· PDF file01.A PROCESS TRANSFORMED The MasterCard Corporate Purchasing Card® is the...

63

I M P L E M E N T A T I O N G U I D E PURCHASING CARD MASTERCARD CORPORATE

Transcript of · PDF file01.A PROCESS TRANSFORMED The MasterCard Corporate Purchasing Card® is the...

I M P L E M E N T A T I O N G U I D E

PURCHASING CARD

MASTERCARDCORPORATE

A PROCESS TRANSFORMED

A. Introduction

B. Traditional Purchasing Process

C. Purchasing Process D. MasterCard Corporate Purchasing Card

Program Functionality and Features

E. MasterCard Corporate Purchasing Card - Who Benefits?

1 Purchasing Department Benefits

2 Internal Business Unit/Employee Benefits

3 Suppliers

F. Purchasing Card Industry Research Analysis

1 Cost by Payment Method

2 Channel Savings

3 Process Costs per Order Incurredby Cardholder

IMPLEMENTATION

A. Overview

B. Phase I - Program Construction

1 Assess Present Practice

2 Set Goals

3 Build Internal Support

4 Create an Implementation Team

5 Establish Program Parameters

6 Enrolling Suppliers

7 Establish Policies and Procedures

8 Training

C. Phase II - Rollout

1Managing and Measuring Your Program

2Monitoring for Policy Compliance

ADVANCED PURCHASING CARD

A. Program Expansion

1 Identify Barriers

2 Determine new card use opportunities

B. E-Commerce

C. International/ Multinational

D. MasterCard Corporate Multi Card

E. Smart Card

APPENDICES

A. Glossary of Terms

B. 1 Sample Supplier Letter 1

2 Sample Supplier Letter 2

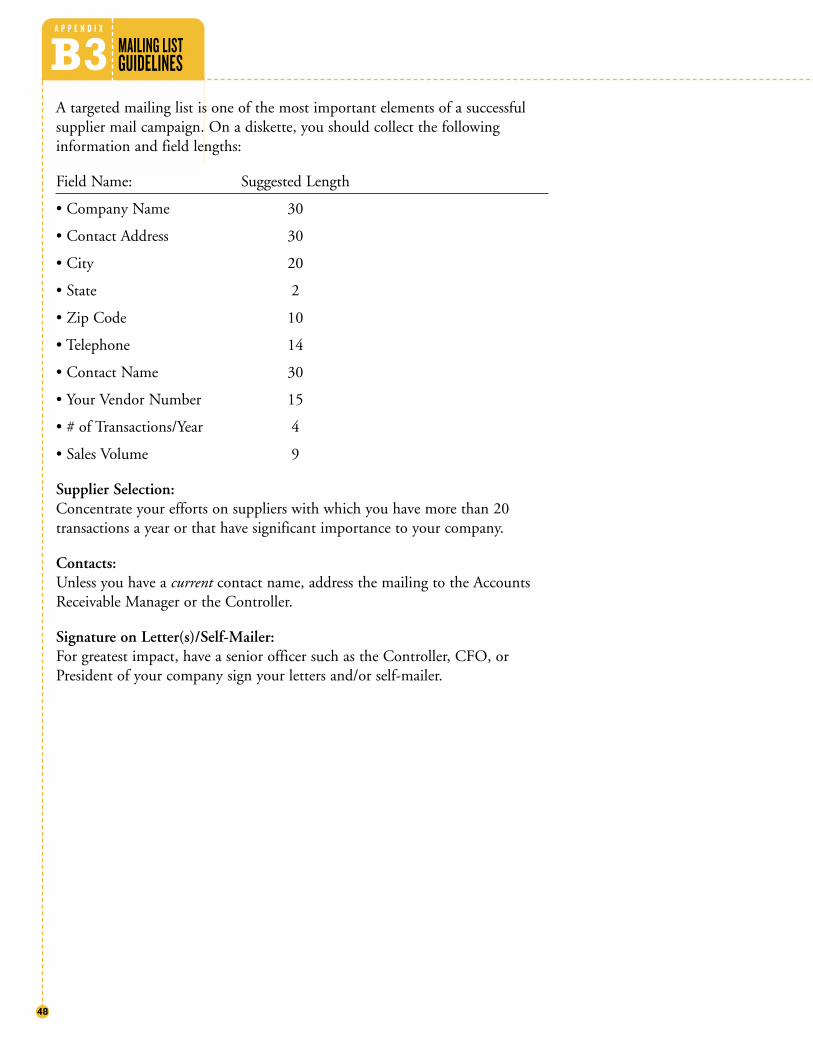

3 Mailing List Guidelines

4 Fax Order Cover Sheet

C. 1 Sample Cardholder Guide

2 Purchasing Card Application

3 Acknowledgment of Responsibilities

D. Sample Implementation Schedule

E. Frequently Asked Questions

04

02

01 03

T A B L E O F C O N T E N T S

01. A PROCESS TRANSFORMED

The MasterCard Corporate Purchasing Card® is the

better way to manage corporate purchasing. Using

this tool, companies can save time and money by

streamlining a labor- and time-intensive purchasing

process. Paperwork can be reduced or eliminated,

and management can exert front- and back-end

controls through the card’s authorization system and

comprehensive information reporting. Many corpora-

tions are turning to the Corporate Purchasing Card,

a MasterCard Corporate Payment Solutions® card

program designed to fundamentally change the way

your company handles its purchasing process.

In 1998, the market for indirect materials (mainte-

nance, repairs, and operational materials known as

MROs) was estimated at $500 billion1. Recent data

shows purchasing card volumes at over $80 billion

for 1999 with annual growth at 33% for the past

two years2, signifying the huge growth opportunity

still available for the purchasing card. Also, the

market for purchasing cards has been increasing to

include recurring payments, payments to service

providers, capital equipment purchases and inven-

tory items; providing even more opportunities to

utilize the Corporate Purchasing Card to save

money for your organization.

The growth of online commerce will also spur

purchasing card usage. Business-to-business buying

via the Internet is estimated to achieve worldwide

volumes in excess of $1 trillion by 2003.3 MasterCard

and its members are working with many e-procurement

solution providers and online exchanges to ensure that

the Corporate Purchasing Card is integrated with these

new marketplaces.

01The MasterCard Corporate Purchasing Card

Implementation Guide was developed to provide

your organization with best practice guidance and

assistance for the purpose of implementing and

maintaining a quality purchasing card program.

S E C T I O N

Your organization can utilize this guide to:

Understand the features and benefits of the

MasterCard Corporate Purchasing Card;

Work with management to identify business issues that

are important to your organization and then make key

decisions about your purchasing card program;

Establish and guide the activities of the project task

force responsible for planning and development,

launching and ongoing management of your company’s

purchasing card program.

A PROCESSTRANSFORMED

1 Packaged Facts®, May 20002 Packaged Facts®, May 20003 WEFA Group Survey, February 23, 1999

3

A. Introduction

4

B. Traditional Purchasing Process

The traditional purchasing process istypically a laborious procedure involv-ing paperwork and verbal communica-tion that begins with the need to pur-chase, and ends with a payment beingmade to the supplier. The steps inbetween are time-consuming for thebusiness unit making the purchases —purchasing and accounts payable. Theprotracted process means those orderinggoods wait a long time to receive themand suppliers wait to get paid.

(See page 5 for process description flow chart.)

This process is still in effect today. Theadvent of computers may have reducedthe need for multi-part forms, but withonly minor exceptions, each party to theprocess is printing a hard copy at theirlocal printer and still matching paper.

The traditional purchasing process oftenbreaks down at the three-way-match step.P.O. numbers are incorrect, or purchaseorders have not been written for a specif-ic delivery. Receiving documents and/orinvoices are misplaced or a myriad ofother situations occur that result in amismatch. Mismatches are resolved withmanual intervention by buyers, account-ing staff, original requestor and receivingstaff. The end result is that an “artificial”match is created, (i.e. duplicate receivingdocuments, duplicate invoices, “after thefact” purchase orders) in order to makethe process work. This “forced match”defeats the entire objective of the “three-way-match” step.

The following chart illustrates the process of the traditional purchase process flow:

01S E C T I O N

A PROCESSTRANSFORMED

5

• Step 1: An employee decides to purchasea good or service.

• Step 2: An employee creates a requisition.

• Step 3: The appropriate individual mustapprove the requisition.

• Step 4: The approved requisition is for-warded to the purchasing departmentwhere a buyer orders the goods and ser-vices. The purchasing department issuesan official purchase order to the supplier,possibly via an ERP system.

- Two copies of the purchase order areheld in the purchasing department forfiling — both numerically by PO numberand alphabetically by supplier name.

- One copy of the purchase order is sentto the accounts payables department.

- One copy is sent to the receiving department.

- The original is sent to the supplier. - An additional copy is sent to the

requestor along with a copy of the requisition to confirm that the orderwas placed.

• Step 5: The receiving department receivesthe goods and matches their PO copywith the packing slip and files thematched papers. The receiving depart-ment issues a two-part receiving docu-ment, (receiver), matching one copy withthe PO and supplier packing slip and thensending a second copy to accountspayable.

• Step 6: The accounts payable departmentreceives an invoice from the supplier.

• Step 7: The accounts payable departmentmatches the PO, invoice and receiverbefore a payment check to the supplier isissued. (This step is known as the “three-way match”.) If a match does not occur,then manual intervention from either theemployee, the purchasing department orthe receiving department takes place.

• Step 8: The accounts payable departmentmakes the payment to the supplier whena match is completed.

• Step 9: The accounts payable departmentadds the transaction to the generalledger, possibly via an ERP system.

6

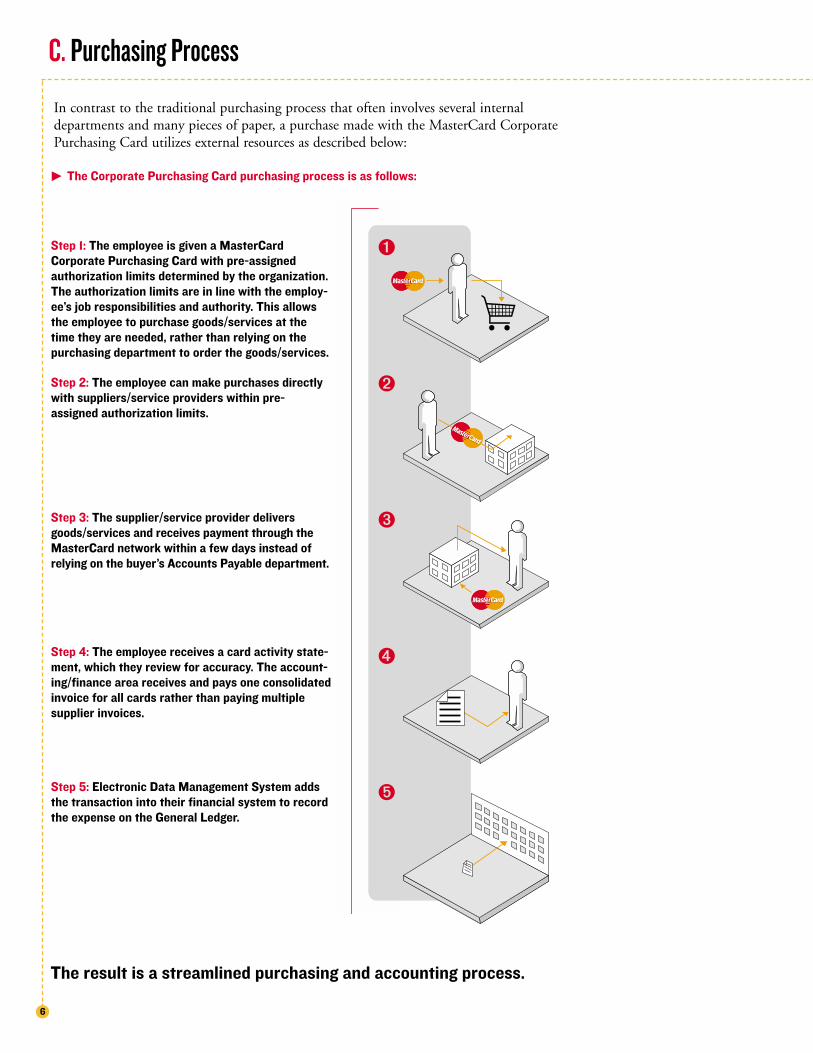

The Corporate Purchasing Card purchasing process is as follows:

The result is a streamlined purchasing and accounting process.

C. Purchasing Process

Step 1: The employee is given a MasterCard

Corporate Purchasing Card with pre-assigned

authorization limits determined by the organization.

The authorization limits are in line with the employ-

ee’s job responsibilities and authority. This allows

the employee to purchase goods/services at the

time they are needed, rather than relying on the

purchasing department to order the goods/services.

Step 2: The employee can make purchases directly

with suppliers/service providers within pre-

assigned authorization limits.

Step 3: The supplier/service provider delivers

goods/services and receives payment through the

MasterCard network within a few days instead of

relying on the buyer’s Accounts Payable department.

Step 4: The employee receives a card activity state-

ment, which they review for accuracy. The account-

ing/finance area receives and pays one consolidated

invoice for all cards rather than paying multiple

supplier invoices.

Step 5: Electronic Data Management System adds

the transaction into their financial system to record

the expense on the General Ledger.

1

2

3

4

5

In contrast to the traditional purchasing process that often involves several internaldepartments and many pieces of paper, a purchase made with the MasterCard CorporatePurchasing Card utilizes external resources as described below:

01S E C T I O N

A PROCESSTRANSFORMED

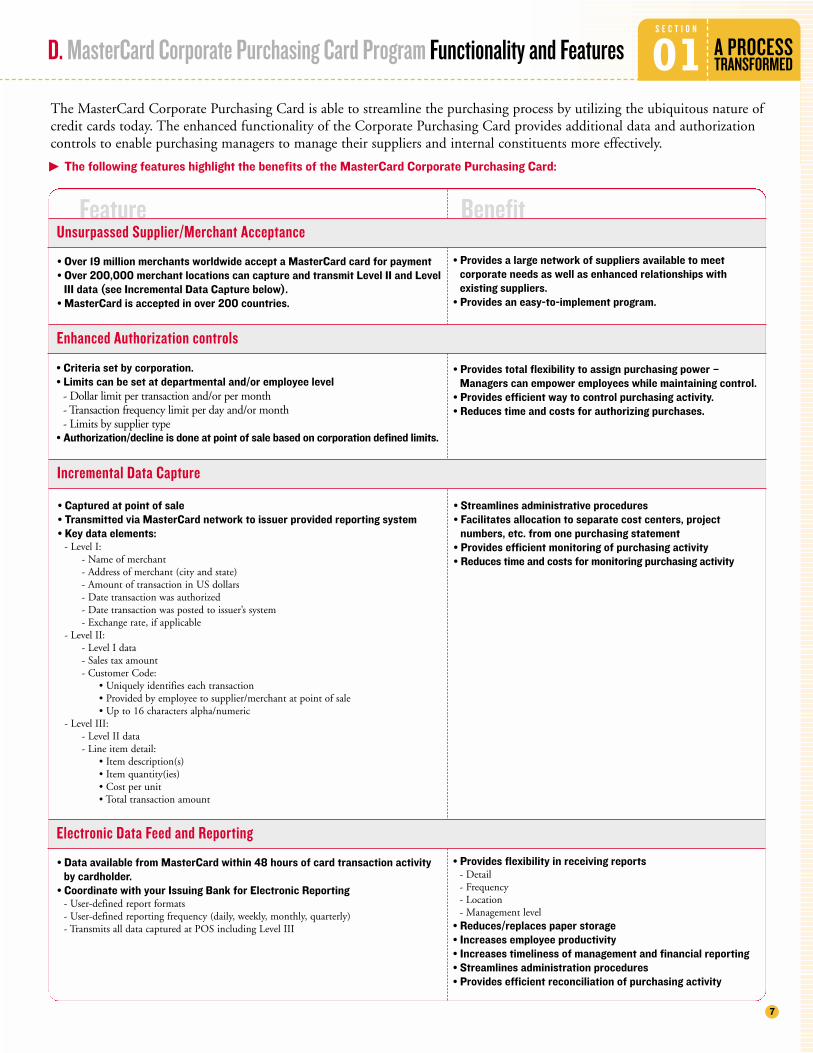

D. MasterCard Corporate Purchasing Card Program Functionality and Features

7

The MasterCard Corporate Purchasing Card is able to streamline the purchasing process by utilizing the ubiquitous nature ofcredit cards today. The enhanced functionality of the Corporate Purchasing Card provides additional data and authorizationcontrols to enable purchasing managers to manage their suppliers and internal constituents more effectively.

Feature Benefit

• Over 19 million merchants worldwide accept a MasterCard card for payment

• Over 200,000 merchant locations can capture and transmit Level II and Level

III data (see Incremental Data Capture below).

• MasterCard is accepted in over 200 countries.

• Provides a large network of suppliers available to meet

corporate needs as well as enhanced relationships with

existing suppliers.

• Provides an easy-to-implement program.

Unsurpassed Supplier/Merchant Acceptance

Enhanced Authorization controls

• Criteria set by corporation.

• Limits can be set at departmental and/or employee level

- Dollar limit per transaction and/or per month- Transaction frequency limit per day and/or month - Limits by supplier type

• Authorization/decline is done at point of sale based on corporation defined limits.

• Provides total flexibility to assign purchasing power –

Managers can empower employees while maintaining control.

• Provides efficient way to control purchasing activity.

• Reduces time and costs for authorizing purchases.

Incremental Data Capture

• Captured at point of sale

• Transmitted via MasterCard network to issuer provided reporting system

• Key data elements:

- Level I:- Name of merchant- Address of merchant (city and state)- Amount of transaction in US dollars- Date transaction was authorized- Date transaction was posted to issuer’s system- Exchange rate, if applicable

- Level II:- Level I data- Sales tax amount- Customer Code:

• Uniquely identifies each transaction• Provided by employee to supplier/merchant at point of sale• Up to 16 characters alpha/numeric

- Level III:- Level II data- Line item detail:

• Item description(s)• Item quantity(ies)• Cost per unit• Total transaction amount

• Streamlines administrative procedures

• Facilitates allocation to separate cost centers, project

numbers, etc. from one purchasing statement

• Provides efficient monitoring of purchasing activity

• Reduces time and costs for monitoring purchasing activity

• Data available from MasterCard within 48 hours of card transaction activity

by cardholder.

• Coordinate with your Issuing Bank for Electronic Reporting

- User-defined report formats- User-defined reporting frequency (daily, weekly, monthly, quarterly)- Transmits all data captured at POS including Level III

• Provides flexibility in receiving reports

- Detail- Frequency- Location- Management level

• Reduces/replaces paper storage

• Increases employee productivity

• Increases timeliness of management and financial reporting

• Streamlines administration procedures

• Provides efficient reconciliation of purchasing activity

Electronic Data Feed and Reporting

The following features highlight the benefits of the MasterCard Corporate Purchasing Card:

8

It is important to note that incrementaldata capture is captured at the suppli-er’s point-of-sale terminal and transmit-ted through the MasterCard network.The sophistication of the supplier’spoint-of-sale device will determinewhat data is captured and transmitted.

To capture Level II information, thesupplier does not generally requirehardware upgrades. Level III capabilitygenerally requires sophisticated hard-ware and software at the merchant loca-tion to handle bar code information orinventory/order entry systems interact-ing with the card authorization termi-nal. This will usually require a signifi-cant investment by the supplier and,therefore, this functional capability willmost likely be limited to larger nationalsuppliers.

MasterCoverage®

Liability Protection Insurance

Experience indicates that employee mis-use of company credit card privileges israre. However, to protect against theselosses if they occur, MasterCard estab-lished the MasterCoverage® LiabilityProtection Program.

The MasterCoverage® LiabilityProtection Program is provided at nocost to financial institutions and com-panies covered by the program for cardsissued in the U.S.* For corporationsthat have four or fewer cards, the liabil-ity protection is up to $5,000 per card-holder, for corporations with five ormore cards, excluding the CorporateMulti Card, the Public Sector MultiCard and the Government IntegratedCard, the liability protection is up to$15,000 per cardholder. For CorporateMulti Cards, Public Sector Multi Cardsand Government Integrated Cards, theliability protection is up to $30,000 percardholder.

*The MasterCoverage Liability Protection Program is provided subject to the terms and conditions set forth in the master policy. For cards issued outside of the United States, there may be an applicable fee.All MasterCard benefits subject to the terms and conditions of the policies and may vary country to country.

D. MasterCard Corporate Purchasing Card Program Functionality and Features

01S E C T I O N

A PROCESSTRANSFORMED

The benefits to be derived fromimplementing your MasterCardCorporate Purchasing Card are notrestricted to only the corporate pur-chasing group. Your external businesspartners (suppliers) and your internalclients (business units and employees)will realize considerable benefits fromyour program.

9

1. Purchasing Department Benefits

aSubstantial reduction in processingcosts (resource time), administrativecost savings (postage, stationery,printing costs, check fees, etc.) andsystem file maintenance and operat-ing costs (supplier file management);

aReduced accounts payable inquiriesfrom suppliers on outstanding payments;

aStrengthened cash management andsimplified bank reconciliation practices;

aEnhanced management control andreporting, with the opportunity tofrequently access transactional data inpartnership with automated postingto the General Ledger (electronic dataplatform);

aIncreased operational and manage-ment time for other core strategic oroperational business activities, and;

aImproved supplier management viaenhanced and readily available MIStools.

2. Internal Business Unit/

Employee Benefits

aControlled empowerment andaccountability to the business unit/cardholder to procure goods and service as required;

aAccelerated delivery time in thereceipt of goods and service resultingin overall increased productivity, and;

aEnhanced budget monitoring result-ing from greater access to transaction-al order data.

3. Suppliers

aImproved cash flow through the rou-tine card settlement process ratherthan through the laborious “invoicing— accounts receivable — bankdeposit” process;

aReduced administrative cost of manag-ing an accounts receivable activity forpurchases made with the MasterCardCorporate Purchasing Card;

aReduced accounts receivables follow-up activity, and;

aImproved customer relations by deal-ing directly with the end user at thecustomer business rather than throughorganizational intermediaries.

E. MasterCard Corporate Purchasing Card-Who Benefits?

10

Gunn Partners 1998 researchanalyzed 22 companies. The sizeof these companies ranged from$1 billion in revenue to $127billion, with median size $15billion. A wide mix of industriesparticipated in the research. The total annual purchasesmade with a purchasing cardranged from $140K (companiesin early stages of implementa-tion) to over $172M.

Illustrated below are charts and analyses prepared by Gunn Partners.

F. Purchasing Card Industry Research Analysis

1. Cost by Payment Method:

As part of the purchasing card research, cost data was collected on four paymentmethods: purchasing cards, purchase orders (for non-inventory transactions),check requests and travel expense reporting (when used for miscellaneous purchas-es). The purchasing card compares very favorably to the three other methods orchannels, with the largest cost advantage of $47 occurring between the purchasingcard ($28.75) and the purchase order ($75.70). The increased cost for the initiatoreffort required in a purchasing card transaction was more than offset by decreasesin purchasing administration.The cost-of-payment differences were converted to savings for each company bymultiplying their transaction volume by the difference in costs for their company(not the averages shown in the chart). The assumption for the savings was that50% of the transactions, from each of the three, (3), alternate methods could beconverted to purchasing cards.

01S E C T I O N

A PROCESSTRANSFORMED

11

$35.00

Saving in $ Millions

$30.00

$25.00

$20.00

$15.00

$10.00

$10.00

$5.00

$0.00

Check Request Travel Reporting Purchase Order

9

1.7

29.7

Cardholder Costs

Cardholder total cost per purchase = $10.56

3. Process Costs per Order

Incurred by Cardholder:

One of the issues cited with the use ofpurchasing cards is that tasks may be shift-ed from the purchasing and accountingfunctions to the cardholder. As indicated,the average cardholder cost per purchase is$10.56. Seventy-eight percent of that costis related to the cost of procurement,while the remaining 22% (matchingreceipts and data entry) are related to theaccounting function.Over the next several years, a dramaticimprovement in each segment of costreduction will take place as more compa-nies implement electronic supplier cata-logs; due to more companies using elec-tronic purchasing.

2. Channel Savings:

The largest opportunity is to convert transactions from PurchaseOrders to Purchasing Cards, as the average saving was over $29 million per year.

Channel Savings ($M)

Average savings by moving 50% of eachchannel volume to Purchasing Cards

02. IMPLEMENTATIONPurchasing cards can greatly improve the efficiency

of your organization’s spending volume. However,

the savings discussed in Section 01 will only occur

if your organization’s purchasing process changes.

A purchasing card implementation must be viewed

as a reengineering effort for your organization, and

given the necessary resources. This section will

explore the steps required to create an effective

Purchasing Card program.

It is vital to spend adequate time on the program construction before issuing cards to your employees. You want to ensure your organization has a completeprocess in place to handle purchasing card transactions.In addition, you need to position your program andexplain the benefits of using a purchasing card toemployees.

Employee acceptance and endorsement of a purchasingcard program is essential to a successful program.

02S E C T I O N

IMPLEMENTATION

Best practice:• A key component in the success of a purchasing card program

is a well-planned implementation. Overwhelmingly, allparticipants in the Gunn Partners research study agreed thathaving a coordinated, cross-functional implementation isimportant to the overall success of the program.

• The implementation should be well planned, appropriately staffed and have specified tasks and goal-related measures set in advance.

• Given a solid plan and the proper management support, four to nine months should be adequate time for implementation.

Purchasing card implementation has four phases:

Phase I - Program construction phase

Phase II - Program rollout

Phase III - Program management

Phase IV - Program expansion

A. Overview

14

Phase 1 is where the implementationprocess begins. This Phaseencompasses the following activities:

1. Assess Present Practice

2. Set Goals

3. Build Internal Support

4. Create an Implementation Team

5. Establish Program Parameters

6. Enroll Suppliers

7. Establish Policies and Procedures

8. Create Communications and

Training Material

B. Phase 1 - Program Construction

1. Assess present practice

A. Initiating the Process

Once you have determined that thereengineering of your purchasingprocess with the use of purchasingcards could be valuable for yourorganization, you can begin animplementation process for yourpurchasing card program.

The first step is to determine who willmanage this effort. This individual orgroup of individuals will be responsiblefor gaining a complete understandingof the current processes and building acase for moving forward. Under Step 4of the process, a full implementationwill be created. However, a staff will berequired to accomplish the first threesteps.

B. Create Analysis, Costing and Mapping

of Current Processes

As previously stated, the cost savings ofa purchasing card program will only berealized if your organization changesthe way that it buys goods and services.In order to understand what needs tobe changed, you must examine thestate of purchasing in your organizationtoday. Document what yourprocurement activities are costing yourorganization in hard and soft dollars,and match those costs to each activityin the current process. Companies thatskip this step will not be able to clearlydocument cost savings later.

First, identify the steps in your currentprocess. In the introduction, wecompared the traditional transactionprocess to the streamlined process,using a MasterCard CorporatePurchasing Card®.

Best Practice: Identify every step in your currentpurchasing process, from the initial“need to buy” through the closing ofaccounts payable entries.

02S E C T I O N

15

Traditional Purchase Process Flow

IMPLEMENTATION

This illustration of the traditionalpurchase flow can assist yourorganization in documenting thecurrent cost of your process.

16

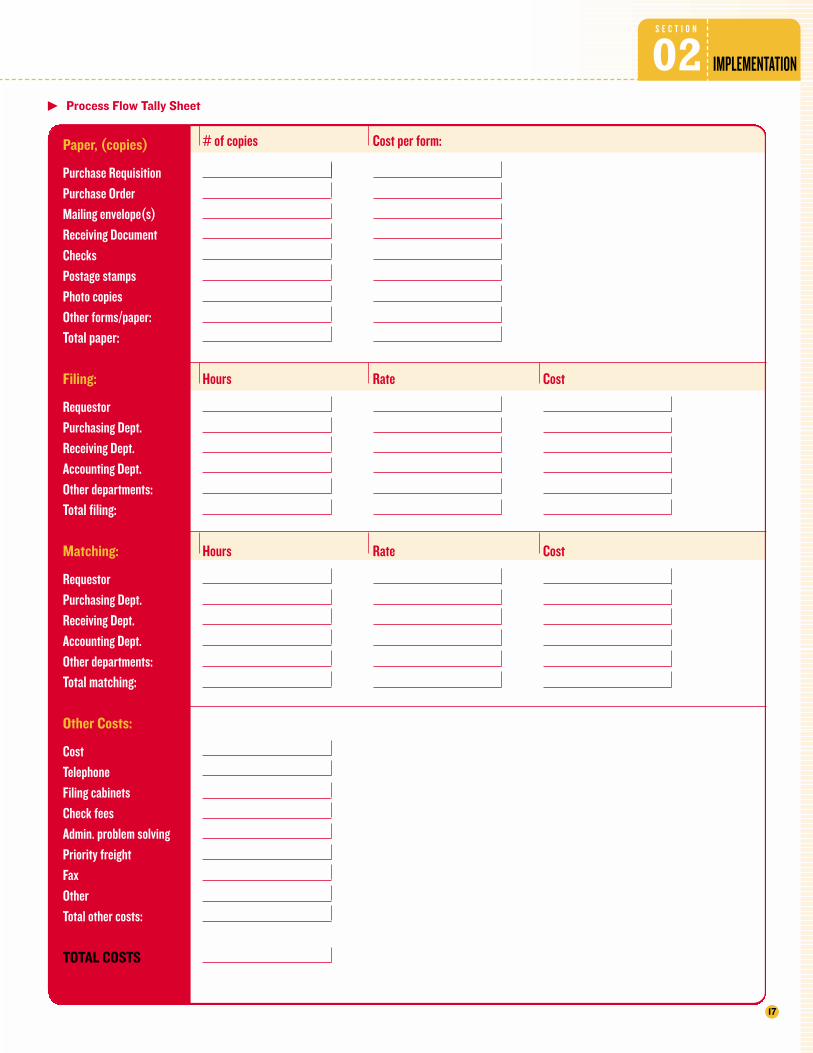

The following table tracks the paper trail created to support the traditional process flow.Your process may have already reduced some of the paper, but a full review of the chartwill probably uncover some similar actions at your company. These tools can be used withthe “Process Flow Tally Sheet” on page 17 to determine the costs of the current process.

Phase 1 - Program Construction

Here are some additional questions thatwill help you to identify your process:

aHow does the purchasing process work?

aHow long does it take fromrequisition to product receipt?

aWhat do you buy? Number oftransactions under US$1000 and$5000 annually?

aWhat authorization controls are inplace?

aWhen errors or disputes occur, howare they corrected?

aHow is the purchasing processaudited? Time involved?

aWho are your suppliers? What type ofdata is currently required fromsuppliers?

aHow are suppliers paid and what isthe average settlement time?

Once the steps are identified, assign acost to each activity. (Use the “tallysheet” on the next page to check yourfindings with the data from pages 14 to16 of this guide. How do your numberscompare?) Typically you’ll arrive atthese costs by analyzing such things as:

aMan-hours in Accounts Payable

aMan-hours in Purchasing

aMan-hours in Receiving

aBank fees for checking

aPostage

aPaper

aCost of funds

aDays of float

aData entry, data storage, MIS reportgeneration

a“Hidden” costs of your currentpurchasing process, including:

• Time spent resolving purchasingproblems (e.g., problem receipts andinvoices, and after-the-fact purchaseorders)

• Other costs incurred (e.g., priorityfreight) due to a time-consumingand complex purchasing process.

• Time spent filling out and receivingapprovals for purchase requisitions.

Step Paper Paper Paper Paper Signature/ Data Number Generation Forward Matching Filing Authorization Entry

Requestor 2 Requisition ( Req. - 3 parts) 2 3 parts to Approver 2 Req. (1 part) 2 Req. (3 parts)3 3 2 parts to Purchasing 3 Req. (2 parts w/P.O.) 3 Req. (2 parts w/P.O.)

Approver 3 Req. (3 parts) to Requestor Req. (3 parts)

Purchasing 4 Purchase Order 1 part to Supplier 1 part w/Req. (for Requestor)Department (P.O. - 6 parts) 1 part w/Req. to Requestor 1 part w/ Req. (for alpha file)

1 part to Accounting1 part to Receiving 1 part w/ Req. to alpha file1 part to numeric file

Receiving 4 4 P.O. to “open P.O.” fileDepartment 5 5 Receiving Document 5 1 part to Accounting 5 1 part w/P.O. 5 w/P.O in “closed P.O.” file

(Receiver - 2 parts)

Accounting 4 4 file P.O. to “open P.O.”Department 5 5 Receiver w/P.O. 5 file P.O. and receiver

in file “awaiting invoice” 7 7 Invoice w/P.O. or 7 If P.O. and receiver OK,

w/P.O. and receiver then file “pending payment”.If only P.O is in, then file“pending receiver”

8 8 Check (3 parts) 8 1 part to supplier 8 1 part w/ P.O., 8 1 part in numeric file, 8 Check (3 parts)receiver and invoice 1 part w/ P.O., receiver

and invoice in alpha file.9 9 adds

transaction to the general ledger

02S E C T I O N

IMPLEMENTATION

Paper, (copies) # of copies Cost per form:

Purchase Requisition

Purchase Order

Mailing envelope(s)

Receiving Document

Checks

Postage stamps

Photo copies

Other forms/paper:

Total paper:

Filing: Hours Rate Cost

Requestor

Purchasing Dept.

Receiving Dept.

Accounting Dept.

Other departments:

Total filing:

Matching: Hours Rate Cost

Requestor

Purchasing Dept.

Receiving Dept.

Accounting Dept.

Other departments:

Total matching:

Other Costs:

Cost

Telephone

Filing cabinets

Check fees

Admin. problem solving

Priority freight

Fax

Other

Total other costs:

TOTAL COSTS

17

Process Flow Tally Sheet

18

Once steps have been identified andcosts quantified, you now need to tiethe cost to the process step thatgenerated the cost. This is the mappingprocess.

If, for example, it takes 13 days fromrequisition to product receipt, howmuch of that thirteen days is suppliertime versus your internal approval/administrative time? How many daysof extra inventory does that require?What is the dollar value of thatinventory? What is your company’scost-of-funds to have that inventory instock? Do you use priority freight toshorten that time? How much moneyis spent on priority freight as a result of the internal process? What are thelabor costs to count, store and retrieveand deliver that inventory whenneeded?

The mapping process is laborious, butit is an important investment in yourimplementation process because itfirmly establishes the baseline fromwhich you will measure your progress.

C. Take Stock of Your Current System

Take an “inventory” of your currentpurchasing process to get a picture ofwho is using it, for what purchases,and at which suppliers. Based on ananalysis of this data, you can select theparameters of the rollout and whattypes of purchases to target for theprogram — who will receive cards,what suppliers will participate, whatare the dollar amounts and types oftransactions.

Cost/Frequency AnalysisFirst, it is useful to consider what typesof purchases your organization makeson indirect materials. Generally, thesepurchases can be categorized into fourquadrants shown above.

Phase 1 - Program Construction

The above chart illustrates thefollowing:

aIf the unit cost is high, and yourorder frequency is low, most likelyyou are using a purchasing contract.It will not be practical to utilize aPurchasing Card for these types oftransactions.

aIf the unit cost is low, and your orderfrequency is high, the PurchasingCard would be a perfect way tohandle these transactions andstreamline the process.

During implementation planning,companies should separate what theybuy into this matrix and concentratetheir initial purchasing card activityin the lower quadrants. These are thelow-dollar/high-frequencytransactions that require largeadministrative effort, resulting incosts relative to the cost of the item.

02S E C T I O N

IMPLEMENTATION

19

Supplier AnalysisAnother useful way to consider yourpurchases is by commodity breakoutand by supplier type.

aGenerally, high-dollar transactions arefor distinctive, non-commodity itemspurchased by your organization. Withthese suppliers, you generally have anestablished partnership withnegotiated payment terms andpayment conducted via blanketcontracts or EDI. It may not bepractical to use a Purchasing Card forthese types of transactions in the earlystages of your program.

aThe Purchasing Card works well forlow-value, high-frequency purchaseswhere your organization is buyingfrom three or more suppliers. Byestablishing a purchase card programfor these transactions, you canconsolidate information about yourpurchases and begin to negotiatebetter pricing with preferredsuppliers. Invoice Analysis

To help you define what purchases willbe eligible to be included in aMasterCard Corporate PurchasingCard program, it’s useful to look atpresent invoices and create an invoiceanalysis chart using the process asoutlined below:

$ per invoice # of invoices % of Total Cumulative % Total $ (mm) % of Total Cumulative %

$0-1,000 60,000 80% 80% $1.35 5% 5%

$1,000-5,000 11,750 15% 95% $4.05 15% 20%

$5,000-10,000 3,000 4% 99% $6.75 25% 45%

>$10,000 750 1% 100% $14.85 55% 100%

aEstablish the volume (%) ofprocurement transactions for severallow- to medium-dollar thresholds

aEstablish the total budgetary value foreach threshold level (%)

In the example below, 95% oftransactions have a transaction value ofless that $5000. Therefore, purchasesless than $5,000 would appear a goodstarting point for your program.

Invoice Analysis Chart

20

Other AnalysisBe sure to examine all types ofpotential spends when you aredetermining which types of purchasesto target for your program.

aConduct a business analysis of allPurchase Orders/Maintenance RepairOrders and Requisition PurchaseOrders.

aReview all business transactions thatresult in a check payment.

aReview all credit/electronic fundstransfer payments that result from amanual order process.

aIdentify the current assetcapitalization transaction level. Thismay be a good way to identify yourinitial limit on Purchasing CardTransactions.

aReview all direct invoice/utilitytransactions that are manuallyprocessed.

aReview the process undertaken forpayment of overseas businesstransactions, particularly bank draftactivity.

2. Set Goals

Companies decide to pursue apurchasing card program for amultitude of reasons — to reduceprocess costs, increase employeesatisfaction, or gather information forsupplier negotiations. This decisionmay be a piece of an overall companyinitiative. Understanding themotivating factors for your company’sdecision to begin a purchasing cardprogram will have substantial effectsthroughout the entire implementationprocess.

aThe first order of business for thenewly formed team is to set goals anda timetable for the program. As withany project, it is important to bespecific about your objectives.Establish primary goals such as:

• Cardholder convenience (i.e.,number of steps to receive what isneeded)

• Minimizing manual efforts (i.e.,eliminate logs, petty cash)

• Strategic purchasing reengineering(i.e., what new terms and conditionscan be negotiated with suppliers —delivery time frames, paymentterms, pricing)

• Information technologyreengineering (i.e., online real-timereporting capability)

• Cost-savings targets (i.e., reducingtotal purchasing/accounting cyclecosts by 75%)

Your goals should be prioritized toensure that they match the reasons forinitiating the program. All of the abovementioned goals are positive, but yourcompany should focus on those goalsthat most match the objectives of theprogram.

The correct metrics will replace hands-on hierarchical supervision. Managersand supervisors can take a“management-by-exception” approachto ensure that purchasing activity isconsistent with company policy andoperational objectives.

The metrics established should beintegrated — individual, team anddepartmental. The reporting ofperformance, vis-à-vis the metrics,should be automated-system generated,easy to produce and timely. Samplemetrics may include:

• Number of transactions

• Number of cardholders

• Average transaction amount

Best practice:Successful companies have establishedgoals, savings targets and metrics thattrack program success.

Phase 1 - Program Construction

02S E C T I O N

IMPLEMENTATION

21

3. Build Internal Support

The information gathered in theevaluation process now needs to bepresented in a management summarythat quantifies the benefits of a well-run program. Potential metrics toenumerate could be:

aNumber of potential transactions tobe transferred to purchasing card

aProcess savings per transaction(personnel hrs. vs. other)

aPotential direct savings fromnegotiated rates as a result of strategicsourcing

The numbers should speak forthemselves and easily convince seniormanagement to support the program.It is advisable to have seniormanagement set up a steeringcommittee consisting of seniormanagers who will monitor progress ofthe implementation, allocate resourcesto the project when required andreconcile interdepartmental issues. Thissteering committee should be asked toacknowledge senior managementsupport for the program by generalmemo to all departments and ongoinginvolvement in the implementation.

4. Create an Implementation Team

Now that you have decided to moveforward with the implementation, youwill require more resources to supportthe program. The typical paper-basedpurchasing system cuts across manyorganizational boundaries, from theemployee who initiates the purchase tothe purchasing, receiving, and accountspayable departments. Each of thesedepartments — and any others thatmay be involved in your purchasingprocess — must work together as ateam to design and implement a newway of handling purchases. Here aresome suggestions on creating a cross-functional team:

A. Select a program manager

The program manager is someone who will assume overall responsibilityfor the design and implementation ofthe program. This may or may not be the individual who you have selected to initiate the process. An effectiveprogram manager will have goodproject-management skills and be able tocommunicate, motivate, and negotiatewell. In particular, the program managerwill use these skills to:

• Chair the cross-functionalimplementation team

• Act as the company liaison to thecard issuer on all program-relatedissues, including setting upcardholder accounts

• Communicate the program tocardholders and suppliers

• Report on the progress of theprogram to senior management

• Coordinate resolution of programquestions and policy issues

• Participate in ongoing programreviews

• Oversee card issuance andcancellation

• Resolve billing disputes if thecardholder is unable to do so

• Help plan continual rollout,maintenance, and enhancement ofthe program

For many organizations, the ProgramManager’s role is a full-time position.You will need to quantify how thescope of this role translates to staffingrequirements for your company.

Best practice:Selection of a cross-functional team and dedicated program administrator to manage the process is a commonfeature of successful companies.

Best practice:Successful MasterCard CorporatePurchasing Card programs have seniormanagement’s strong endorsement andvisible commitment for the program.

22

B. Appoint implementation team and

create implementation schedule

Typically, the implementation team is across-functional team consisting ofrepresentatives from these functions:

aAccounting and Finance Because your accounting/financedepartment will be impacted by thenew program, by doing more controland audit, and less paper processing;it must be represented on your phaseprogram team.

aPurchasing DepartmentPurchasing will play an important rolein the new process. Purchasing mustbe on the team to consider such issuesas supplier reporting, supplier-basereduction, preferred suppliers, andsupplier-base management techniquesthat will require specialized reporting.They also will continue to beresponsible for the overall terms andconditions of the supplier base.

Supplier management will bediscussed later in this document inSection 02-6, Enrolling Suppliers.

aInformation TechnologyThe Information TechnologyDepartment will help make decisionsabout how the purchasing card datawill interface with existing internalfinancial reporting systems:

• What medium (Internet tomainframe, Internet to PC’s, client-server access, EDI transmissions,paper reports, magnetic tape, CD,disk, etc.)?

• What format (custom EDI data file,Flat files, preformatted reports, etc.)?

• How frequently will data bereceived?

• How will the data be distributed?

• What access security measures willbe required?

• What impact does this effort haveon other company-wide informationtechnology initiatives (ERP, newhardware installation or othersystem upgrades)?

• How will this facilitate anye-Commerce efforts currentlyunderway?

aInternal AuditAny purchasing process — whethertraditional paper-based or your newMasterCard Corporate PurchasingCard program — will be audited.That’s why it’s a good idea to includeinternal auditors on your programdesign team. They can make sure thatthe new system has the propercontrols in place to ensure compliancewith company policies.

aTax DepartmentA Tax Department representative canreview the process for handling salesand use tax payments and reporting.

aHuman ResourcesBecause redesigning the purchasingprocess involves communicating withemployees and determining policesand procedures, the human resourcesdepartment may be represented onthe implementation program team.Human Resources may also beresponsible for training cardholders.

aLegalA representative of the company’sLegal Department should be amember of the team, advising on suchmatters as contract negotiations withthe card issuer, legal and regulatorymatters, and liability issues.

Phase 1 - Program Construction

IMPLEMENTATION02S E C T I O N

23

C. Create detailed implementation

schedule

After the team is complete, you shoulddevelop an implementation schedule,to which you will add tasks as youdevelop the program parameters for thepurchasing card implementation.

The implementation schedule is theroad map for the tasks that need to becompleted for a successful purchasingcard program. The schedule lays outthe timing of sequential and parallelefforts as well as identifying thoseindividuals responsible for thecompletion of each task.

Identify committed resourcesIn addition to listing and organizing allrequired tasks, the implementationschedule must identify committedresources to the project. These arepeople who must be available to attendmeetings, and complete assigned taskson the schedule.

The program manager must ensure thatthe committed resources are activeparticipants and complete their taskson time. Typically these resources’current functional job responsibilitieshave not been reduced. As a result,there may be priority conflicts that theprogram manager will need to resolve.

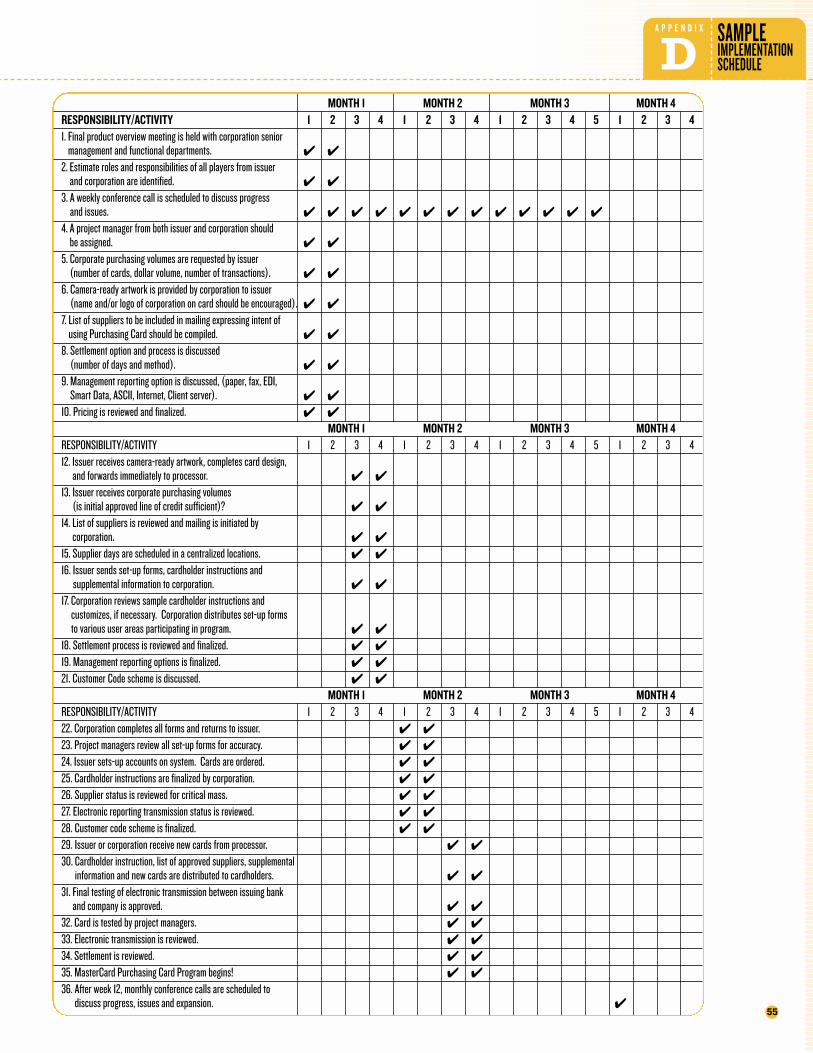

Modify the generic implementationscheduleThis generic schedule provides astarting point from which the team candevelop its own detailedimplementation plan. The final detailedimplementation plan should, at aminimum, include all of the itemsmentioned in section B “Phase 1”. It isimportant that the team develops andagrees on the plan. Hence, committingto the success of the program. Thegeneric implementation schedule isincluded in Appendix D. An electroniccopy is also available.

aWhen using the genericimplementation schedule, the teamshould modify the time line forresource constraints. The programmanager will have a constantbalancing act between the needs ofthe project and the ever-changingavailability of resources.

aIn addition to resource constraints,the team may need to modify thetime line for unique requirements.Some purchasing cardimplementations may requirecustomization of standard productofferings because of uniqueorganizational structure, specializedcustom reporting requirements,complex software integration with in-house systems, major supplier sign-upprograms, etc. Any relevant factorthat could impact the time lineshould be considered. Review progresswith the implementation team.

aThe program manager should reviewprogress with the implementationteam on a weekly basis via a regularlyscheduled weekly meeting whereprogress on the implementationschedule is reviewed, and appropriateadjustments made to the time line oravailable resource base. Thesemeeting should have a preset andpredistributed agenda. In addition,ongoing dialogue with individualteam members should occur as theneed arises.

Identify issues and report progress tosenior managementMinutes should be taken at each weeklymeeting. These minutes should identifyissues and report progress to seniormanagement. Recommended solutionsto any issues should be included in theminutes. Typically the suggestedresolutions will be to change an existingpolicy, extend the time line or addresources to the project. It isimperative that the minutes bedistributed as soon as possible after themeeting to both the team members andsenior management.

Best Practice: From the beginning of the program,develop an implementation schedule withresources assigned for the completion ofindividual tasks.

IMPLEMENTATION

24

5. Establish Program Parameters

Defining the program parameters is theheart of program design. Here is whereyou will decide the structure of yourprogram — which employees willreceive cards, what purchases willqualify, what other internal controlsyou should utilize, how payments willbe settled with your bank, and how toreconcile your transactions with yourGeneral Ledger.

A. Assigning Purchasing Authority

As the process flow illustrates, theprocess change that must accompanythe purchasing card implementationempowers buyers to actually pay for thegoods and services that they use,relieving the purchasing departmentand the accounts payable group fromhaving to perform these tasks.Empowerment of employees can alwaysfeel risky for a corporation. Setting upprogram parameters defines purchaseauthority based on dollar limits andmerchant category codes (MCC) andwill help to control this risk. The desireto control perceived risk must betempered by the need to provide

employee purchasing flexibility. If theemployee finds the program toorestrictive, it will fail. Understandingwhat types of requisitions and othertypes of purchases the cardholdertypically makes to perform his/her jobshould provide the guidance in settingappropriate limits. This will require aculture shift from front-end managerialcontrols to automatic back-endauthorization features.

Purchasing authority can be assigned toindividual cardholders according to anycombination of criteria you choose:dollars per month, dollars pertransaction; number of transactions perday or month, even by supplier type.This means that each individual, eachdepartment, or each division can haveits own custom designed purchasingparameters. This ability to tailor yourauthorization criteria gives you muchcontrol over purchasing expenditures.

When setting spending limits, it’simportant to strike a balance betweenadequate controls and the flexibilityemployees need. You’ll want toperiodically review the spending limitsyou’ve established to see how wellthey’re meeting your organization’sneeds. The program manager cancontact the card issuer to requestadjustments to a cardholder’s purchaseauthorization.

The following details the specifics ofeach authorization control:

• Credit limits — There will be anoverall company credit limitestablished by the card issuer.

• Cardholder monthly spending limit— At the cardholder level, you canset monthly spending limitsappropriate to the employee’s jobresponsibilities. Again, your existingsystem will give you guidance onsetting limits under the new system.You’re likely to want to givesomeone who currently has $10,000a month in spending authority thesame limit on the MasterCardCorporate Purchasing Card.

• Supervisory or departmental roll-upspending limits — The MasterCardCorporate Purchasing Card programallows you to have checks andbalances. In addition the individualcredit limit, a supervisory roll-upspending limit can also beestablished. Here is an example:

An engineering department with abudget of $10,000 per month has sixemployees. The budget manager doesnot know in advance how much of themonthly budget each of the employeeswill spend within a given month.However, he can comfortably assigneach employee a monthly spendinglimit of $3,000, knowing that oncethe group’s cumulative monthlyspending reaches $10,000, alladditional purchases will be declinedauthorization at the time of purchase.

Best Practice:Set up your initial rollout to allow it toreach wide and deep enough to givemeaningful results.

Phase 1 - Program Construction

02S E C T I O N

IMPLEMENTATION

• Transaction limits — In addition tothe dollar limits per month, you canplace limits on individualpurchasing power based on criteriasuch as:

– Dollars per transaction– Number of transactions per day– Number of transactions per

month

In determining your dollar limits pertransaction, consider:

• The statistical business dataobtained from your invoice analysis;(Described on page 19)

• The asset capitalization thresholdvalue of your organization — Manyprograms do not initially allowassets to be procured via theirpurchasing card and, therefore, setdollar limits below this rate

• Supplier categories — You also havethe ability to define the types ofsuppliers where your employees’MasterCard Corporate PurchasingCard can be used.

In the MasterCard network, allmerchants, (suppliers), arecategorized by merchant categorycode (MCC), which is similar to theStandard Industrial Classification(SIC), the code system establishedby the United States Department ofCommerce. You may elect toinclude (or exclude) types ofsuppliers where your MasterCardCorporate Purchasing Card can beused, based on these categories orset different authorization controlsfor different categories of spending.

For example, you could giveauthorization to an employee to makepurchases only at merchants classifiedas office supply merchants and excludeor limit use of the card for travel andentertainment merchants such asairlines, car rentals, hotels andrestaurants. The types of merchantswhere cardholders are allowed to makepurchases and the sizes of thesepurchases are entirely in your control.

Be careful to only enhance thecomplexity of controls where necessary.While it is feasible to allowauthorizations to vary by suppliercategories administered by you, thismay result in inconveniences andconfusion for cardholders attempting touse the card for legitimate businessexpenses. Your company should thinkthrough its spending policies to ensurethat they are realistic and not overlyrestrictive for cardholders.

Using these criteria, you can customizespending authority for your employees.

aAn office manager may be authorizedto make purchases of up to $45,000per month, up to $1500 pertransaction and can only makepurchases with office supply vendors.

aA buyer in the purchasing departmentmay have larger dollar limits and adifferent range of vendors that will beauthorized for purchasing cardpurchases.

aAn administrative assistant may beauthorized to make five transactionsper day, not to exceed $50 pertransaction.

If a cardholder tries to make a purchasethat violates any of the limits placed onthe card — departmental dollar limitsper month, cardholder limits permonth, number of transactions per dayor month, or type of supplier — thetransaction will not be processed.

Maintaining authorization parameterson the cards, increases control, but alsoadds administrative responsibilities forthe card programs. To minimizeadministrative responsibilities, establishno more that three or four programparameter templates includingmonetary and MCC type parameterdesignations.

25

26

The chart above demonstrates two scenarios, one in which allauthorization parameters are met, and one in which an authorizationparameter is violated. In the latter case,the supplier category used to make thepurchase did not match the parametersset up for the cardholder. As a result,the transaction was declined at thepoint of sale.

B. Choosing cardholders for initial rollout

You may want to test your programparameters on an initial rollout todetermine if the program parametersshould be modified before the cards aredistributed throughout the enterprise.While the initial rollout should be of amanageable size, one that is too limitedin scope will not truly test the newprocess.

Selecting a cross section of cardholderswill help you see how the MasterCardCorporate Purchasing Card programcan work in a variety of situations. Youcan use any criteria you like, forexample:

aEmployees (those who request thepurchase rather than today’sauthorized buyers) who generate alarge portion of the low-dollarinvoices.

aUsers who charge all of theirpurchases to one cost center oraccount number ( e.g., secretaries, librarians)

aSelect functional areas (e.g., facilitiesmanagement or maintenance)

aA selected geographical location (i.e.,a plant or a headquarters office)

Phase 1 - Program Construction

Maximizing control over small purchases

IMPLEMENTATION02S E C T I O N

27

C. Electronic Data Management

Your issuer will most likely provide youwith a reporting tool that allows you tomanage and control your purchasinginformation. You should utilize thistool to achieve the following:

aReceive transactional dataelectronically from your issuer;

aDistribute transactional dataelectronically to the cardholder and/ordelegate, and;

aProvide an electronic upload ofvalidated and confirmed transactionaldata directly to your EnterpriseResource Planning (ERP) system.

The following types of functionalityshould be considered whencontemplating your electronic datamanagement needs:

aSystem compatibility with your ERPsystem and operating environment,with proven applicationenvironments;

aCardholder access to electronictransactional data;

aRequired levels of base systemfunctionality, user friendliness andproduct support, maintenance,upgrade conditions, etc.;

aFrequency of transaction dataacquisition from your issuer (matureprograms are now finding the need tohave access to data more frequentlythan monthly to meet financial andexception reporting needs);

aData distribution capabilities,including data validation andpopulation options such astransaction splitting, cost allocationoptions, line item text, projectcosting, taxation accountabilities;

aManagement and exception reportingfunctionality;

aSystem security protocols andprogram position security profiles.

D. Internal Controls and Exception

Reporting

Many companies are moving fromcontrolling at the point of purchase todeveloping audit procedures to ensurepolicy compliance. This has the benefitof empowering employees withoutlosing the ability to monitorcompliance.

Your management reporting tools canbe configured to identify card usageoutside of set parameters and can beviewed by program administrators andline management.

E. Settling Payments with your Issuer

First, you must collaborate with yourbank to define a monthly billing cycleperiod/ program-reporting period tosuite your business needs.

Next, you should establish a simplisticreconciliation process, whereby datadownloads via the issuer or theMasterCard network are reconciled tothe direct debit sweep by your issuer.

F. Reconciling to the General Ledger

Traditionally, cardholders use theirpaper statement to perform datavalidation and cost allocation. Thetraditional paper statement processcontains the following steps:

aCardholder validation of cardtransaction detail on IssuerCardholder Statement to retainedtransaction receipts;

aReconciliation of commercial cardtransactions to manually preparedcardholder transaction log;

aPopulation of transaction log withappropriate cost/charge code andother required line item detail, thensubmission to cost/budget centermanager for endorsement, and;

aCost/budget center managerendorsement, then forwarded toAccounts Payable for journal entryposting to Accounts Payable/GeneralLedger.

The above process requires extensivepaper shuffling and excessive data inputactivity. With recent improvements inreporting and management tools, youcan more efficiently perform these tasksfor your organization.

Utilizing an electronic datamanagement tool with yourMasterCard Corporate Purchasing Cardprogram for transaction data validationand cost/charge code allocation is a bestpractice. The process steps fortransaction data validation and cost/charge code allocation would be;

aElectronic transaction datadistribution to the cardholder (ordelegate where cardholder has nosystem access) or all downloadedtransactions since last distribution(may be daily, weekly, monthly);

aCardholder validates transactiondetails from retained receipts/invoices;

aCardholder can allocate appropriateexpense/account code to thetransaction (or amend the defaultexpense/account code where linked toa Merchant Category Code/Group).Specified range of your organizationsexpense/account codes are loaded intothe system for menu access bycardholder or delegate;

aAdditional project code, assetpurchase details, line item description,taxation information, can be providedto the transaction in fields allocatedwhere required;

Best Practice:Use the Purchasing Card with anelectronic data management tool toreconcile with general ledger.

IMPLEMENTATION

28

aCardholder/delegate can split thetransaction either by amount orpercentage across expense/accountcodes and/or across cost/budgetcenters as necessary,

aCardholder/delegate can screen printconfirmed transactions, attachsupporting documentation and retainfor audit and/or managementscrutiny,

aCardholder/delegate completesvalidation and cost allocation processand forwards transactionselectronically to the cost/budgetcenter for endorsement. Onendorsement, the manager forwardstransaction data electronically to yourMasterCard Corporate PurchasingCard Program Administrator

aProgram Administrator, as and whenrequired, uploads all programendorsed cardholder transaction datato the ERP system as designed.

The use of such a reporting andmanagement tool provides thefollowing benefits:

aUnlimited flexibility in the datavalidation and cost allocation processdesign,

aSignificantly reduces data entryactivity, while enabling expanded datapopulation options,

aDetailed data audit trail ofcardholder/delegate validation andcost allocation activity, and

aGreatly enhanced management andexception reporting as and whenrequired.

All information on your ProgramParameters should be included in yourCardholder Guide. An example of theseguidelines is included in Appendix C1.

6. Enrolling Suppliers

Many successful purchasing cardprograms define supplier categories,such as office supplies, consultingservices, or hardware, which shouldalways be paid via the purchasing cards.The purchasing department then worksto ensure that all suppliers withnegotiated rates in those categoriesaccept the purchasing card.

When invoices are sent from thosesupplier categories for payment, theaccounts payable department can rejectthose invoices and demand that thepurchaser contacts the supplier to paywith his or her purchasing card.During employee training you shouldeducate employees as to which supplier

categories he or she should pay via thepurchasing card versus any otherpayment method.

Supplier categories may be selectedbased on any criteria you choose, suchas volume of invoices or supplier type.For example, you might select suppliercategories that account for the highestvolume of purchase transactions(purchase orders or invoices) asopposed to those with significant dollarvolume.

The following is a supplier strategy thatyou may wish to employ in yourimplementation.

A. Establish selection criteria based on

data analysis.

The objective is to maximizetransaction reduction opportunities.The common rule is 80/20; low-dollarpurchases will often comprise over 80%of the total transaction volume, butthese orders represent under 20% ofthe total dollars spent.

Best Practice:Determine which suppliers to include inyour program by analyzing your currentsupplier database and then develop aspecific action plan.

Phase 1 - Program Construction

OfficeSupplies

ABCStationery

$42,653 565

Hardware Joe'sHardware

$15,000 103

ConsultingServices

SandyGlaser

$110,456 52

SupplierCategory

NameTotal

Dollars

Number ofInvoices/yr.

$ 1000

Sample Supplier Analysis

IMPLEMENTATION02S E C T I O N

29

The Sample Supplier Analysisdemonstrates that office supplies andhardware are supplier categories forwhich your organization gets a majorityof invoices, but which represent asmaller portion of dollars spent. Theseare perfect supplier category candidatesfor your purchasing card program.

B. Determine Data Level Needs

Requirements.

In the introduction, different types ofdata, such as Level II and III, availablewith the purchasing card were outlined.Your organization must determine ifthat enhanced data is needed to ensurethe success of your purchasing cardprogram.

With the purchasing card transaction,along with the merchant address andphone number, you may receiveadditional information from themerchant such as:

a1099 indicator

aMWOB data

aSmall business status

aDuns number

aSupplier’s TIN

This information can help you withyour tax calculations. By purchasingfrom certain suppliers, such as minority-or women-owned businesses, yourorganization may be eligible for taxbreaks. The 1099 indicator can assistyou in reporting taxable transactions tothe government.

Level II data provides sales tax data thatcan assist a company in ensuring thatthey are paying correct taxes for goodspurchased, particularly out of state.This information will assist a companyif the state tax authorities ever auditthem. Level II data also providesadditional information regarding thestatus of the supplier that is needed to

determine whether tax breaks areavailable as a result of using certainminority or women suppliers. If youwant to utilize Level II information toassist with your tax preparations, youmust demand that all of your supplierspass this information. The supplieraction plan below will tell you how toinstruct your suppliers on this matter.

Level II information can also provide acustomer code that uniquely identifieseach transaction — assisting inassigning transactions to your GeneralLedger.

Level III data will provide line-itemdetail to help your company determineexactly which items were purchased.This can assist your procurementdepartment in negotiating better rateson frequently purchased items. Also,this information can allow yourpurchasing department to auditwhether your employees are purchasingthe company-required items — forexample, the negotiated $150 cellphone instead of a top of the linemodel $500 cell phone.

C. Develop a supplier action plan.

Once you have compared your datarequirements to your suppliers’capabilities, you must determine whatactions should be taken to convertsupplier categories defined above to theMasterCard Corporate Purchasing Cardto realize the program benefits.

To determine which of your targetsuppliers currently accept MasterCardcards, and what their current datacapture capabilities are, you mightwant to conduct a survey. In additionto gathering information regardingyour suppliers’ capability to processLevel II and III purchasing card data,the survey can make your suppliersfeel more involved in your program.

If your supplier already accepts cards andprovides the level of data you require:

Convert purchases in the suppliercategory to MasterCard CorporatePurchasing Card. To effectively convertthese transactions, take the followingactions:

aEstablish a supplier list for eachsupplier category of spending.

aMake cardholders aware of thesesuppliers.

aHave the buyer pay for thesepurchases with his/her MasterCardCorporate Purchasing Card.

aInstruct your accounts payabledepartment not to accept invoicesfrom these suppliers or to pay usingthe MasterCard Corporate PurchasingCard.

aRemind cardholders that suppliersmust provide the data you require. Forexample, if customer code is required,ensure that cardholders are trained onproviding this code to the supplier.

If your supplier accepts cards, but doesnot provide the level of data you require:

aInstruct the supplier to contact theirMasterCard card service provider(acquiring bank) for an upgrade.Their MasterCard card terminal orsoftware must be upgraded to eitherLevel II or III data capture as youspecify. Be aware that suppliers musthave a personal computer or hostcomputer to perform Level III.

aSet a time frame for supplierparticipation and communicate thisto the supplier.

aConsider switching suppliers ifcurrent suppliers choose not toparticipate. Select from the list of“Level II and III” suppliers in theMasterCard Corporate PurchasingCard Supplier Directory, located onthe MasterCard web site atwww.mastercard.com.

IMPLEMENTATION

30

If your supplier does not accept cards yet:

aInstruct them to contact theirfinancial institution for a referral to a MasterCard card service provider.They must request Level II or IIIcapability. Set a time frame forsupplier participation andcommunicate this to the supplier.

aPlace your card acceptance and datarequirements in your next RFP orcontract with the supplier.

aInvite your supplier(s) to a seminar —ask your card issuer for a supplierseminar kit.

aConsider switching suppliers ifcurrent suppliers choose not toparticipate. Select from the list of“Level II or III” suppliers and askyour card issuer for a copy of theMasterCard Corporate PurchasingCard Supplier Directory.

To convince suppliers to accept thepurchasing card, you may wish toeducate them on the benefits that theywill receive by accepting the card forpayment.

aReduce the receivable financingcosts: By accepting MasterCardcards, payment will be receivedwithin a few days of orderfulfillment, rather than the typical30- to 60-day receivable cycle.

aReduce invoicing and collection costs:Your suppliers incur significantadministrative costs generating andprocessing invoices. MasterCard cardacceptance means reduced invoices,reconciliation and credit checks fornew accounts.

aReduce bad debt expense: Becausepurchasing authority is verifiedelectronically at the point of purchase,credit risk is transferred from thesupplier to the issuer.

aConcentrate your business within thatcategory: Communicate to yoursupplier that you plan to concentratebusiness within the category andthose suppliers passing the datarequired by your company are likelyto be the preferred vendors and,subsequently, gain additional business.

D. Communicate with your suppliers

Companies have had success with manymethods of communicating their cardprograms to their suppliers. You’ll wantto consider some or all of thefollowing:

aAn announcement letter An announcement letter sent to yoursupplier is the most effective means ofsecuring supplier cooperation with yourprogram. This is an opportunity toclearly communicate to your suppliersthe reasons why your corporation willbe using the MasterCard PurchasingCard, and what benefits they canexpect to realize. (Use the opportunityto enclose a survey asking if theycurrently accept MasterCard cards, andif not, whether they’d be interested inaccepting them). You should alsoinclude a referral to a MasterCardmerchant acquirer that can allow thesupplier to provide the level of data yourequire (your financial institution canidentify service providers for you). Toencourage a supplier to accept the cardfor payment, you may wish to statethat in the future you will only bebuying from merchants who accept thepurchasing card for this type of goodand will no longer accept invoices forpayment for this good category.

Samples of announcement letters mayinclude:

aSupplier Letter 1 (See Appendix B1)

aSupplier Letter 2 (See Appendix B2)

A strong targeted letter campaign canhave great impact. Response rates varywidely, depending on the accuracy ofmailing lists and the strength of yourdirective in the letter. You can createyour own mailing list utilizing yourvendor database. A targeted mailing listis one of the most important elementsof a successful direct mail campaign.See attached appendices for samples of:

aMailing List Guidelines (See Appendix B3)

aSample Fax-Order Cover Sheet (See Appendix B4)

A fax cover sheet alerts suppliers to thecompany’s new payment method.

aSupplier seminarsInvite key suppliers to a seminar toexplain your program. Your card issuercan assist you in this effort, and involvea MasterCard merchant acquirer toreceive applications from interestedsuppliers on the spot.

aInformation pamphletsInformation pamphlets may beavailable through your card issuer. Theyhighlight the benefits to the supplier,and instructs the supplier on how tobegin accepting MasterCard cards ifthey don’t already. The pamphlet willalso explain the requirements for anyadditional data that you, the customer,may require.

aTelephone contactYou may want to speak to key suppliersdirectly to explain the new program orhave a MasterCard card providermarket its services to your suppliers.

Use every opportunity to get yourmessage across.

Phase 1 - Program Construction

IMPLEMENTATION02S E C T I O N

31

E. Develop Reporting on Supplier

Categories

As the purchasing department’s time isfreed from administrativeresponsibilities, it should have moretime to monitor spending to certainsuppliers in certain categories todetermine how much is being spentwith each supplier and what purchasemethod is being used. Thisinformation can assist in:

aSupplier base reduction

aSupplier base management

Your issuer may be able to assist you indeveloping certain suppliermanagement techniques using the datayou receive from your purchasing cardprogram coupled with the dataavailable via your ERP system.Successful supplier management canprovide significant hard dollar savingsto your companies and can befacilitated by analysis of the data thatwill be available to you.

7. Establish Policies and Procedures

Since the purchasing cardimplementation will be changing howpurchases take place in yourorganization, the implementation teammust ensure that it develops policies forthe distribution and maintenance ofthe cards, card usage criteria, roles ofdifferent constituents in thereconciliation of purchases, and disputeof purchases.

aYou must determine how you wantthe cardholder to handle:

• The receipt of materials and servicespurchased with the card

• Maintaining and reconciling recordsand receipts

• The resolution of errors, disputes,and credits.

aHow are you going to distribute cardsto your employee cardholders? Youshould establish a secure, central placeto store the cards you receive fromyour card issuer; and requireemployees to sign for them whenpicking them up.

aYou should immediately cancel adeparting employee’s MasterCardCorporate Purchasing Card (inaccordance with your card issuer’spolicy), and notify the employee of

the card cancellation in writing. This should be part of your standardoperating procedure for any cardholderwho leaving the company, whethervoluntarily or not. The cancellationnotice sent to the employee mustinstruct the individual to immediatelydiscontinue all use of his or herMasterCard Corporate PurchasingCard, and to return the card to thecompany.

aIf there is a dispute over a transaction,the cardholder is empowered toresolve the dispute. The cardholdershould first try to resolve it with thesupplier. If this is unsuccessful, thecardholder should contact theprogram manager.

aSince the card is issued in theemployee’s name and is to be used forbusiness expenditures only; it shouldnot be used by anyone other than thecardholder

aThe card should only be used to makepurchases within the parametersestablished by the company, such asdollar limits or supplier category. (Youshould include instructions on whatto do if a transaction is denied at thepoint of sale.)

aWhile the cardholder may not beresponsible for making payments, thecardholder should be responsible forverifying and reconciling all accountactivity. The cardholder shouldsurrender and cease use of his/hercard on termination of employment,whether for retirement, voluntaryseparation, resignation, dismissal, orin the event of transfer or relocation.The cardholder may also be asked tosurrender the card at any timedeemed necessary by the companymanagement.

Best practice:It is important for your employeecardholders to understand that benefitsand responsibilities of using aMasterCard Corporate Purchasing Card.Consider asking each cardholder to signa formal cardholder agreement detailingthese responsibilities.

IMPLEMENTATION

32

These guidelines and responsibilitiesshould all be included in a CardholderGuide, which must be signed by theindividual cardholder when he or shereceives the card. A sample CardholderGuide is included in Appendix C1. TheCardholder Guide will be discussedfurther in the next Section, Training,since the agreement will be the primarymeans of training the cardholders ontheir roles and responsibilities.

Other Internal Audiences:The impact of implementing thisprogram stretches beyond thecardholders. Many other employees —purchasing, receiving accounts payable,MIS, and internal audit, for example— will need to understand how theprogram will work and what their newroles and responsibilities will be.Examples of policies and procedures toconsider include:

aHow will disputed items be handledin Accounts Payables, (i.e., will A/Pwithhold the disputed amount fromthe payment or will they pay in fulland wait for the credit to post on thenext billing cycle)?

aWhat markings will the receivingdepartment be looking out for onsupplier deliveries made forpurchasing card shipments?

aWhat human resources policies willbe employed if an employee misusesthe purchasing card?

aWhat degree of reconciliation and bywhom, is required to meet internalauditing requirements?

Sections of the guide must also bedeveloped for each of theseconstituencies to ensure that roles andresponsibilities are easy to understandand to follow.

8. Training

Training should be comprehensive,explaining the reasons for the companyembarking on the effort as well asfocusing on specific operational tasks ofeach group.

A. Prepare internal communication

aCardholdersCardholders are where the new processbegins. They will now becommunicating directly with thesuppliers to request goods and servicesbe delivered to the company in orderthat cardholder’s various jobresponsibilities can be completed. Theyneed to be educated in the propercommunication to use with suppliers.

The following are suggested strategiesin tackling the training challenge:

a“Kick-off ” meeting where questionscan be answered

aOnline interactive tutorials

aInternal and external support lines

aNewsletters by internal email or paperfor implementation and on anongoing basis

We recommend that you prepare acardholder guide for your MasterCardCorporate Purchasing Card program asreference for participating employees.The cardholder guide should be givento each cardholder with their card.

While the contents of such a guide willobviously depend on the particulars ofyour program, it should cover thefollowing subjects: (A samplecardholder guide is provided inAppendix C1 of this guide.)

aSenior management endorsementThe guide should begin with a letteracknowledging senior management’scommitment to making the program asuccess.

aProgram overviewTo encourage employee participationand support of the program, employeesshould be given a basic description ofhow the program is going to work.

aCard controlThis section should include a copy of the cardholder application andagreement; information on cardrenewal and cancellation; what to do if the card is lost or stolen; and tips on keeping the MasterCard CorporatePurchasing Card secure.

aCardholder responsibility This section should include the resultsof the policy decisions made in Section02-7 “Establish policies and procedures”.

aList of contactsInclude a list of important contacts forthe program (i.e., how to contact theprogram manager or the card issuer’scustomer service area).

Best Practice:The one common thread shared by allsuccessful programs is a strongcommitment to user training.

Phase 1 - Program Construction

02S E C T I O N

33

IMPLEMENTATION

aReceiving The receiving function also will haveprocedural changes. Typical examples ofthe impact of the purchasing cardprogram are changes in suppliermarkings that Receiving should lookfor on delivered packages and howReceiving should respond to suchmarkings. In addition, there may bedifferent procedures for delivery ofitems received from purchasing cardorders as opposed to the traditionalprocess.

aAccounts PayableAccounts Payable may still be receivinginvoices from suppliers who ship bothpurchasing card orders and traditional“purchase order-invoice” orders. Therewill also be situations where invoicesare inadvertently sent for goods alreadybilled to cardholder purchasing cardaccounts. Accounts Payable personnelneed to be able to recognize theseevents and take the proper action.

aPurchasing DepartmentThe role of the purchasing departmentchanges significantly. For itemspurchased via the purchasing card, itsfocus will be on supplier basemanagement, contract negotiations andcontract compliance. Purchasing willneed to learn how to use the newreports they have available to them tonegotiate with the supplier base.

Program education forums should beheld with all these internalconstituencies to actively driveacceptance and participation in theprogram.

B. Conduct external communication

As discussed in Step 6, EnrollingSuppliers, participation by yoursuppliers is a vital component of thesuccess of your program.

Suppliers also need to be trained inhow they will now be expected todeliver goods and services to thecompany. Key changes from previousroutine may include:

- Special markings on the outside ofpackaging, indicating that thisdelivery is for a purchasing cardtransaction.

- Suppression of the issuance of aninvoice.

- Inclusion of the MasterCard cardreceipt with the packing list andgoods.

- How to identify and properly chargecardholders when consolidatingmultiple orders from multiplecardholders.

- What action to take if a cardauthorization is declined.

Maintaining frequent communicationwith your major suppliers on theprogress of your Purchasing Cardimplementation can ensure that theirstaff is educated about your program toprocure business goods and services.

34

In Phase 1, the groundwork was laidfor the actual issuance of cards tocardholders. In Phase 2, you areready to distribute cards, have youremployees make actual purchasetransactions and monitor all of thesystems, processes and procedures.You should be prepared to makeminor adjustments as eventstranspire that were not adequatelyaddressed in Phase I.

1. Managing and measuring your

program

While each company’s programmanagement will be different, there areseveral tips that every company shouldconsider: