphasis Mindtree LTTS

Persistent Cyient Zensar Tata Elxsi(%)

0.0

10.0

20.0

30.0

40.0

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

1Q

FY

22E

LTI Mphasis Mindtree LTTS

Persistent Cyient Zensar Tata Elxsi(%)

Page | 10

1QFY22E Results Preview

Valuation charts

NIFTY IT Index Valuation Trend (P/E 1-yr fwd) IT Index Valuation Trend vs NIFTY

Source: Bloomberg, HSIE Research Source: Bloomberg, HSIE Research

TCS P/E (1-yr fwd) Trend Infosys P/E (1-yr fwd) Trend Wipro P/E (1-yr fwd) Trend

Source: Bloomberg, HSIE Research

HCL Tech P/E (1-yr fwd) Trend TECHM P/E (1-yr fwd) Trend L&T Infotech P/E (1-yr fwd) Trend

Source: Bloomberg, HSIE Research

10

15

20

25

30

Jun

-11

Dec

-11

Jun

-12

Dec

-12

Jun

-13

Dec

-13

Jun

-14

Dec

-14

Jun

-15

Dec

-15

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

NIFTY IT Index Median

+1 SD -1 SD

+2 SD -2 SD

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

5

10

15

20

25

30

Jun

-11

Dec

-11

Jun

-12

Dec

-12

Jun

-13

Dec

-13

Jun

-14

Dec

-14

Jun

-15

Dec

-15

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

(P/E) Prem/ (Disc) to NIFTY IT Index P/E

10

15

20

25

30

35

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

10

15

20

25

30

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

8

12

16

20Ju

n-1

6

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

8

10

12

14

16

18

20

22

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean1SD + 1SD -2SD + 2SD -

8

11

14

17

20

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean1SD + 1SD -2SD + 2SD -

5

10

15

20

25

30

35

40

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

Page | 11

1QFY22E Results Preview

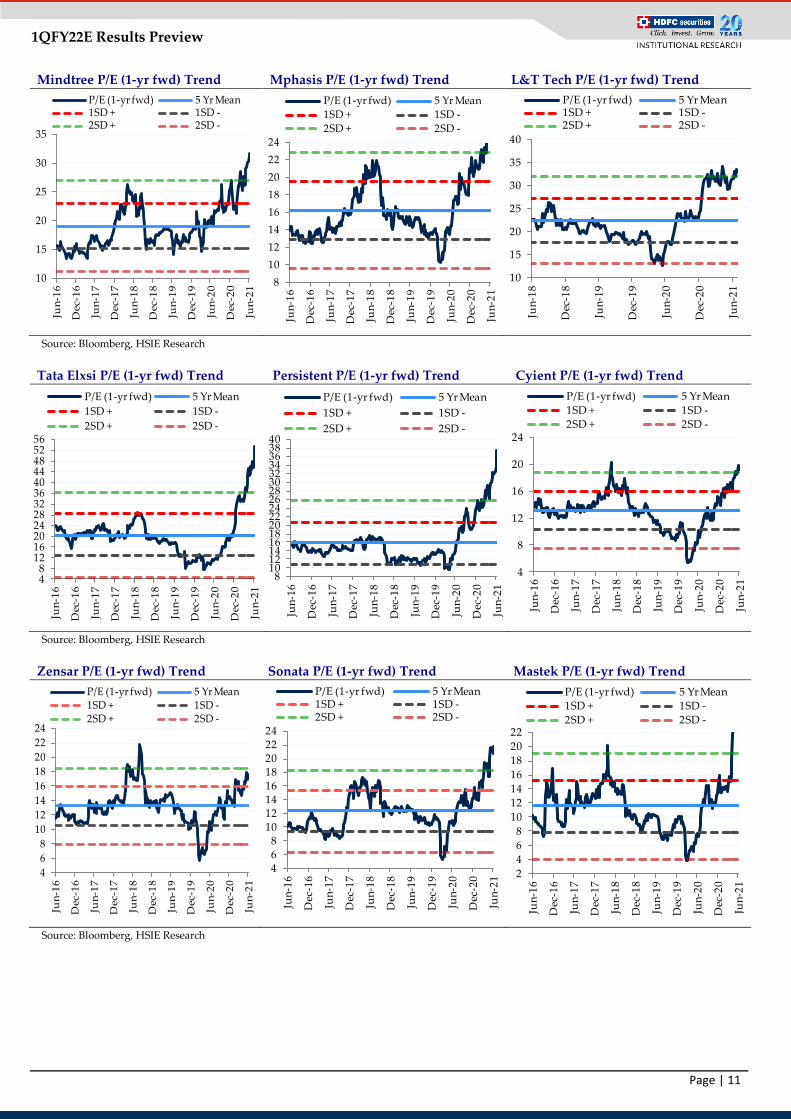

Mindtree P/E (1-yr fwd) Trend Mphasis P/E (1-yr fwd) Trend L&T Tech P/E (1-yr fwd) Trend

Source: Bloomberg, HSIE Research

Tata Elxsi P/E (1-yr fwd) Trend Persistent P/E (1-yr fwd) Trend Cyient P/E (1-yr fwd) Trend

Source: Bloomberg, HSIE Research

Zensar P/E (1-yr fwd) Trend Sonata P/E (1-yr fwd) Trend Mastek P/E (1-yr fwd) Trend

Source: Bloomberg, HSIE Research

10

15

20

25

30

35

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean1SD + 1SD -2SD + 2SD -

8

10

12

14

16

18

20

22

24

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

10

15

20

25

30

35

40

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean1SD + 1SD -2SD + 2SD -

48

121620242832364044485256

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

810121416182022242628303234363840

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

4

8

12

16

20

24

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

4

6

8

10

12

14

16

18

20

22

24

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean1SD + 1SD -2SD + 2SD -

468

1012141618202224

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean1SD + 1SD -2SD + 2SD -

2

4

6

8

10

12

14

16

18

20

22

Jun

-16

Dec

-16

Jun

-17

Dec

-17

Jun

-18

Dec

-18

Jun

-19

Dec

-19

Jun

-20

Dec

-20

Jun

-21

P/E (1-yr fwd) 5 Yr Mean

1SD + 1SD -

2SD + 2SD -

Page | 12

1QFY22E Results Preview

Rating Criteria

BUY: >+15% return potential

ADD: +5% to +15% return potential

REDUCE: -10% to +5% return potential

SELL: > 10% Downside return potential

Disclosure: We, Apurva Prasad, MBA, Amit Chandra, MBA & Vinesh Vala, MBA authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest. Any holding in stock –No HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475. Disclaimer: This report has been prepared by HDFC Securities Ltd and is solely for information of the recipient only. The report must not be used as a singular basis of any investment decision. The views herein are of a general nature and do not consider the risk appetite or the particular circumstances of an individual investor; readers are requested to take professional advice before investing. Nothing in this document should be construed as investment advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in securities of the companies referred to in this document (including merits and risks) and should consult their own advisors to determine merits and risks of such investment. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete. HSL is not obliged to update this report for such changes. HSL has the right to make changes and modifications at any time. This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction. If this report is inadvertently sent or has reached any person in such country, especially, United States of America, the same should be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published in whole or in part, directly or indirectly, for any purposes or in any manner. Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. This document is not, and should not, be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report should not be construed as an invitation or solicitation to do business with HSL. HSL may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments. HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report. HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business. HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report. HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066 Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600 HDFC Securities Limited, SEBI Reg. No.: NSE, BSE, MSEI, MCX: INZ000186937; AMFI Reg. No. ARN: 13549; PFRDA Reg. No. POP: 11092018; IRDA Corporate Agent License No.: CA0062; SEBI Research Analyst Reg. No.: INH000002475; SEBI Investment Adviser Reg. No.: INA000011538; CIN - U67120MH2000PLC152193

HDFC securities

Institutional Equities

Unit No. 1602, 16th Floor, Tower A, Peninsula Business Park,

Senapati Bapat Marg, Lower Parel,Mumbai - 400 013

Board : +91-22-6171 7330 www.hdfcsec.com