· Web viewPRIVATE PENSIONS: REGULATORY ISSUES Jean-Jacques Gollier 2000 Insurance and Private...

138

Organisation for Economic Co-operation and Development Publication sponsored by the Japanese Government INSURANCE AND PRIVATE PENSIONS INSURANCE AND PRIVATE PENSIONS COMPENDIUM COMPENDIUM FOR EMERGING ECONOMIES FOR EMERGING ECONOMIES Book 2 Book 2 Part 2:1)d Part 2:1)d PRIVATE PENSIONS: REGULATORY ISSUES Jean-Jacques Gollier 2000 This report is part of the OECD Insurance and Private Pensions Compendium, available on the OECD Web site at www.oecd.org/daf/insurance-pensions/ The Compendium brings together a wide range of policy issues, comparative surveys and reports on insurance and private pensions activities. Book 1 deals with insurance issues and Book 2 is devoted to Private Pensions. The Compendium seeks to facilitate an exchange of experience on market developments and promote "best practices" in the regulation and supervision of insurance and private pensions activities in emerging economies.

Transcript of · Web viewPRIVATE PENSIONS: REGULATORY ISSUES Jean-Jacques Gollier 2000 Insurance and Private...

Organisation for Economic Co-operation and DevelopmentPublication sponsored by

the Japanese Government

INSURANCE AND PRIVATE PENSIONSINSURANCE AND PRIVATE PENSIONSCOMPENDIUMCOMPENDIUM

FOR EMERGING ECONOMIESFOR EMERGING ECONOMIES

Book 2Book 2Part 2:1)dPart 2:1)d

PRIVATE PENSIONS: REGULATORY ISSUES

Jean-Jacques Gollier

2000

Insurance and Private Pensions UnitFinancial Affairs Division

This report is part of the OECD Insurance and Private Pensions Compendium, available on the OECD Web site at www.oecd.org/daf/insurance-pensions/ The Compendium brings together a wide range of policy issues, comparative surveys and reports on insurance and private pensions activities. Book 1 deals with insurance issues and Book 2 is devoted to Private Pensions. The Compendium seeks to facilitate an exchange of experience on market developments and promote "best practices" in the regulation and supervision of insurance and private pensions activities in emerging economies.The views expressed in these documents do not necessarily reflect those of the OECD, or the governments of its Members or non-Member economies.

Directorate for Financial, Fiscal and Enterprise Affairs

TABLE OF CONTENTS

Introduction 3Chapter I - General features of a private pension system 3

Section 1. Definition of private pension systems 3Section 2. Why private pension schemes? 4Section 3. Typology of private pension systems. Design of plans 6Section 4. Financing mechanisms of private pension systems 8Section 5. Regulations applicable to private pension funds 13Section 6. The role of financial institutions 14

Chapter II – Private pension funds in the countries studied 15Section 1. Structural options for the first pillar 15Section 2. Interaction between the three pillars 22

Chapter III – Second-pillar schemes and control rules in the countries studied 27Section 1. Statistics on funding provisions 27Section 2. The relative proportion of insurers in private pension schemes 30Section 3. Applicable supervisory standards 38Section 4. Technical standards 41Section 5. Tax standards 43Section 6. Accounting standards 46Section 7. Selected information about the third pillar 47

Chapter IV - Some specific points 54Section 1. The switch from defined benefit to defined contribution schemes 54Section 2. Commutation of benefits. Property aspects 58Section 3. Methods of adjustment 63

Chapter V – A dynamic approach to private pension management 64Section 1. General Considerations 64Section 2. Prudential standards and asset liability management 68

Chapter VI -- Current issues -- Conclusions 81Section 1. Review of current issues 81Section 2. Synthesis of main trends 85Section 3. By way of conclusion. 86

Note No. 1 : THE MEANING OF THE PARAMETER B1 88

Note No. 2 : USE OF REGRESSION LINES 89

3

Introduction

1. There have been many studies of private pension fund systems, in particular by the OECD. A lot of information is available on this issue, as well as on social security systems. It is, however, extremely difficult to collate this information and comment because:

social security and private pension systems often differ significantly from one country to another;

it is difficult to communicate information within the same country and even more difficult for specialists from other countries to understand this information. As in many other areas, communication in this area is a big problem because what is considered quite normal in one country may be considered incomprehensible elsewhere.

when the study covers several countries there is always a risk that laws and regulations have changed between the date the general report was written and the date the documentation on the countries is compiled.

there are often shortcomings in the statistical material and it is sometimes difficult to know what the figures given actually correspond to. The difficulty is compounded when one tries to compile comparable tables of data that are valid at the same date.

This study covers the following countries. Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Japan, Korea, Luxembourg, Netherlands, New Zealand, Portugal, Spain, Sweden, Switzerland, United Kingdom, United States.

It aims to highlight a number of factors which are essential to the understanding of private pension systems and focuses in particular on the interactions between private pension funds and the financial services, insurance and banking sectors.

To facilitate understanding of the issues, the author thought it was preferable to begin by outlining the general features of a private pension system and then to describe actual systems in relation to the general model. This is done in Chapter I. Chapters II and III, after presenting the general typology of first-pillar pension systems which is essential for understanding the other two pillars, discuss the main features of the 22 countries studied in relation to the general model. A number of specific points are discussed in Chapter IV.

Chapter V offer some guidelines that may lead to a dynamic management of private pensions, within the context of the European Commission green book. Finally, Chapter VI reviews the main issues in the various countries and concludes.

Two notes are included in an annex, the first one concerning the precise meaning of parameter B 1 (a measure of the compensation bracket covered by first tier pensions), the second one deals with the use of regression analysis.

Chapter I - General features of a private pension system

Section 1. Definition of private pension systems

2. For the purpose of this study the term 'private pension system' shall refer to any financial arrangement implemented within a company or group of companies for the purpose of providing the

4

employees thereof and their beneficiaries with complementary pension benefits in addition to those paid out by government pension schemes. That definition also encompasses systems set up

by companies on behalf of agents, or their beneficiaries, even though they are not payroll employees but rather independent contractors;

by trade and professional associations on behalf of individuals meeting the criteria for membership, or their beneficiaries.

The primary characteristic of such arrangements is that they are at once outside the realm of government pension plans such as social security and that they complement the benefits of the latter. Under normal circumstances, their purpose is not to substitute completely government pensions. A partial substitution exists in certain instances, such as in the United Kingdom, through the practice of 'contracting out', which is aimed at reducing the burden on government institutions and generating reserves applicable against future expenses.

The fact that these private pension systems are outside the government systems evidently does not mean that they escape monitoring by the authorities or even in some cases government oversight. The opposite in fact is true. We will see that multiple technical, legal, social, tax and accounting controls apply to them.

3. It should be noted that the above definition covers a very large number of schemes that differ in terms of the structure of the system as well as of the financing supports used. They have a common purpose, namely to supplement social security benefits, but they function in different ways and are hence subject to different government control structures.

The purpose of this report is to describe the common features of such schemes and to suggest some directions in which they might converge.

Hereafter the term “private pension fund” will denote any private system as defined above.

4. This study examines the pensions of civil servants only insofar as they have a first-pillar social security scheme which covers all workers in both the private and public sectors, together with supplementary schemes which can be usefully compared with private pensions.

Section 2. Why private pension schemes?

5. Before proceeding any further, it is worth describing briefly the three-pillar system which underpins our general model. In such a system, the theory of which comes from Switzerland, pensions should ideally comprise three pillars:

the first is the State-run public pension that is part of the social security system. In principle, it aims to provide a minimum income, is based on solidarity and is normally financed on a pay-as-you-go basis, without constitution of large reserves;

the second is the supplementary pensions provided collectively by firms or socio-professional groups. It aims to provide a deferred income in addition to the first which offers a sufficient rate of replacement of earned income. These pensions are usually funded;

5

the third pillar consists of all the savings put aside by an individual for his old age. These are thus personal savings that need to be distinguished from precautionary saving for a nearer future.

6. A preliminary and fundamental question that needs to be asked is why second-pillar pensions, the supplementary pension plans, exist in the first place.

The social security system is the first constituent of old-age coverage and is based on the notion of solidarity, generally operating, therefore, on a pay-as-you basis, meaning that reserves do not need to be proportional to future commitments.

However, solidarity cannot be stretched without limit, even paying for pensions at the highest income brackets, since it normally implies a certain redistribution from the richest to the poorest.

Above a given ceiling, reliance on solidarity must hence be limited and an approach that is closer to capitalisation has to be used.

Under the circumstances, why would it not be sufficient to have social security on the one hand and individuals' personal savings on the other? In other words, why create a second pillar, that of supplementary pension plans set up by companies or trade associations? Why has this second pillar emerged between the first and the third?

Many answers can be given to these questions, the principal motives cited being

the risk that individuals will be improvident, even at a relatively high level of income;

the notion that employers have a certain responsibility towards their employees, even at this level of income;

the notion of deferred income, with compensation for workers consisting increasingly of elements other than cash wages;

the possibility of obtaining higher returns and of reducing financial risks when acting jointly.

These are some of the reasons why supplementary company pension plans, the so-called second pillar, have come into being.

7. In this three-pillar approach, where overlapping or substitution possibilities exist, pensions are ultimately divided into three constituent parts, which are

a common revenue, i.e. social security retirement benefits

deferred income, i.e. company supplementary pension plans

saved income, i.e. individual provident savings.

To sum up:

Social security can provide only limited pension benefits, restricted to what solidarity between generations allows short of taking excessive economic or political risks;

6

the third pillar, made up of purely individual savings or provident plans, is financially risky from many points of view because of economic and social developments as well as the lack of foresight on the part of individuals.

All of this explains the existence and the continued growth of the second pillar, that of supplementary pension plans. Occupying a place between the first pillar - which is wholly collective, compulsory and interdependent - and the third, which is purely individual, it makes it possible to achieve objectives that supplement the former and the latter with a greater degree of security than either.

8. There is another important reason for the growth of supplementary pension plans, namely the ageing of the world population, especially in OECD Member Countries.

The drop in birth rates and the increase in life expectancy on the one hand (demographic factors) and the impact on employment of productivity increases in domestic economies as well as in the world as a whole (as a result of globalisation), on the other, are going to significantly increase the burden of pensions as measured in terms of the share of the total wage bill for which coverage exists, which, for all these reasons, will increase less rapidly than the benefits to be paid.

It cannot be postulated that solidarity between generations is limitless, with our children and grandchildren consenting, under an unfunded benefit system, to pay significantly higher contributions in return for the same or even lower pensions for themselves.

The current generations must therefore now accept to pay higher contributions in order to build up reserves that can be applied against future expenses. Those reserves will have a particularly positive impact since they will be invested directly into the economy, thereby promoting economic growth.

There are thus very good reasons to create such reserves as part of the second pillar, the supplementary private pension systems, as governments, in their role as managers of the first pillar -- the State pensions -- cannot usually perform that task.

Section 3. Typology of private pension systems. Design of plans

9. The idea of an objective to be attained

We shall first examine what form those systems can have, what is often referred to as the design of supplementary plans.

It is evident that, when creating this type of pension system, a given purpose is foremost in mind and certain objectives should be agreed upon jointly with representatives of the future beneficiaries of the pensions, following preliminary discussions concerning the general appropriateness and economic feasibility of the project.

At this stage of our examination, it would be useful to describe the financing mechanism used, which can be pictured by the following graph:

7

During the worker's years of employment (A to R) contributions are paid which are, if possible, capitalised as reserves so as to enable the fund to pay out expected benefits from the time the worker ceases to be gainfully employed until the death of the worker, or of the worker's spouse if there is a beneficiary clause (R to D). The deferral of a portion of the worker income makes it possible gradually to generate the worker's replacement income.

10. Systems with defined benefits or defined contributions

Actuarial methods make it possible to compute the actual ratio of contributions to benefits. It would seem therefore that we are faced with an equation with two variables, where one is designated as the unknown, whose value must be determined. Consequently, two systems exist and operate in an opposite fashion, so to speak:

under a system of defined benefits, these benefits are determined primarily on the basis of pay rates, so that what needs to be computed are the contributions that make this possible; contributions are thus the unknown factor in the equation;

under a system of defined contributions (or costs), contributions are set initially and the benefits ultimately payable are the unknown element.

In the above graph, the movement can be said to be from the right to the left under a system of defined benefits, and from the left to the right under one of defined contributions, which shows that the systems operate in opposite ways.

It is evident that, in either instance, actuarial methods make it possible to compute the amounts required to be set aside in the case of defined benefits, or the benefits available at retirement time under a system of defined contributions. Increasingly, sophisticated actuarial and financial practices have considerably reduced the uncertainty margins in the contributions/benefits equation or, at least, have served to highlight those parameters whose variations are critical and the potential repercussions of such variations. In this connection, computing technology now makes it possible to achieve considerable progress in that area.

11. The existence of a degree of freedom

A further remark: contrary to frequently held views, a certain degree of freedom still remains as to the computation method, namely concerning the ways in which promised or expected benefits are calculated. Different actuarial methods can call for various manners of allocating contributions over the working life of employees, for instance by contributing little early on and far more in later years of employment. The assumptions made for the parameters can have a similar impact.

8

If for instance, a high rate of interest is chosen for computation purposes, contributions required for funding will be lower when the employee is young, since pension benefits are still distant in time and accumulated reserves are expected to have a high yield. Had the assumption been made that interests rates would be lower, required contributions would be higher at first, but excess interest income over the assumption made would subsequently make it possible to reduce them.

Such a possibility of spreading in different ways over time the contributions required for funding a given benefit is not free of risks for future beneficiaries, including the possibility that the company may fail, or may experience difficulties in meeting fast-rising expenses; or even for the company's shareholders or creditors, who watch the financial position of the company deteriorate over time due to increasing pension contributions.

12. Obligation of “best effort” or of “result”

Attention must be given to the fundamental difference that separates defined benefit systems from those with defined contributions. From a legal point of view, the former carry an obligation to achieve a specific result (performance requirement), whereas the latter are only subject to a best efforts standard.

Systems with defined benefits guarantee the payment of a certain replacement income upon retirement or in the event of death either before or after retirement (obligation of result). Their operation therefore involves certain risks for contributors, plan members and employers. Since contributions vary according to developments of a demographic, economic and financial nature affecting the system, a clause may be included in the system's bylaws, pursuant to which, in the event that expenses incurred exceed a given level, the planned benefits may be adjusted accordingly. That is the type of problem that most government pension plans in OECD countries are currently faced with.

On the other hand, under defined contributions systems, the only obligation concerns funding, meaning that there is a commitment to make the contributions called for and to invest those set aside as prospective reserves in a responsible and prudent manner. Still, if the benefits obtained at the end are insufficient, contributions may have to be raised, for such purposes as to pay supplemental benefits out of reserves set aside or from additional contributions, required whenever inflation accelerates.

13. Commutation of benefits

Second-pillar schemes sometimes provide for the option of a partial payment in the form of a capital sum. In some cases, the pension may be paid entirely in the form of a lump sum.

The latter case, which corresponds in fact to a sort of severance pay, is usually found in countries with rapidly rising inflation, where private pension funds, and thus employers, find it difficult to finance life annuities.

When it is merely a case of partial or total commutation of benefits, it may be warranted by the attraction of a capital sum even if the price is a lower income.

Section 4. Financing mechanisms of private pension systems

14. Internal or external mechanisms

Once a decision has been made as to the 'design' of a private pension system, a financing mechanism has to be selected for it. As part of the financial package which the system requires, who is going to handle the

9

process from point A where plan members contribute, to point R where they receive the benefits guaranteed by the system?

Hereafter we shall limit our discussion to those systems - the most common ones - set up by companies on behalf of their employees. A distinction must be made here between internal and external mechanisms.

In the case of internal mechanisms, the company makes no payment outside its accounts prior to the time when benefits are to be paid pursuant to the plan. It is often said, in such cases, that these supplementary pensions are not funded.

Then there are external mechanisms for which amounts required for funding are paid out by the company to an entity which subsequently pays the benefits called for under the plan.

We are going to examine first internal mechanisms, then external ones.

15. First internal mechanism: overhead expenses budget

The first internal mechanisms is the payment of pension benefits directly out of the company's budget for overhead expenses (the so-called "pay-as-you-go" practice). In this instance, a company pays benefits directly from the time of an employee's retirement or death, to that employee or to his or her beneficiaries. Payment can be made on the basis of internal company rules, either known to employees or not, or else on a case-by-case basis depending on merit or needs.

Operating in this manner is considered very hazardous

for the company which does not set aside any reserves for the future, even though the cost of the system is expected to increase with time and could pose a threat to the future financial soundness of the business;

for shareholders, as the profit and loss account does not reflect the accrued cost of supplementary pension benefits; dividends paid out today are therefore artificially high and biased in favour of current shareholders, at the expense of future ones;

for retired as well as current employees, who could lose everything if the company went bankrupt. Most countries have prohibitions against such pay-as-you-go systems.

16. Second internal mechanism: book reserves

The company and its shareholders can reduce the risks from pension costs being charged to overhead expenses by setting aside reserves in the books. The amount of such provision is computed by actuarial methods that are often the subject of detailed regulations.

The properties of such as system are as follows:

for the company, the setting aside of reserves against pension benefits payable in the future makes it possible to absorb coming increases in costs, while the corresponding funds are available to the company and can be invested in its operations;

Everything proceeds as if the long-term provisions were added to the company's equity, enabling it to fund its pension commitments. The interest paid on those provisions is equal only to the technical interest that serves as an underlying basis for the provisions and is generally below the long-term rate on money markets. In most cases, the provisions are in

10

fact invested in the company, the return on them being that on the company, which usually makes it possible to cancel out the consequences of inflation, especially in countries where it is rising rapidly;

for the shareholders, fairness is restored between the generations;

for retired and current employees, on the other hand, the situation remains unchanged in terms of the risk that the company could go bankrupt; they have no special privileged claims on assets and are considered to rank equally with other creditors, after the tax authorities and social security administration, etc., meaning that they stand little chance of recovering a significant share of their pension benefits in the event of bankruptcy.

It is also possible to reinsure commitments entered into by a company under this kind of system. If an employer chooses to do so, it can secure a group policy from an insurer, providing coverage for the commitments made with respect to employees, either in whole or in part. The company, rather than its employees, is the beneficiary of such a policy.

Normally, the company thereby will book in its assets a claim against the insurer equal to the amount of the actuarial reserve set aside by the latter.

This approach enables the company to cut down on liquidity problems caused by the payment of benefits, although it does not seem, on the other hand, to provide employees with improved guarantees in the event of bankruptcy. Yet the safeguarding of vested pension rights, as that of the benefits themselves, has been the subject of a European directive (80/987 EEC).

In order to reconcile the interests of employers and employees and the requirements of the European provisions, some countries have introduced a reinsurance system covering companies' solvency in the event of bankruptcy, for those setting aside pension provisions in their balance sheet. Under that system, employers pay annual premiums to an insolvency reinsurance pool, based on reserves that are or should be set aside in order to pay future pension benefits to current and future retired employees, whenever no such provisions have been made outside the company.

17. Individual pension guarantees

A company may wish to provide special pension benefits to some of its employees or officers, on a purely individual basis.

This is sometimes handled through a personal pension guarantee in the form of an agreement between the company and the employee or officer in question.

Under that guarantee, the company promises to pay benefits upon retirement or in case of death prior to retirement and, in some instances, of disability. Normally, as in item 16, the company should set aside a reserve in its books.

It can avoid having to do so, however, by taking out an individual insurance policy on its own behalf, as in the case of the reinsurance of provisions, for the same benefits as those promised under the pension agreement.

18. First external mechanism: self-administered pension funds

11

The first external mechanism is the self-administered pension fund. It is a legal entity distinct from the employer itself, generally a non-profit company or a similar legal entity, or trust on the Anglo-Saxon model.

The employer calculates - or has an actuary calculate - what reserves are required to provide for future benefits, and allocates to the pension fund, which is independent of the company, the corresponding amounts, taking into account interest income by the fund and benefits payable.

Because self-administered pension funds exist independently of the company, the employees of the latter are protected in the event the company goes bankrupt, with the effect being only that no more money is paid into the fund, while amounts already in the fund cannot be reclaimed by the company.

It is evident that this type of financing mechanism necessarily involves both fixed and variable administrative expenses. Among fixed expenses are those incurred for starting up the fund, preparing legal documents, accounting, etc. and they may account for a major share of total expenses. It is therefore obvious that such a structure can generally be used only if contributions to the private pension fund are substantial.

It must be recognised that savings can be realised only if the sums managed are substantial and if competition among insurance companies would not make it possible to obtain equally advantageous conditions, with the added advantage of limiting the investment risks.

The question may be asked whether the main advantage of self-administered pension funds is not precisely that they give employers the opportunity to choose on their own the financial risk to which they agree to be exposed.

All the available statistics show that properly managed higher-risk investments have a medium-to-long-term yield that is significantly higher than risk-free investments.

However, in that event, it is extremely important that the employer limits that risk as much possible, with due regard to the exposure of the company itself, for it would definitely run counter to the interest of the fund for it to incur investment losses at a time when the company is having problems, a factor that underscores the need to properly manage fund assets.

This situation is more likely to arise in the case of self-administered funds than in that of funds handled by outside insurers, unless more sophisticated methods of investment allocation are used.

Lastly, it should be noted that pension funds do not have performance obligations to their members. They collect contributions paid to them by employers so as to live up to the commitments resulting from the pension plan bylaws. Any financial shortfall would therefore be covered by the employer.

19. Second external support: group insurance

The second external mechanism consists of group insurance. Under that system, employers turn to an insurance company. The employer and the insurer jointly draft a group insurance contract specifying the respective rights and obligations of the parties, namely the insurer, the employer, policyholders and their beneficiaries.

Based on that contract, the insurer computes the premium that needs to be paid, in the form of contributions either by employees or by their employer.

12

Individual contributions are always individually funded and therefore pay for individual insurance policies guaranteeing the payment of benefits upon retirement or in the event of death prior to retirement.

Under a system of defined contributions, contributions by employers are always individually funded and hence also pay for individual insurance policies.

On the other hand, under systems of defined benefits, two approaches are available. If the method used is that of individual funding, employer contributions are paid on individual policies, whereas if employer contributions are part of a group funding, no such individual policies exist.

The individual funding part determines the ratio of premiums to benefits, based on a life insurance rate schedule. That schedule in turn depends on interest rates, technical interest rates, mortality tables and administrative expenses incurred by the insurance company in connection with its operation as well as, in certain instances, commissions paid to intermediaries.

The fact that life insurance rates are used evidently implies that the insurer has performance obligations, since specific benefits are guaranteed in consideration for the payment of premiums.

It should be noted, in addition, that whenever employer contributions are - at least in part - allocated to collective funding, a certain interest rate can also be guaranteed, so that here again the insurer makes a commitment insofar as performance is concerned.

From the point of view of the insurer, the obligation to achieve a specific result is in fact always limited to the level of compensation established at the time of computing the premium. The performance obligation -- with benefits expressed as a percentage of the final income, in case of defined benefits -- implies that the necessary premiums are recomputed every year and thus always hinges on the employer being willing and able to pay the required premiums.

The case may also arise where the insurer funds all or part of the employer contributions on a group basis without making a commitment as to the rate of interest or the nominal value. This is the situation when assets are managed as mutual funds or as allocated investments.

20. The management of group pension funds

The notion of collective funding in group insurance is akin in fact to another concept, that of the management by insurance companies of group pension funds.

The technique was developed several decades ago, at the same time as group insurance. It is sometime referred to as 'deposit administration' or 'separate account'. As pointed out earlier, this is a special form of group insurance, where the insurance company manages a joint account into which an employer pays contributions, and from which the insurer pays out the benefits specified by the policies when they come due, hence the term 'deposit administration' reflecting the idea of an account that is set aside for a specific purpose, which constitutes a collective provision on the liability side of the insurer’s balance sheet.

One can go even further by covering this liability with an allocated investment, which is then called a “separate account”.

The insurer, or an actuary working for the employer, calculates -- using recognised actuarial methods -- the amount of contributions required by the group pension fund in order to enable it to pay out the benefits promised by the employer to the fund members, pursuant to the fund's bylaws.

13

It can therefore be noted that, except where the insurer guarantees a minimum rate of return, it makes a commitment only to use its best efforts, just as in the case of self-administered pension funds.

This shows how close a group pension fund is to the notion of a pension fund. The major difference is that group pension funds are offered by insurance companies.

It should be noted, in addition, that insurance companies are in a position to offer a choice of two separate methods, one where the assets are considered by the insurance company to be part of its own technical provisions and are managed as such, the other where they are managed on behalf of a third party which actually owns a self-administered pension fund, the role of the insurance company being merely to perform financial management and actuarial duties on the fund's behalf.

In that instance, technical provisions are the property of the pension fund rather than of the insurance company, with all the legal, tax and other differences which that implies.

Section 5. Regulations applicable to private pension funds

21. Various kinds of regulations can apply to private pension funds. They vary in accordance with the type of fund and its financing support. Control can be exercised by various bodies accountable to the government.

22. Tax regulations

Private pension funds, the second pillar, constitute a system of deferred income accompanied by tax breaks, tax usually being deferred like income. Quite logically, the first control is tax legislation, which lays down the rules regarding their operation and the limitations to tax reliefs.

This legislation lays down the following:

tax deductibility and reduction;

limitation of benefits or contributions

mode of benefits taxation

tax status of financing supports

taxation of interest

inheritance taxation on benefits in case of death

23. Technical regulations

These consist primarily of financial and actuarial methods designed to ensure that pension funds actually deliver pensions. They concern actuarial methods, the choice of technical definitions, interest rates and mortality tables. They may set minimum reserves and solvency rules over and above them;

24. Business regulations

These rules, which are often coupled with tax or technical regulations, lay down minimum requirements regarding the soundness of supplementary pension schemes, i.e.

14

whether or not plans are compulsory at national, sectoral and firm level;

possibility, or lack thereof, of discriminating between categories;

vesting and portability;

solvency margin and insurance against insolvency;

disclosure to members.

25. Accounting regulations

Technical and business regulations are designed to ensure that supplementary pension schemes pay out pensions to existing or future beneficiaries. For the benefit of shareholders of companies that had set up private pension funds, and more broadly of their creditors and the outside financial world, it was necessary to improve the clarity of financial statements of companies with regard to pension liabilities. Accounting standards, usually drawn up by national associations of statutory auditors, have therefore laid down (either privately or publicly) a set of fairly precise rules regarding:

disclosure in annual financial statements or notes thereto of financial shortfalls or surpluses (FAS 87 and more recently IAS 19);

other accounting standards (SSAP 24);

impact on the net worth of companies in the event of mergers or spin-offs.

With the growing globalisation of economies, these rules are beginning to be applied in an increasingly uniform fashion in large companies.

Section 6. The role of financial institutions

26. It is fairly safe to say that the second and third pillars would never have attained their present level of development without the wide range of services proposed by financial, insurance and banking institutions.

The services sector in the broadest sense of the term has likewise been involved in the growth of the first and second pillars. Actuaries, accountants, consultants, brokers, lawyers and auditors, to mention only some, have facilitated the application of the various regulations listed in section 5 of this chapter.

But obviously the biggest contribution of the services sector to the financing of pensions has been the financial management of the very large technical provisions accumulated in the second-pillar schemes, and to a lesser degree in the third pillar.

In the case of the second pillar, particularly private pension funds, it is important to examine more closely the structure of relationships between the funds and the financial managers. When a fund is run by a bank or financial institution, it usually remains the owner of the assets covering its liabilities.

In contrast, when a fund is run by an insurer, it usually constitutes a claim on the insurer, who becomes the owner of the assets covering the liabilities. In consequence, the management of such funds may be less transparent, and in particular it may be difficult to determine the allocation of profits and losses. However, in the most advanced countries the arrangements proposed by bankers and insurers are increasingly similar.

15

This difference can also be expressed as follows: “...with few exceptions, institutions for retirement provision are essentially non-profit bodies, while banks and insurance companies charge for their financial services. In fact, the latter provide financial services, while pension funds buy financial services, a difference that is important to keep in mind”. [2]

In one form or another, the financial services sector plays an important role in the functioning of private pension funds, which in their turn contribute to the prosperity of firms of all kinds in the financial sector.

In this connection, mention may be made of the high administrative costs of defined-benefit schemes in the United States, which according to the US Department of Labor amounted in 1985 to 8.3 per cent of contributions to multi-employer schemes and to 4 per cent of the contributions to single employer schemes [19].

Chapter II – Private pension funds in the countries studied

Section 1. Structural options for the first pillar

27. It is not possible to grasp the various forms that private pension funds have taken in the countries studied without first looking at the structural particularities of the respective first pillars. Before studying private pension funds, it is therefore important to examine the options for basic schemes.

These schemes must first be defined. They include all Social Security systems, along with those mandatory supplementary schemes whose funding is almost exclusively on a pay-as-you-go basis. From this standpoint they encompass all systems that are based on national or socio-occupational solidarity, with funded plans excluded and subsumed under the second pillar.

It is necessary to distinguish between schemes that provide for flat-rate pensions and those in which benefits are wage-related, generally up to a certain earnings ceiling. Table 1 (“Typology of First-Pillar Schemes”) describes the actual situation in the 22 countries studied and shows that there are nine countries (40 per cent) with flat-rate pensions and 13 (60 per cent) in which first-pillar pensions are wage-related.

28. Flat-rate basic pension schemes

By all logic, flat-rate pension systems ought to be financed by taxes, but Table 1 shows that a majority of them (five cases out of nine) are funded by contributions that are proportional to wages. However, since taxes are themselves determined with respect to earnings, the two systems have more in common than might appear, except that contributions are generally tax deductible whereas taxes usually are not.

It must also be noted that, with the exception of Australia, no country applies means-testing to the attribution of flat-rate state pensions. Furthermore, as long as there has been a cessation of employment, the pension is generally provided to anyone who has resided in the country in question, irrespective of the type of work previously engaged in, whether dependent employment, self-employment or civil service.

29. Wage-related basic pension schemes

Wage-related first-pillar pension schemes are to be found in 13 of the 22 countries studied. Obviously, contributions in these countries are themselves related to wages.

16

Wage ceilings generally apply in computing benefits and contributions alike, except in Portugal, where there are no ceilings. Ceilings on contributions (and especially those paid by employers) are in some cases higher than the ones used in computing pensions (reflecting the solidarity aspect).

17

Table 1 – Typology of First-Pillar SchemesFlat-rate state pensions (9 out of 22 countries)

Australia Financed by the national budget and granted only after means-testing in respect of total income and personal wealth. As a result, managers are generally not eligible, especially if they receive supplementary pension benefits.

Canada Taxed-financed OAS + CPP/QPP benefits financed by personal and employer contributions on earnings. No means-testing.

Denmark Financed by the national budget. No means-testing.

Finland Same as above.

Ireland Personal and employer contributions up to a capped level of earnings. No means-testing.

Japan Flat-rate personal and employer contributions. No means-testing.

Netherlands Financed by worker contributions, proportional to income up to a certain ceiling. No means-testing.

New Zealand Financed by the national budget without means-testing.

United Kingdom Financed by worker and employer contributions up to a certain ceiling. No means-testing.

Wage-related basic pensions (13 out of 22 countries)All of the other countries, with a number of particularities, inter alia:

Switzerland Depending on income level, from 100 to 33 per cent at the highest wages.

United States Same as above, ranging from 72 to 24 per cent.

18

In Belgium in particular, there is no longer any ceiling on contributions, whether personal or employer-paid, whereas the basic pensions of private-sector workers are capped at a certain level of earnings.

Wage-related first-pillar pensions are generally calculated on the basis of capped adjusted average career earnings, with a certain guaranteed minimum. In some countries, however, they are linked to average earnings near retirement age—for example, the last eight years in Spain and the best ten out of the past 15 years in Portugal.

In some countries, including the United States and to a lesser extent Switzerland, the percentage of past wages to be paid out in pensions decreases with the level of earnings—another type of measure that enhances solidarity and seeks to limit current and future liabilities.

Lastly, it should be noted that wage-related basic pensions can sometimes incorporate a flat-rate amount (as in Luxembourg).

Apart from limitations on receiving pensions and earned income at the same time, all of these wage-related pensions are awarded without any means-testing.

30. Mandatory supplementary schemes

Alongside many basic systems there are mandatory supplementary schemes which can also be considered part of the first pillar because they are, in fact, mandatory and therefore based on solidarity.

Of the nine countries with flat-rate state pensions, five also have mandatory supplementary schemes. Except in Denmark and Finland, it is possible to contract out of these schemes, providing that the business in question has a supplementary retirement plan that meets a number of minimum conditions. In Japan in particular, such corporate plans must provide benefits that are at least 30 per cent greater than those of the mandatory supplementary Employee Pension Insurance (EPI) scheme.

Of the 13 countries with wage-related basic pensions, four have mandatory complementary schemes, which in turn are related to wages. In only one country—Greece—is it possible to contract out.

Lastly, in France and Switzerland the mandatory complementary schemes involve defined contributions (money purchase) and not defined benefits.

In Section 2, and Table 2 in particular, we shall be coming back to supplementary schemes, including those that are mandatory.

19

Table 2. Typology of Supplementary Schemes in the Countries Studied

SOCIAL SECURITY(basic scheme)

provides aCOMPLEMENTARY SCHEMES ARE

MANDATORY except for CONTRACTING-OUTif there is a scheme that is

VOLUNTARY

FLAT-RATE STATE PENSION

DENMARK (ATP): flat-rate

FINLAND: wage-related

AUSTRALIA (SGB): wage-related

JAPAN (EPI) : same as above

UK (SERPS) : same as above

CANADADENMARKIRELANDNEW ZEALANDNETHERLANDS

WAGE-RELATED BASIC PENSION

FRANCE (ARRCO + AGIRC)

KOREA

SWEDEN (ATP)

SWITZERLAND (BVG)

All wage-related

GREECE (TEAM) : wage-related GERMANYAUSTRIABELGIUMSPAINUNITED STATESFRANCE (rare)ITALY (rare)LUXEMBOURGPORTUGAL (rare)KOREASWEDENSWITZERLAND

20

31. Table 2 (“Typology of Supplementary Schemes in the Countries Studied”) shows the position of mandatory supplementary schemes in nine of the 22 countries studied.

In the four cases in which contracting-out is possible, the mandatory complementary schemes in a sense play a minimum back-up role for employers who fail to voluntarily set up adequate supplementary pension plans. These countries are Australia (Superannuation Guarantee Bill, or SGB), Greece (TEAM), Japan (EPI) and the United Kingdom (SERPS). All of these systems are wage-related.

In the five countries in which mandatory complementary schemes do not permit contracting-out, supplementary pensions are wage-related, except in Denmark, where there are flat-rate benefits (ATP).

Table 2 summarises first- and second-pillar schemes in the 22 countries studied.

32. Wage brackets covered by basic schemes - Parameter B1

It is interesting to determine a number of parameters for assessing the importance of the other two pillars in relation to the basic schemes.

The first of these parameters is B1, the respective compensation bracket covered by each country’s basic system. We have identified five possible variants:

1. Countries in which the basic scheme is wage-related and applies a more or less standard percentage, up to a given ceiling. In this case, B1 is equal to this ceiling [non-managers (INPS) in the case of Italy].

2. Countries in which the basic scheme provides a flat-rate pension. In order to compare these schemes with those of countries in which the basic scheme is wage-related, we shall assume that this flat-rate pension covers 50 per cent of a basic wage. B1 will therefore be equal to double the flat-rate pension.

3. Countries (Switzerland and the United States) in which the basic pension is wage-related but the applicable percentage declines sharply as earnings rise. We have set B1 equal to the wage level for which the basic scheme covers 50 per cent.

4. Countries having a mandatory supplementary scheme:

If it is possible to contract out, we have disregarded the supplementary scheme, and B1 is equal to the basic scheme ceiling calculated as in (1) or (2).

Otherwise, B1 is equal to the ceiling of the supplementary scheme, also calculated as in (1) or (2), i.e. equal to the ceiling of the ARRCO scheme for non-managers.

5. Countries (Finland and Portugal) placing no ceiling on first-pillar pension benefits. Here we have set B1 equal to “infinity”.

The parameter B1 provides a measure of the compensation bracket covered by first-pillar pensions (see also Note 1 of the Annex).

33. Average earnings (AE)

21

The second parameter is AE, which is the average gross earnings of manufacturing workers. Commonly used in international comparisons, and by the OECD in particular, it can serve to measure the wage level of each country.

GNP or per capita GDP, which are more readily available data, have the drawback of being affected by non-wage income, which we feel ought not to be taken into account in a study focusing essentially on private pension funds that are related to wage income alone.

34. A significant parameter: B1/AE

The third and final parameter is B1/AE, i.e. the ratio between the basic scheme “ceiling” (B1), as defined under Item 36, and average earnings, AE, as defined under Item 37. This parameter denotes the portion of average earnings that is covered by each country’s basic scheme.

Table 3 lists the values of B1, AE and B1/AE for each of the countries studied.

Later on, we shall see the major significance of B1/AE—a parameter that shows how important the second and third pillars can be to the funding of pensions in these countries.

22

Table 3 Portion of Earnings Covered by the First Pillar

Country AE 95 B1 95 B1/AE

Local currency

(A) (B) (C) (D)

Germany 55.625 93.600 1.68

Australia 34.800 0 0

Austria 293.010 529.200 1.81

Belgium 890.138 1.335.317 1.51

Canada 33.500 26.400 0.79

Korea n.a. 7.438.584 n.a.

Denmark 231.333 158.760 0.69

Spain 2.061.586 4.346.280 2.11

United States 27.000 28.800 1.07

Finland 126.782 unlimited unlimited

France 119.191 467.820 3.93

Greece 2.584.617 4.542.000 1.76

Ireland 14.107 7.384 0.52

Italy 32.349.267 109,400,000 3.38

Japan 4.150.000 1.560.000 0.38

Luxembourg 1.037.441 2.372.900 2.29

New Zealand 33.300 18.467 0.55

Netherlands 57.546 36.312 0.63

Portugal 1.284.833 unlimited unlimited

United Kingdom 15.178 6.120 0.4

Sweden 190.596 270.000 1.42

Switzerland 60.500 34.920 0.58Notes: The figures in this table for the variables AE and B1 are based on the year 1995. The figures for 1997 have

been examined and found to show no significant variation relative to those of 1995. Hence, the level of the parameter B1 / AE shown in this table will be the one used in this study.

Source: (B): OECD, The tax/benefit position of production workers 1991-94, Paris, 1995.(C): Various sources listed in the bibliography.

23

Section 2. Interaction between the three pillars

35. Various issues dealt with in the previous sections deserve a closer look in order to carry out a detailed examination of the second pillar.

In particular, we should examine in more detail the typology of pension arrangement, paying special attention to the multiple situations of “hybridisation” that exist. In these cases, a strict separation of concepts can sometimes be an arduous task.

The procedure we will follow is to start from a synthesis table of the typology of pension arrangements and of the different concepts relating to it.

Table 4 gives a broad outline of types of pension scheme together with the concepts that may be associated with them. The vertical dividers indicate the current theoretical situation and the lower case letters refer to particular schemes operating in the interstices between the zones thus defined (see text). The arrows indicate the dominant direction of change.

In the table:

6. DB = defined benefit, DC = defined contributions

7. The obligations are those of contributors or policyholders, not those of the organisations responsible for paying benefits. For the contributor, the obligation of results therefore implies paying the amounts necessary to obtain a given result. Best efforts implies merely paying the scheduled amount of the contribution or premium when the policy is taken out.

8. “Non-commercial” means the non-profit sector and “commercial” means the for-profit sector of the economy.

9. The decision-taker is the entity which chiefly decides how the pillar operates.

10. For information, the same individual can be a member of all categories.

24

Table 4 Typology of pension schemes

PILLARS 1 <==

(a)

2 <==(b)

3

SCHEMES (1) DB <=== (c) DC

OBLIGATION (2) RESULT <=== (c) EFFORTS

SUPPORT (3) NON-COMMERCIAL <=== (d) COMMERCIAL

DECISION-TAKER (4) Authority <=== Employer <== Individual

WHO PAYS? (5) Taxpayer / shareholder / individual

As regards obligations (2), obligation of results means here that, unless laws, regulations or contracts are changed, the person responsible for paying the contributions or premiums must accept any adjustment to the contributions or premiums such as to enable the stipulated legal, regulatory or contractual result to be achieved. If that is not the case, we assume that the obligation is one of best efforts.

The line (3) SUPPORT intends to make a distinction between funding supports, i.e. from public sector and from insurance companies and financial institutions, established in commercial form. The Mutuals and Co-operatives which offer their products as insurance or financial markets are considered as being part of “commercial sector”. This distinction could also have been made between market/non market.

It can also be seen in the table that all the arrows indicate a move from right to left. As we will explain later, this shift represents an increase in individual choice, that is, a heightened responsibility of the individual and a shrinking role for the state.

In order to complete the picture, the last two lines of Table 4 are

Who decides?

and Who pays?

The preceding paragraphs have revealed a general trend towards deregulation and greater freedom of choice. It is interesting to see that the same movement is taking place at the decision-making level, with individuals replacing companies, which are themselves assuming obligations that used to lie with public authorities. Thus, Table 4 shows a broad movement from right to left, illustrating this trend.

In connection with the question Who pays?, we could raise the problem of the effect of these pension schemes on government budgets, referred to in broad terms as “tax expenditure”, but this goes beyond the

25

remit of the present report. We have included the question for information only, in order for our treatment of the subject to be as comprehensive as possible.

36. Hybridisation of pillars: substitution effects

The separation marked (a) in Table 4 is the separation between the first pillar, namely social security pensions, and the second pillar, namely supplementary pensions constituted through company, occupational or assimilated schemes.

On this point, it should be noted that some countries, such as Chile, have replaced earlier pay-as-you-go (PAYG) schemes (which existed until 1981 in Chile’s case) with a system of funded schemes based on individual accounts. Contributions have been paid to pension funds or insurance companies in free competition with each other under the supervision of the appropriate authorities. Contributions are paid entirely by the worker (10% for retirement pension and 2.5 - 3.75% for invalidity, death and management costs). It is a defined contribution scheme (DC).

The switch from PAYG to a funded scheme was made by attributing vouchers representing previously acquired rights to all workers who had contributed to schemes before 1981. On retirement, these vouchers will be added to the accumulated proceeds of contributions. The private fund management organisations in the Chilean scheme invest about 40% of their reserves in government securities, thus facilitating the government’s funding of the vouchers.

In the Chilean system, therefore, the first pillar disappears for the future and is absorbed not into the second pillar but into the third pillar, since affiliations are individual and the employer plays no part. This does not in principle prevent the development of a second pillar at company or occupational level (a contribution to a funded scheme equal to 10% of wages guarantees at most a pension of around 40% of wages, thus leaving the door open for supplementary pensions).

However, competition has caused fund managers to incur high management and marketing costs, since contributors under pressure from a highly active sales network change funds too often. The Chilean authorities have had to step in to limit the frequency of such changes so as to avoid a reduction in returns relative to gross premiums.

Nonetheless, the Chilean experiment has aroused considerable interest in other countries, notably Mexico, which has recently introduced a similar system, and various other Latin American and east European countries. The main advantage of the system lies in the creation of substantial reserves which can be invested in the economic development of these countries, stimulating growth.

The situation would be very different in more developed countries, where the additional contributions needed to constitute such supplementary reserves would doubtless lead to a net reduction in household assets and a simple switch from individual to collective savings.

As long as the government covers the vouchers as they mature, the Chilean system therefore represents a shift from the first pillar to the third pillar, albeit in the form of compulsory collective saving.

37. The effects of contracting out

In the United Kingdom it is possible to partially substitute the second pillar for the first pillar, a less radical and older reform than the Chilean experiment. A relatively small flat-rate national old-age pension has existed in the UK since 1948, financed from tax revenue. A second pension was added in 1961, funded by contributions from workers and employers and linked to wages within a defined bracket.

26

In order to take account of the importance of private pensions in the UK (in many cases dating back to the 19th century), employers were allowed to opt out of the scheme providing that they could prove that their pension scheme met certain minimum conditions. This method of partially replacing the first pillar with the second pillar is called “contracting out”.

The shift from the second pillar towards the first was consolidated by the Social Security Pensions Act of 1975, which maintained a relatively small flat-rate national basic pension (currently approx. £3,250 a year) alongside a pension linked (25%) to the portion of wages within a given bracket, a systems called SERPS (state earnings-related pension scheme). The possibility of contracting out was maintained and still exists. In this case, both worker and employer are exempted from a portion of their social security contributions, respectively 1.8% and 3% of wages in excess of £62 a week (i.e., approx. £3,250 a year).

It is interesting to note that the vast majority of large and even medium-sized firms have contracted out, for three main reasons:

11. some wonder whether the SERPS pension will be able to provide the promised 25%. The system was recently changed so that the pension would be calculated on the basis of a contributor’s entire working life and not just the last twenty years;

12. the 4.80% total saving on social security contributions can fund a pension equal to 25% of a worker’s average career wage;

13. private pension funds in the UK manage to extract extremely high returns, meaning that even the 4.80% contribution is unnecessary to fund contracting-out obligations.

In different forms, contracting out also exists in Australia, Japan and Greece, in all cases with the possibility of partially substituting the second pillar for the first.

In a nutshell, the rationale for contracting out runs as follows: some governments, perhaps rightly, wish to limit their excessively long-term commitments. As long as economic circumstances were favourable, the welfare state could promise ever bigger pensions without undesirable side effects. But as soon as these conditions (economic, demographic, etc.) start to deteriorate, the outlook becomes increasingly bleak. It is worth noting in passing that long-term projections in the UK have always been carried out by a government actuary, whereas during the “golden Sixties” in Belgium, for example, projections relating to state pensions were carried out with a horizon of only four to five years. For all these reasons, British governments have always been able to take a longer term view and hence rationally have encouraged contracting out.

The British reform system, therefore, favours the growth of second-pillar funded supplementary pensions while preserving the indispensable PAYG system and an element of solidarity in the basic pension.

A comparison of this method, based on a permanent combination of PAYG and funded schemes, with the Chilean method of gradually replacing PAYG with funded schemes would be of the greatest interest as regards

the long-term reliability of each method,

their macroeconomic results,

the resulting level of comprehensive coverage.

27

As mentioned earlier, a distinction should doubtless be drawn between countries according to their level of capital intensity because the two methods lead to different levels of reserves for pensions: to what extent are additional savings desirable before they begin to crowd out other existing forms of saving?

38. Second-pillar/third-pillar hybridisation

The separation marked (b) in Table 4 is the separation that exists or ought to exist between the second and third pillars, i.e., between collective company, occupational or assimilated pension schemes and individual saving or provident schemes with or without tax incentives.

However, there are many cases of hybridisation between the second and third pillars.

In the UK, for example, since 1986 contracting out - a shift from the first pillar to the second - has gone hand in hand with a shift from the second pillar to the third. The 1986 Social Security Act allowed salaried workers to opt for an Appropriate Personal Pension scheme (APP) instead of SERPS or the company pension scheme. Available statistics indicate that some 5 million workers have chosen APPs, almost all with insurance companies.

This situation is comparable to the situation in Chile. When, as a result of excessively liberal policy, individuals are allowed to choose the type of scheme into which they pay their contributions, numerous excesses are possible because of the information asymmetry between insurer and policyholder in a particularly complex field. APP contracts are currently a hot issue in the UK and the subject of many legal claims, since under the terms of the Finance Security Act insurance brokers are required to give their clients best advice and tell them how much commission they (the brokers) will receive on life insurance business. The rows that have erupted over personal pensions suggest that the experiment was far from being a complete success.

There is also a trend in the United States towards partial substitution of the second pillar for thethird, though in this case the operation has been largely successful. Employees taking out so-called “401(k) plans” ask their employers to withhold a certain amount from their salaries in order to constitute a supplementary pension. The employer may also contribute to these individual schemes. Both employee and employer contributions to 401(k) plans are tax-deductible within certain income limits.

Their flexibility has made them highly popular, causing a shift from the second pillar to the third inasmuch as the plans, like APPs in the UK, are a matter of individual choice, although they are often partly funded by employers. The commercial excesses noted in the UK and Chile do not seem to have occurred in the US, doubtless because of the part played by employers in 401(k) plans.

In Belgium, and perhaps in other countries (though in order to be sure it would be necessary to carry out an in-depth study of the tax rules that apply), it is possible for a company to make individual pension commitments in favour of a limited number of executives or employees.

These commitments are generally covered by individual life insurance policies enabling the company to meet them at term. Premiums are paid by the company, though in return beneficiaries often accept a cut or smaller-than-otherwise rise in salary. This system is thus not without similarities to 401(k) plans in the US.

However, there is no direct link between the pension commitment and the insurance policy. This has a favourable tax effect, since the employer can deduct the amount of the premium and the beneficiary is taxed on the benefit only at term. As purely individual arrangements these schemes seem to fall into the third pillar, but in view of the employer’s role they in fact appear closer to the second.

28

Chapter III – Second-pillar schemes and control rules in the countries studied

Section 1. Statistics on funding provisions

39. Having defined the characteristics and limitations of the first pillar in the countries studied, we are now going to examine the available statistics by comparing them with the parameter B 1/AE presented above. We will subsequently analyse the resultant findings in order to highlight the role played by the insurance sector in the development of the second and third pillars.

Financially, and as explained under Item 9, both of these pillars involve the accumulation of contributions in the form of reserves which will ultimately generate the projected benefits. Contributions constitute a flow and the reserves a stock.

To gauge the macroeconomic significance of these flows it is necessary to ascertain the amount of contributions allocated to private pension funds and to the third pillar in each country. However, the only information available is fragmentary—total premiums for group life insurance in a number of member countries of the European Insurance Committee (CEA), as a percentage of GDP in each of the countries concerned [14]. We shall come back to this later.

With regard to stocks, it should be reiterated, as explained in Chapter I - Section 4, that provisions can take the form of book reserves (Item 16), self-administered pension funds (Item 18), group insurance (Item 19) or management of group pension funds (Item 20). Statistics on insured funds are available from the CEA [14], and we were able to obtain figures on self-administered funds from the European Federation of Pension Funds (EFPF). The report of European Commission experts [2] provided useful information on book reserves in the countries that allow them.

40. Reference level for funding provisions

This enabled us to prepare Table 5, which lists the amounts, in local currency, set aside as of year-end 1994 for each funding method—insurance, self-administered pension funds, and book reserves. The interpretation of these data and the estimation of the market share of the insurance sector should however remain cautious, since it is not obvious that group pension funds managed by insurers (Item 20) have always been included in insurance data in national statistics. By comparing this total with the GDP of each of the countries studied, we can express aggregate second-pillar provisions as a percentage of GDP in each of the countries for which figures are available.

In order to proceed further, it is necessary to be able to compare this figure with the total provision that would exist if all first- and second-pillar pensions were funded. An initial indication is the OECD’s calculation [20] of the theoretical level of that provision in 1990 if all public pension schemes in the G7 countries had been operated on a funded basis. Without going into too much actuarial detail, it can be stated that, based on a discount rate, net of inflation, of 4 per cent for 20 years and 3 per cent thereafter, this provision averages roughly 200 per cent of GDP.

Based on our own estimates and a discount rate of 3 per cent net of inflation, which we feel is more realistic, we estimate [21] that a scheme that provides each pensioner with a pension of about 50 per cent of their previous earnings should entail a funding provision of approximately 250 per cent of GDP. This figure is obviously open to question, but we believe it makes little difference, the sole intention being to provide a reference for estimating the proportion of funding in overall pension financing and thus to be able to make comparisons across the various countries studied.

29

41. Retirement allowance schemes

Some countries have allowance schemes which provide for (sometimes substantial) capital payouts when people stop working, e.g. when they retire. Such allowances can amount to as much as one month’s pay for each year of service with a given enterprise. These allowances are not generally considered part of the second pillar and, at most, are provided for as liabilities on corporate balance sheets and are not included in Table 5.

42. Respective proportions of funding and pay-as-you-go in the reference level

Table 5 therefore assumes that aggregate reserves of a funded reference system require a total provision equal to 250 per cent of GDP. Accordingly, the funded proportion in each country is equal to the ratio of the total provision actually constituted, as a percentage of GDP, and 250 per cent. The difference between this figure and 100 per cent is therefore the estimated proportion of pensions that are disbursed on a pay-as-you-go basis.

It can be seen that the pay-as-you-go proportion always exceeds 50 per cent, and that the countries listed can be divided into three categories with regard to funding:

14. In Switzerland, the Netherlands and the United Kingdom, the proportion of funding ranges from 35 to 41 per cent with respect to the reference level. It should be noted that this proportion is on the rise compared to a similar study carried out some ten years ago.

15. In the United States, Sweden and Japan, the proportion of funding varies between 12 and 18 per cent with respect to the reference level.

16. In the other countries for which figures are available in Table 5, the proportion of funding with respect to the reference level is less than 10, and in some cases 5, per cent.

Table 5 Second-pillar provisions and proportion of funding vs PAYG

Country GDP 94 Actual provisions in billions of local currency units

Prov. in %

% Funded

% PAYG

Billions

local curr.

Ins. Funds Book reserve

Total GDP Funded / 250 %

Balance

(A) (B) (C) (D) (E) (F) (G) (H) (I)

Germany (92) 3075,6 88 95 250 433 14,1 5,6 94,4

Australia 443,4

Austria 2262,9 16,2

Belgium 7625,9 601,8 219,6 0 821,4 10,8 4,3 95,7

Canada 750,1

Korea 185700

Denmark 933,2 167,8

Spain 64616,8 456,8 1497,4 n.a. 1954,2 3,1 1,2 98,8

United States 6931,4 900 2255 0 3155 45,5 18,2 71,8

Finland 507,8 6,7 46,4 n.a. 53,1 10,5 4,2 95,8

France 7376,1 270

30

Greece 23196,3 23,6

Ireland 34,7

Italy 1641105,1 36483,9

Japan 479100 n.a. n.a. n.a. 152027 31,7 12,7 87,3

Luxembourg 468,6 1

New Zealand 84,2

Netherlands 608,4 126,5 499 0 626,5 102,8 41,1 58,9

Portugal 13755 90,7 892 n.a. 982,7 7,1 2,9 97,1

United Kingdom 666,2 120(e) 451,8 0 578,8 86,9 34,8 65,2

Sweden 1516,9 224,4 374,6 n.a. 599 39,5 15,8 84,2

Switzerland 351,9 67,5 296 0 363,5 103,3 41,3 58,7n.a. data not availableSources : (B) : OECD 1996; (C) : GAP-FFSA, Les marchés de l’assurance vie en 1995

(D) : EFRP 1997; (G) : Total second-pillar provision; (H) : Proportion of funded pensions in relation to a reference system wherein pensions are equal to 50 per cent of wages, and for which the necessary provision would be approximately 250 per cent of GDP. H therefore equals G/250.

Group (1) includes (see Tables 1 and 2) two countries with flat-rate state pensions—the Netherlands and the United Kingdom—and one with a wage-related basic pension—Switzerland, although Swiss pensions are set at a very low level and the percentage declines sharply as eligible earnings rise. It is therefore logical that in these countries private pension funds account for a particularly large proportion of the total. It should be noted that Switzerland has instituted a funded mandatory second-pillar complementary scheme, which is included in our figures, and that the United Kingdom also has a mandatory complementary scheme (SERPS), but one from which businesses can contract out.

43. The impact of the B1/AE parameter on the proportion of funding

Looking also at the make-up of groups (2) and (3) shows that it is not the typology of the first pillar that determines the proportion of pension financing that is funded (% CAP). We shall now see that the determining parameter is B1/AE, i.e. the proportion of earnings to be covered by the basic scheme, as defined under Item 34. The higher the ratio of B1 to AE, the lower the proportion of pensions that are funded.

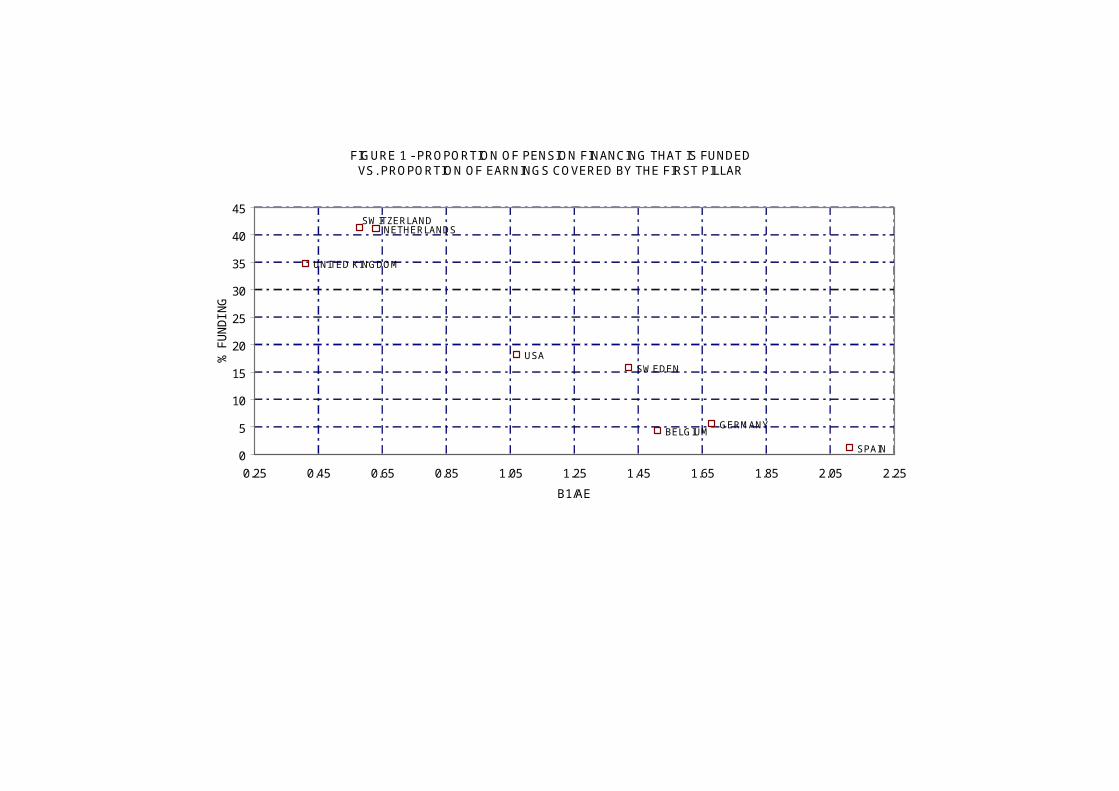

Table 6 and Figure 1 derived from it depict this situation in countries for which both CAP and B1/AE are known.

Table 6 Values of B1/AE and CAPin countries for which these figures can be estimated

Country B1/AE % CAPBelgium 1.51 4.3Germany 1.68 5.6Netherlands 0.63 41.1Spain 2.11 1.2Sweden 1.42 15.8United kingdom 0.41 34.8United states 1.07 18.2

31

Table 6 draws upon data from Tables 3 and 5 and has been used to plot Figure 1, which does in fact show a strong negative correlation between CAP and B1/AE.

Regression analysis yields the following equation for the straight line passing closest to the points:CAP = 50.95 – 26.07 * B1/AE.

(standard error of estimate Y5.96, R2 0.890, standard error of coefficient – 3.73)

Figure 1 shows that the Netherlands is overfunded but that Belgium is underfunded, which explains the large standard deviations of the linear regression.

Other conclusions can be drawn: for example, Belgium, as compared to Germany, also has a lower B1/AE but also a lower CAP, which can be explained by the fact that in Belgium over 90 per cent of people opt for the capital sum on retirement, whereas in Germany they are obliged to take an annuity.

Section 2. The relative proportion of insurers in private pension schemes

44. As we said in item 40, it is often difficult to determine precisely the share of the insurance sector in the flows and stocks of the second and third pillars.

From the statistics available at the CEA [14], the GAP and in the review SIGMA [25][15], it is possible to ascertain total life insurance premiums, as a percentage of GDP, in each of the countries concerned, in some cases making a distinction between individual and group policies.

It is interesting to note that in France since 1995, the statistics have lumped group insurance together with voluntary subscriptions to individual life insurance.

In Table 7, we have listed 1995 data for total, group and individual life insurance premiums, along with the value of B1/AE in each of the countries studied when these data were available. Table 7 also gives a more general picture of the role of insurers in various countries. It also highlights the relationship between the various macroeconomic aggregates, as described below.

The impact of B1/AE on total life insurance premiums

Table 7 can be used to plot Figure 2, which depicts the negative correlation between B1/AE and total paid-in life insurance premiums in each of the countries studied, and to perform regression analysis, subject to the reservations below.

Figure 2 shows clearly that some countries do, in fact, lie outside a possible regression line. There are a number of reasons for this, including:

bancassurance in France (where total premiums are relatively higher);

international life insurance operations in the United Kingdom (higher);

the very under-developed state of the life insurance industry, due to a history of high inflation, in Greece and Italy (lower).

32

Table 7 Life Insurance Premiums as a % of GDP vs. B1/AE

Country A1/AE Total Life Insurance 95/ %

Gdp

Group Life Insurance 95/ % Gdp

Individual Life Insurance