. Presentation Title.

42

. www.InsuranceCommunityUniversi ty.com Presentation Title

-

Upload

opal-parrish -

Category

Documents

-

view

215 -

download

1

Transcript of . Presentation Title.

.www.InsuranceCommunityUniversity.com

Presentation Title

.www.InsuranceCommunityUniversity.com

•Insurance forms and endorsements vary based on insurance company; changes in edition dates; regulations; court decisions; and state jurisdiction. The instructional materials provided by The Insurance Community Center and its authors is intended as a general guideline and any interpretations provided by The Community do not modify or revise insurance policy language. •Information which is copyrighted and proprietary to Insurance Services Office, Inc. (“ISO Material”) is included in this publication. Use of the ISO Material is limited to ISO Participating Insurers and their Authorized Representatives. Use by ISO Participating Insurers is limited to use in those jurisdictions for which the insurer has an appropriate participation with ISO. Use of the ISO Material by Authorized Representatives is limited to use solely on behalf of one or more ISO Participating Insurers.•The authors of these materials, Segale Consulting, LLC and The Insurance Community Center assumes neither liability nor responsibility to any person or business with respect to any loss that is alleged to be caused directly or indirectly as a result of the instructional materials provided.

Segale Consulting, LLC714 206-9583

[email protected] www.segaleconsulting.com

www.theinsurancecommunity.com Copyright 2010

All Rights Reserved

2

.www.InsuranceCommunityUniversity.com

Recall Purpose

3

.www.InsuranceCommunityUniversity.com

What is a Recall?

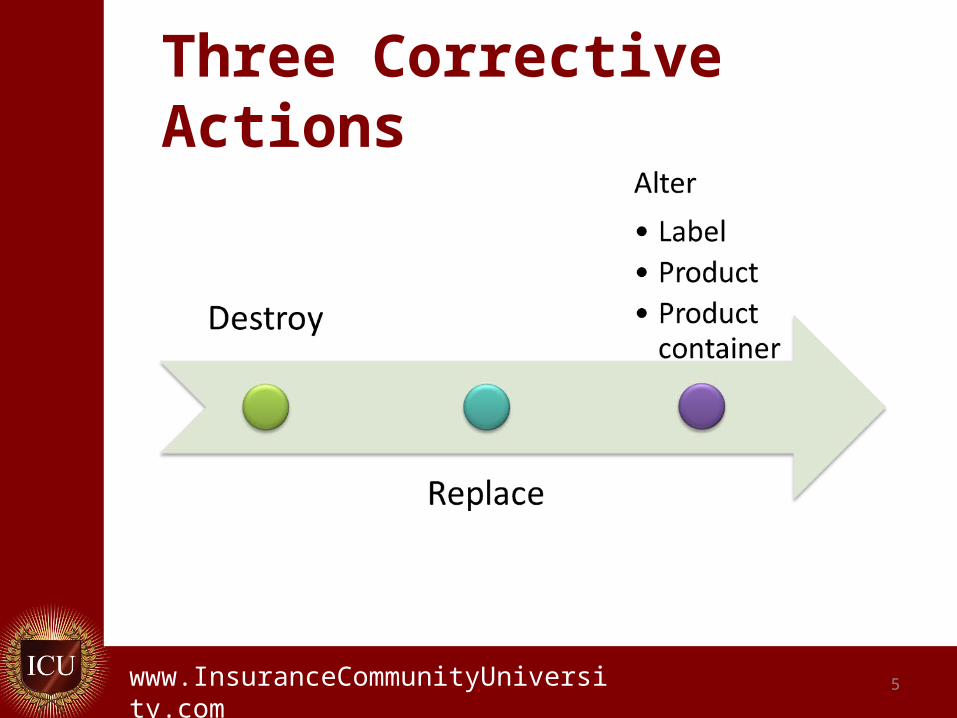

Remove product that can or has caused injury or damage to a consumer from stream of commerce

Includes corrective actions needed to protect consumers from potentially adverse effects of a contaminated, adulterated, or misbranded product

4

.www.InsuranceCommunityUniversity.com

Three Corrective Actions

5

.www.InsuranceCommunityUniversity.com

Who Requires?

Government agency responsible for product category can require and enforce through courts

Recalls are conducted by industry in cooperation with federal and state agencies

6

.www.InsuranceCommunityUniversity.com

Government’s Role

Even though a recall is a company management decision, a government agency can force the company to recall potentially misleading and/or hazardous product from distribution and marketing

Although most recalls are voluntary, these agencies may ask the company to initiate a recall

7

.www.InsuranceCommunityUniversity.com

Common Law Duties

Post-sale duties form part of the common law of negligence

What would a reasonable manufacturer do in the circumstances? Reduce risk to consumer

8

.www.InsuranceCommunityUniversity.com

Reasons For Recall

Labeling mistakes Improper instructions for use Customer complaints

Quality Injury or damage

Contaminants in ingestible items Metal fragments, glass, plastic Insects or other foreign items

9

.www.InsuranceCommunityUniversity.com

Recalls are Expensive

Successful recalls are measured differently

10

.www.InsuranceCommunityUniversity.com

Plan Ahead

11

.www.InsuranceCommunityUniversity.com

Implementation

12

.www.InsuranceCommunityUniversity.com 13

.www.InsuranceCommunityUniversity.com

Product Recall Insurance

14

.www.InsuranceCommunityUniversity.com

Coverage Issues

15

.www.InsuranceCommunityUniversity.com

Coverage Issues and Questions

16

.www.InsuranceCommunityUniversity.com

Generally Desirable Coverages

17

.www.InsuranceCommunityUniversity.com

Generally Desirable Coverages

18

.www.InsuranceCommunityUniversity.com

Generally Desirable Coverages

19

.www.InsuranceCommunityUniversity.com

Generally Desirable Coverages

20

.www.InsuranceCommunityUniversity.com

Coverage Specifics

Policy Language Samples

21

.www.InsuranceCommunityUniversity.com

Policy A

We will pay for expenses you incur for the withdrawal of your product or impaired property, when such withdrawal is made necessary by reason of determination by the insured or by any ruling of any governmental body that the use of such product or property could result in bodily injury or property damage, because of any known or suspected defect, deficiency, inadequacy or dangerous condition in it.

22

.www.InsuranceCommunityUniversity.com

Policy A

This insurance applies only to expenses incurred from withdrawal of such product or property, initiated during the policy period and within the coverage territory.

23

.www.InsuranceCommunityUniversity.com

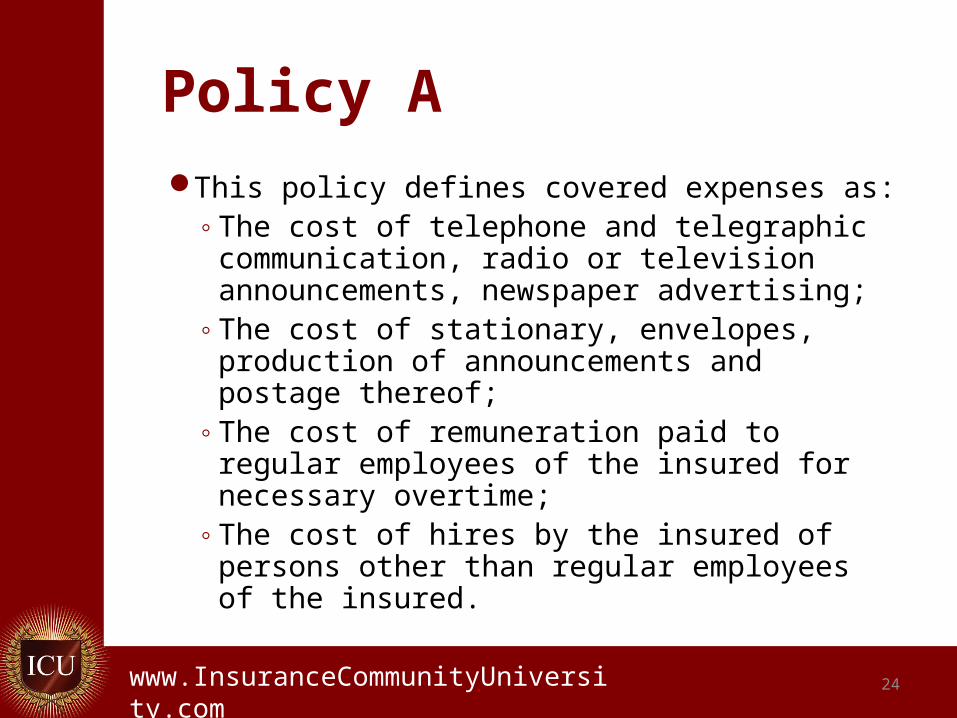

Policy AThis policy defines covered expenses as:◦The cost of telephone and telegraphic

communication, radio or television announcements, newspaper advertising;

◦The cost of stationary, envelopes, production of announcements and postage thereof;

◦The cost of remuneration paid to regular employees of the insured for necessary overtime;

◦The cost of hires by the insured of persons other than regular employees of the insured.

24

.www.InsuranceCommunityUniversity.com

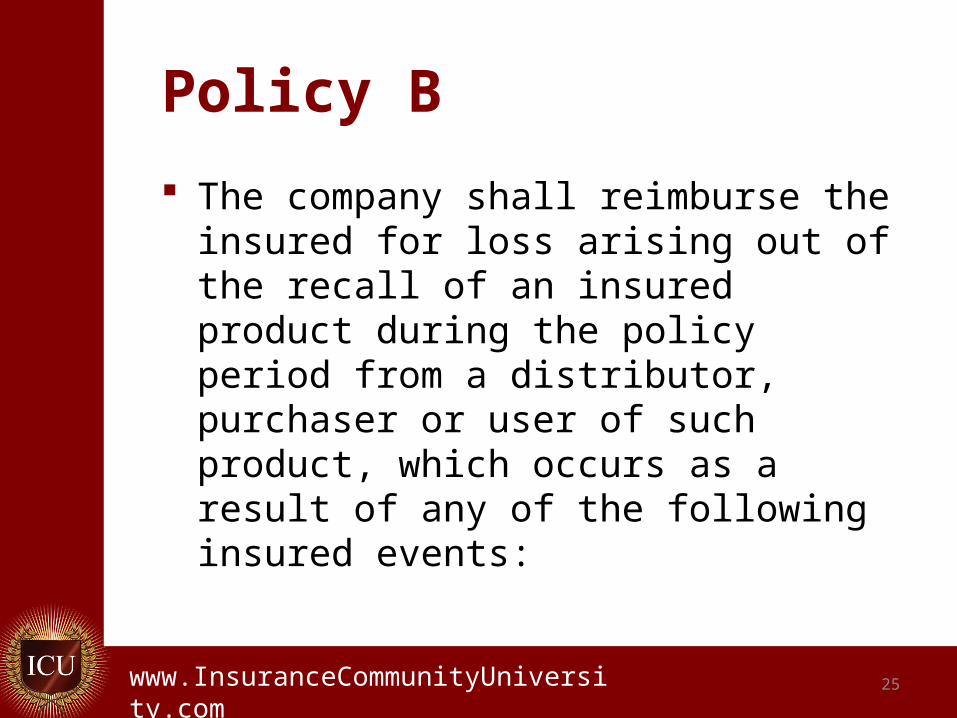

Policy B

The company shall reimburse the insured for loss arising out of the recall of an insured product during the policy period from a distributor, purchaser or user of such product, which occurs as a result of any of the following insured events:

25

.www.InsuranceCommunityUniversity.com

Policy B

◦ Accidental omission of a substance in the manufacture of the insured product; or

◦ Accidental introduction or accidental substitution of a substance in the manufacture of the insured product; or

◦ Error in the design, manufacture, packaging, blending, mixing, compounding, labeling or storage of the insured product; or

◦ Intentional damage to the insured product by an employee or by a third party.

26

.www.InsuranceCommunityUniversity.com

Policy B

Provided, that the use of the insured product has resulted or would result in widespread physical injury or widespread property damage caused by or because of the four points above and that insured adheres to the recall plan in responding to the recall.

27

.www.InsuranceCommunityUniversity.com

Policy BAny reasonable and necessary costs incurred by

the insured to inspect, withdraw, destroy, repair or replace the insured product.

This may include the following:◦The cost of communications to notify others of

an insured event resulting in a recall, including but not limited to radio or television announcements and Internet or printed advertisements;

◦The cost of shipping the insured product from any purchaser, distributor or user to the place or places the insured designates

28

.www.InsuranceCommunityUniversity.com

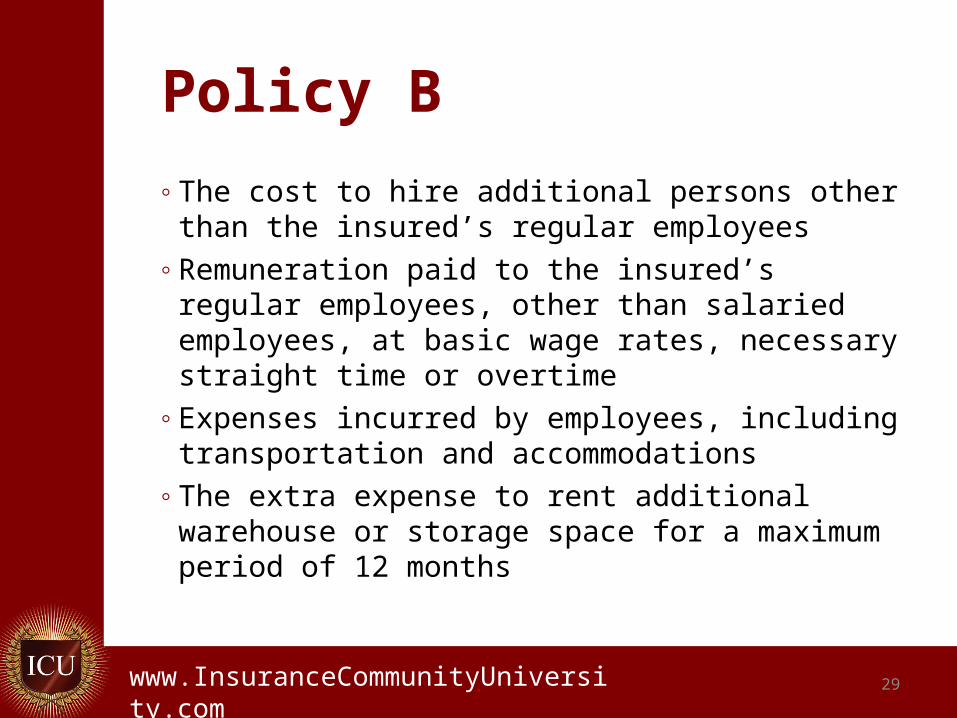

Policy B

◦The cost to hire additional persons other than the insured’s regular employees

◦Remuneration paid to the insured’s regular employees, other than salaried employees, at basic wage rates, necessary straight time or overtime

◦Expenses incurred by employees, including transportation and accommodations

◦The extra expense to rent additional warehouse or storage space for a maximum period of 12 months

29

.www.InsuranceCommunityUniversity.com

Policy B

The actual cost of disposal of the insured product, but only to the extent that specific methods of destruction other than those usually employed for trash discarding or disposal are required to avoid bodily injury or property damage as a result of such disposal

The actual cost to redistribute any recalled or restored insured products

30

.www.InsuranceCommunityUniversity.com

Policy B

Reasonable and necessary fees and costs of independent security, public relations or recall consultants to assist insured in responding to an insured event, provided that the company has given prior consent to the use of such independent specialist companies. These fees and costs are not subject to any deductible under this policy.

31

.www.InsuranceCommunityUniversity.com

Policies A & B

Both policies allow for reimbursement of standard recall expenses: The cost of informing the public of the recall, The cost of having the product returned or

destroyed, Overtime expenses for regular employees

necessary to effectuate the recovery, and The cost of hiring outside persons to assist in the

recall process.

32

.www.InsuranceCommunityUniversity.com

Policies A & B Some major differences:

Policy A bases coverage on the insured’s determination of necessity

Policy B’s coverage is narrower because it is limited to the occurrence of specific events

Policy A includes a listing of specific costs covered by the policy

33

.www.InsuranceCommunityUniversity.com

Policies A & B

Policy B bases reimbursement on "any reasonable and necessary costs" and also lists covered costs

Policy B’s list of reimbursable costs is more realistic and inclusive

Policy B requires prior approval by the insurance company of an insured’s recall plan and requires adherence to the plan by the insured

34

.www.InsuranceCommunityUniversity.com

Policies A & B

The requirement in Policy B to follow a recall plan approved by the insurance company could be significant to a company implementing its procedures

Policy B defines the recall plan as "the insured’s written product recovery document submitted to and approved by the insurance company, which forms part of the policy"

35

.www.InsuranceCommunityUniversity.com

Coverage Review

Determine your client’s specific needs Industry Self-funding capability Loss Control measures employed

Quality control Testing Recall manual

Obtain policies and review coverage language for appropriate response

36

.www.InsuranceCommunityUniversity.com

US Agencies Involved In Recall Oversight

37

.www.InsuranceCommunityUniversity.com

Product Lines of Oversight

Food and Drug Administration Medical devices

Food Safety and Inspection Service of the U.S. Department of Agriculture Meat and poultry

Bureau of Alcohol, Tobacco and Firearms Alcoholic beverages containing impurities or

unapproved substances, or mislabeled)

38

.www.InsuranceCommunityUniversity.com

Product Lines of Oversight

Two government agencies, the Food and Drug Administration (FDA) and the U.S. Department of Agriculture Food Safety and Inspection Service (USDA FSIS) share regulatory responsibility for food product recalls The FDA is responsible for domestic and imported

foods The USDA FSIS is responsible for meat and poultry

39

.www.InsuranceCommunityUniversity.com

Product Lines of Oversight

As an exception, responsibility for eggs is shared by the FDA and the USDA

The USDA FSIS regulates pasteurized egg products (eggs that have been removed from their shells for further processing) and the FDA assumes responsibility for egg products after leaving the processing plant

40

.www.InsuranceCommunityUniversity.com

MarketsCapacity always major issue (high loss ratio)Expanding marketplace (buyer awareness)◦Chartis and Lloyd’s of London largest insurers◦ Liberty Mutual◦XL◦C. V. Starr◦Crum & Forster◦Zurich◦Specialty markets for health related items, food

and auto parts and manufacturing

41

.www.InsuranceCommunityUniversity.com

Summary

Risk Management◦ Insured should be prepared◦Utilize Product Recall Manual◦Quality control measures in place◦Updates on government requirements

Insurance◦The proper coverage is hard to find and very

expensive◦ Insured will share in loss with large deductibles

42

![[PPT]Title of presentation Title of presentation Title of …unstats.un.org/unsd/accsub/2012docs-20th/Presentation... · Web viewTitle Title of presentation Title of presentation](https://static.fdocuments.us/doc/165x107/5aec2a637f8b9ac3619019c7/ppttitle-of-presentation-title-of-presentation-title-of-viewtitle-title-of.jpg)

![[Presentation Title]](https://static.fdocuments.us/doc/165x107/5552690fb4c905d41d8b50ba/presentation-title-5584a0ded60d0.jpg)