! Return)and)Risk)Exposure)in)Pairs)Trading)

166

Copenhagen Business School MSc Advanced Economics and Finance (Cand. Oecon) Return and Risk Exposure in Pairs Trading C Evidence from the German Equity Market Abstract: We construct monetary neutral daily rebalanced pairs trading portfolios and test their profitability in the period 200392012. Our strategy yields abnormal risk9adjusted returns exceeding the market index. We also find further opportunities to improve the strategy by adopting risk management tools. Furthermore, we find evidence that pairs trading is a liquidity providing strategy and performs well in a volatile market environment. Keywords: Statistical arbitrage, pairs trading, market efficiency, market neutral, volatility, liquidity Author: Fabian Berg Author: Jørgen Bråten Nordby Handed in: August 2013 Number of pages (characters): 96 (217 575) Advisor: Lasse H. Pedersen, Professor at the Department of Finance, Centre of Financial Frictions (FRIC), Copenhagen Business School The John A. Paulson Professor of Finance and Alternative Investments at NYU Stern School of Business

Transcript of ! Return)and)Risk)Exposure)in)Pairs)Trading)

Copenhagen)Business)School)

MSc)Advanced)Economics)and)Finance)(Cand.)Oecon))

!

!

Return)and)Risk)Exposure)in)Pairs)Trading)

C)Evidence)from)the)German)Equity)Market)

!

!

Abstract:))

We#construct#monetary#neutral#daily#rebalanced#pairs#trading#portfolios#and#test#their#

profitability#in#the#period#200392012.#Our#strategy#yields#abnormal#risk9adjusted#returns#

exceeding#the#market#index.#We#also#find#further#opportunities#to#improve#the#strategy#by#

adopting#risk#management#tools.#Furthermore,#we#find#evidence#that#pairs#trading#is#a#liquidity#

providing#strategy#and#performs#well#in#a#volatile#market#environment.##

#

Keywords:))

Statistical#arbitrage,#pairs#trading,#market#efficiency,#market#neutral,#volatility,#liquidity#

!

)

)

Author:)Fabian)Berg) ) ) Author:)Jørgen)Bråten)Nordby)

)

)

Handed)in:)August)2013)

Number)of)pages)(characters):)96)(217)575))

)

)

Advisor:!Lasse)H.)Pedersen,##Professor#at#the#Department#of#Finance,#Centre#of#Financial#Frictions#(FRIC),#Copenhagen#Business#School#

The#John#A.#Paulson#Professor#of#Finance#and#Alternative#Investments#at#NYU#Stern#School#of#Business)

Executive)Summary)

!

This!thesis!finds!evidence!of!abnormal!returns!in!pairs!trading.!We!obtain!a!Sharpe!ratio!of!

0.47!compared!to!the!market’s!0.38!during!the!period!of!2003A2012.!In!addition,!we!find!a!

potential!improvement!to!the!strategy!by!adoption!of!risk!management!tools.!Our!returns!can!

be!partly!explained!by!lagged!relationships!between!our!returns!and!exposure!to!volatility!

and!liquidity!risk,!but!the!effects!are!too!small!to!offer!predictive!value!or!be!considered!main!

drivers!of!return!within!pairs!trading.!!

!

The!first!part!of!the!thesis!provides!a!thorough!discussion!of!the!theoretical!foundation!and!

most!relevant!risk!factors!for!pairs!trading.!Furthermore,!it!provides!an!explanation!of!how!a!

pairs!trading!strategy!is!typically!constructed!and!implemented!by!an!investment!

professional.!The!empirical!part!of!the!thesis!tests!the!profitability!of!a!daily!rebalanced!

monetary!neutral!pairs!trading!strategy!in!the!German!equity!market!between!2003A2012.!

Similar!to!recent!literature!!(Do!and!Faff!2012),!our!portfolios!do!not!yield!abnormal!returns!

for!a!6!months!trading!period.!We!also!construct!a!portfolio!with!a!12!months!trading!period!

to!give!pairs!longer!time!to!converge!and!take!into!account!the!worsened!arbitrage!risk!

proposed!by!Do!and!Faff!(2010).!Our!best!pairs!portfolio,!with!a!12!months!trading!period,!

yields!abnormal!riskAadjusted!returns!that!are!substantially!higher!than!the!market!index,!

even!after!conservative!estimates!of!transaction!costs!are!taken!into!account.!We!further!

suggest!that!the!profit!can!be!improved!by!implementing!risk!management!tools,!and!even!

though!our!approach!is!slightly!unrealistic,!it!shows!that!successful!implementation!can!

improve!the!performance!of!the!portfolio.!The!constructed!portfolio!has!a!significant!positive!

market!exposure,!and!this!is!in!conflict!with!the!common!perception!of!pairs!trading!as!a!

market!neutral!strategy.!The!remainder!of!the!thesis!tries!to!make!implications!about!the!

drivers!of!return.!Our!regressions!identify!volatility!and!funding!liquidity!risk!as!nonA

negligible!drivers!of!return!within!pairs!trading.!However,!the!dependency!on!these!variables!

seems!to!be!lagged!rather!than!dependent!on!values!in!the!current!market!environment.!The!

explanatory!power!is!too!small!to!consider!either!liquidity!or!volatility!main!drivers!of!return,!

so!just!as!previous!literature!we!are!unable!to!fully!explain!the!returns!from!pairs!trading.!!

!

!

) 2)

)Table)of)contents)

1.) INTRODUCTION!.................................................................................................................................................!4)2.) MARKET!NEUTRAL!STRATEGIES!AND!STATISTICAL!ARBITRAGE!....................................................!6)2.1.) WHAT)IS)MARKET)NEUTRALITY?).....................................................................................................................................)6)2.1.1.) Monetary#neutral#........................................................................................................................................................#7)2.1.2.) Beta#neutral#...................................................................................................................................................................#8)2.1.3.) Sector#neutral#...............................................................................................................................................................#9)

2.2.) MARKET)EFFICIENCY)AND)PROFITCMAKING)FOR)A)MARKET)NEUTRAL)STRATEGY).................................................)9)2.3.) LEVERAGE)IN)MARKET)NEUTRAL)STRATEGIES)..........................................................................................................)13)2.4.) THE)EQUITY)MARKET)NEUTRAL)STRATEGY)AS)A)HEDGE)IN)THE)INVESTMENT)PORTFOLIO)..............................)14)2.5.) PORTFOLIO)REBALANCING).............................................................................................................................................)14)2.6.) STATISTICAL)ARBITRAGE)...............................................................................................................................................)15)

3.) AN!INTRODUCTION!TO!PAIRS!TRADING!................................................................................................!17)3.1.) WHAT)IS)PAIRS)TRADING?)..............................................................................................................................................)18)3.2.) THE)ORIGIN)OF)PAIRS)TRADING)...................................................................................................................................)19)3.3.) PREVIOUS)LITERATURE)...................................................................................................................................................)19)3.3.1.) Most#Influential#academic#papers#....................................................................................................................#20)3.3.2.) Empirical#Findings#..................................................................................................................................................#21)

4.) SOURCES!OF!RISK!AND!RETURN!IN!PAIRS!TRADING!.........................................................................!23)4.1.) SOURCES)OF)RISK).............................................................................................................................................................)24)4.1.1.) Arbitrage#Risk#............................................................................................................................................................#24)4.1.2.) Liquidity#risk#..............................................................................................................................................................#26)4.1.3.) Short#squeeze#.............................................................................................................................................................#28)4.1.4.) Model#risk#....................................................................................................................................................................#29)

4.2.) SOURCES)OF)RETURN).......................................................................................................................................................)30)5.) CONSTRUCTING!A!PAIRS!TRADING!PORTFOLIO!.................................................................................!31)5.1.) SCREENING)OUR)DATA/STOCKS)....................................................................................................................................)32)5.1.1.) Market#capitalization#............................................................................................................................................#32)5.1.2.) Liquidity#in#prices#....................................................................................................................................................#33)5.1.3.) Short#sale#restrictions#and#short#sale#constraints#.....................................................................................#34)5.1.4.) Corporate#actions#....................................................................................................................................................#35)

5.2.) PAIR)FORMATION)............................................................................................................................................................)35)5.2.1.) Normalization#of#prices#.........................................................................................................................................#35)5.2.2.) The#formation#period#.............................................................................................................................................#38)5.2.3.) Identification#and#ranking#of#pairs#..................................................................................................................#39)

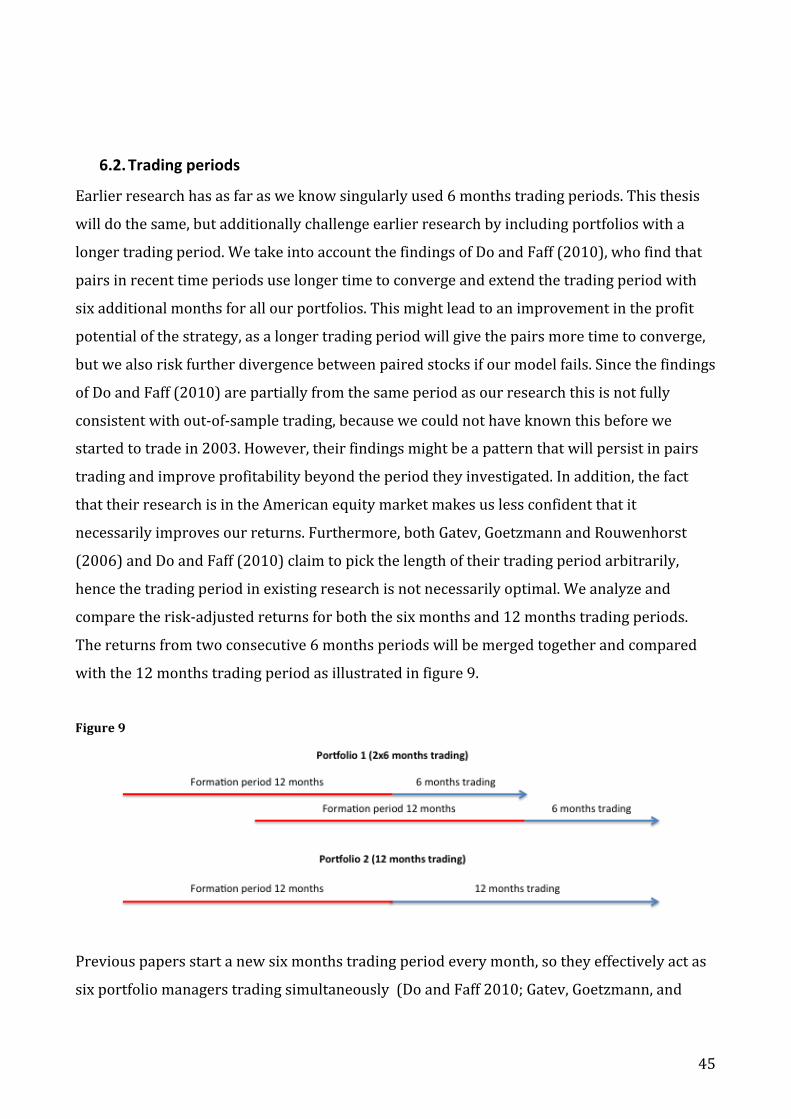

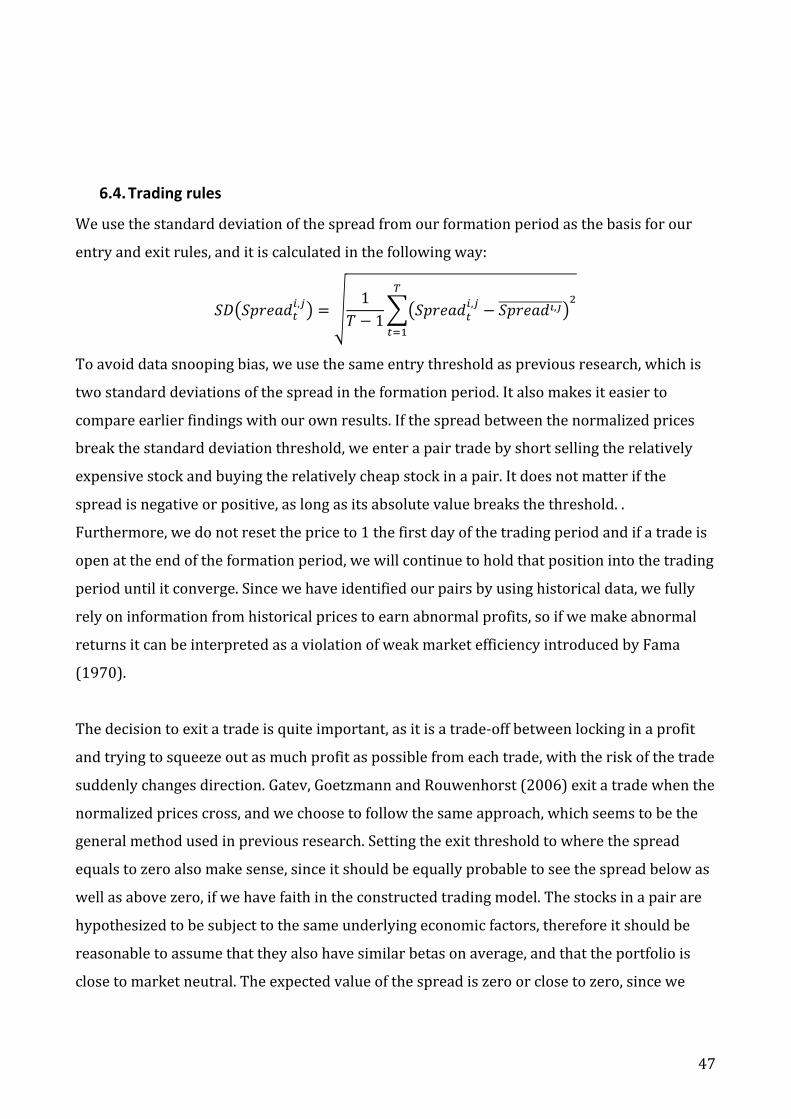

6.) TRADING!...........................................................................................................................................................!43)6.1.) INCSAMPLE)VERSUS)OUTCOFCSAMPLE)TRADING)..........................................................................................................)44)6.2.) TRADING)PERIODS)...........................................................................................................................................................)45)6.3.) POSITION)SIZING)..............................................................................................................................................................)46)6.4.) TRADING)RULES)...............................................................................................................................................................)47)6.5.) RETURN)CALCULATION)...................................................................................................................................................)49)

7.) EMPIRICAL!RESULTS!.....................................................................................................................................!50)7.1.) DATA)..................................................................................................................................................................................)51)7.2.) PRECTRANSACTION)COSTS)RETURNS)............................................................................................................................)52)7.3.) POSTCTRANSACTION)COSTS)RETURNS)..........................................................................................................................)58)

) 3)

7.4.) PAIRS)RANKED)81C100)..................................................................................................................................................)61)7.5.) INTRACINDUSTRY)PAIRS).................................................................................................................................................)63)7.6.) PAIRS)TRADING)IN)DIFFERENT)MARKET)ENVIRONMENTS)........................................................................................)65)7.7.) MANAGING)RISK)...............................................................................................................................................................)67)7.7.1.) Stop#loss#........................................................................................................................................................................#67)7.7.2.) Drawdown#control#..................................................................................................................................................#70)7.7.3.) Our#pairs#trading#portfolio#as#a#hedging#component#..............................................................................#72)

7.8.) REGRESSION)ANALYSIS)...................................................................................................................................................)74)7.8.1.) Explanatory#Variables#and#Hypotheses#.........................................................................................................#74)7.8.2.) Regression#results#....................................................................................................................................................#82)

8.) DISCUSSION!......................................................................................................................................................!94)9.) CONCLUSION!....................................................................................................................................................!98)REFERENCES!..........................................................................................................................................................!100)APPENDIX!...............................................................................................................................................................!103))) )

) 4)

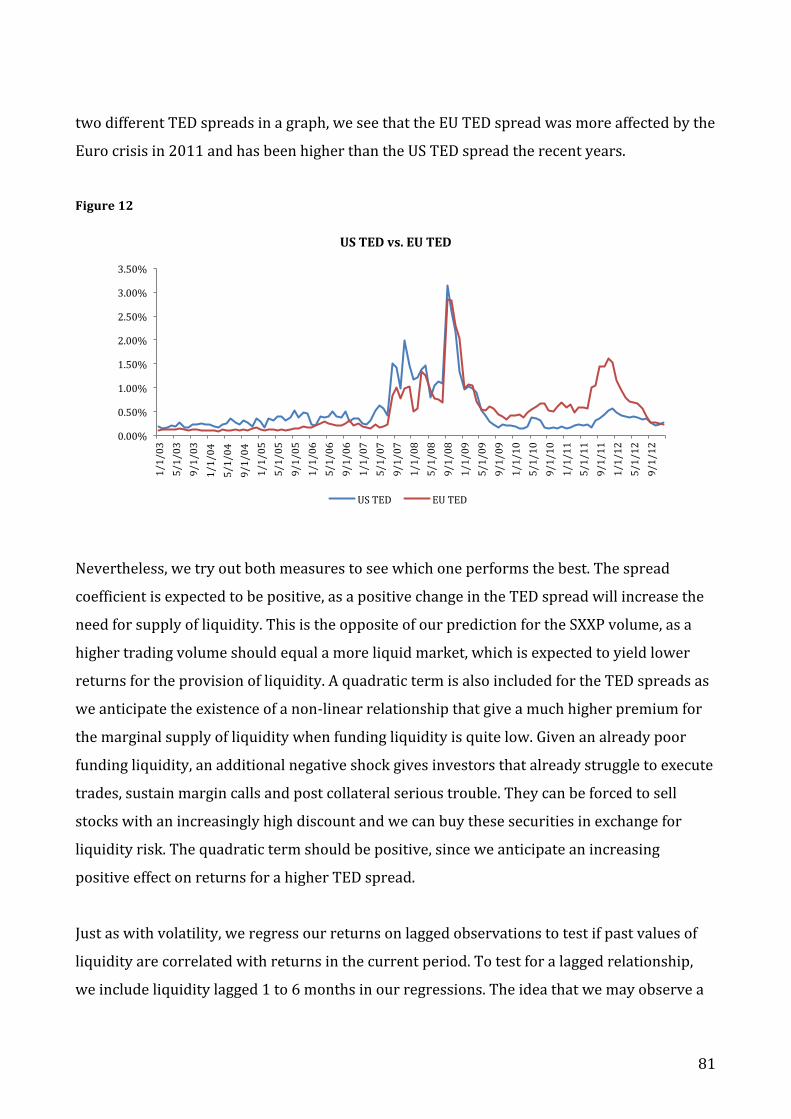

1. Introduction,Pairs)trading)is)a)wellCknown)trading)strategy)popularly)used)by)hedge)funds)and)proprietary)trading)desks,)and)it)has)proven)to)be)both)profitable)and)have)a)low)market)exposure.!Few)investment)strategies)are)able)to)beat)the)market)on)average,)but)pairs)trading)seems)to)be)one.)With)the)intense)competition)between)sophisticated)investors,)it)is)difficult)to)understand)how)such)a)simple)strategy)can)beat)the)market)over)longer)periods)of)time.)The)inability)of)rational)investors)to)arbitrage)away)the)abnormal)profit)from)this)strategy)seems)odd,)and)makes)pairs)trading)an)interesting)strategy)to)study)further.!Our)main)focus)is)to)investigate)if)pairs)trading)generates)abnormal)returns)in)the)period)from)2003)to)2012,)and)we)construct)a)pairs)trading)portfolio)with)stocks)listed)on)the)Frankfurt)Stock)Exchange.)Our)data)sample)includes)data)from)the)Euro)crisis,)which)has)(to)our)knowledge))not)yet)been)analyzed)in)academic)literature,)and)this)is)of)particular)interest,)since)past)research)finds)that)pairs)trading)has)performed)especially)well)during)financial)decline.)Furthermore,)we)examine)how)the)profitability)of)pairs)trading)changes)with)the)market)environment,)and)try)to)identify)the)main)drivers)of)the)returns.)The)questions)concerning)the)performance)of)pairs)trading)are)our)main)motivation)to)dig)even)further)into)the)subject)and)the)focus)of)our)thesis)is)summarized)by)the)following)research)question:)))”Does#pairs#trading#yield#abnormal#returns#and#what#are#the#main#drivers#of#profitability#within#

pairs#trading?”#

#

The)thesis)provides)a)thorough)discussion)of)the)underlying)concepts)and)assumptions)in)pairs)trading,)and)makes)the)reader)more)familiar)with)concepts)such)as)market)neutral)hedge)funds,)statistical)arbitrage)and)market)efficiency.)Moreover,)we)show)how)a)pairs)trading)portfolio)is)typically)constructed,)and)go)through)each)step)of)the)implementation)process)for)our)traded)portfolio.)We)construct)portfolios)with)different)pairCidentifying)techniques)and)the)best)performing)strategy)is)based)on)a)combination)of)the)sum)of)squared)differences)(SSD))and)zero)crossings)(ZC),)first)suggested)by)Do)and)Faff)(2010).)Our)portfolio)differs)from)those)discussed)in)previous)literature,)because)we)impose)a)strict)rebalancing)regime)on)the)portfolio,)and)it)is)definitely)a)plausible)explanation)for)why)some)of)our)results)differ)from)previous)research.)For)our)estimates)of)transaction)costs)and)chosen)trading)rules)

) 5)

we)find)excess)postCtransaction)costs)returns)between)2.20)%)and)5.66)%)per)annum,)dependent)on)the)length)of)the)trading)period)and)how)we)identify)our)pairs.)Both)the)annual)excess)return)and)Sharpe)ratio)is)improved)by)extending)the)trading)period)compared)to)previous)literature,)so)our)best)portfolio)has)a)trading)period)of)12)months.)The)best)portfolio)has)a)significantly)higher)Sharpe)ratio)than)the)market,)even)after)transaction)costs)is)taken)into)account.)The)pairs)in)our)base)portfolios)are)based)purely)on)statistical)relationships,)but)we)also)test)if)restricting)stocks)in)a)pair)to)the)same)industry)can)improve)the)profitability)of)the)investment)strategy.)Contrary,)to)previous)literature)(Gatev,)Goetzmann,)and)Rouwenhorst)2006;)Do)and)Faff)2010))we)find)no)evidence)that)homogeneity)among)pairs)is)performance)enhancing.)We)also)look)at)how)a)potential)adaption)of)risk)management)tools)could)be)done,)and)under)slightly)unrealistic)circumstances)we)find)a)small)improvement)in)the)riskCadjusted)returns)after)the)implementation)of)stop)loss.)Additionally,)we)look)at)a)combination)of)the)pairs)trading)and)the)market)index,)to)see)if)the)proposed)low)correlation)between)the)two)strategies)could)increase)the)performance)of)the)strategy)through)benefits)of)diversification.)Our)results)imply)that)investor)will)rather)hold)the)individual)pairs)trading)portfolio)than)a)combination)with)the)market)index.)))Moreover,)we)regress)our)returns)on)proposed)return)factors)to)try)to)identify)the)sources)of)return)for)our)traded)portfolio.)Our)analysis)shows)that)pairs)trading)profits)are)strongly)negatively)correlated)to)momentum,)which)is)largely)explained)by)the)trading)pattern)of)our)strategy.)Volatility)is)also)correlated)with)our)returns,)and)we)explain)the)relation)with)an)increased)crossing)frequency)between)the)paired)stocks)in)a)volatile)environment.)We)also)find)a)statistically)significant)relation)between)our)profits)and)funding)liquidity)in)the)market,)and)the)negative)coefficient)is)consistent)with)compensation)for)exposure)to)liquidity)risk)introduced)by)Acharya)and)Pedersen)(2005).)We)are)not)able)to)specifically)address)the)relationship)between)our)returns)and)the)three)sources)of)premium)discussed)by)Acharya)and)Pedersen,)but)consider)all)of)them)to)be)plausible)explanations)for)the)generation)of)excess)returns)in)pairs)trading.)Current)observations)of)volatility)and)liquidity)both)appear)insignificant)when)we)take)into)account)past)values)of)the)variables,)but)then)the)lagged)values)are)significant.)Therefore)the)relationships)seem)to)be)lagged)rather)than)dependent)on)the)values)in)the)current)market)environment.)In)addition,)we)find)a)similar)result)between)our)returns)and)the)implied)volatility)as)the)one)discovered)by)Nagel)(2012),)which)indicates)

) 6)

predictive)power)for)implied)volatility)on)returns)of)liquidity)providing)strategies.)The)explanatory)power)in)our)regressions,)still)imply)that)our)identified)relationships)only)explain)a)limited)part)of)the)pairs)trading)returns,)thus)there)seems)to)be)yet)to)be)discovered)factors)that)generate)return)for)the)pairs)trading)strategy.)The)thesis)is)structured)as)follows:)(2))Market)neutral)strategies)and)statistical)arbitrage,)(3))An)introduction)to)pairs)trading,)(4))Sources)of)risk)and)return)in)pairs)trading)(5))Constructing)a)pairs)trading)portfolio,)(6))Trading)the)portfolio,)(7))Empirical)results,)(8))Discussion)and)(9))Conclusion.))

2. Market,Neutral,Strategies,and,Statistical,Arbitrage,

The)hedge)fund)industry)is)mostly)known)for)highly)complex)and)nonCtransparent)trading)strategies)that)are)difficult)to)understand)for)less)sophisticated)investors.)Hedge)funds)can)provide)value)to)investors)by)exploiting)investment)opportunities)that)are)unavailable)to)most)individual)and)institutional)investors.)The)main)part)of)this)thesis,)will)try)to)shed)light)on)a)very)narrow)part)of)the)hedge)fund)universe,)which)is)a)market)neutral)strategy)called)pairs)trading.)Before)we)dive)further)into)pairs)trading,)we)will)give)a)brief)introduction)to)market)neutral)strategies)and)statistical)arbitrage,)as)these)concepts)are)the)cornerstones)pairs)trading)is)built)on.)))Figure!1!

)))

)Figure)1.)We)consider)statistical)arbitrage)a)subCstrategy)of)equity)market)neutral)strategies)and)pairs)trading)to)be)one)of)several)strategies)within)the)broader)statistical)arbitrage)category.)))

2.1. What,is,market,neutrality?,

The)most)common)perception)of)a)market)neutral)portfolio,)in)the)world)of)financial)securities,)is)an)investment)portfolio)that)is)independent)of)market)fluctuations.)The)common)interpretation)of)market)independency)is)that)the)portfolio)is)uncorrelated)with)the)relevant)stock)index.)We)stick)to)this)definition)in)our)thesis,)but)will)provide)a)thorough)discussion)of)market)efficiency)and)the)market)neutrality)concept.)The)intention)is)to)help)the)reader)better)

) 7)

understand)the)implications)of)market)efficiency)and)how)it)relates)to)a)pairs)trading)portfolio.)))It)is)important)to)emphasize)that)even)if)a)portfolio)is)uncorrelated)with)the)market)index)it)might)have)significant)exposure)to)specific)industries.)In)other)words,)a)market)neutral)portfolio)is)not)automatically)immune)to)everything)that)happens)in)the)market.)It)is)reasonable)to)assume)that)it)is)uncorrelated)to)the)stock)index,)but)market)neutrality)does)not)by)any)means)imply)that)the)portfolio)is)risk)free,)just)that)the)portfolio)is)not)subject)to)market)risk.)The)capital)asset)pricing)model’s)(CAPM))main)assumption)is)that)market)risk)is)the)only)factor)for)which)the)investor)is)compensated,)thus)a)beta)neutral)portfolio)is)considered)risk)free)from)the)perspective)of)the)CAPM.)Therefore,)according)to)CAPM)a)beta)neutral)portfolio)should)not)be)able)to)earn)more)than)the)risk)free)return.)However,)subsequent)financial)research)has)made)it)reasonable)to)assume)that)investors)can)earn)returns)by)being)exposed)to)additional)risk)factors.)Identifying)these)risk)factors)are)however)quite)difficult,)but)compensation)for)exposure)to)liquidity)risk)(Acharya)and)Pedersen)2005;)Nagel)2012))and)arbitrage)risk)(Shleifer)and)Vishny)1997;)De)Long)et)al.)1990;)Abreu)and)Brunnermeier)2002))has)been)widely)discussed)in)financial)literature,)and)empirical)evidence)are)strongly)supportive)of)a)premium)for)bearing)these)risks.)Section)4)of)the)thesis)will)further)discuss)risk)factors)in)market)neutral)investment)strategies,)and)how)the)manager)can)earn)excess)returns)by)being)exposed)to)different)factors)of)risks.)For)now)we)should)just)take)with)us)that)a)market)neutral)portfolio)should)be)immune)to)general)market)fluctuations,)but)is)not)risk)free.)))Ehrman)(2006,)29C32))presents)several)concepts)of)market)neutrality)and)we)will)elaborate)on)those)relevant)for)the)remainder)of)the)thesis.)These)concepts)of)market)neutrality)is)especially)relevant)for)position)sizing,)as)we)must)make)a)decision)on)how)to)weight)the)two)stocks)in)a)pair)when)we)perform)pairs)trading.)))

2.1.1. Monetary,neutral,

Monetary)neutral,)or)in)our)case)a)Euro)neutral)portfolio,)has)an)equal)monetary)amount)in)the)long)and)short)positions,)hence)a)zero)net)monetary)exposure)to)the)market.))

) 8)

)€!"#$ = €!!!"#)

)The)Euro)neutral)manager)expects)stocks)he)goes)long)to)outperform)the)stocks)he)goes)short,)thus)he)tries)to)profit)from)the)relative)performance)between)the)stocks)in)his)portfolio.)The)dollar)neutral)portfolio)is)selfCfinancing,)because)the)same)monetary)amount)is)invested)in)long)and)short)position)each)time)an)investment)is)made1.)What)is)also)worth)mentioning)is)that)a)dollar)neutral)portfolio)might)have)a)very)different)risk)profile)on)the)long)and)short)positions)and)thus)might)operate)with)a)beta)that)deviates)significantly)from)zero.)Therefore)a)dollar)neutral)portfolio)is)not)necessarily)independent)of)the)market.)!

2.1.2. Beta,neutral,

A)beta)neutral)portfolio)weights)the)positions)in)each)stock)to)make)the)net)beta)of)the)long)and)short)positions)in)the)portfolio)is)zero.)))

!!"#$ = !!!!"#!)The)idea)behind)the)weighting)scheme)is)to)have)the)same)market)risk)on)the)long)and)short)components)of)the)portfolio.)If)you)invest)long)in)a)stock)with)a)beta)of)1)and)short)a)stock)with)a)beta)of)1.5,)you)end)up)taking)a)€)1.5)position)in)the)long)stock)and)€)C1)position)in)the)shorted)stock,)because)the)short)position)is)more)risky)than)the)long)position.)This)makes)the)pair)beta)neutral,)but)it)should)be)quite)obvious)that)a)beta)neutral)portfolio)is)not)necessarily)monetary)neutral.)Beta)weighting)of)the)long)and)short)positions)creates)a)strictly)market)independent)portfolio,)but)requires)frequent)adjustments)to)be)kept)market)neutral.)Even)though)monetary)neutral)is)the)most)commonly)used)method,)beta)neutrality)is)the)theoretically)correct)method)to)create)a)portfolio)that)is)independent)of)the)market)(Ehrman)2006,)29C32).))!

))))))))))))))))))))))))))))))))))))))))))))))))))))))))1)This)is)true)under)the)assumption)of)no)rebalancing,)as)any)rebalancing)will)lead)to)cash)flows)that)violate)the)selfCfinancing)condition.)2)The)main)strategies)reported)by)Malkiel)and)Saha)(2005))include)Convertible)bond)arbitrage,)Dedicated)short)bias,)Emerging)markets,)

) 9)

2.1.3. Sector,neutral,

The)manager)might)also)want)to)protect)his)portfolio)against)industry)specific)shocks,)and)can)construct)the)portfolio)so)that)it)becomes)immune)to)fluctuations)both)in)the)general)market)and)specific)industries.)For)instance,)a)trader)that)invests)in)technology)stocks,)might)prefer)to)be)unaffected)by)the)development)of)the)technology)industry.)He)can)obtain)this)by)combining)long)and)short)positions)to)create)a)neutral)portfolio)that)is)unaffected)by)changes)in)that)particular)industry.)The)investor)can)become)sector)neutral)in)terms)of)either)monetary)or)market)beta)exposure.))

2.2. Market,efficiency,and,profitBmaking,for,a,market,neutral,strategy,

So)why)does)a)fund)manager)want)to)be)independent)of)the)market?)The)main)advantage)of)market)neutrality)is)that)the)manager)is)able)to)make)relative)bets)instead)of)directional)bets.))To)become)market)neutral)the)fund)manager)must)use)a)combination)of)long)and)short)positions,)which)makes)returns)a)result)of)the)relative)performance)of)the)long)positions)versus)the)short)positions,)different)from)a)traditional)long)portfolio)that)derive)its)returns)from)absolute)performance)(Ehrman)2006,)89C90).)Jacobs)and)Levy)(2005))underline)that)an)equity)market)neutral)strategy)lets)the)investment)manager)fully)focus)on)security)selection)and)isolates)the)stock)picking)abilities)of)the)manager.)Moreover,)the)market)neutral)strategy)will)let)the)investor)exploit)the)universe)of)securities)even)better)than)the)traditional)long)strategy.)The)market)neutral)manager)can)act)on)all)his)views,)both)the)positive)and)negative,)as)well)as)profit)from)perceived)relative)mispricing)between)securities)or)sectors.)))From)the)above)paragraph)it)should)be)clear)that)the)market)neutral)strategy)tries)to)profit)from)market)inefficiencies)or)statistical)anomalies.)So)the)obvious)question)is)if)the)market)is)efficient)or)not?)Furthermore,)if)it)is)possible)to)consistently)identify)overC)and)undervalued)securities)and)earn)abnormal)returns?)The)“efficient)market”)is)a)term)first)introduced)by)Eugene)Fama)(1970).)He)defined)an)efficient)market)as)a)market)where)prices)fully)reflect)information,)and)in)the)same)paper)he)discusses)the)different)degrees)of)market)efficiency.)In)a)weakly)efficient)market,)prices)reflect)all)past)information,)thus)a)trading)strategy)based)on)historical)information,)should)not)be)able)to)earn)abnormal)returns.)A)stronger)degree)of)market)efficiency)is)semiCstrong)market)efficiency,)which)indicates)that)prices)reflect)all)

) 10)

public)information)and)is)continuously)updated)as)information)becomes)public.)Finally,)in)a)strongly)efficient)market)even)private)information)is)incorporated)in)prices.)As)the)careful)reader)has)probably)recognized,)even)weak)market)efficiency)would)dismiss)any)possibilities)of)abnormal)riskCadjusted)profits)from)technical)analysis,)and)a)semiCstrong)efficient)market)excludes)the)possibility)of)abnormal)riskCadjusted)profits)from)fundamental)analysis.)In)other)words,)semiCstrong)efficiency)rules)out)any)legal)possibilities)of)earning)consistent)abnormal)profits)in)the)financial)markets,)which)means)that)insider)trading)is)the)only)way)to)earn)abnormal)returns.)Therefore)we)will)concentrate)our)arguments)on)why)the)market)might)not)be)fully)efficient)and)why)even)the)weakest)form)of)market)efficiency)might)not)hold)at)all)times.)))An)important)point)in)the)discussion)on)market)efficiency)is)the)choice)of)equilibrium)model.)Fama)(1998))claims)that)the)only)way)to)prove)that)the)market)is)inefficient)is)to)be)able)to)statistically)reject)the)hypothesis)of)market)efficiency)independent)of)equilibrium)model.)So)far)market)efficiency)has)(to)our)knowledge))only)been)rejected)for)one)equilibrium)model,)CAPM,)and)according)to)Fama)it)is)just)as)likely)that)we)operate)with)the)wrong)equilibrium)model)and)that)there)are)yet)to)be)discovered)factors)that)drive)returns.)Even)though)there)is)no)formal)research)(as)far)as)we)know))that)gives)a)definitive)measure)of)the)efficiency)of)the)market,)the)lack)of)persistence)in)returns)for)both)hedge)fund)and)mutual)fund)managers)indicates)that)the)market)is)quite)efficient.)))Grossman)and)Stiglitz)(1980))introduce)an)interesting)contribution)to)the)discussion)on)market)efficiency.)They)present)a)model)with)an)equilibrium)degree)of)disequilibrium,)and)argue)how)cost)of)information)makes)a)fullCinformation)equilibrium)impossible.)The)model)is)based)on)heterogeneous)information)among)investors)and)the)assumption)that)investors)have)to)pay)to)retrieve)information.)They)argue)that)a)completely)efficient)market)cannot)exist)under)circumstances)when)information)is)costly)to)obtain,)because)investors)demand)compensation)to)search)for)information,)and)no)investor)is)incentivized)to)gather)information)in)a)perfectly)efficient)market.)According)to)arguments)by)Fama)(1965))deviations)from)fundamental)prices)can)appear,)but)should)be)corrected)by)arbitrageurs)almost)instantaneously.)Thus,)deviations)from)the)Law)of)One)price)(LoOP))should)be)minor)and)only)exist)for)a)very)short)period)of)time.)Black)(1986))has)an)opposing)view,)he)discusses)the)

) 11)

concept)of)noise)traders)and)describes)how)the)actions)of)noise)traders)can)drive)prices)away)from)fundamentals.)Another)example)of)a)violation)of)market)efficiency,)in)the)context)of)the)capital)asset)pricing)model,)is)evidence)from)research)by)Fama)and)French)(1992).)They)construct)a)portfolio)that)invests)long)in)stocks)with)a)small)market)cap)and)short)stocks)with)a)large)market)cap,)and)this)portfolio)is)able)to)explain)average)returns)in)the)period)from)1963C1990.))This)has)later)been)known)as)the)small)minus)big)factor)(SMB))and)has)been)one)of)very)few)factors)that)have)shown)explanatory)power)of)market)returns)for)longer)periods)of)time.)The)HML)factor)is)another)statistical)anomaly)that)has)shown)the)ability)to)explain)average)stock)returns,)and)is)defined)as)a)portfolio)long)stocks)with)high)book)value/market)value)(B/M))ratio)and)short)stocks)with)a)low)ratio.)What)are)considered)high)or)low)ratios)is)at)the)individual)managers)discretion,)but)the)industry)average)is)typically)used)as)the)separation)point.)The)rationale)is)that)a)firm)with)a)higher)B/M)relative)to)its)peers)is)cheap)compared)to)a)firm)with)a)low)B/M,)which)is)considered)expensive.)The)problem)with)the)SMB,)HML)and)other)strategies)that)seems)to)generate)returns)over)a)longer)period)of)time)is)that)there)are)few)explanations)or)theoretical)arguments)that)can)rationalize)the)results.)When)we)do)not)have)a)rationale)to)support)the)results,)they)come)up)more)as)statistical)anomalies)than)explanations)of)inefficiencies)in)the)market.)A)statistical)anomaly)that)actually)has)been)accompanied)by)a)reasonable)explanation)is)the)momentum)effect.)Jegadeesh)and)Titman)(1993))find)that)buying)recent)winners)and)selling)recent)losers)results)in)returns)that)significantly)outperform)the)market.)The)evidence)implies)that)it)is)not)due)to)systematic)risk,)but)the)existence)of)a)momentum)effect)caused)by)a)delayed)reaction)to)firm)specific)news.)Pedersen)(Not)yet)published))tells)a)slightly)different)story,)and)explains)that)trends)start)when)people)underreacts)to)news)and)as)prices)reach)fundamentals)more)traders)continues)to)invest)in)the)trade,)leading)to)a)delayed)overreaction,)before)it)reverses)back)to)the)fundamental)value.)))De)Bondt)and)Thaler)(1985))find)evidence)of)an)overreaction)to)market)news,)consistent)with)temporary)deviations)from)market)efficiency.)They)find)that)previous)losers)the)last)3C5)years)outperform)previous)winners)during)the)next)3C5)year)period.)This)is)often)termed)the)reversal)or)value)effect)and)is)an)example)of)the)reversion)to)the)fundamental)value)that)follows)an)overreaction.)In)recent)times,)Asness,)Moskowitz)and)Pedersen)(2013))show)that)a)portfolio)with)50/50)combination)of)momentum)and)value)delivers)excess)returns)and)

) 12)

outperforms)the)two)individual)strategies)in)both)the)American)and)European)market)during)the)period)1975C2008.)They)argue)that)the)combined)strategy)benefits)from)the)negative)correlation)between)the)two)individual)strategies,)since)momentum)is)positively,)while)value)is)negatively)correlated)to)liquidity)risk.)Frazzini)and)Pedersen)(Forthcoming))furthermore)demonstrate)that)a)portfolio,)which)shorts)high)beta)stocks)and)makes)a)leveraged)investment)in)low)beta)stocks,)effectively)creating)a)market)neutral)portfolio,)is)able)to)earn)abnormal)riskCadjusted)returns.)They)claim)that)it)is)due)to)some)investors’)natural)preference)of)high)beta)stocks,)because)they)are)unable)leverage)or)have)conservative)restrictions)on)the)use)of)leverage.)Pension)funds)or)mutual)fund)managers,)unable)to)leverage,)invest)in)high)beta)assets)to)be)able)to)meet)their)required)return)on)capital.)The)result)is)excess)demand)for)high)beta)stocks,)which)become)relatively)expensive)compared)to)low)beta)stocks,)and)this)is)an)opportunity)that)can)be)exploited)by)arbitrageurs.)Despite)these)examples)that)the)market)behaves)with)some)degree)of)inefficiency)on)occasion,)the)majority)of)the)strategies)or)rules)that)provide)excess)returns)seem)to)only)work)for)a)limited)period)of)time.)Malkiel)(2003))points)out)that)strategies,)which)yield)abnormal)returns)seem)to)stop)working)after)they)get)attention)in)financial)literature.)He)further)argues)that)the)IT)bubble)of)the)late)1990’s)is)an)example)of)a)time)when)the)prices)was)incorrect,)but)he)emphasizes)that)there)were)no)arbitrage)opportunities,)because)nobody)could)possibly)know)what)the)future)of)the)internet)would)be.)Thus)the)market)was)not)inefficient,)because)prices)actually)reflected)the)available)information)at)that)time.)His)conclusion)is)that)whatever)irrationalities)and)mispricing)exist)in)the)market,)they)are)only)in)existence)for)a)short)amount)of)time,)so)any)methods)or)strategies)that)obtain)excess)returns)are)unlikely)to)persist.)The)difficulty)of)consistently)beating)the)market)gathers)further)support)from)Malkiel)and)Saha)(2005).)They)show)that)once)you)adjust)for)reporting)biases)convertible)bond)arbitrage)is)the)only)main)hedge)fund)strategy2)that)generates)a)higher)Sharpe)ratio)than)the)S&P)500)in)the)period)between)1995C2003.)They)find)huge)cross)sectional)variations)and)the)difference)between)the)best)and)the)worst)performing)funds)within)a)certain)investment)strategy)is)substantial.)They)only)find)limited)evidence)of)persistence)for)the)managers)that)perform)above)median)in)a)given)year,)which)is)supportive)of)relatively)high)market)efficiency.)A)final)point)is)that)some)strategies)are)either)very)transaction)costs)intensive)or)require)significant)investments)in)infrastructure)or)))))))))))))))))))))))))))))))))))))))))))))))))))))))))2)The)main)strategies)reported)by)Malkiel)and)Saha)(2005))include)Convertible)bond)arbitrage,)Dedicated)short)bias,)Emerging)markets,)Equity)market)neutral,)Event)driven,)FixedCincome)arbitrage,)Fund)of)funds,)Global)macro,)LongCshort)equity)hedge,)Managed)futures)and)other)strategies.)

) 13)

equipment,)hence)to)discover)the)true)profitability)of)a)strategy)it)should)be)evaluated)after)taken)all)these)costs)into)account.))This)thesis)is)by)no)means)an)attempt)to)summarize)the)full)discussion)on)market)efficiency,)but)we)believe)it)is)of)great)benefit)to)the)reader)that)we)address)some)of)the)findings)in)the)literature)on)market)efficiency.)The)above)examples)underline)the)difficulty)of)outperforming)the)market)over)time.)At)the)same)time,)there)are)several)examples)of)strategies)that)have)seemed)to)crack)the)code)at)least)for)a)limited)period,)and)it)seems)like)there)is)occasional)existence)of)what)appears)to)be)market)inefficiencies.)To)conclude)this)section,)we)emphasize)the)findings)of)Malkiel)and)Saha)(2005).)They)find)evidence)of)very)diverging)results)for)investment)managers)using)similar)strategies,)so)it)is)not)enough)to)simply)choose)the)right)strategy,)but)execution)is)also)instrumental)to)beat)the)market.))

2.3. Leverage,in,Market,Neutral,strategies,

Leverage)plays)an)important)role)in)profit)making)for)investors)that)use)a)market)neutral)strategy.)Hedge)funds)use)leverage)by)financing)long)positions)with)proceeds)from)short)positions,)to)increase)the)absolute)returns)of)the)portfolio.)Additional)leverage)is)usually)financed)by)the)hedge)fund’s)prime)broker,)and)historically)the)ability)to)use)considerable)amounts)of)leverage)has)helped)hedge)funds)make)sizeable)returns,)which)other)investment)classes)struggle)to)compete)with.)We)will)provide)a)short)example)to)explain)how)hedge)funds)can)obtain)leverage)by)using)proceeds)from)short)positions.)If)a)market)neutral)hedge)fund)has)$100)million)to)invest,)they)can)take)a)position)of)$90)million)long)and)$90)million)short)simultaneously.)How)can)they)do)this)with)only)$100)million)in)total)funds?)When)they)sell)a)position)short)they)instantly)receive)the)proceeds)from)the)short)sale,)which)allows)them)to)have)approximately)$180million)in)active)long)and)short)positions.)The)proceeds)from)the)short)investment)are)held)by)the)prime)broker)as)collateral,)and)our)original)$90)million)covers)the)long)position.)If)the)investor)wants)to)further)increase)the)magnitude)of)his)positions)he)can)take)on)additional)leverage)by)i.e.)borrow)from)his)prime)broker,)but)we)ignore)that)for)now.)So)what)happens)to)the)remaining)$10)million)that)was)not)invested?))They)are)kept)by)the)broker)to)cover)potential)losses)in)the)short)position.)The)case)of)Long)Term)Capital)Management)(LTCM))is)a)good)example)of)how)important)it)is)to)control)

) 14)

leverage)and)have)a)sufficiently)large)liquidity)buffer)in)your)portfolio.)Even)if)you)are)right)in)the)end,)as)first)expressed)by)John)Maynard)Keynes:)“The)market)can)stay)irrational)longer)than)you)can)stay)solvent”.)Therefore)it)is)important)to)keep)a)liquidity)buffer)in)a)portfolio,)to)make)sure)that)you)are)not)forced)out)of)your)positions,)and)unable)to)profit)on)your)trades.)The)fact)that)hedge)funds)have)the)opportunity)to)leverage)makes)us)more)interested)in)measures)of)riskCadjusted)returns,)as)these)are)independent)of)leverage.)The)Sharpe)ratio)is)a)common)measure)of)riskCadjusted)return,)and)it)normalizes)the)excess)return)by)the)standard)deviation)of)the)return.)A)hedge)fund)can)always)reduce)or)apply)leverage)to)adjust)the)risk)of)the)portfolio,)and)thus)modify)the)expected)return.))

2.4. The,Equity,Market,Neutral,strategy,as,a,hedge,in,the,investment,portfolio,

An)investment)strategy)is)often)discussed)in)isolation,)but)by)combining)different)strategies)with)a)low)or)negative)correlation,)the)investor)can)achieve)additional)benefits)of)diversification.)The)work)of)Fung)and)Hsieh)(1999))show)that)returns)from)hedge)funds)have)a)very)low)correlation)to)the)return)of)mutual)funds)and)market)indices.)They)also)argue)that)a)hedge)fund)strategy)should)not)be)thought)of)in)isolation,)but)rather)as)a)part)of)a)larger)investment)portfolio.)With)that)in)mind)we)can)easily)argue)that)investments)in)different)hedge)fund)strategies)is)an)additional)tool)of)diversification)for)the)multiple)asset)class)investor.)Furthermore,)a)market)neutral)strategy)should)be)a)good)diversifying)component)in)an)investment)portfolio,)as)it)has)a)low)correlation)to)marketCtiming)hedge)fund)strategies)(Fung)and)Hsieh)1999).)To)elaborate,)marketCtiming)strategies)include)strategies)with)directional)bets)i.e.)Global)Macro)or)Managed)Futures)strategies,)so)they)are)different)from)nonCdirectional)strategies)like)equity)market)neutral.)This)makes)market)neutral)investments)not)only)a)good)diversifier)with)nonChedge)fund)investments,)but)also)with)other)hedge)fund)strategies.)))

2.5. Portfolio,rebalancing,

Several)hedge)fund)strategies)require)dynamic)adjustments)of)the)portfolio)components.)An)example)is)convertible)bond)arbitrage.)In)convertible)bond)arbitrage)the)investor)tries)to)exploit)the)theoretical)discount)on)convertible)bonds)compared)to)its)theoretical)value.)The)

) 15)

convertible)bond)is)a)combination)of)a)corporate)bond)and)an)equity)option,)so)the)arbitrageur)can)replicate)the)convertible)bond)with)positions)in)a)corporate)bond)and)the)equity)of)the)company.)It)is)crucial)that)the)replicating)portfolio)is)frequently)updated)so)it)perfectly)mirrors)the)value)of)the)convertible)bond.)This)might)feel)a)little)offCtopic,)but)the)point)is)that)more)sophisticated)investment)strategies)often)require)dynamic)adjustments,)and)portfolio)rebalancing)plays)an)important)role)in)equity)market)neutral)strategies.)Ideally)the)hedge)fund)manager)should)rebalance)his)portfolio)frequently)to)make)sure)he)stays)close)to)market)neutral)at)all)times.)Based)on)earlier)discussion,)this)can)for)instance)be)neutral)in)terms)of)monetary)exposure)or)market)risk.)A)potential)consequence)of)lack)of)rebalancing)is)that)the)portfolio)is)subject)to)a)significant)market)exposure)the)manager)initially)wanted)to)avoid.)After)the)portfolio)is)traded)for)a)day,)prices)change)and)so)does)the)exposure)of)the)portfolio.)If)the)portfolio)is)left)alone)it)can)develop)a)meaningful)exposure,)and)the)characteristics)of)the)portfolio)can)end)up)quite)different)from)the)initial)market)neutral.)The)problem)is)that)frequent)rebalancing)of)the)portfolio)results)in)high)transaction)costs,)so)there)is)a)tradeCoff)between)these)costs)and)a)wellCbalanced)portfolio.)The)choice)of)rebalancing)frequency)is)dependent)on)both)the)trading)horizon)and)the)type)of)investment)strategy,)and)a)traditional)market)neutral)portfolio)is)usually)rebalanced)weekly,)monthly)or)quarterly)dependent)on)the)risk)profile)and)investment)horizon)(Credit)Suisse)Asset)Management,)LLC)2009).)It)also)worth)mentioning)that)the)bidCask)spread)has)decreased)substantially)in)recent)years,)so)the)cost)of)rebalancing)is)significantly)lower)now)than)it)was)10)or)20)years)ago)(Do)and)Faff)2012).)))

2.6. Statistical,Arbitrage,

The)previous)subsection)discussed)potential)market)inefficiencies,)and)the)pure)essence)of)statistical)arbitrage)is)to)earn)a)profit)by)exploiting)market)inefficiencies)found)in)historical)data.)So)an)investor)engaging)in)statistical)arbitrage)is)by)definition)convinced)that)the)market)cannot)be)completely)efficient.)!)The)most)common)understanding)of)arbitrage)is)a)case)where)you)can)earn)a)certain)profit)by)going)long)one)stock)and)short)another,)typically)due)to)different)prices)for)the)same)asset)

) 16)

across)markets.)A)more)formal)definition)of)arbitrage)is)a)portfolio)with)0)or)negative)cost)and)positive)value)or)with)a)negative)cost)and)zero)or)positive)value.)This)is)formally)expressed)as:))

!"#$% ≤ 0!!"#!!"#$%% > 0!!"!

!"#$% < 0!!"#!!"#$%% ≥ 0))Two)of)the)best)examples)of)these)kind)of)arbitrage)opportunities)are)Shell/Royal)Dutch)and)3com/Palm,)but)such)opportunities)are)very)rare,)and)too)few)to)offer)frequent)profits)for)investors.)Royal)Dutch)and)Shell)had)a)dual)listed)company)structure)until)2005,)so)theoretically)the)stock)prices)of)the)two)companies)should)have)moved)in)lock)step,)as)they)were)entitled)to)the)same)cash)flows.)Contrary)to)expectations)the)prices)experienced)spreads)significantly)different)from)zero)in)the)period)between)1976)and)1986)(Rosenthal)and)Young)1990))and)offered)opportunities)to)profit)from)the)price)difference)in)the)two)companies.)3com)and)Palm)is)another)example.)3com)owned)95%)of)Palm,)but)had)negative)stub)value)for)a)longer)period)in)2000.)A)negative)stub)value)implied)that)the)assets)owned)by)3com)had)a)negative)value)after)3Com’s)stake)in)Palm)was)subtracted.)This)is)also)a)clear)arbitrage)opportunity,)according)to)financial)theory,)since)the)actual)value)of)Palm’s)remaining)assets)without)a)doubt)was)nonCnegative.)In)both)the)aboveCmentioned)cases)investors)can)invest)long)in)the)underpriced)security)and)short)the)overpriced)security)to)earn)an)arbitrage)profit.)Profiting)from)an)arbitrage)opportunity)is)though)not)as)easy)as)it)seems.)To)extract)the)profit)from)the)mispricing)the)investor)must)be)able)to)hold)his)positions)through)further)mispricing)until)prices)eventually)diverge.)Several)of)the)investors)in)Shell/Royal)Dutch)had)leveraged)positions)and)as)prices)continued)to)diverge)they)where)unable)to)cover)the)margin)calls.)Even)though)they)where)right)to)identify)the)arbitrage)opportunity)they)were)unable)to)structure)the)trade)right,)and)ended)up)with)substantial)losses.)It)should)also)be)mentioned)that)in)the)case)of)3com/Palm)the)arbitrage)opportunity)could)not)be)exploited,)as)the)Palm)stock)was)impossible)to)short)(Lamont)and)Thaler)2003).)))In)contrast)to)the)common)perception)of)arbitrage,)statistical)arbitrage)is)related)to)mispricing)based)on)deviations)from)the)expected)and)not)the)actual)value.)In)this)case,)there)is)no)guarantee)that)a)price)will)ever)equal)its)expected)value,)but)the)mispricing)is)true)in)

) 17)

expectation.)Additionally,)the)calculations)of)the)expected)value)will)often)differ)between)managers)dependent)on)the)number)of)observations)and)time)horizon.)Bondarenko)(2003))defines)a)statistical)arbitrage)opportunity)as)a)zero)cost)strategy)with)a)positive)expected)payoff.)The)idea)behind)statistical)arbitrage)is)that)price)relationships)will)converge)to)their)expected)values)on)average,)so)even)if)the)strategy)occasionally)yields)negative)returns)it)will)offer)positive)average)returns)in)the)long)run.)The)challenge)for)the)investment)manager)is)to)sustain)margin)calls)in)the)years)with)negative)returns,)so)the)broker)does)not)liquidate)the)positions)when)the)trade)is)valued)at)its)lowest.)A)statistical)arbitrage)manager)exploits)deviations)from)the)expected)value)of)a)price)relationship)between)two)or)more)securities)and)makes)a)profit)if)the)price)relationship)returns)to)its)expected)value.)Avellaneda)and)Lee)(2010))mention)three)common)features)of)statistical)arbitrage)as)an)investment)strategy:)1))trading)signals)are)systematic)2))the)portfolio)has)a)beta)of)zero)and)3))statistical)techniques)are)used)as)a)tool)to)generate)returns.)Statistical)arbitrage)often)involves)a)large)amount)of)trades)so)the)performance)of)the)portfolio)is)less)dependent)on)the)performance)of)a)single)trade.)The)trading)opportunities)are)identified)using)historical)price)data)and)strategies)are)often)very)data)intensive)and)performed)by)advanced)computer)systems.)Moreover,)statistical)arbitrage)portfolios)are)usually)very)wellCdiversified,)and)a)typically)consists)of)a)large)number)of)stocks.)Since)these)strategies)are)model)driven,)the)manager)can)include)a)large)number)of)stocks,)whereas)a)fundamental)investor)will)be)restricted)by)the)time)used)to)analyze)each)individual)stock)or)industry.)In)the)upcoming)section)on)pairs)trading,)we)will)see)that)a)pairs)trading)strategy)has)a)lower)number)of)stocks,)which)is)atypical)for)a)statistical)arbitrage)portfolio.)The)low)number)of)stocks)in)a)portfolio)has)a)very)simple)explanation.)CoCmovement)between)stocks)is)rare,)and)an)increase)in)the)number)of)stocks)will)damage)the)quality)of)the)pairs,)so)the)lower)number)of)stocks)in)the)portfolio)is)just)due)to)low)availability)of)qualified)pairs.))

3. An,introduction,to,pairs,trading,Now)that)we)have)introduced)some)of)the)more)fundamental)concepts)pairs)trading)is)based)on,)we)are)ready)to)proceed)to)the)main)part)of)the)thesis.)We)consider)pairs)trading)an)interesting)case)for)further)investigation,)as)it)is)a)simple)investment)strategy)that)has)yielded)

) 18)

excess)returns)over)longer)periods)of)time)and)performed)especially)well)during)periods)of)market)turbulence)(Gatev,)Goetzmann,)and)Rouwenhorst)2006;)Do)and)Faff)2010).))

3.1. What,is,pairs,trading?,

The)authors)of)this)thesis)consider)pairs)trading)to)be)just)one)of)many)strategies)that)fit)under)the)broader)category)of)statistical)arbitrage.)The)essence)of)pairs)trading)is)to)identify)stocks)that)have)historically)moved)together,)and)create)pairs)of)these)securities)with)the)belief)that)they)will)continue)to)move)together)in)the)future.)Under)the)discussion)of)statistical)arbitrage)we)mentioned)that)arbitrageurs)try)to)exploit)deviations)from)expected)values,)and)this)is)exactly)what)the)pairs)trader)does.)In)the)case)of)pairs)trading)the)expected)value)is)the)average)historical)spread)between)the)returns)of)the)two)securities)in)a)pair,)so)for)high)quality)pairs)the)expected)value)of)the)spread)is)going)to)be)close)to)zero.)The)pairsCtrading)manager)expects)the)historical)relation)to)continue)to)hold)in)the)future)and)will)initiate)a)trade)when)the)prices)between)two)paired)securities)diverge)beyond)a)predetermined)threshold.)He)tries)to)exploit)a)deviation)from)the)expected)value)by)taking)a)long)position)in)the)relatively)cheap)stock)and)sell)short)in)the)relatively)expensive)stock,)and)if)the)prices)of)the)two)stocks)converge)back)to)the)expected)relationship)the)manager)exit)the)positions.)This)is)a)simplified)explanation)of)the)pairs)trading)process,)and)a)more)thorough)and)informative)explanation)will)be)provided)in)the)section)where)we)explain)how)to)construct)a)pairs)trading)portfolio.))It)is)difficult)to)understand)how)such)a)simple)strategy)can)be)profitable,)and)this)makes)pairs)trading)a)challenging)and)interesting)subject)to)study.)Pairs)are)often)constructed)with)stocks)from)the)same)or)related)industries,)but)they)can)also)be)constructed)across)industries.)Constructing)pairs)with)stocks)from)different)industries)makes)it)even)more)difficult)to)explain)why)stocks)follow)each)other)closely,)but)greatly)increases)the)universe)of)stocks)from)which)the)investor)can)construct)pairs.)It)is,)however,)not)uncommon)for)pairs)traders)to)exclude)identified)pairs)that)appears)to)be)directly)counterintuitive)when)they)form)pairs)across)industries)(Ehrman)2006,)147).)Possible)explanations)for)the)coCmovement)in)stocks)might)be)that)they)have)equal)exposure)to)the)same)risk)factors.)Different)attempts)to)understand)the)returns)from)pairs)trading)argue)about)market)inefficiency)or)compensation)

) 19)

for)exposure)to)other)risk)factors)than)the)market)beta.)So)far)none)of)these)attempts)has)been)able)to)fully)explain)how)the)strategy)can)earn)abnormal)returns,)and)the)absence)of)a)satisfactory)understanding)of)the)sources)of)returns)makes)this)an)interesting)subject)for)further)research.))

3.2. The,Origin,of,Pairs,Trading,

The)idea)of)looking)at)pairs)of)stocks,)instead)of)a)single)stock)in)isolation,)can)be)traced)back)to)as)far)as)the)early)1900’s)and)the)trader)Jesse)Livermore,)who)by)many)is)claimed)to)be)one)of)the)best)traders)of)all)times.)He)analyzed)two)stocks)in)the)same)industry)at)the)same)time)to)confirm)his)fundamental)analysis.)His)rationale)was)that)stocks)in)the)same)industry)should)move)in)tandem,)and)by)following)two)stocks)instead)of)one)he)would)better)understand)the)changes)in)the)price)of)the)stocks.)Livermore)then)looked)at)the)development)between)two)stocks)to)trade)on)what)he)considered)irregularities)(Smitten)2004).)Hence)the)initial)idea,)which)pairs)trading)was)based)on)is)related)to)coCmovement)between)stocks)from)the)same)industry.)Even)though)we)can)trace)elements)of)pairs)trading)back)to)Jesse)Livermore,)what)we)today)consider)pairs)trading)did)not)appear)until)the)mid)1980’s.)Nunzio)Tartaglia)and)his)quant)group)at)Morgan)Stanley)were)the)first)to)initiate)in)pairs)trading,)and)during)their)first)years)of)operations)the)firm)earned)impressive)profits.)The)group)was)nevertheless)disbanded)in)1989)after)suffering)losses)the)preceding)couple)of)years,)but)the)early)performance)of)the)quant)group)at)Morgan)Stanley)had)caught)the)interest)of)the)public.)After)the)success)of)Tartaglia’s)group,)pairs)trading)has)become)a)popular)investment)strategy,)particularly)at)proprietary)trading)desks)and)hedge)funds)(Gatev,)Goetzmann,)and)Rouwenhorst)2006).)))

3.3. Previous,literature,

Previous)literature)on)pairs)trading)has)mostly)been)concerned)with)the)US)equity)market,)and)far)as)the)authors)of)this)thesis)know,)earlier)research)only)covers)the)time)period)from)1962C2009.)Thus)there)is)limited)literature)on)pairs)trading)beyond)US)data)and)no)academic)research)on)how)the)investment)strategy)performs)during)the)last)couple)of)years,)after)the)outbreak)of)the)Euro)crisis.)The)performance)of)pairs)trading)during)the)Euro)crisis)is)of)particular)interest)since)pairs)trading)is)known)to)work)well)in)periods)with)poor)market)

) 20)

returns.)In)this)section)we)will)present)some)of)the)most)important)academic)papers)and)empirical)findings,)as)these)are)the)main)inspiration)for)our)research)and)the)methods)we)use)in)the)construction)of)our)portfolio.))

3.3.1. Most,Influential,academic,papers,

The)pairs)trading)approach)in)this)thesis)is)to)a)large)extent)inspired)by)the)pair)identifying)metrics)and)methods)used)in)the)most)influential)papers)about)pairs)trading.)Some)of)the)terms)and)methodology)in)this)section)might)be)new)to)the)reader,)but)those)relevant)for)the)remainder)of)the)thesis)will)be)further)explained)when)we)construct)our)own)pairs)trading)portfolio.)))The)first)paper)to)discuss)pairs)trading,)Gatev,)Goetzmann)and)Rouwenhorst)(2006),)investigate)the)performance)of)the)strategy)between)1962)and)2002.)They)choose)a)formation)period)of)12)months)to)identify)coCmovement)in)returns)between)different)stocks.)The)authors)look)at)the)total)return)series)of)different)stocks)and)rank)potential)pairs)by)the)sum)of)squared)differences)(SSD),)which)is)a)measure)of)how)close)the)different)securities)move.)Pairs)are)ranked)from)the)lowest)to)highest)in)terms)of)the)SSD)measure.)Furthermore,)they)construct)portfolios)consisting)of)pairs)ranked)top)5,)top)20,)101C120)and)one)portfolio)with)all)their)pairs)in)their)sample)to)separate)the)performance)by)pairs)with)different)rankings.)The)entry)threshold)is)set)based)on)the)standard)deviation)of)the)spread)between)securities)in)a)pair)during)the)formation)period.)If)prices)diverge)more)than)two)times)the)standard)deviation)from)the)formation)period,)they)open)a)trade)and)hold)it)until)prices)converge.)If)an)open)pair)does)not)converge)before)the)end)of)the)trading)period,)they)exit)the)position)at)the)last)day)of)the)trading)period.)The)profit)is)of)course)dependent)on)the)level)of)the)spread)at)entry)versus)the)level)of)the)spread)when)they)exit)the)trade.)Trades)are)constructed)to)be)selfCfinancing,)which)means)that)$)1)is)invested)long)in)the)relatively)cheap)stock)and)$1)is)invested)short)in)the)relatively)expensive)stock.)They)use)a)six)months)trading)period,)and)start)trading)a)new)portfolio)every)month.)This)means)that)they)have)six)different)portfolios)active)at)all)times.)Gatev,)Goetzmann)and)Rouwenhorst)also)separate)between)unrestricted)and)restricted)pairs,)where)unrestricted)pairs)are)chosen)solely)by)their)mathematical)relationships.)The)restricted)pairs)on)the)other)hand,)are)restricted)to)only)contain)stocks)

) 21)

from)the)same)industry)and)are)chosen)from)the)four)Standard)&)Poor’s)industry)classifications)Transportation,)Utilities,)Financial)services)and)Industrials.)))Another)influential)paper)within)pairs)trading)is)Do)and)Faff)(2010),)and)they)analyze)pairs)trading)returns)in)a)more)recent)time)period,)2003C2009.)Do)and)Faff)also)use)the)SSD)metric)to)sort)out)potential)pairs,)but)suggest)additional)measures)to)identify)better)pairs.)One)of)them)is)zero)crossings)(ZC),)defined)as)the)number)of)times)the)two)cumulative)return)series)in)a)pair)crosses)each)other.)They)discover)that)the)most)profitable)trades)exhibit)a)high)number)of)zero)crossings)in)the)formation)period,)which)is)supportive)of)their)hypothesis)that)ZC)could)be)a)good)measure)to)identify)profitable)pairs.)Moreover,)they)construct)portfolios)by)combining)the)SSD)and)ZC)approach,)where)they)first)sort)out)the)pairs)by)SSD)and)then)rank)these)pairs)according)to)ZC.))

3.3.2. Empirical,Findings,

Gatev,)Goetzmann)and)Rouwenhorst)(2006))find)annualized)excess)returns)of)up)to)11%,)and)evidence)of)abnormal)returns)even)after)accounting)for)transaction)costs.)Furthermore,)by)looking)at)the)length)of)the)holding)period)of)a)position,)estimated)to)be)close)to)4)months,)they)claim)that)pairs)trading)should)be)considered)a)medium)term)investment)strategy.)They)emphasize)the)importance)of)diversification)and)find)that)minimum)realized)returns)actually)increases,)while)maximum)return)remains)quite)stable)when)they)increase)their)portfolios)from)top)5)to)top)20)pairs.)This)indicates)the)existence)of)a)very)favorable)diversification)effect)when)the)number)of)pairs)in)the)portfolio)is)increased.)Moreover,)the)standard)deviation)of)the)portfolio)decreases)as)they)increase)the)number)of)pairs,)once)again)consistent)with)a)favorable)diversification)effect.)They)try)to)regress)their)returns)on)common)risk)factors,)and)find)no)clear)evidence)of)a)factor)exposure)that)can)fully)explain)the)excessive)returns.)In)their)top)20)pairs,)momentum)is)negative)and)the)only)significant)variable,)but)the)regression)does)not)offer)enough)explanatory)power)to)explain)the)average)returns.)By)including)all)pairs)they)find)that)coefficients)of)reversal)and)momentum)have)significant)and)expected)signs,)but)also)seem)too)small)to)fully)explain)the)returns)of)pairs)trading.)Instead)they)suggest)that)there)is)a)latent)risk)component)that)can)explain)the)profit)of)pairs)trading,)but)they)do)not)offer)any)explanations)of)what)this)factor)might)be.)Nevertheless,)they)suggest)

) 22)

that)the)abnormal)returns)are)compensation)for)enforcing)the)Law)of)One)Price)(LoOP).)The)paper)also)discovers)a)declining)profitability)in)pairs)trading)after)1988)compared)to)earlier)periods.)They)claim)that)it)is)due)to)increased)competition)between)arbitrageurs)who)drive)away)the)potential)profits)of)pairs)trading.)This)is)in)accordance)with)the)view)that)opportunities)to)earn)abnormal)returns)disappear)as)they)get)attention,)and)are)exploited)by)more)investors)(Malkiel)2003).)Gatev,)Goetzmann)and)Rouwenhorst)(2006))state)that)their)findings)of)abnormal)returns)in)the)US)equity)market)is)in)conflict)with)market)efficiency,)but)they)further)argue)that)risk)factors)with)the)potential)to)explain)returns)are)difficult)to)find)and)that)the)market)might)be)efficient)when)the)latent)risk)factor)is)taken)into)account.))Do)and)Faff)(2010))provide)further)evidence)of)the)decreasing)trend)in)the)profitability)of)pairs)trading,)but)conclude)that)profitability)can)be)improved)by)creating)more)homogenous)pairs)and)taking)the)frequency)of)price)crossings)into)account.)Homogenous)pairs)are)defined)as)stocks)within)the)same)industry)classification,)and)they)hypothesize)that)a)narrower)classification)might)increase)the)profitability)of)pairs)trading.)In)contrast)to)Gatev,)Goetzmann)and)Rouwenhorst)(2006),)they)claim)that)the)decreasing)trend)in)the)profitability)of)pairs)trading)cannot)be)due)to)more)intense)competition)between)pairs)traders.)They)find)a)much)larger)proportion)of)nonCconverging)trades)in)the)period)1989C2002)compared)to)1962C1988,)and)this)is)inconsistent)with)the)explanation)that)the)profitability)of)pairs)trading)has)declined)because)arbitrageurs)are)too)quick)to)correct)deviations)from)the)LoOP.)Do)and)Faff)(2010))explain)the)worsened)performance)of)pairs)trading)in)recent)periods)with)a)lower)proportion)of)convergence)for)open)pairs)and)that)pairs)use)longer)time)to)converge)on)average.)A)more)efficient)market)would)have)implied)a)larger)proportion)of)nonCtraded)pairs)instead)of)a)tendency)not)to)converge,)thus)the)argument)made)by)Gatev,)Goetzmann)and)Rouwenhorst)cannot)be)true,)if)the)proposed)statistical)relationship)is)correct.)The)proportion)of)pairs)that)does)not)converge)increased)from)26%)to)40%)from)the)period)1962C1988)to)2003C2009.)In)addition,)the)fraction)of)pairs)that)trade)multiple)times)during)the)trading)period)decreased)from)42%)to)24%)between)the)same)periods.)Do)and)Faff)(2010))explain)their)findings)as)evidence)of)a)worsening)arbitrage)risk)during)the)period.)We)will)elaborate)on)arbitrage)risk)in)the)section)about)sources)of)risk)in)pairs)trading.))

) 23)

Engelberg,)Gao)and)Jagannathan)(2008))also)discuss)the)rationale)behind)potential)profits)in)pairs)trading)and)study)how)idiosyncratic)news,)common)news)and)liquidity)are)affecting)the)pairs’)performance.)They)claim)that)news,)which)temporarily)decreases)the)liquidity)in)one)of)the)stocks)in)a)pair,)increases)the)probability)of)convergence)in)the)pair.)They)argue)that)news)may)lead)to)a)faster)reaction)in)one)of)the)stocks,)depending)on)the)difference)in)the)liquidity)level)of)the)two)securities.)This)theory)is)supportive)of)liquidity)supply)as)one)of)the)main)drivers)of)profitability)within)pairs)trading,)but)while)Engelberg,)Gao)and)Jagannathan)(2008))focuses)on)the)liquidity)of)single)stocks,)our)empirical)research)will)focus)more)on)the)role)of)the)overall)market)and)funding)liquidity.)They)also)find)that)idiosyncratic)news)that)fundamentally)changes)the)underlying)operations)of)one)of)the)stocks)in)a)pair)can)lead)to)a)permanent)divergence)for)the)stocks)in)a)pair.)Andrade,)Di)Pietro)and)Seasholes)(2005))offer)additional)support)for)liquidity)as)an)important)driver)of)profitability.)They)look)at)the)relationship)between)uninformed)demand)shocks)and)pairs)trading)returns.)The)data)is)collected)from)the)Taiwanese)stock)exchange,)and)they)try)to)estimate)the)uninformed)demand)in)the)market)by)using)aggregate)net)shares)held)long)on)margin)as)a)proxy)for)uninformed)demand.)The)authors)find)evidence)that)a)stock’s)expected)return)increases)with)the)volatility)of)changes)in)uninformed)long)margin)holdings.)They)find)a)relationship)between)the)level)of)uninformed)trades)and)pairs)trading)returns,)and)suggest)that)pairs)trading)return)is)compensation)for)providing)liquidity)to)the)excess)demand)from)uninformed)investors.)According)to)the)authors)the)market)with)uninformed)investors)is)a)market)with)limited)risk)bearing)capacity)and)will)therefore)compensate)provision)of)liquidity.)All)these)papers)are)an)inspiration)for)future)research)within)pairs)trading,)as)there)are)still)unanswered)questions)related)to)the)drivers)of)profitability)for)this)investment)strategy.))

4. Sources,of,risk,and,return,in,pairs,trading,A)substantial)part)of)the)pairs)trading)analysis)is)related)to)the)different)risks)the)strategy)faces.)Even)if)a)strategy)seems)to)yield)promising)returns,)the)manager)must)be)aware)of)the)sensitivity)the)portfolio)has)to)unexpected)events)or)unforeseen)changes)in)the)macro)environment.)This)is)even)more)important)for)a)leveraged)strategy,)and)the)proportion)of)leverage)in)the)portfolio)financing)should)be)a)factor)of)the)portfolio’s)sensitivity)to)different)

) 24)

risk)factors.)Furthermore,)the)accumulation)of)returns)can)be)a)direct)consequence)of)the)factor)exposure)the)portfolio)is)subject)to,)as)exposure)to)some)risk)factors)should)be)compensated.)Therefore)what)might)seems)be)abnormal)returns)might)actually)be)exposure)to)additional)risk)that)also)can)affect)the)performance)of)the)portfolio.))

4.1. Sources,of,risk,

An)investment)strategy)is)subject)to)several)types)of)risk.)It)is)therefore)crucial)for)the)investor)to)be)conscious)about)the)risk)exposure)of)the)portfolio,)so)it)is)properly)managed.)In)the)upcoming)section)we)dig)further)into)types)of)risk)we)consider)especially)relevant)for)pairs)trading.)We)separate)between)risks)the)investor)will)be)compensated)for)and)risks)that)threaten)the)performance)of)the)portfolio)but)offer)no)compensation)to)the)investor.)Arbitrage)risk)and)liquidity)risk)are)factors)of)the)former)category,)and)we)anticipate)these)to)be)two)important)factors)of)both)risk)and)return)within)pairs)trading.)We)also)elaborate)on)the)occurrence)of)short)squeezes)and)model)risk,)which)are)not)necessarily)sources)of)return,)but)still)substantial)sources)of)risk)for)statistical)arbitrage)strategies.)We)do)not)include)market)risk)since)the)portfolio)is)intended)to)be)market)neutral,)but)admit)that)a)pairs)trading)portfolio)are)likely)to)have)some)exposure)to)the)market.))

4.1.1. Arbitrage,Risk,

Arbitrage)risk)is)very)relevant)for)pairs)trading,)as)the)essence)of)pairs)trading)is)to)exploit)statistical)anomalies)or)arbitrage)opportunities.)The)term)arbitrage)risk)is)a)broader)term)that)contains)fundamental)risk)(Shleifer)and)Vishny)1997),)noise)trader)risk)(DeLong)et)al.)1990))and)synchronization)risk)(Abreu)and)Brunnermeier)2002).)Fundamental)risk,)in)the)context)of)pairs)trading,)is)the)risk)that)idiosyncratic)shocks)will)lead)to)a)permanent)change)in)the)relationship)of)the)two)stocks)in)a)pair.)A)company)can)for)instance)divest)part)of)its)business,)change)its)core)focus,)be)taken)over)by)another)company)or)be)subject)to)drastic)changes)in)its)business)environment.)A)good)example)from)our)own)dataset)is)IKB)Deutsche)Industrie)Bank)in)August)2007.)IKB)suffered)huge)losses)and)was)put)under)administration)by)the)German)government.)This)led)to)a)loss)of)182%)for)a)single)pair)in)one)of)our)portfolios,)and)caused)the)worst)loss)suffered)by)a)single)pair)throughout)our)whole)trading)period)(Figure)2).)))

) 25)

Figure!2!

)According)to)Shleifer)and)Vishny,)it)is)very)difficult)for)arbitrageurs)to)diversify)away)such)risks.)For)pairs)trading)in)particular)it)can)be)difficult)to)find)a)sufficient)number)of)pairs)with)satisfactory)quality)to)make)a)large)and)diversified)portfolio.)Mitchell,)Pulvino)and)Stafford)(2002))also)address)fundamental)risk)and)show)that)not)even)negative)stub)values)are)risk)free)arbitrage)opportunities,)as)the)opportunity)can)fail)to)materialize)if)the)parent)company)or)the)subsidiary)defaults,)is)acquired)or)delisted.)For)the)pairs)trading)portfolio,)a)large)corporate)event)represents)a)significant)threat)as)it)can)change)the)nature)of)a)company)and)break)the)link)between)the)two)cumulative)stock)returns)in)a)pair.)This)will)result)in)permanent)divergence)in)the)normalized)prices)and)hurt)the)profitability)of)the)portfolio.))Noise)trader)risk)(De)Long)et)al.)1990),)in)the)case)of)pairs)trading,)concerns)the)possibility)of)further)divergence)due)to)the)presence)of)noise)traders.)The)behavior)of)noise)traders)is)impossible)to)predict,)and)their)actions)can)drive)prices)far)away)from)the)fundamental)value.)The)existence)of)noise)traders)is)supported)by)the)simple)idea)that)there)is)never)complete)consensus)about)the)value)of)an)asset.)Most)of)the)time)there)are)both)buyers)and)sellers,)thus)one)of)the)parties)must)be)wrong)about)the)value.)Even)if)the)arbitrageur)is)eventually)right,)noise)traders)can)force)prices)in)an)unfavorable)direction)and)force)the)arbitrageur)to)liquidate)his)positions.)Shleifer)and)Vishny)(1997))explain)that)the)presence)of)noise)traders)not)only)drive)prices)away)from)fundamentals,)but)also)delays)the)convergence)back)to)the)expected)value.)They)further)show)that)even)if)arbitrageurs)do)not)face)longCterm)fundamental)risk,)shortCterm)deviations)can)force)them)to)liquidate)positions,)even)when)

0)

0.5)

1)

1.5)

2)

2.5)

Pair!divergence!in!the!trading!period!

IKB) Krones)

) 26)

trades)get)more)profitable)in)expectation.)A)saying)from)Joseph)P.)Kennedy,)a)famous)investor)from)the)1920’s,)illustrates)how)noise)traders)can)play)a)role)in)the)market:)“You)know)it’s)time)to)sell)stocks)when)the)shoeshine)boy)tries)to)give)you)stock)tips”.)The)morale)of)this)saying)is)that)when)the)stock)market)has)attracted)enough)people)completely)clueless)about)financial)markets,)it)is)impossible)to)predict)the)direction)of)the)market)and)better)to)just)stay)away.)There)are)several)examples)throughout)history)where)its)seems)like)the)price)of)assets)have)been)driven)far)away)from)their)fundamental)values,)most)recently)with)mortgage)backed)securities.)))The)last)risk)type)of)arbitrage)risk)is)synchronization)risk)(Abreu)and)Brunnermeier)2002),)which)is)the)risk)that)arbitrageurs)delay)the)correction)of)the)mispricing)to)minimize)their)holding)costs.)A)small)number)of)arbitrageurs)are)unable)to)force)prices)back)to)fundamentals)by)themselves,)so)they)are)dependent)on)other)market)participants)to)help)correct)the)prices.)Thus)the)arbitrageur)risks)that)it)takes)time)before)the)mispricing)is)corrected)and)in)the)meantime)the)price)can)experience)even)further)divergence)before)it)is)possible)to)profit)from)the)arbitrage)opportunity.)Therefore,)a)pair)trade)is)risky)since)all)our)trades)are)liquidated)at)the)end)of)the)trading)period,)even)if)we)expect)prices)to)converge)at)some)point)in)the)future.)As)previously)mentioned,)Do)and)Faff)(2010))find)evidence)that)it)takes)longer)time)for)pairs)to)converge)during)the)period)2003C2009)than)earlier)periods,)and)this)is)consistent)with)the)idea)that)arbitrageurs)hesitate)to)correct)mispricing.)Additionally,)the)mispricing)must)be)significant)so)the)expected)profits)are)attractive)enough)for)the)arbitrageurs)to)incur)the)aboveCmentioned)risks.)))

4.1.2. Liquidity,risk,

Before)stocks)are)considered)eligible)for)pairs)trading)they)are)usually)screened)with)respect)to)liquidity)by)looking)at)daily)price)changes)and)trading)volume.)However,)we)cannot)be)certain)that)stocks)will)maintain)a)sufficient)level)of)liquidity)in)the)trading)period.)If)stocks)suddenly)experience)a)decline)in)liquidity,)we)risk)large)transaction)costs)when)we)enter)or)exit)the)positions)in)illiquid)stocks.)According)to)Brunnermeier)and)Pedersen)(2009),)market)liquidity)and)funding)liquidity)are)connected)and)mutually)reinforcing,)which)leads)to)liquidity)spirals.)These)liquidity)spirals)can)have)an)ambiguous)effect)on)the)pair)portfolio,)

) 27)

and)can)result)in)either)a)profit)or)a)loss)for)the)investor.)A)low)funding)liquidity)would)make)investors)more)reluctant)to)take)on)positions,)which)will)lead)to)lower)market)liquidity.)A)consequence)of)the)lower)market)liquidity)is)that)prices)become)more)volatile)(Brunnermeier)and)Pedersen)2009),)and)a)higher)volatility)can)lead)to)an)increase)in)the)crossing)frequency)of)the)stocks)in)a)pair,)which)is)considered)an)attractive)attribute)that)might)improve)the)profitability)of)the)portfolio.)However,)severe)liquidity)crunches)and)downward)spirals)can)also)lead)to)an)extreme)deviation)in)the)spread)of)a)pair.)Consequently,)the)portfolio)can)suffer)huge)losses)if)the)spread)does)not)return)to)its)expected)value)during)the)trading)period)or)the)investor)is)forced)to)exit)his)trades)due)to)margin)calls.)If)a)pair)is)expected)to)converge)in)the)long)term,)but)experiences)divergence)in)the)shortCterm,)arbitrageurs)can)be)forced)to)exit)their)positions)when)the)trade)is)at)its)most)promising,)if)funding)liquidity)is)scarce.)During)the)subCprime)crisis)banks)responded)to)the)decline)in)market)liquidity)by)further)increasing)funding)constraints)and)position)margins,)which)lead)to)a)selfCenforcing)downward)liquidity)spiral.)Ibbotson)(1999))finds)that)security)brokers)and)speculators)have)betas)exceeding)one,)and)this)helps)to)explain)why)capital)constraints)are)more)likely)to)be)hit)and)liquidity)is)more)likely)to)dry)up)during)periods)of)market)decline.)For)portfolios)that)rebalance)frequently)a)large)liquidity)buffer)is)needed,)as)the)portfolio)must)be)updated)constantly.)Furthermore,)rebalancing)is)often)most)needed)when)liquidity)conditions)are)poor,)so)a)sufficient)liquidity)buffer)is)extremely)important,)especially)in)the)years)where)funding)liquidity)is)low.)Acharya)and)Pedersen)(2005))discover)a)premium)for)holding)stocks)that)become)illiquid)when)the)market)becomes)illiquid.)Additionally,)they)find)that)investors)are)willing)to)pay)a)premium)for)stocks)that)stay)liquid)despite)a)decline)in)market)returns.)This)is)relevant)for)pairs)trading,)because)the)pairs)trader)sells)stocks)that)perform)relatively)well)and)buy)the)stocks)that)yield)relatively)poor)returns.)Consequently,)in)periods)of)market)decline)the)pairs)trader)can)earn)a)liquidity)premium,)because)he)ends)up)selling)liquid)stocks)at)a)premium)and)buys)illiquid)stocks)at)a)discount,)when)other)investors)run)towards)liquid)assets.)The)downside)is)that)these)stocks)can)experience)further)depreciation)in)value)and)incur)high)transaction)costs.))

) 28)

4.1.3. Short,squeeze,

The)pairs)trading)manager)has)a)large)amount)of)short)positions)and)can)suffer)large)losses)if)one)of)the)short)positions)experiences)a)short)squeeze.)A)short)squeeze)occurs)when)the)supply)for)a)stock)is)limited)and)there)is)excessive)demand.)The)excessive)demand)will)push)prices)up,)and)the)probability)that)investors)with)short)positions)are)forced)to)liquidate)are)greatly)increased)as)they)get)larger)and)larger)margin)calls.)Since)a)pair)trader)is)typically)leveraged)this)is)definitely)a)possible)scenario)for)the)pairs)trader.)A)short)squeeze)typically)happens)to)small)cap)stocks,)but)one)of)the)most)famous)examples)of)a)short)squeeze)happened)to)one)of)the)world’s)largest)car)manufacturers.)As)illustrated)below)(Figure)3),)Volkswagen)almost)fiveCdoubled)its)stock)price)within)two)days)during)October)2008.)))Figure!3!

)At)the)end)of)the)October)2008,)several)hedge)funds)was)forced)to)liquidate)their)short)positions)in)the)Volkswagen)share)after)they)learned)that)Porsche,)the)car)manufacturer,)had)a)stake)of)more)than)75%)in)Volkswagen.)The)proportion)of)shares)owned)by)Porsche)accounted)for)almost)every)single)circulating)stock)in)the)market,)and)after)it)was)public)information,)Porsche)could)demand)whatever)price)they)wanted)to)sell)Volkswagen)stocks)to)the)unfortunate)hedge)funds.)The)funds)suffered)losses)amounting)to)several)billion)Euros,)and)illustrate)the)crucial)consequences)of)being)caught)in)a)short)squeeze)(Krstic)2009).))

0)

5000)

10000)

15000)

20000)

25000)

30000)

35000)

1/1/08) 2/1/08) 3/1/08) 4/1/08) 5/1/08) 6/1/08) 7/1/08) 8/1/08) 9/1/08) 10/1/08) 11/1/08) 12/1/08)

Volkswagen!Short!Squeeze!

VW)C)Total)Return)Index)

) 29)

4.1.4. Model,risk,

Model)risk)is)the)risk)that)our)model)is)not)performing)the)task)that)it)is)built)for.)In)our)case,)this)would)be)the)risk)that)the)parameters)used)and)the)model)we)built)is)not)able)to)identify)pairs)that)move)together)in)the)future.)A)typical)explanation)could)be)that)our)model)is)based)on)the)wrong)assumptions.)For)instance,)that)we)should)have)used)a)longer)formation)period,)because)12)months)is)simply)too)short)a)time)to)identify)coCmovement)between)stocks,)or)that)our)trading)period)is)so)short)that)the)pairs)do)not)get)sufficient)time)to)converge.)Another)source)of)model)risk)would)be)that)the)zero)crossing)or)the)minimum)distance)parameters)are)unable)to)identify)profitable)pairs.)We)have)no)guarantee)that)the)information)inserted)in)the)trading)model,)in)our)case)the)pair)identifying)metrics,)are)informative)factors)for)future)returns.)There)might)be)other)metrics)that)are)much)better)at)identifying)pairs,)but)are)yet)to)be)discovered.)The)pair)pictured)in)the)graph)below,)incur)a)loss,)even)though)it)looks)promising)in)the)formation)period.)The)divergence)between)the)prices)in)the)trading)period)(starting)01.01.2003))shows)that)our)ability)to)identify)pairs)that)move)together)is)by)no)means)perfect.))Figure!4!

)All)models)that)predict)future)outcomes)are)subject)to)uncertainty,)so)past)success)is)no)guarantee)for)future)success.)Our)model,)presented)in)section)5,)is)for)instance)not)able)to)foresee)bankruptcies,)takeovers)or)bailouts,)and)these)are)one)of)the)most)important)contributors)to)negative)returns)in)our)portfolio.))!

0.3)0.5)0.7)0.9)1.1)1.3)

Diverging!pair!

Deutsche)Post) TUI)

) 30)

4.2. Sources,of,return,