© The Pension Protection Fund An Actuary’s Role Kulin Patel and Martin Hooper Higham Group 29...

19

© The Pension Protection Fund An Actuary’s Role Kulin Patel and Martin Hooper Higham Group 29 November 2005

-

date post

19-Dec-2015 -

Category

Documents

-

view

215 -

download

1

Transcript of © The Pension Protection Fund An Actuary’s Role Kulin Patel and Martin Hooper Higham Group 29...

©

The Pension Protection FundAn Actuary’s RoleKulin Patel and Martin HooperHigham Group

29 November 2005

©

Agenda

Background to Occupational Pensions in UKSecurity of Occupational PensionsThe Pension Protection FundWhere actuarial students and actuaries fit in

©

Occupational Pensions in UK

Retirement Savings in the UK Based on a 3 tier system Turner report

Employers have set up pension schemes Tax incentives on contributions Part of Reward and HR Strategy

Incentives to interact with State Pensions

©

Occupational Pensions in UK

Employer schemes Defined Benefit Defined Contribution Hybrid

Defined Benefit Schemes Many rules and regulations Employers must fund for the future

promises

©

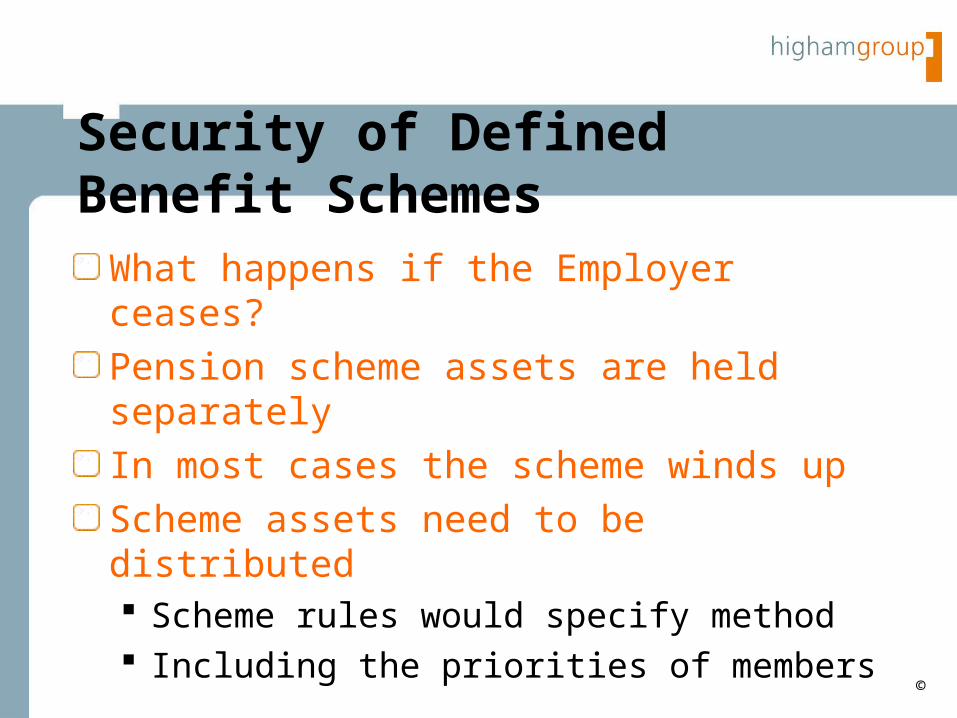

Security of Defined Benefit Schemes

What happens if the Employer ceases?Pension scheme assets are held separatelyIn most cases the scheme winds upScheme assets need to be distributed Scheme rules would specify method Including the priorities of members

©

Security of Defined Benefit Schemes

What happens if the scheme has a shortfall?Benefits have to be reduced when assets distributedThere was no legislation covering this scenarioPensions Act 1995 (effective from 6 April 1997) changed this

©

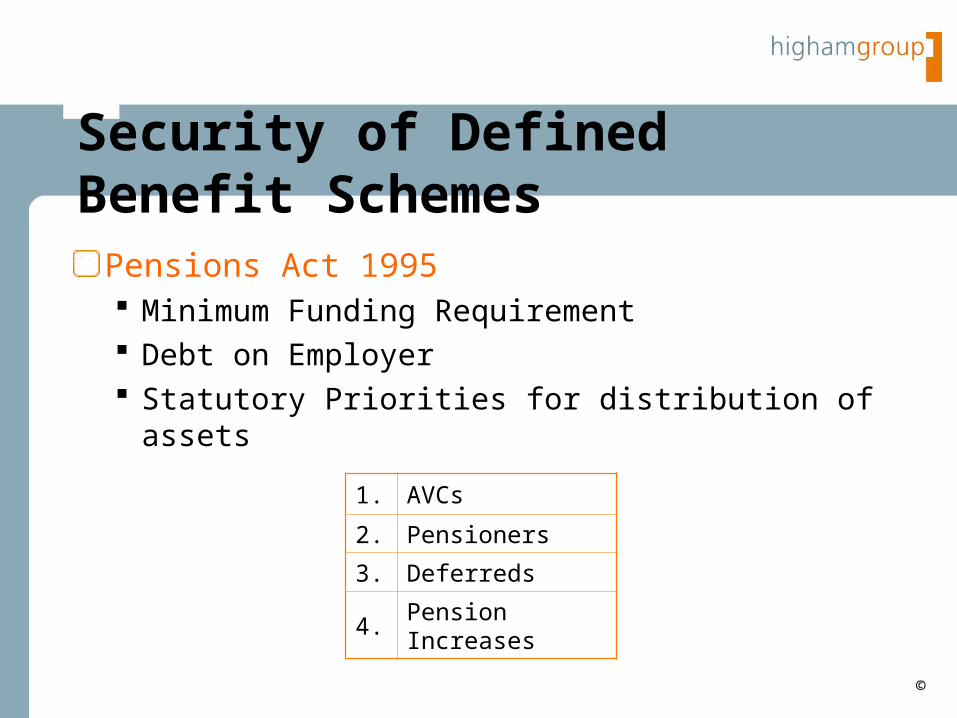

Security of Defined Benefit Schemes

Pensions Act 1995 Minimum Funding Requirement Debt on Employer Statutory Priorities for distribution of assets

1. AVCs

2. Pensioners

3. Deferreds

4.Pension Increases

©

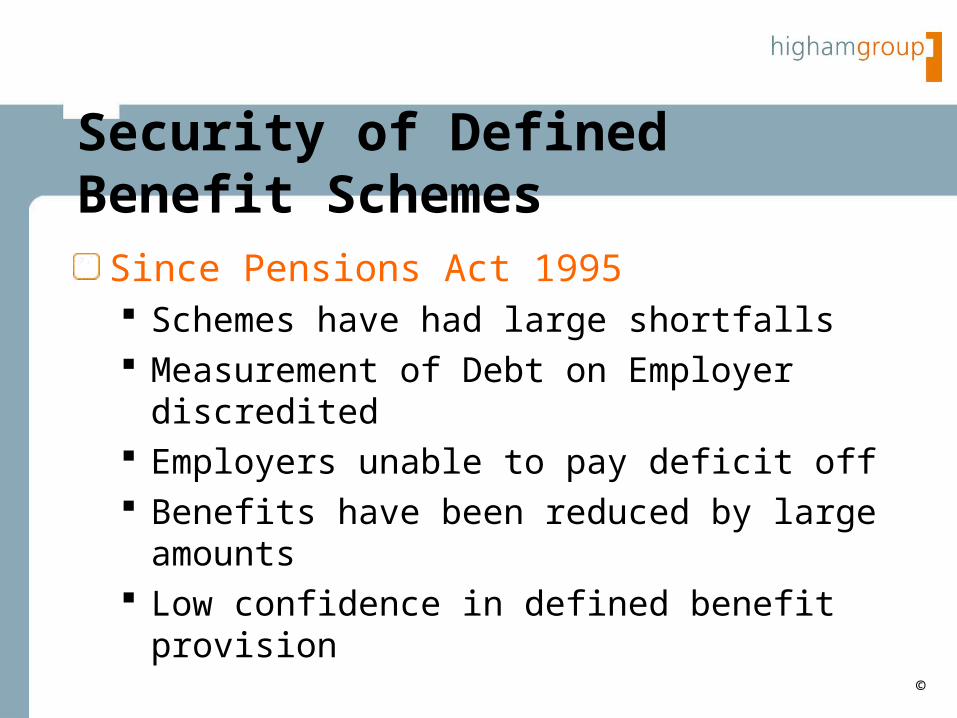

Security of Defined Benefit Schemes

Since Pensions Act 1995 Schemes have had large shortfalls Measurement of Debt on Employer

discredited Employers unable to pay deficit off Benefits have been reduced by large

amounts Low confidence in defined benefit provision

©

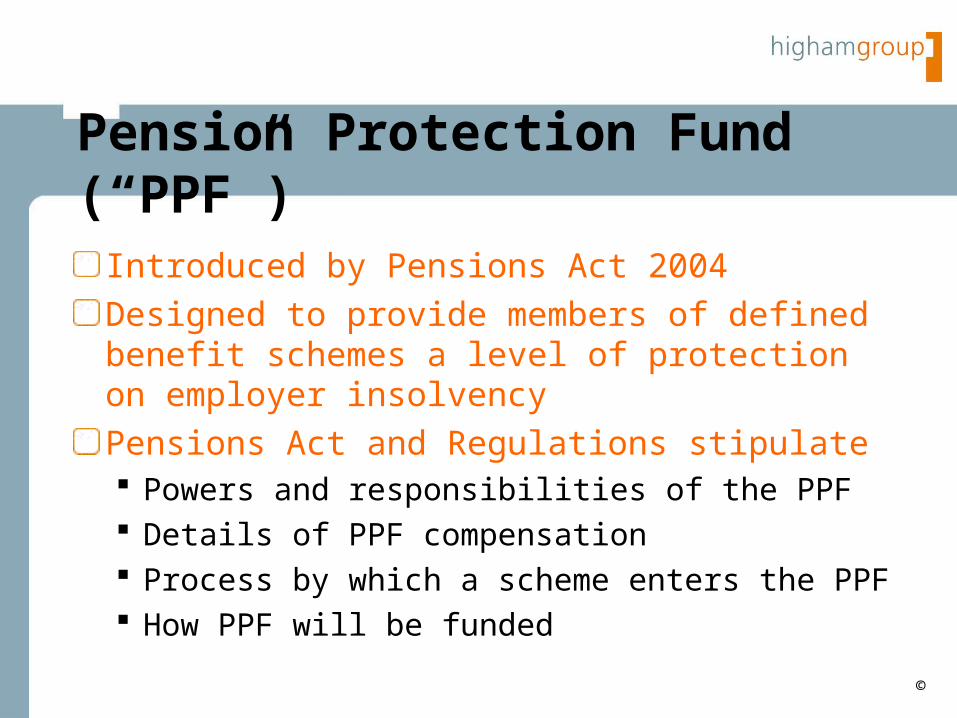

Pension Protection Fund (“PPF”)

Introduced by Pensions Act 2004Designed to provide members of defined benefit schemes a level of protection on employer insolvencyPensions Act and Regulations stipulate Powers and responsibilities of the PPF Details of PPF compensation Process by which a scheme enters the PPF How PPF will be funded

©

Pension Protection Fund

Assessment Period Compensation LevelsPPF Levies

©

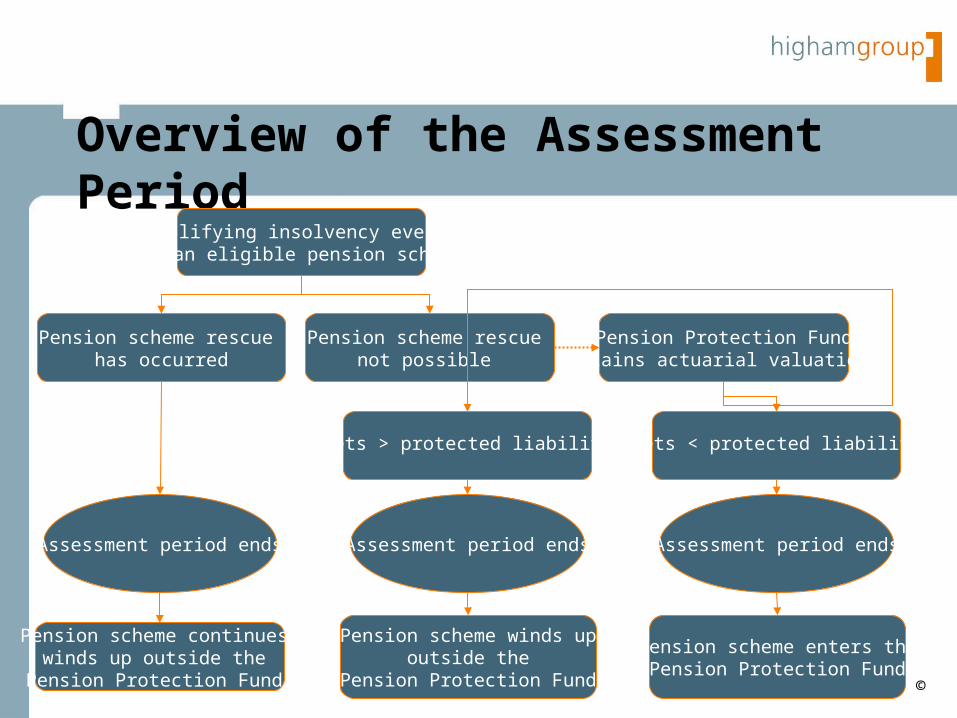

Overview of the Assessment Period

Qualifying insolvency event for an eligible pension scheme

Pension scheme continues/winds up outside the

Pension Protection Fund

Pension scheme rescue has occurred

Pension scheme rescue not possible

Assessment period ends

Pension Protection Fundobtains actuarial valuation

Assets > protected liabilities

Assessment period ends

Pension scheme winds upoutside the

Pension Protection Fund

Assets < protected liabilities

Assessment period ends

Pension scheme enters thePension Protection Fund

©

Compensation Levels

Over NPA at Insolvency Event

(IE)?

Yes

100% current

entitlement

No

Cap at £27,778 pa

Scale back to 90%

©

Compensation Levels (2)

Schedule 7Pensions in payment: Early retirements Ill-health SurvivorsPensions not in payment: Revalue to IE (existing regime) Revalue from IE at LPI (5%) Test against Cap, reduce to 90% (Unless over NPA at IE)

©

Compensation Levels (3)

Escalation in payment LPI (2.5%) on post 97 tranche only

Death benefits Provision for death benefits DAR: 50% post commutation DID: 50% re-valued to death

Other benefits Commutation: Up to 25% of pension Early / late retirement: Reduce to PPF level Ill health retirement: Not allowed

©

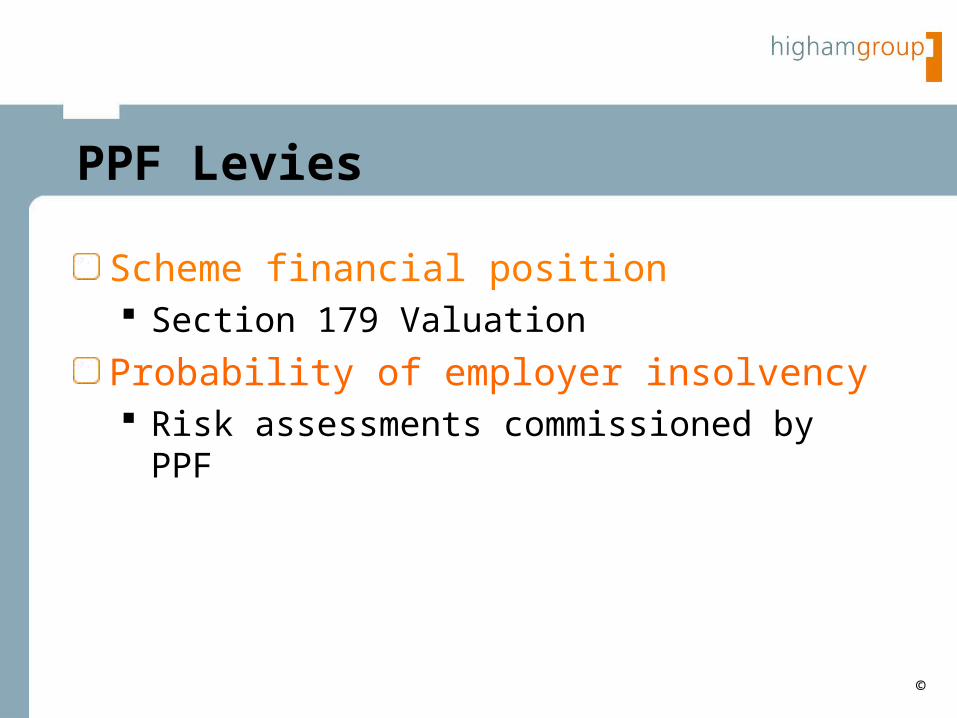

PPF Levies

PPF needs to raise capital (est. £300m p.a.)Levy on all eligible schemesFrom 2006/07 PPF to take risk based approach Scheme financial position on PPF basis Probability of employer insolvency Combined in a formulae to determine the

levy

©

PPF Levies

Scheme financial position Section 179 Valuation

Probability of employer insolvency Risk assessments commissioned by PPF

©

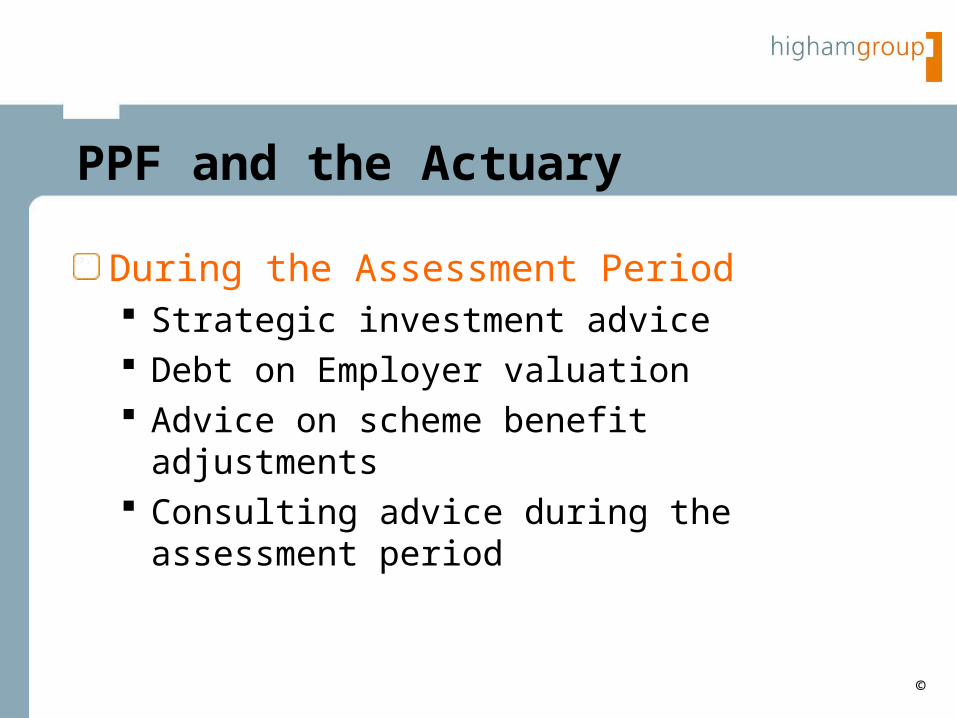

PPF and the Actuary

Section 179 Valuation Market value of assets Adjustments made to scheme benefits for

PPF compensation

Section 143 Valuation Market Value of assets plus future

recoveries from debt on employer Actual PPF benefits valued

©

PPF and the Actuary

During the Assessment Period Strategic investment advice Debt on Employer valuation Advice on scheme benefit adjustments Consulting advice during the assessment

period

©

Questions

?

![Research Matters Nick Higham School of Mathematics The …higham/talks/writing... · 2019. 4. 25. · Better: as shown by Vaughan and Williams [2]. Nick Higham How to Write Scientific](https://static.fdocuments.us/doc/165x107/608a984d889371198b4dbed9/research-matters-nick-higham-school-of-mathematics-the-highamtalkswriting.jpg)