| RETURN TO Public Disclosure Authorized WVV'itT HIN 1 P … · The Banlk G,ounp does not ace-pt...

91

| RETURN TO REPORT DESK WVV'itT HIN U,l~T O~NE WEEK 1 P AITUM IIONAL BANK FOR RECONSTRUCTION NNe *i1'iTi3?T A PT A T T7 nEl' rT A OOCITAATIOiLou IN1E 1Rd¶'4A tII0'JINIiL Li.VE.Arv ILi O Ail J Not For piuhbir IM Te Report No. 165-IN SURVEY OF COMMERCIAL VEHICLE INDUSTRY INDIA A Background Paper in connection with the Appraisal of the Eighth Industrial Imports Credit May 16,j 197 3 Industrial Projects Department This report was prepared for official use only by the Bank Group. It may not be published, quoted of cited without Bank Grouinp authorLyation. The Banlk G,ounp does not ace-pt respoon-sb. f.t. ehnI accuracy or completeness of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of | RETURN TO Public Disclosure Authorized WVV'itT HIN 1 P … · The Banlk G,ounp does not ace-pt...

| RETURN TOREPORT DESK

WVV'itT HIN U,l~TO~NE WEEK 1 P

AITUM IIONAL BANK FOR RECONSTRUCTION NNe*i1'iTi3?T A PT A T T7 nEl' rT A OOCITAATIOiLouIN1E 1Rd¶'4A tII0'JINIiL Li.VE.Arv ILi O Ail J

Not For piuhbir IM Te

Report No. 165-IN

SURVEY OF COMMERCIAL VEHICLE INDUSTRY

INDIA

A Background Paper in connection with theAppraisal of the Eighth Industrial Imports Credit

May 16,j 197 3

Industrial Projects Department

This report was prepared for official use only by the Bank Group. It may not be published, quotedof cited without Bank Grouinp authorLyation. The Banlk G,ounp does not ace-pt respoon-sb. f.t. ehnI

accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Currency Equivalents as at Ma 11, 1973

1 US $ Rs 7.6*1 Rupee = US $ 0.131 Million Rupees US $ 132,000

* India has not yet declared a new par value following the devaluation ofthe US dollar. The Rupee is officially valued at a fixed Pound Sterlingrate; and, as the Pound is now floating relative to the US dollar, theUS dollar-rupee exchange rate is subject to change. Conversion in thispaper were made at Rs 7.9 to US $ which was the prevailing rate at thetime of preparation of this report.

Time Spans

The Indian Government financial year runs from April 1to March 31. In this report the financial years arewritten as, for example, 1972/73 designating the financialyear from April 1, 1972 to March 31, 1973.

Longer intervals of time are written as, e.g., 1970-72(two year interval), 1970-1978 (eight year interval).

Abbreviations

TELCO - Tata Engineering and Locomotive Co.DGTD - Directorate General of Technical DevelopmentCKD - Completely Knocked-Down UnitSKD - Semi-Knocked-Down UnitAU License - Actual User import license (issued to

manufacturers based on established levelof consumption, not transferable)

REP - Import Replenishment Entitlement (importlicense issued to exporter, total valuein any year is based on percentage ofexport (sales)

SURVEY OF COMMERCIAL VEHICLE INDUSTRY

INDIA

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS i -

I. INTRODUCTION 1

II. SECTORAL FRAMEWORK 2A. History, Government Policy and Institutions 2B. Industry Structure 4C. Fixed AssetsD. OwnershipE. Employment and Capital Intensity 6F. Vertical Integration 7

III. ANALYSIS OF PERFORMANCE 7A. Production, Capacity Utilization and Market Share I

1. Medium/Heavy Vehicles 72. light Commercial Vehicles 83. Three Wheelers 94. Diesel Engines 9

B. Plant Operations r

1. Product Engineering 102. Manufacturing I3. Materials Management 124. Marketing 125. Financial Controls and Reports 126. Organization and Management 12

C. Indigenization Trend 13D. Financial Performance 14

1. Prices 142. Cost Structure 153. Profitability, Productivity and Financial Struecture 16

E. Economic Costs and Benefits 191. Medium/Heavy Vehicles 202. Light Vehicles 213. Jeeps and Jeep Trucks 22

F. Exorts 22

TV. A FPANSTON PLANS 2LA . Medium/Heavy Vehicles 2BR. T.ight VahicleR 25

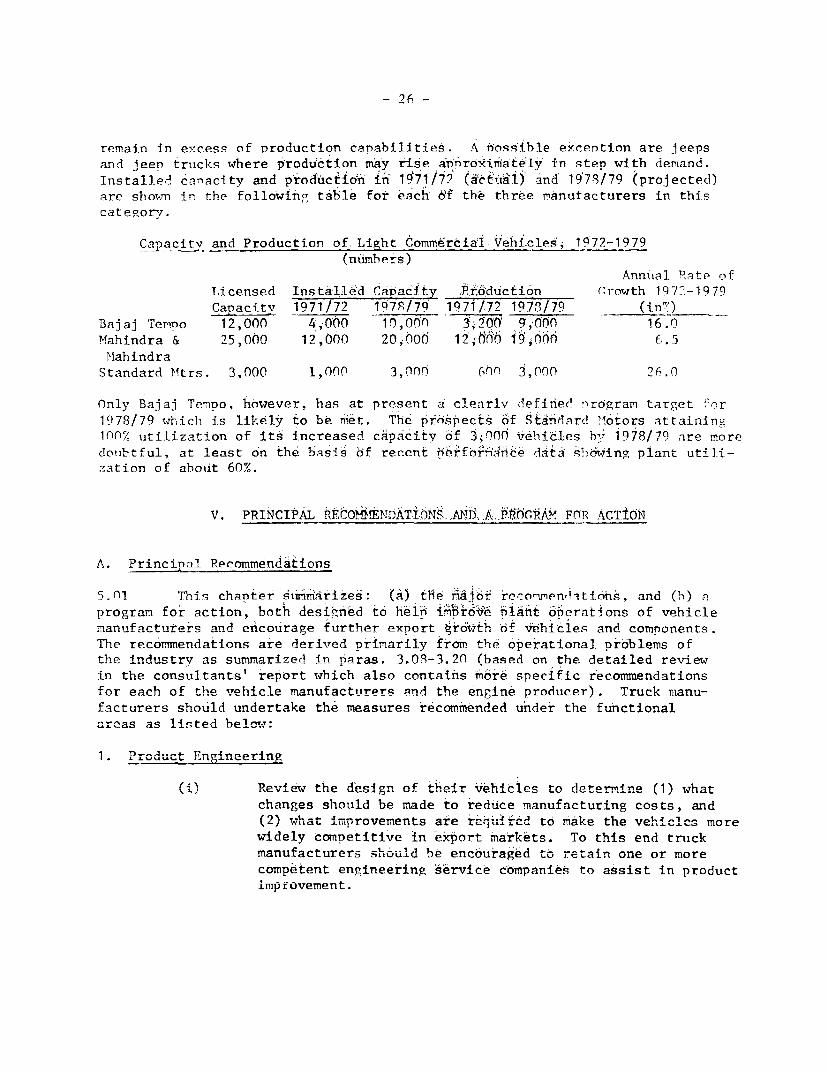

PpRTMrTPAT. RERMMMFMlATTOUR ANM A PROr'RAM FOR AGTTON 26A. Principal Recoimmendations 26

1. Product Rnginreering 26

2. M7ianufacturing 27

TABLE OF CONTENTS, (CoNT.)

3. Materials Management 274. Marketing 285. Financial Controls and Report 286. Organization 28

B. A Program for Action 281. Role of Government 282. Role of Vehicle Manufacturers 303. Joint Effort - Government and Industry 30

Annex 1/

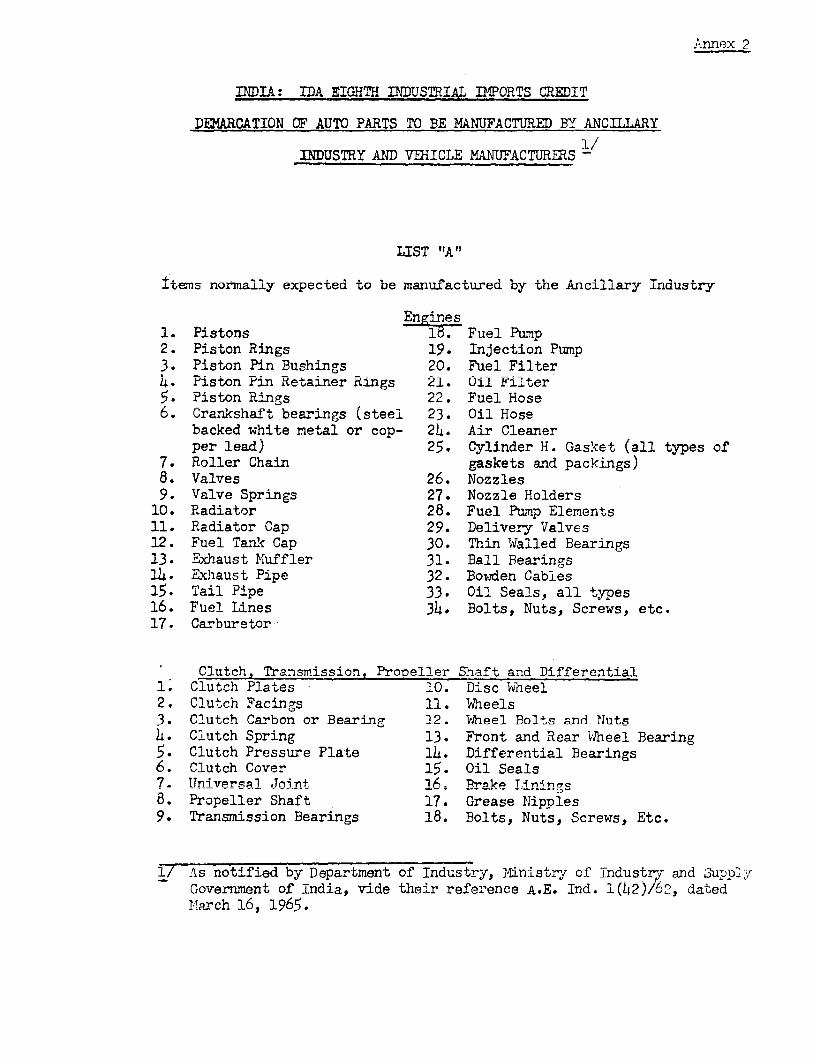

1 Vehicle PonunIt1inn 19 4R-19722 Demarcation of Component Production by Ancillaries

3 Note on Indian Export Promotion Incentives4 World Truck and Bvs Produceion rk%iy rompa^ 19Q655 Licensed Capacity, Installed Capacity and CaDacity

TTHiliz,atio n - Meedium/heav y Conm.aerclal Vehicles,1964-1979

6 Licensed CapacIty, Installed Capacity and CapacItyUtilization - Light Commercial Vehicles and Jeeps1966-79

7 Plant Operations Rating SystemR Progressc of TnAdigemn^,, Contont-

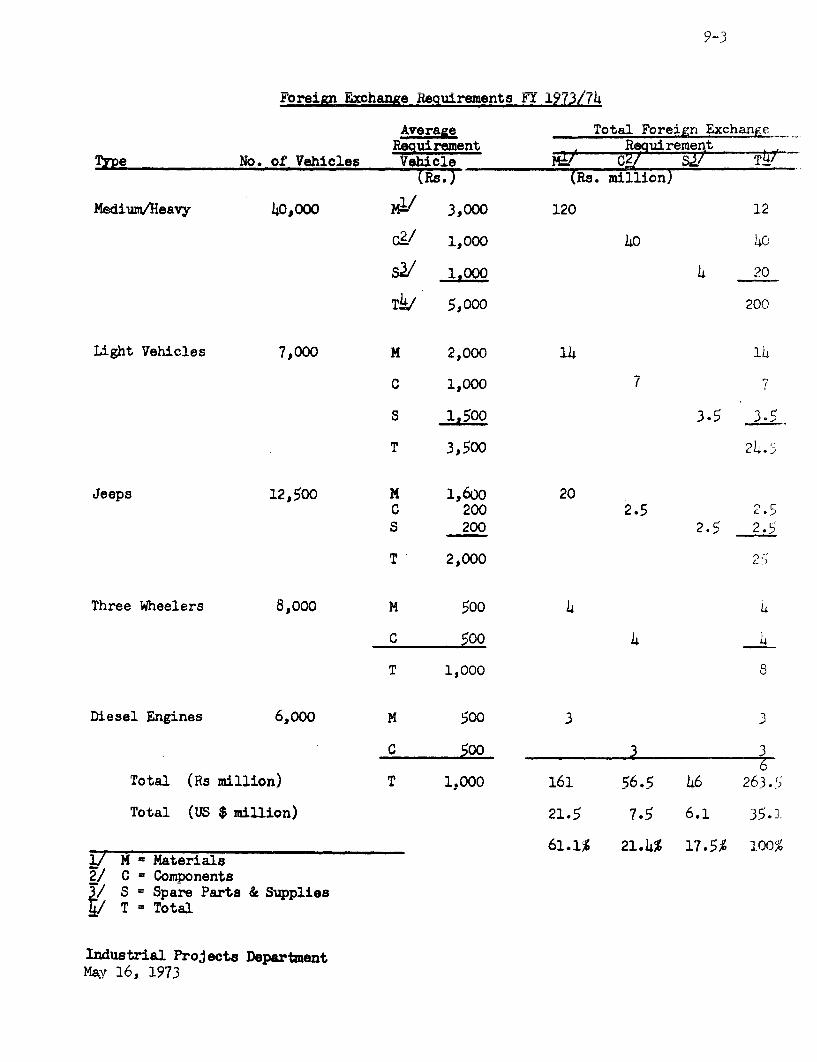

9 Foreign Exchange Requirements10 Fir.ancial Data and AnlysIs11 Economic Analysis12 E Mr Ma:ke Stutr - Sources uEyo LoJ)an

Destination (countries)13 DomestIc 1r-ces, Ex-dou r and nReai zatIon

Commercial Vehicles, 1971/7214 xoLrs o Uf Co,-[U,eIrcIalI _ Vehicles andU Components, 19' 115 Export Performance of Manufacturers, 1969-197216 Demand Forecast17 Actual and Projected Production, 1964-1979

Map Locations of Commercial Vehicle Manufacturers

! Additional data is contained in a separate report entitled: India,Commercial Vehicle Sector, General Appraisal (Vol. 1) and India,individual Truck Manufacturers, General Appraisal (Vol. 2) datedJanuary 15, 1973 and prepared by Raymond E. Danto Associates, Inc.,Detroit, U.S.A., consultants. Tne consultants! report is availablefrom Mr. Goderez of the Industrial Projects Department on special re-quest only and since it contains confidential data on each of thecommercial vehicle manufacturers its use is restricted to authorizedpersonnel within the Association and Indian Government officials.

SURVEY OF COMMERCIAL VEHICLE INDUSTRY

INDIA

SUMMARY AND CONCLUSIONS

J. Silnce 1964, the International Development Association (IDA) hasextended seven credits to India totalling US$680 million for the import ofmaterials, components, spares and some balancing equipment for selected in-dustrial sectors. The purpose of these credits has been to increase capacityutilization and operating efficiency and reduce manufacturing cost by helpingto provide a timely flow of needed imported inputs at competitive world prices.In its past appraisals, -DA had given about equal attention to each of the 5to 12 industrial sectors variably covered but these appraisals were evidentlynot sufficiently detailed to allow meaningful recommendations on specificmeasures regarding sectoral policies and improvement of industrial performance.To achieve this goal it was recognized that more intensive sectoral surveyswere required; consequently this report on the Indian Commercial Vehicle In-dustry is the first of a series of surveys that IDA intends to undertake inclose cooperation with the Indian Government in the course of the next fewyears.

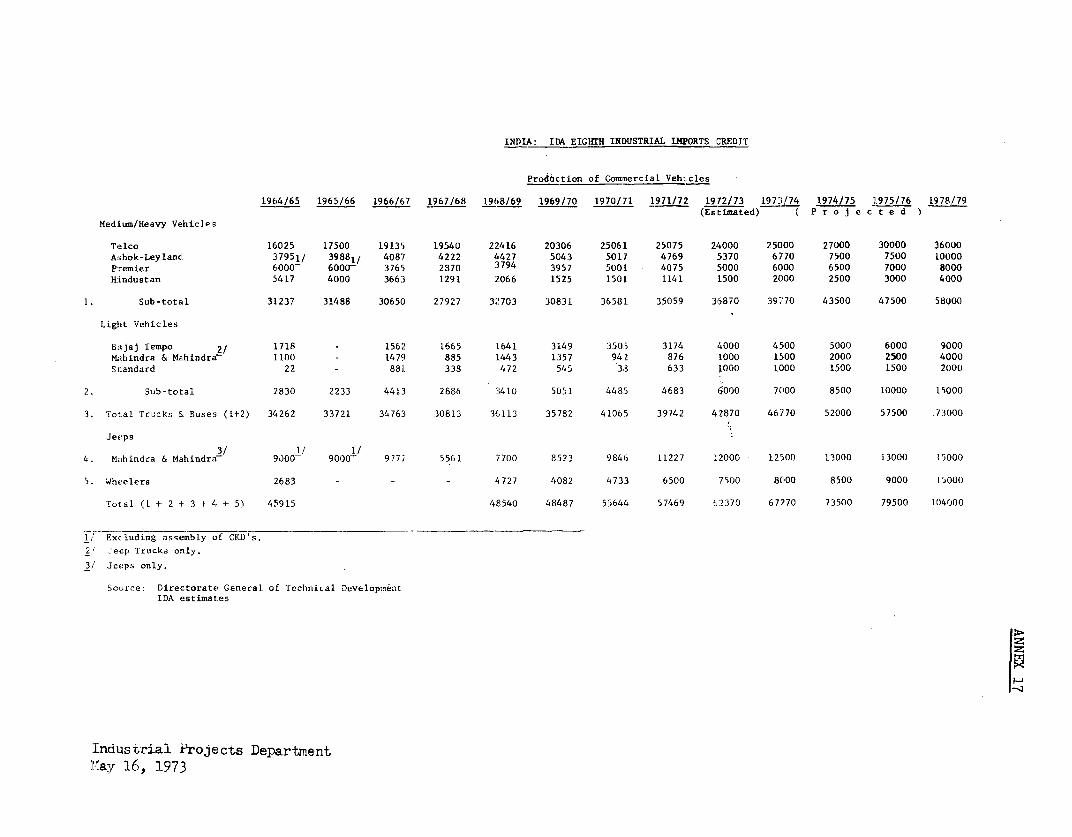

ii. The commercial vehicle industry, one of the highest priority sec-tors in India, has been included in every IDA industrial imports credit for acumulative allocation of about US$139 million, equal to 20.47 of the totalcredits granted. Prior to 1952, production was based entirely on the assemblyof imported components. In the relatively short period of 20 years, the in-dustry has converted to indigenous production and today only 8 to 10% of theex-factory price of a vehicle corresponds to foreign exchange cost of directimports. During the same 20 year period, production in terms of numbers ofvehicles grew at an average annual rate of 18% and current production is about60,000 per year in all vehicle sizes; by 1978/79 annual production is prolectedto reach 100,000. Gross product value currently amounts to Rs. 2 billion perannum (US$255 million) and accounts for about 8% of the total production ofengineering goods in India.

iii. There has also been an encouraging beginning in exports of vehiclesand parts which have increased from virtually nothing in the mid-1960's to anestimated Rs. 150 million (US$20 million) in 1972/73 and are expected to growfurther to Rs. 300 million by 1978/79. Over the last few years exports aver-aged 5.5% of gross product value and have earned about half of the foreignexchange expended in direct imports. It is worth noting that if indigenousdeep-draw steel sheets were available domestically, this industrv would alreadybe earning more foreign exchange than needed for direct imports.

iv. While the efficiency of the industry has imnroved, Indian trurksare still priced 10 to 20% higher than foreign models if ex-factory prices arecompared. This price handicap and the eenerally outmoded designs of Indiantrucks have been major constraints inhibiting export growth. Exports dependon cash and other incentives to comnensate for the 30 to 35 price discount(below domestic f.o.b. vehicle prices) at which exports must be made to placeorders and even then epnorts are on the whole limited to special trading sit-

--4 -r

uations where bilateral agreements and Indian export credit are able to inducebuyer acceptance. Nevertheless, compared to the opportuni;ty cost of Lorelgnexchange, such exports are economic. A further increase in cash incentiveswould not be economically justified and therefore only those incentives andmeasures should be considered which contribute to reduction in manufacturingcosts and improved product quality.

v. The performance of the sector in terms of efficiency of piant op-erations, capacity utilization, earnings and financial strength, degree ofinternational competitiveness both in quality and price and export performance-a_ries widely among the manufacturers. For example, while capacity utilizationof the industry is 71%, this average hides the fact that in the medium/heavyvehicle range, TELCO, the largest and most efficient manufacturer, is operatingat 104% of installed capacity and Hindustan Motors, the least efficient produc-er, at only 8%. Other manufacturers are operating between 60 and 80% of capa-city. TELCO also accounts for more than 70% of the industry's exports. Profitsbefore taxes and interest varied from 7 to 17% of total capital employed in1971/72 and have been increasing at modest rates since 1969 when prices weredecontrolled. However, since finished vehicle prices have risen at a slowerrate than the cost of external inputs (bought-out materials and parts), it maybe concluded that overall plant efficiency -- measured by labor and capitalproductivity -- has generally improved.

vi. Despite the sector's past growth and other achievements, there issubstantial room for improvement. Only TELCO and Bajaj Tempo have successfullybeen implementing a methodical plan of expansion and improvement based on com-petent management and adequate resources, but even these relatively efficientmanufacturers could better their performance in certain functional areas. Allother firms, especially Hindustan Motors and Simpson (the latter the only in-dependent producer of engines) need considerable overall improvement, particu-larly in product planning and engineering, manufacturing methods, marketing,financial controls and corporate organization and capabilities. Improvementin plant operations is the area where a major effort is required and whereimportant cost reductions could be rapidly achieved.

vii. In castings, forgings and machined components and assemblies forthe vehicle industry. India appears to be already internationally competitivein price and quality, at least among a number of more efficient ancillary pro-ducers. There is a worldwide shortage of these comoonents and large vehiclemanufacturers in developed countries are searching the world for new sources.With organized promotion, it should be feasible to develon significant exnortsales of Indian components to the developed countries. A longer range buteqnutll fpeasble goal wtould he to tepn tin exnnrts of nmnlpete vehicles tounderdeveloped countries parallel with a drive to increase operational effi-ciency and reducesa nots. neveunnitna count-rieq, -with onditinns szimilar to

India's -- overloading of vehicles, substandard roads and severe climate -- area natural market for Tndian uehicles whirh Aar kno.nn to be able to stand upwell to extraordinary stresses.

- iii -

viii. The Government has accepted proposals for a program of action to

improve plant operations with a view to help accelerate the development of the

industry and export growth. Main responsibility for the action program must

rest with the vehicle manufacturers. The Government's contribution to the

program would consist of policy and procedural measures; these would involve

marginal liberalization of import licensing, support in establishing overseas

trade development centers to foster exports of components, and more liberal

interpretation of the rules governing foreign collaboration agreements and

technical assistance contracts.

I. INTRODUCT1UION

1.01 In May 1972, in presenting the Seventh Industrial Imports Projectin India, the Executive Directors of the International Development Association(IDA) were informed that IDA, in close cooperation with the Indian Government,would thenceforth carry out intensive surveys of the priority sectors that hadbeen receiving assistance under the Association's industrial import credits.The purpose of these surveys would be: (a) to establish in the Bank a betterunderstanding of sectoral problems, constraints and potential for growth and(b) to suggest possible remedies for improvement of industrial performance.

1.02 In its past appraisals, IDA gave equal emphasis to each of the 5to 12 sectors variably covered by the seven credits approved between 1964 and1972. This approach has adequately served the purpose of producing whatmight be termed macro-evaluations of acceptable depth for the sectors. But ithad also become increasingly apparent that meaningful recommendations on morespecific measures affecting sectoral policies and industrial performance wouldhave to be supported by more reliable data and more incisive analysis. Fur-thermore, since it was clearly beyond the capacity of any reasonably-sizedmission, time schedule or budget to undertake intensive surveys of severalsectors simultaneously it was recognized that a new appraisal methodology wasrequired.

1.03 The appraisal of the Eighth Credit therefore was implemented intwo steps: (a) an intensive survey of the commercial vehicle and agriculturaltractor industries, two categories deemed of high priority, and (b) a reapprais-al of the remaining IDA industries based on a limited field survey and theupdating of performance data. In each future appraisal, it is planned tosurvey intensively one or two of the other IDA industries, so that in a cvcle ofthree to four years all will have been appraised in depth. This report reviewsthe commercial vehicle industry. 1/

1.04 Essential to the successful imnlementation of the intensive reviewwas the need to incorporate in it a higher level of technical expertise thanhad been the nrantiep in nrior missions. After cnnsiAdratinn of a nmber of

international consulting firms, the services of R.E. Danto Associates, Inc.Of Detroit (USA) were contracted. The company's evnertricp res-ts on lnng year

of experience in operations and management plus consulting services to leadingtrurk and trantor manufactuirern in the TJ=S= anti ahroad.

1.05 The renoret /- reflecr.s the findings of the mission 1n Tndia in

September/October 1972 which consisted of Messrs. Goderez (Chief) andIskander of the Indtrl e De_artmentnd.Rindn- atnl Po - n- ent nA -- P nnt a

D. Rowe, consultants. It is based on a comprehensive questionnaire returnedby1 all -om nrcial *re'h4icle ma -nufturers -ror to t h te- arrival of the m.issior

in India; visits to all major and most of the smaller plants; and discussionswith company managements a.d Goverr-met officials. A short follow-up mission

1/ A similar survey for the agricultural tractor industry is attached tothe President's Report.

2/ This report was prepared by Messrs. Goderez and Iskander of the IndustrialProjects Department.

- 2 -

took place in January 1973 to fill some data gaps but more importantly to re-view with the Government the major findings and recommendations for action ofthis report, to which the Government reacted favorably. The excellent coop-eration extended to the mission by Government officials and company managementsand staff is highlv appreciated! without the indiemnous i.puts,amanngfulreport could not have been prepared.

TT, SCETOR.41. FRXI..EWRK

A. History, Government Policy and Institutions

2.01 Manufacture of commercial vehicles in India is of rather recentorigir.; until tshe early- .19°50's the industLy was subst LantLIa'L'Ly an assemblLoperation importing partially or completely knocked down (CKD's) units orfinished -eh_4cles. imp;or-s in all fo.-msL were tabout 9 ,500 vehicles in i95i,the year in which the Government decided to establish indigenous manufactureo-f vehi4cles. At the -'me there were 12 vehicle assembly piants in india ofwhich only two (Hindustan Motors and Premier Automobiles) had progressed tothe point of local manufacture of some com,lponents. In 1953 the Governmentdecreed that all firms without a definite timetable for progressive domesticmanufacture of components should cease operations and declared the productionof commercial vehicles a priority industry. 11 The remaining producers weregiven suLfficient foreign exchange to meet their tooling needs. Furthermore,to offset the increases in cost anticipated with domestic production of partsand componients, tne Government lowered the duties on some items still permittedto be imported.

2.02 By 1956 there were seven surviving manufacturers of commercialvehicles and one manufacturer of diesel engines; of these, four produced trucksof medium to heavy range (5 tons and above), and one each produced light com-mercial vehicles, jeeps and jeep trucks and three-wheelers. As a result ofthe Government policy of restricting imports and promoting local manufacture,indigenous production increased rapidly to about 20,000 vehicles in 1956/57with a local content of about 50%.

2.03 Following the foreign exchange crisis of 1956/57, import controlswere intensified and imports of parts and components were banned whenever theGovernment was satisfied that adequate domestic capacity existed. Productionfell by about 7% in the following year (1957/58). Because of unsatisfied de-mand, price controls and vehicle allocations were instituted. This situationpersisted until 1964/65 when production reached 46,000 vehicles. The recessionof the mid-sixties, however, put an end to the seller's market, production

1/ Priority industries are listed in the annual publication "Import TradeControl Rules and Procedures" and are entitled to more favorable treatmentthan non-priority industries under licensing regimes. In 1972/73. thiscategory was comprised of 59 industries, including all IDA sectors.

-3-

stagnated and some tirms which had been selling poor quality products suffereda marked decline in demand. It was not until 1970/71 that production and de-mand recovered to pre-recession levels.

2.04 Production in all sizes including 3-wheelers was reported at 57,400vehicles in 1971/72 and estimated at 62,900 for 1972/73, implying an annualrate of growth of 18% over the last two decades. Though still small by U.S.and European standards, the Indian market for commercial vehicles is the secondlargest in Asia, next to Japan, and fourth among the developing countries afterBrazil, Spain and Argentina. The registered number of commercial vehicles hasrisen from 128,000 in March 1951 to an estimated 565,000 at the end of 1971/72broken down as follows: trucks - 340,000; buses - 100,000; jeeps - 87,000

and three-wheelers - 38,000 (Annex 1).

2.05 During the last two decades the principal instruments used by theGovernment to promote industrial development have been the industrial licensingand import licensing regimes. Failure to meet targets for "indigenous content"could result in significant delays or refusal of license applications for im-ports of parts and materials. During the 1960's indigenous production of ve-hicle components started in virtually all categories. The pressure towardsincreased indigenization, however, initially led vehicle manufacturers to under-take in-house production of parts contrary to the intent of the Governmentwhich was to encourage production by ancillary plants.

2.06 In 1965, the Government formalized its policy of encouraging growthand diversification in the ancillary industries by restricting a series of itemsto production only by ancillaries (subject to considerations of quality, deli-very and price) while permitting other items to be produced by both ancillariesand vehicle manufacturers (Annex 2). Vehicle manufacturers already producinggoods reserved to the ancillary industry could continue operations but werenot permitted to expand. These policies -- import restrictions (banned list)tngether with the list of nroducts reserved to the ancillaries -- providedstrong protection to potential entrants into the automotive ancillary industryand rapidly increased the indigenous content of commercial vehicles from about50% in the mid-1950's to close to 100% in the early 1970's (disregarding im-port content of botught-out ancillary components and materials).

2.07 iultanisly, in the 1960's the Government began to encourageexports through a number of incentive schemes. Until the 1966 devaluation,these consisted of import entitlements and direct tax concessions,, both tied

to export performance. Following the devaluation, new incentive schemes wereintroduced t1 including duty drwback; cash assistance; import replenishmententitlements; supply of steel at international prices; and sales tax exemption.The drawback system is a cash payment designed t-o compensatP firms for customqand excise duties paid on its inputs and averages about 12-16% of the f.o.b.value of th1e exportedAvehicle. Cash assistance re-resents a payment eqlual to

a specified percentage of the f.o.b. value of exports. It is meant 2/ to"comer.sat-e exports flor the te-.,porar; han.d caps th-at ste-" from transT tional

1/ Export incentives are briefly described in Annex 3.2/ Export Policy Resolution 1970, para. 14, page 7.

-4-

difficulties iniherent in a developing economy and to alleviate the disadvantages

arising from India's fiscal policies or tariff barriers in developing countries".

The rates of cash assistance are 251% for commercial vehicles and 20% for jeeps.

Import replenishment entitlements (REP's) are special import licenses issued

to the exporter in addition to the Actual Users import licenses; for commerc-'l.

vehicles REP's are issued in an am,ount equal to 20% of the f.o.b. value of

exports. The advantages of the REP's over Actual Users licenses are: (1)

free foreign exchange (Actual Users licenses are primarily issued against bi-

lateral credits); (2) somewh4at less riaiditv in applying the constraints of

the banned list; (3) transferability within the same industrial sector;

REP's can com ^nd a premium of about 50% of the nominal value when sold.

B. ILrdustry Structu,-e

2.08 In. term of the nuiMber of com.anies involved, the rcommercial vehicle

sector has changed very little since the mid-1950's. Only two additional firms

have appeared -- Bajaj Temtpo (in 1959) and Ba4aJ Auto (in 1960) Tb. follosirn

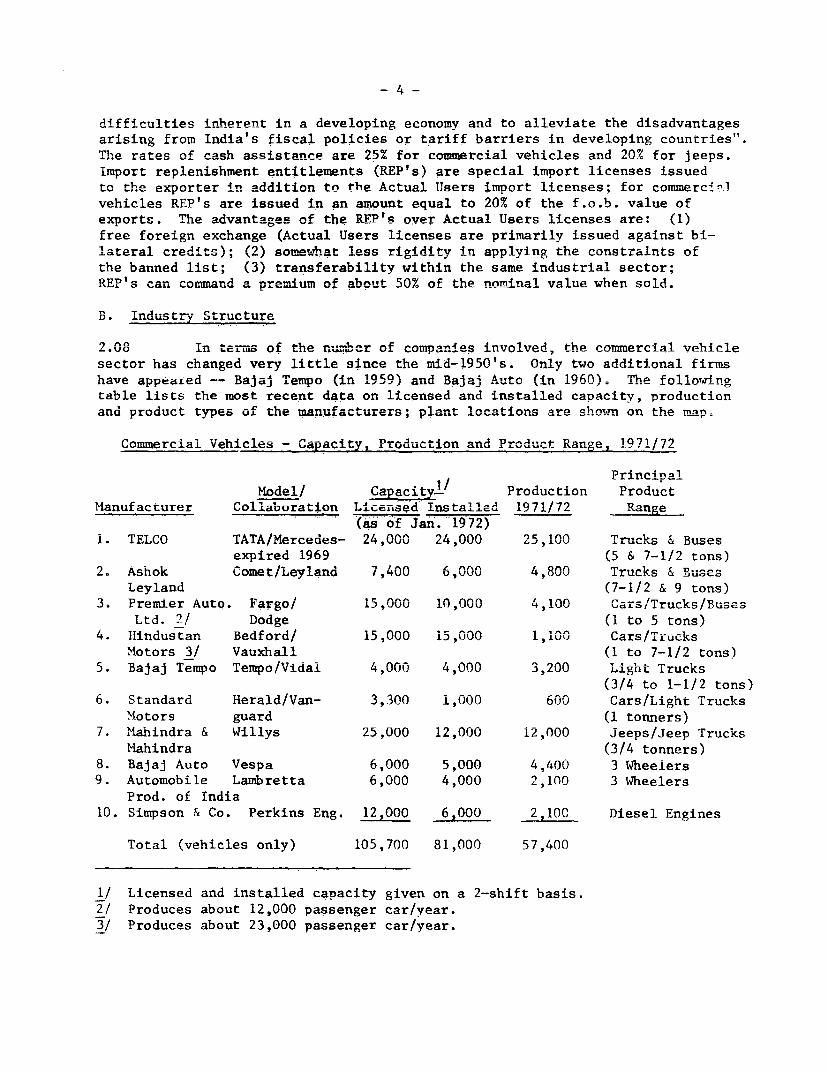

table lists the most recent data on licensed and installed capacity, production

and product types of the manufacturers; plant locations are shown on the mqp.

Commercial Vehixcles - Capacity, Production and Product Range, 1971/72

Principal

Model/ Capacity! Production Product

Manufacturer Collaboration Licensed Installed 1971/72 vae

f Jan. 1972)

i. TELCO TATA/Mercedes- 24,000 24,000 25,100 Trucks & Buses

expired 1969 (5 & 7-1/2 tons)

2. Ashok Comet/Leyland 7,400 6,00u 4,800 Trucks & Buses

Leyland (7-1/2 & 9 tons)

3. Premier Auto. Fa go/ 15,000 10,000 4,100 Cars/Trucks/Buses

Ltd. 2/ Dodge (I to 5 tons)

4. Hindustan Bedford/ 15,000 15,000 1,100 Cars/Trucks

Motors 3/ Vauxhall (1 to 7-1/2 tons)

5. Bajaj Tempo Tempo/Vidal 4,000 4,000 3,200 Light Trucks(3/4 to 1-1/2 tons)

6. Standard Herald/Van- 3,300 1,000 600 Cars/Light Trucks

Motors guard (1 tonners)

7. Mahindra & Willys 25,000 12,000 12,000 Jeeps/Jeep Trucks

Mahindra (3/4 tonners)

8. Bajaj Auto Vespa 6,000 5,000 4,400 3 Wheelers

9. Automobile Lambretta 6,000 4,000 2,100 3 Wheelers

Prod. of India10. Simpson & Co. Perkins Eng. 12,000 62000 2,10C Diesel Engines

Total (vehicles only) 105,700 81,000 57,400

1/ Licensed and installed capacity given on a 2-shift basis.

2/ Produces about 12,000 passenger car/year.3/ Produces about 23,000 passenger car/year.

- 5 -

Excludina diesel enaines, total nroduction in 1971/72 of 57,400 units renre-sented an ex-factory value estimated at about Rs. 1,940 million, accountingfor 8% of all engineering goods pnrduction in the organized sector (Rq 25,nn0million) and about 2.7% of all industrial production. With the exception ofTELC0, which accounts for over 40% of the total output (in nu mbers) and Ma-hindra & Mahindra with 20% of the total, the scale of operations is very small

Fy developed count.Lty standards Aex 4).

2.09 The npay.load range of co.merciai vehicles has changed o tim-

Up to 1955 almost the entire fleet consisted of light trucks of up to 3-toncapacity, but between 1955 and 1965 demand shited to 5-t-on (medium.., and si.c

then to 5-7-1/2 ton trucks. Both because of the shortage of trucks and therapidly increasing Uurde, ol taxes andu levies that t-he IndA4an road transport

system has to bear, overloading is common. Trucks generally run at load levelsabout 25/o above uianufacturersU recuLLuLenUat.Lons and often higher. Ll..e resultingwear and tear, further aggravated by sub-standard road conditions, makes majoroverhauls necessary at much shorter iLnterLva'Ls than 'Ls the practiLce iLn developUeudcountries and truck life is reduced. Trucks and buses are mainly diesel powered(85%o or ene total production) and are prouuceu in Uothi 4 X 2 and 4 A 4 drive

versions. Total installed capacity and production for 1971/72 for the varioustypes of vehicles are summarized below from Annexes 5 and 6.

Installed Capacity and Production by Vehicie Type, 1971/72

Type Installed Capacity ProductionMedium/Heavy Vehicles 55,000 67.9% 35,100 61.2%Light Vehicles 7,000 8.6% 4,600 8.0%Jeeps 10,000 12.5% 11,200 19.5%Three Wheelers 9,000 11.0% 6,00 11.3%

Total 81,000 100.0% 57,400 100.0%

C. Fixed Assets

2.10 For the automobile and commercial vehicle sector combined, fixedassets totalled nominally about Rs. 1,300 million (US$163 million) in December1971, of which Rs. 350 million were in buildings and Rs. 950 million in machinesand equipment. No separate figures are available for commercial vehicles, butit is estimated that fixed assets devoted to commercial vehicle manufacturewere about Rs. 900 million (US$117 million). This figure underestimates thereal market value of the assets, partly because of price increases which haveoccurred since investment and partly because much of the investment in thecommercial vehicle industry took place from 1954 to 1964 prior to the 1965 de-valuation. Total capital employed in the commercial vehicle industry is esti-mated at about Rs. 1,600 million, of which Rs. 900 million is fixed capitaland Rs. 700 million working capital.

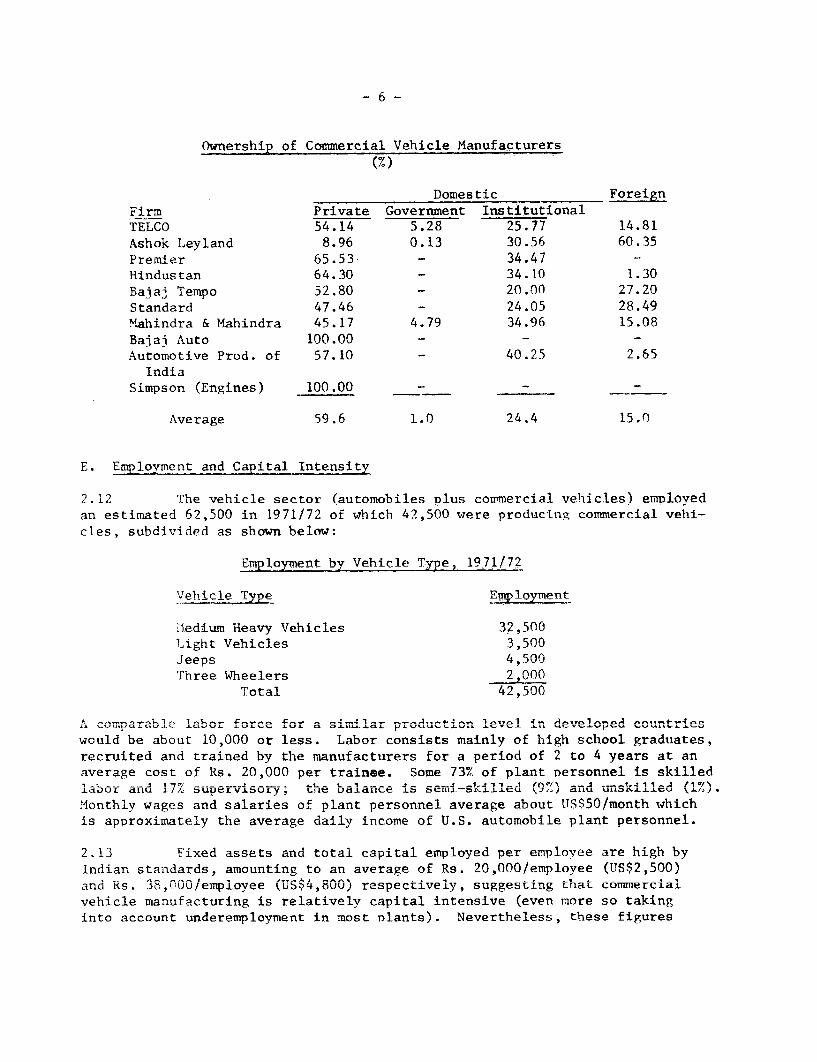

D. Ownership

2.11 Equity participation in the commercial vehicle sector is about 85%domestic and 14% foreign with the former subdivided into 60% private, 1%government and 24% institutional (banks and insurance companies) as shown inthe following table:

- 6 -

Ownership of Commercial Vehicle Manufacturers

Domestic ForeignFirm Private Government InstitutionalTELCO 54.14 5.28 25.77 14.81Ashok Leyland 8.96 0.13 30.56 60.35Premier 65.53 - 34.47 -Hindustan 64.30 - 34.10 1.30

Bajaj Tempo 52.80 - 20.00 27.20Standard 47.46 - 24.05 28.49Mahindra & Mahindra 45.17 4.79 34.96 15.08Bajai Auto 100.00 - - -Automotive Prod. of 57.10 - 40.25 2.65

IndiaSimpson (Engines) 100.00 - - -

Average 59.6 1.0 24.4 15.0

E. Employment and Capital Intensity

2.12 The vehicle sector (automobiles Dlus cormercial vehicles) employedan estimated 62,500 in 1971/72 of which 42,500 were producing commercial vehi-cls. subdivided as shown below:

Emoloyvment bv Vehicle Tvne. 1971/72

V-h i r 1 t Tvny Emnl nvmPnt

.iediu m Heavy IT eh icl 32,50nLight Vehicles 3,500Jeeps 4,500Three Wheelers 2,000

Total! 42,500

, coumparable labor Iforce for a sim41.lar prodution level- in dvle4tiwould be about 10,000 or less. Labor consists mainly of high school graduates,recruiLteA an' tralr,el ly -le ,-,nufacturers 'or a perG d 40A 2 to 4 years al. anaverage cost of Rs. 20,000 per trainee. Some 73YO of plant personnel is skilledlabor and 17% supervisory; the balance s semi-skilled (9%) and unskilled (1%').Monthly wages and salaries of plant personnel average about US$50/month whichis approximately the average daily income of U.S. autoiLobile plant prUsoUnUl.

2.I3 tixec assets ana total capiLa; emnployeu per emplUyee arle hgu byIndian standards, amounting to an average of Rs. 20,000/employee (US$2,500)and Rs. 38,00/employee (US$4,800) respectively, suggesting that commercialvehicle manufacturing is relatively capital intensive (even more so takinginto account underemployment in most Diants). Nevertheless, these figures

- 7 -

are only 15 to 20% of the corresponding figures in developed countries. Thefixed asset/employee ratio ranges from Rs. 12,000 in the light commercial ve-hicle sector to Rs. 18-19,000 in the medium/heavy with the exception of Hindu-stan Motors where it is Rs. 35,700. The high figure for Hindustan is an ano-maly, reflecting the extremely low capacity utilization of that company.

F. Vertical Integration

2.14 The degree of vertical integration, as indicated by the ratio ofmaterials plus bought out parts over sales (excluding excise tax), has notchanged in the last three years and ranges from 0.66 for TELCO to 0.75 forAshok Leyland 1/. This range of ratios is comparable to those of commercialvehicle manufacturers in develoned countries where the dearee of verti-a-1lintegration averages about 0.64.

TTT ANATLYSTS OF PERF'ORMA1NCE

A. Production, Capacity Utilization and Market Share

1. Medium/Heavy Vehicles

3.01 The following table summarizes the trends in production, capacityutilizatior. and rmaket share of the four medium/heavy commwercial vehicle manu-facturers since 1964/65 (Annex 5):

Production, Capacity Utilization and Market Share, 1964-1972

Production(Nunbers) Capacity Utilization(%) Mkt. Share (%)J1764/J 197I/7/ I964/6D 9I7//1; 19O64/65 i97l/72

TELCO 16,100 25,057 89 104 51.4 71.5Ashok Leyland 3,800 4,769 60 75 12.1 13.6Premier Automobiles 6,000 4,075 100 68 19.1 11.6Hindustan Motors 5,400 1,141 52 8 17.3 3.3

Total 31,300 35,042Index UV h0/ 1I1

3.* 02 Production stagnated during the second half of the 1960's but in-creased substantially following the economic recovery at the end of that period.Since 1970/71, however, growth has again levelled off and preliminary production

1/ For the other producers, the ratio is Hindustan 0.69; Premier 0.69 andlight commercial vehicles 0.72. The higher the ratio isj the lower thethe degree of vertical integration.

2/ Base year 1964/65 index = 100.. official production figures were deflatedto reflect only production and do not include assembly of imported CKD's.

figures for 1972/73 total only 37,000 (Index 118), i.e. marginally above theproduction of 36,561 vehicles reached in i970/711. mne average annual rate of

growth therefore was only about 1.7% between 1964/65 and 1971/72.

3.03 The largest producer, TELCO, has been implementing a methodicalplan of expansion backed by adequate technical and commercial resources anda reputation for high quality products. As a consequence, its market share isincreasing (the order backlog has been about six months production recently)and the limiting factor to growth seems to be TELCO's plant capacity. Next toTELCO in the medium/heavy payload range is Ashok Leyland, which appears to beholding its position. Although 15 to 20% more expensive than equivalent payloadTELCO trucks, Ashok Leyland has maintained its market share primarily as a re-sult of a reputation for sturdy design. Premier has managed to maintain amodestly acceptable level of capacity utilization, but its market share hasslipped substantially. This is partly due to quality problems and partly tothe shortage of diesel engines supplied by Simpson, which has been sufferingchronic labor unrest and strikes. In view of the very low production andcapacity utilization of Hindustan Motors and the persistent negative trend,management may soon be faced with a decision as to whether continued productionof commercial vehicles is viable.

2. Light Commercial Vehicles (including jeeps and jeep trucks)

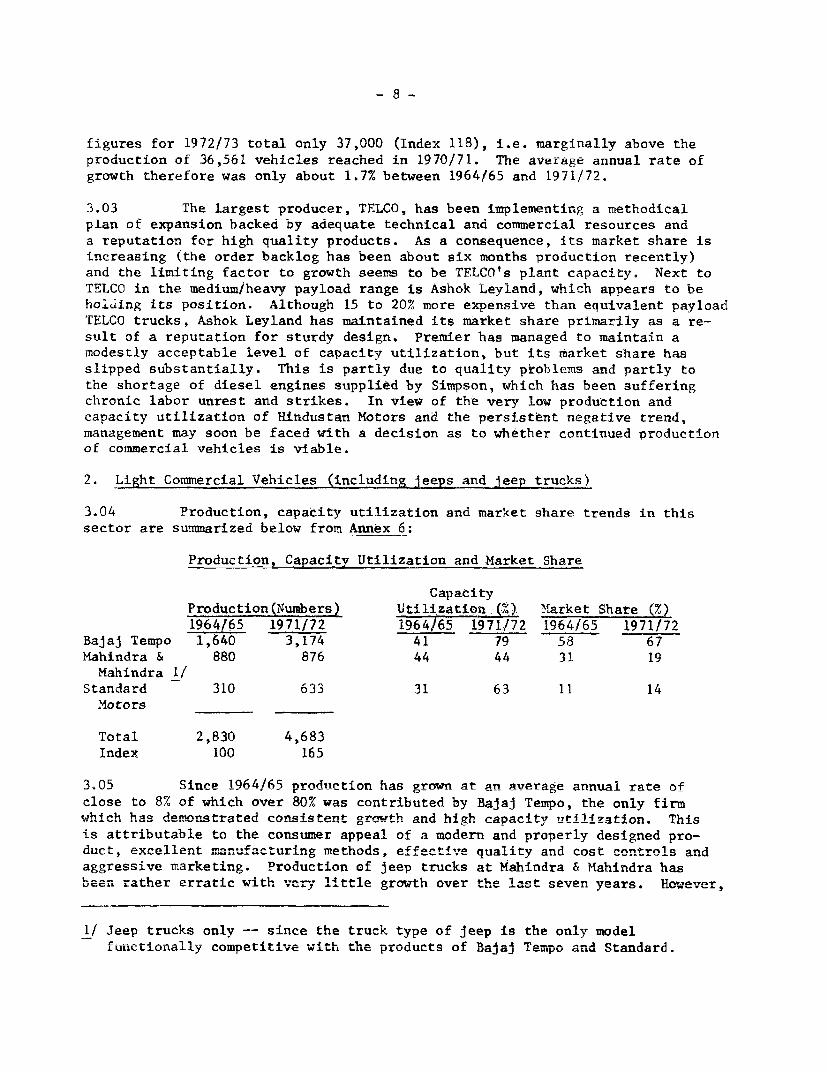

3.04 Production, capacity utilization and market share trends in thissector are summarized below from Annex 6:

Production, Capacity Utilization and Market Share

CapacityProduction(Numbers) Utilization m(.), Market Share (%)

1964/65 1971/72 1964/65 1971.172 1964/65 1971/72Bajaj Tempo 1,640 3,174 41 79 58 67Mahindra & 880 876 44 44 31 19

Mahindra i/Standard 310 633 31 63 11 14

Motors

Total 2,830 4,683Tndex 100 165

3n05 S1nre 1964/65 nrndait-l on has grown at an average annual rate ofclose to 8% of which over 80% was contributed by Bajaj Tempo, the only firmwhich has demonstrated consistent growth and high ca-acitv utilizatlon. Thisis attributable to the consumer appeal of a modern and properly designed pro-duct, excellent m-nufacturitng methods, effective quality ar. cost controls and

aggressive marketing. Production of jeep trucks at Mahindra & Mtahindra haslbeen. rathLer erratic wit-h ver-. 14ttle gr5 th over t1.e last seven years. Hw ever,

1/ Jeep trucks only -- since the truck type of jeep is the only model

Lurict'LorLaLLLy comUpetiLtiLve wiLLth Use proLducts of Bajaj Tem,po andA' Standard.

- 9 -

production and capacity utilization figures for jeep trucks along present adistorted picture of company size and performance since there is a good dealof functional and component substitutability between jeeps -- the malor product --and jeep trucks. Capacity utilization figures for the conbined productionhas averaged a high 97% over the last three years and production has increasedfrom 8,000 in 1968/69 to 12,000 in 1971/72, the latter valued at Rs. 230 million(US$33 million) or 12% of the gross product value of the industry. Productionat Standard Motors has been quite erratic mainly as a result of labor problems.

3. Three Wheelers

3.06 There are only two companies, Bajaj Auto and Automobile Productsof India, together licensed to mAnufacture 12,0Q0 three wheelers of which in-stalled capacity is 9,000 at present. Annual production has increased from4.700 in 1968/69 to 6,500 in 1971/72 and an estimated 8,000 in 1972/73. Util-ization of capacity was 72% in 1971/72, having risen from 59% in 1968/69 and1970/71. Gross nroduct value was reported as Rs. 37 million (US$5 m4llIonN) in1971/72 as against Rs. 25 million in 1968/69 and accounts for less than 2% ofgross nrndu-t value of the comnercial vehicle sector.

4. Diesel Enaineqs

3=n7 There is or.e indeper.det m-nufacturer of diesel eng4nes used Intrucks and buses, Simpson Co., licensed to manufacture 12,000 Perkins engineswith an installed capacity of 6,000 units at present. Simpson suJp'les en-gines to Premier (the only vehicle manufacturer without in-house engine pro-duction facilIties) and TAFE (tractors) in the range of 3510r to 120 !1P.Utilized capacity was a low 43% in 1971/72 having fallen from 46% in 1968/69an.d 53Y% 4,, 'L. T.he if'Lri-u'UsUpoor performa,ce 18 attributUable to antiquatedproduction methods, poor management and poor labor relations.

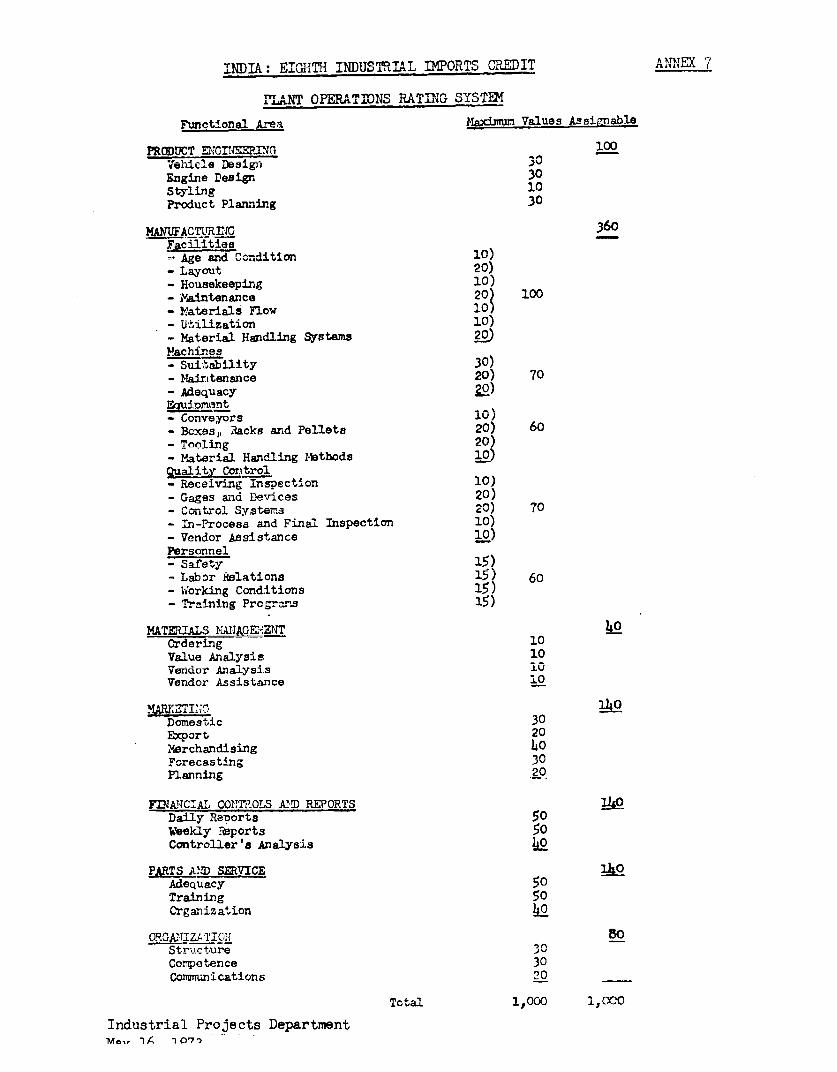

B. Plant Operations

3.08 Evaluation of plant operations was carried out by the consultants.The performance oI the major firms in seven major functional areas of plantoperations as well as the average sector performance are given in the table

L1 . A A~ 1~ below. A Uetailed description of the functional areas and the rating systemis given in Annex 7.

- 10 -

Summary Performance Ratings of the Six Major Vehicle Manufacturers(percent)

Bajaj Mahindra &TELCO Ashok Premier Hindustan Tempo Mahindra Average

Prod. Engineering 77 38 43 15 88 32 -49Manufacturing 87 51 79 29 89 35 62Materials Management 88 58 75 20 90 23 59Marketing 75 39 25 26 78 25 45Parts & Service 100 57 50 32 79 43 60Financial Controls and

Reports 54 26 49 21 86 29 44Organization 90 56 59 33 89 34 60

Overall 82 46 58 26 85 33 55

3.09 In the following paragraphs, the principal features of operatingperformance are discussed. By necessity, a summary of this sort cannot do morethan touch on the differences in performance between individual manufacturers,which -- as the above table demonstrates -- varies widely. Detailed descriptionsof each manufacturer's performance is given in the consultants report.

1. Product Engineering

3.10 Product engineering, including vehicle and engine design, stylingand product planning are on the whole deficient by world standards with twoexceptions - TELCO and Bajaj Tempo. The truck lines of the latter are wellengineered, suitably styled and economical to manufacture and with the growingscale of production should soon be competitive in export markets. TELCO's pro-ducts are quite good both as to functional design and economv of manufacturingin the context of the Indian market, but require updating if export marketpenetration is to be accelerated. Basic vehicle designs for the other manufar-turers, on the other hand, are substantially out of date. For the most partthese vehicles lack eye appeal; driver comfort and comnetitive nerfnrmancp rhar-acteristics and are costly to manufacture and operate.

3.11 Engine development lags seriously behind the needs of the domesticas well 2S the pmnrt market. Most engines are out of date arnd some are ex-cessively costly to build and maintain. Only Bajaj Tempo is regarded as havinga fully suitable en-4ne All d4esel -owee trucks -roduced in India aregrossly underpowered, based on generally accepted ratios of gross vehicle weightto engine (cylinder) dIsplacementJ- Taking in-…- acour.t a'-^ th -- al- pracice

of over-loading beyond the recommended payload, the two factors together resultin excessive wear, bre -qA owns nd costly ove.-hauls a- muchL more fLreque. inter-valsthan normal by modern standards.

3.12 Product planning, which is concerned with the design and developmentofl products to meet cLear'Ly defifned cost ar,d markACetir.g VobUJ CL.LVC, Uoes nOL

exist in India as an organized effort although TELCO and Bajaj Tempo are develop-ing capaDiiLities Li this area. Detailed stuLes of manufacturing costs and tnemost appropriate manufacturing methods, including standardization of materials,

- 11 -

are not generally carried through when preparing to produce a new, or substan-tially modified, product or part. Investigation of material or component sub-stitutions to reduce cost, improve performance or ease procurement problems isnot generally practiced. Competitive vehicles are not disassembled to identifyopportunities to cut costs and improve performance. Little attention is givento assessing customer needs and preferences as a guide to developing newmodels.

2. Manufacturing

3.13 Vehicle manufacturing in India, in general, compares favorably withsimilar activities in the U.S. and Canada. The commercial vehicle industrv isvirtually self-sufficient except for deep-draw sheet steel and a relativelysmall number of special materials and comnonents. Production builaings nre nfup to date design and the overall layout of most truck plants is good, althoughin some cases improper location of one or more nroduction departments giveSrise to unnecessary and time-consuming material handling and additional in-processinventorv. Buildines are generallv well maintained nnd wilt-h the nx-AntAn nfHindustan Motors and Mahindra & Mahindra, housekeeping is good to excellent.Material handling systemc have not kept pace with increased production and 4Sapparently not yet recognized as a major production cost factor. Improperhandling of gears and other highly mnchined parts, contribute to higher thanwarranted rejection rates.

3.14 Plants are generally well equipped considering current productionlevels and cost consdr io with a roximtely half of the metal workigr,

machines made in India. Most machines are single purpose and are deemed suit-ahlp fnr riiurrnt prodtiont, inn A pou4 .o M ei4-, -an vol.. -- of. pro=

duction. However, cutting speeds and rates could be increased in most machining.orin. Most of Idia's truck manufactur g plants re under=utilized

even considering the normal work period of two shifts per day and six days aweek. Underutilization can be attri-buted in a-large -l-a-uL Lo poor -c-e-ulLg,

inadequate floor supervision, shortages of parts and electric power and to alesser Aegree to Ineffie- plant la-yout, poor product accepLaLice (a majorfactor in at least one case) and some weaknesses, or inexperience, in general

mangemMnrt .n,ni oan osn J_

3.15 The qu a4.Lty ofJL most tLUk proUUUceU Ld I LL.dia, partLiu.Larly that Of

TELCO and Bajaj Tempo, is good. On the whole, quality control is given ade-quat attLeto but there is some 'uoseness in the systems of tabulating andreporting quality defects in a timely manner. Such systems are essential toreduce the LatdLtofl time and eliminate defects berore ratner than arter thefact. Bad castings are a major source of quality problems and in some plantsthey do not seem to be identified until after costly macnining. Generally,the relatively large number of "finished" vehicles observed in the repairareas at some plants suggests that both in-process inspection and assemblysupervision need strengthening.

- 12 -

3.16 Possibly the weakest function in the broad area of manufacturingis personnel relations. Only TELCO, Bajaj Tempo and Premier appeared todemonstrate appropriate concern for employee welfare. The apparent indifferenceto legitimate employee welfare objectives in other plants may be a root causeof labor unrest. Training programs, on the other hand, are generally ratedhigh. Many of those trained by truck manufacturers have moved to the automo-tive ancillary industries and are in large part responsible for the rapiddevelopment of India's mechanical industries, particularly metalworking.

3. Materials ianagement

3.17 Materials management, which is concerned with procurement, storageand inventory control, usually is not assigned to a single executive in India'struck companies. Partly as a consequence of diffused responsibility, inventoriesof raw and in-process materials tend to be higher than warranted, even takinginto account typical procurement difficulties. Because qualified supply sourcesare limited, the buying function in this industry is largely an ordering pro-cedure and too little attention is being paid to prices and delivery schedules.However, the more efficient manufacturers (who are also the larger customers)are rating suppliers on price, delivery and quality and this is having a salu-tary effect on the entire ancillary industry. These efforts bv the manufactur-ers still have limited impact because in many categories competition is minimumor absent and the supplier is in a stroneg "seller's market" position.

4. Marketing

3.18 Because at present truck demand is far ahead of supply in Indiathe marketing function is virtually non-existent and is largely limited to or-der nrncessina. With the excention of TELCO and Baiai Tempo. there are also

deficiencies in the distribution of spare parts and repair services and littleeffort seems tn he devnted tn deaeAr development- Virtually no attemnt i9 heingmade to systematically develop exports, with the exception of TELCO which isplanning l0ng ri"an penetration nf three In-rape ovPreQas mnrket - Egvnt

Nigeria and Indonesia - based on assembly line production in those countries.

5. Financial Controls and Reports

3.19 All truck companies are handicapped in varying degrees in achievingMax4m, ut-lizatior, of mApower an.d e Mi p m- absennce of varlable-

volume budgeting and a system of action-oriented reports on performance thatare accuratte, til y zn- -- A co-e,a i. *rU- 4nds.--t. overal rating i.n thU

critical area is the lowest of all categories evaluated (44X).

6. Organization and Management

3.20 Deficiencies in organization are reflected in the problems discussedabove. The major organization/structural deficiencies include (1) the non-existence of, or the low priority given to, important positions or functions;(2^) the failure to group together related functions and operations; and (3)the failure to clearly assign duties and responsibilities. Although it wasnot in the missionTs terms of reference to evaluate key personnel they were

- 13 -

Jugel to le comarable in com-e-en.ce and perfo,mance to their cour.terpartsJ U L.I u ~ C&~U.L~ A.L LIUL LCLL LU L~ _LLl~LL~ L.LLL A- L.LJ.LL~L~L

in North America and Europe. Most of the operational problems noted appearto be due priMarily to inadequate organiZation planning rather than to iL-competent management. 1/

C. Indigenization Trend

3.21 The impressive production growth rate averaging 18% over the lastdecace nas Deen paraiieiea Dy an equally remarkable growth in indigenous con-tent, 2/ shown in the table below (Annex 8):

Growth of Indigenous Content, 1962-1971

Vehicle Type i96i/62 i964j65 i970/7i

Truck, BusesTELCO 67.0 86.0 98.5Ashok Leyland 43.3 81.5 97.7Premier 74.0 88.2 99.8Hindustan 60.9 73.9 93.0

Jeeps 59.0 90.0 98.0Three Wheelers 59.0 86.5 97.4Diesel Engines 70.0 87.5 97.5

3.22 The figures given above do not include materials imported by thevehicle manufacturers or the import content of components purchased from theancillary industries (Annex 9). If these inputs were to be included, the"true" indigenous content would drop to about 85%. A major item in the 15%of total imported value is deep-draw steel sheet and if domestic productionwere able to supply the demand, the indigenous content figure would rise toover 90% which is probably very close to the maximum economic level.

1/ In Chapter V, recommendations on action needed to overcome the operational~~~~U,tcu e AM thi S=_ _V 4arte S--111a i e . .M_Jw_- WzLL-LL&L..L> ULJ.Uat:U 1&L WLL.L b~LUVL a, bLu1J1~ ±I.«tu.

21 "Indigenous content" is defined by the government as the foreign value ofsez-fiL.Lnished anud 'L'u.sUdU cUUminuuie.± WILLCLI are prLoUUUCeU UUd L.±caly, ex-pressed as a percentage of the ex-factory price of the equivalent foreignvehicle. It is expressed mathematically as 1 - m/p where m is the ex-ractoryforeign value of imported components and p is the ex-factory foreign price ofthe vehicle. import of raw materials are not included in m because it is notpart of the manufacturers responsibility to produce his own raw materials.Furthermore, m does not include the import of finished and semi-finished ma-terials used by the ancillary industry. -This a manufacturer that buys a largeportion of its components from domestic suppliers will show a very high levelof indigenous content even though the impore content of his suppliers might behigh. Indigenous content was so defined to give"every encouragement to manu-facturers to buy components from outside ancillaries". To the extent that the"indigenous content" does not take into account direct imports of raw materialsand indirect import of materials and components by suppliers, it tends to over-state the foreign exchange savings.

- 14 -

3.23 The ancillary industry now consists of over 500 firms (2n0 in theorganized sector, and more than 300 in the small scale sector) producing over4,000 different products and employing about 100,000 persons. It sunnlies65-70% of the gross value of commercial vehicles. Needless to say, there havebeen considerable growing pains with regard to sub-standard nrodunts, highprices and poor delivery schedules but reportedly the problems are progressivelybeing overcome with the active assistance of the truck manufacturer8 TFT CO'srecord in this respect is outstanding. Technical and financial assistance isextended in product design, manufacturing methods and nrocesses and qntilitycontrol procedures; TELCO also makes available modern testing facilities andprocurement assistance to the smaller ancillA- uni ts, going as far as toprovide them with gauges and raw materials of rigid specialized specificationswhich are invariahlv in shnrt .- PnPly

3.24 Vehirle maniuffane-rs rpeprted tha.t- dpite 4 -proved performanceby ancillaries in recent years, maintenance of a regular flow of indigenouscornonents continued to be a problem be-use of brea'-Aw..S 4; nsuppliers' plants,strikes, non-availability of transport, power shortages, etc. Uinder presentlicensing procedures unexp-ected shortages of locally produced i'tem can-lot besubstituted rapidly by emergency imports, even when the licensing authoritiesare svymnthotir tn the need. Asaresult, manufacturers are forced to main,-tain higher inventories than normal with concomitant financial costs and higherfinizh.ede .yliehlcl rcs

D. Finrancial Performance

1. Pr4ces

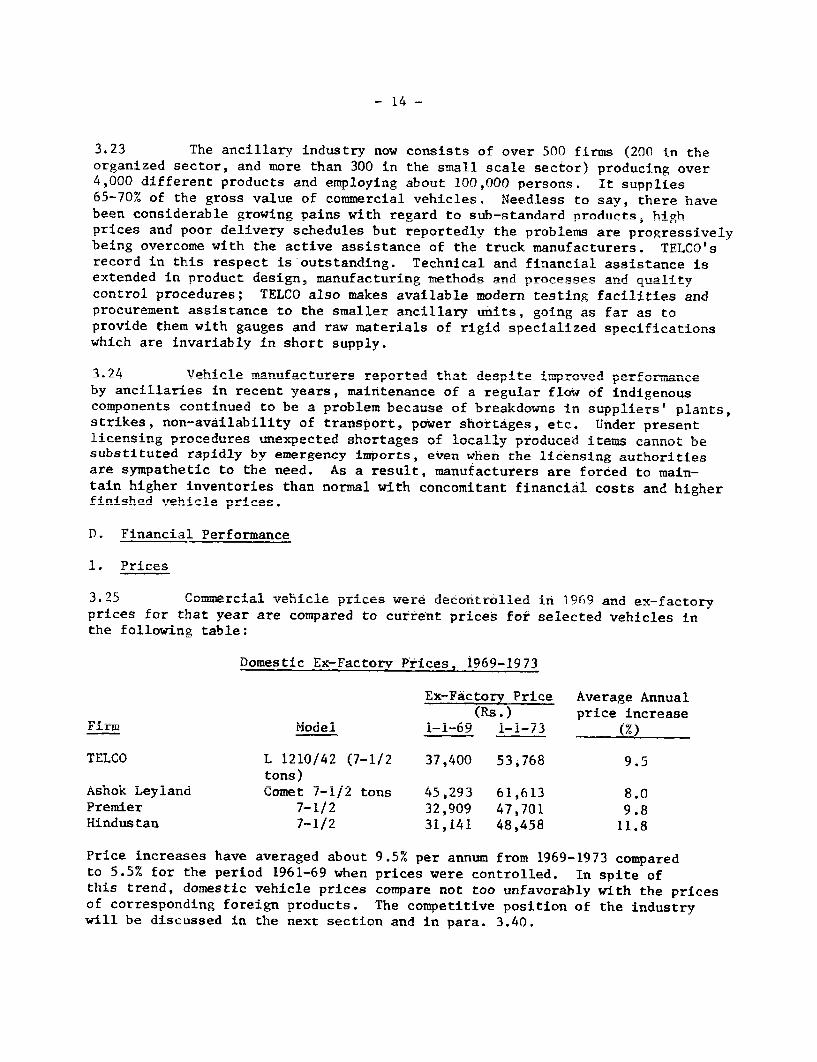

5Commercial vehicle prces were decontrolled in i1969 and ex-factoryprices for that year are compared to current prices for selected vehicles in

lom-iesti c Ex-Factory Prices, 1969-1973

Ex-Factory Price Average Annual(Rs.) price increase

Firm Model 1-1-69 1-1-73 (%)

TELCO L 1210/42 (7-1/2 37,400 53j768 9.5tons)

Ashok Leyland Comet 7-1/2 tons 45,293 61,613 8.0Premier 7-1/2 32,909 47,701 9.8Hindustan 7-1/2 31,141 48,458 11.8

Price increases have averaged about 9.5% per annum from 1969-1973 comparedto 5.5% for the period 1961-69 when prices were controlled. In spite ofthis trend, domestic vehicle prices compare not too unfavorably with the pricesof corresponding foreign products. The competitive position of the industrywill be discussed in the next section and in para. 3.40.

2. Cost Structure

3.26 The table below compares the cost structure of the more efficientIndian producers with the best available estimate of comparable foreign pro-ducers:

Comparison of Indian and Foreign Cost Structure

Domestic Cost Foreign CostBreakdown Breakdown

(%) (%)Bought-out(a) Materials 10 - 33 n.a.(b) Components 65 - 33 n.a.

Total Bought-out (average) 71 64

Labor (direct and indirect) 10 - 14 15 - 22Other Expenditures 3 - 6 4 - 6Depreciation 2 - -5 5 - 7Interest 3 - 6 3 - 4Profit before Tax 4 - 8 6 - 10

Average Conversion 29 36

Total 100 100

The essential differences between the Indian and foreign cost structure are:(i) external innuts- basiatllv materials and comnonents, are nabnt 10 higherin India, and (ii) conversion cost (value added) is about 20% lower. If theforeign rnat breAkdownm wuere adJusted to reflect theo '-.n% lower f .o.b priceof foreign vehicles, however, the differences in terms of actual foreigncurrency or equivalenrt r-ee costs tould be reduced by 5-10Zv.

327 Matp l AiMlervals, ma4n1y steel,- are pronnred rthrtuih Hinfiictan Steel

(HSL). Manufacturers reported that their supply of steel is adequate and,even. during the-n 0naseso g ir. 197071 , no firm experIenced anysignificant slowdown in production because of the shortages. On the averageprices of IndTia.n anrd i4nort steeal arae a.bout nq1 A large nwmbe.ar of compo

nents are already competitively priced. These are usually made of steel andhave a hbi4gh abnr content, e. . castng forn r_r.gs, machined parts A.A C-.df

injection pumps. On the other hand, prices of proprietary items such asAn1nQe_4nn1n ke.. 5 .4at A O A F4 _An A) _. 2 4 -4 _,A k J.- s 4-ks 4 S5 E;t. XXr4cals, batteries an. tAireOS are 2 Lt *VJ Xt8ime as hiL911L aO tLhe c.. * vL*. prLcs0

of comparable imports primarily because of high cost of raw materials and the'Low sca.le oli operaLoC LsLPA. fl0U LLLL Iou LtiLCtL O UIpLCI aii3.9C1.. LII LUa 1 Jo -I±I.lwsale of oprLi.-. L)gt=u ir,d'L.Lnger.ous co,..or.ents ra-L.ge from lOfo highrerthan c.i.f. for TELCO to 30% higher for Bajaj Tempo. The relatively lower costLiLgure Lor TEL,CO ib UUe PdLL±. LU Lil .arLgeL scale operations of the ancillaryproducers developed by TELCO who supply both the original equipment demand(2J5UU0 truckrs/year) and the replacement market (j;5,000 urucks on tne road),and partly because of TELCO's bargaining power vis-a-vis suppliers. The premium

- 16 -

of 30% paid by Bajaj Tempo would be even higher were it not for the company'sstrategy of maintaining multiple sources of supply to induce competition andguard against disruption of operations. Relative to the low scale of operations,30% is a reasonable premium and testifies to the success of the firm's procure-ment strategy.

3. Profitability, Productivity and Financial Structure

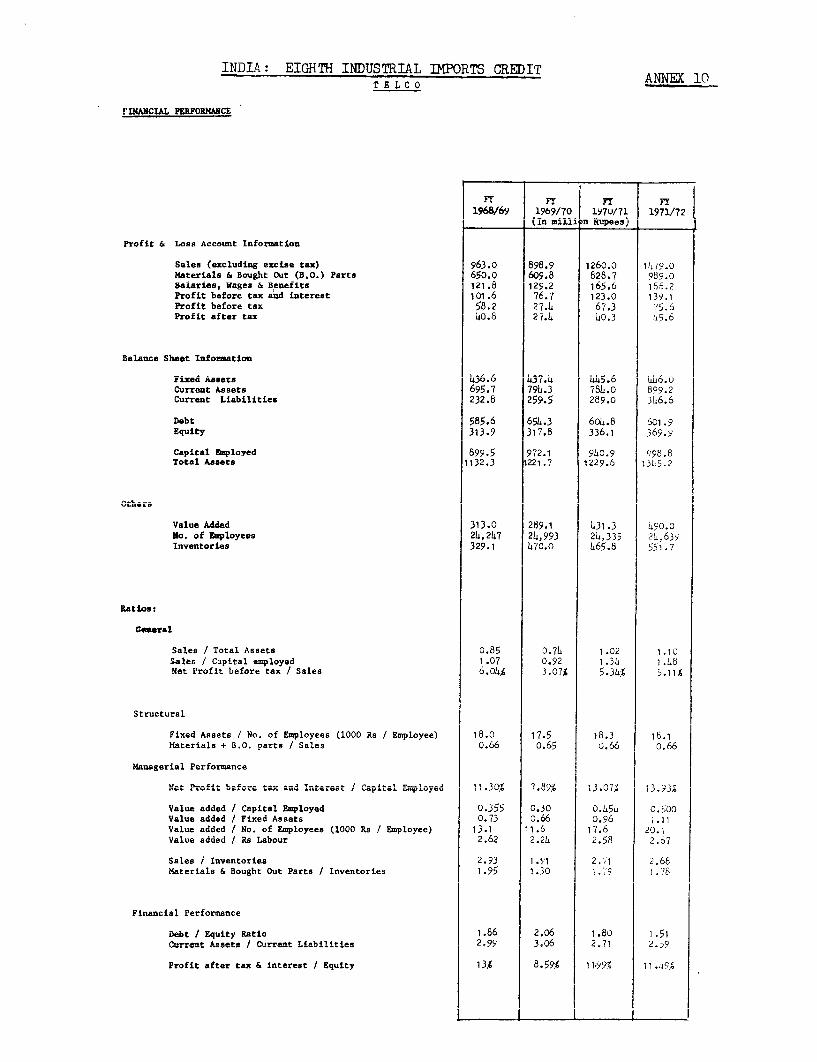

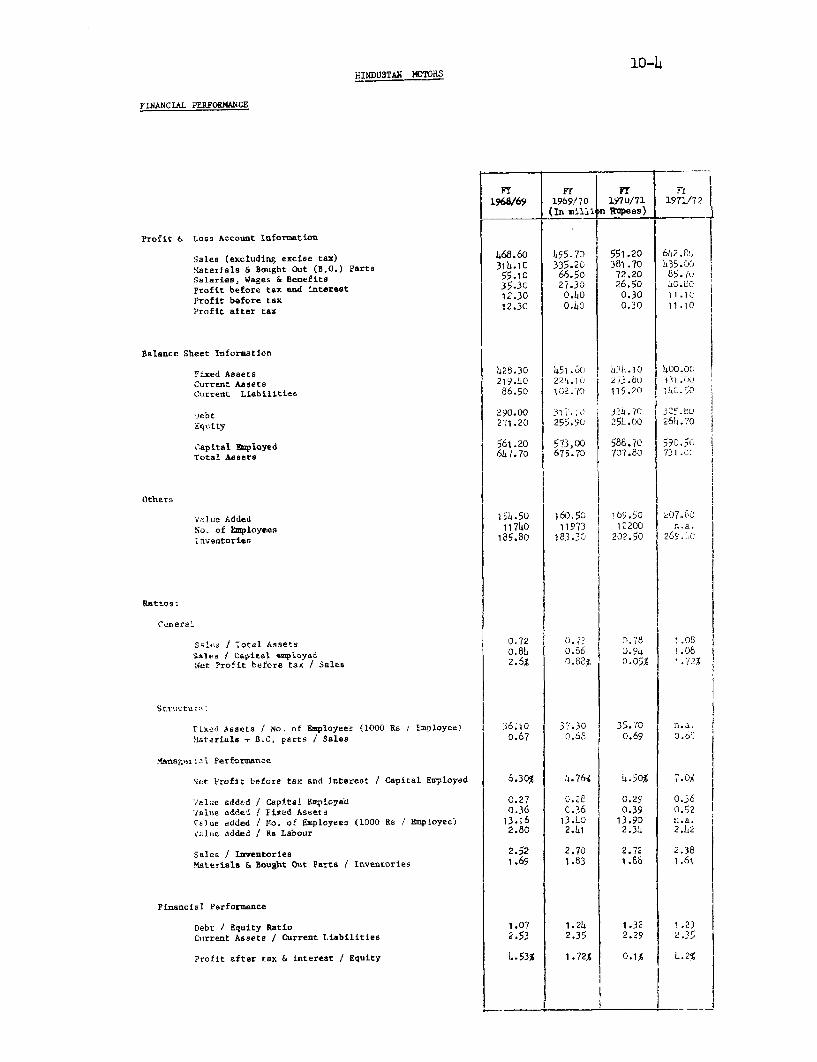

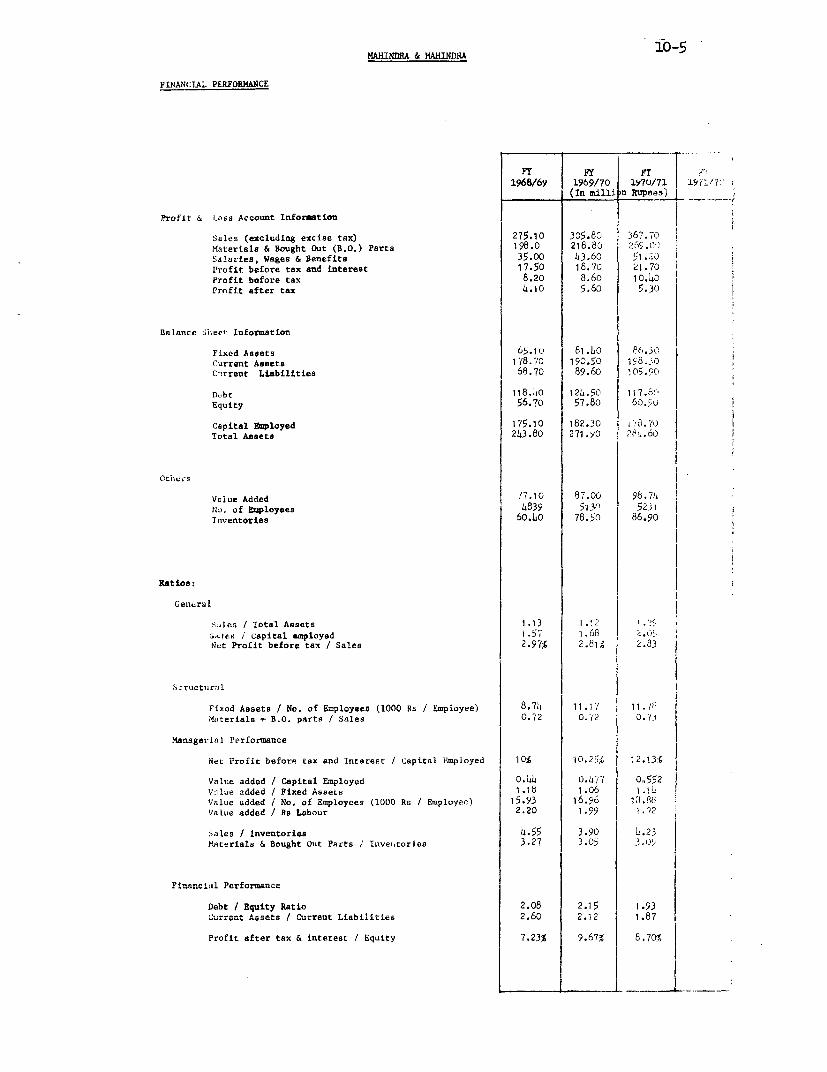

3.28 The principal indicators of financial performance for the commercialvehicle producers over the past three years are shown on the following page.Aaior trends are briefly summarized below and are supported by the detaileddata in Annex 10.

3.29 Profitability as related to sales has deteriorated somewhat forall vehicle producers except for Balai Tempo wqhich showed a strong gain. Therehas been a definite improvement, however, in the return on capital, which, withthe exception of Hindustan and Premier, is good by Indian standards. The lossrate at Premier is decreasing but Hindustan's profitability remains rather poorand. indeed; would have to be renorted as a loss if full deDreciation were tobe charged. The growth in profitability was achieved despite an average annualincrease of 16% for raw materials and 10% for items bought from ancillarv in-dustries compared to only a 7-10% annual increase in comrmercial vehicle prices.This indicates that nlant efficiencies are fmnrovingn At rates that m-re thancompensate for the rise in prices of external inputs. Also part of the priceincrasqes are eip ton nrtdti-t- inrovements- eopeninl1v at TETGC0

3.30 ''na117tin0 of 2ssets as meaiired hv r2t40sn of valuep qeAr overtotal capital employed and fixed assets respectively, has generally increased

improved. Despite the significant improvement at Hindustan, primarily as aresult of increased production of passenger cars, its performance as a co0ercialvehicle manufacturer has remained extremely poor. Some further gains can beexpected 4n the coming years by i..creasin.g producto4n at Ashok 1e al T -. A -r,d

Bajaj Tempo, but for firms which have already reached their rated capacity (TELCO& at..fllA c '. a.o,~t,..t ,- -it. JJla .. .LLJA iVt&pA W. L.± A. iCVt L. isntny Li.LUIn

more efficient production methods.

3.31 Labor productivity as measured by value added (at constant prices)per eployee las increased by between5 o Jh for hind1UUstLanLU Ji. 5 ur 1TLU overthe last two years. The sharp increase in TELCO's labor productivity can beexplained by the intensive training given by that company. In spite of theincrease in value added per employee for all firms, only two, TELCO and BajajTempo, 'nave experienced an increasea in value added per rupee of iabor.

INDIASELECTED FINANGLAL PER]FORMANCE INDICATORS OF

('CQ0MERCIAL VEHICLE MANUFACTURERS - 1969-1972

Mahindra &TELCO Ashok Leyland Premier _ Hindustan Mahindra _laja; Tenmo

1969 1972 1969 1'972 1969 1972 1969 1972 1969 1972 1969 1972

Sales (Rs. million) 963.0 1,479.0 3365.1 339*5* 306 3 382.5* 468.6 642.8 275.1 367.7* 46.4 63.2*

Profit before Tax, Rs. millionr, (loss)58.2 75.5 18.5 20.4* (71.1) (67.(\)* 12.3 11.1 8.2 10.4 i.0 5.40

Profit before Tax as; % of Sales 6.0 5.l 7.0 9* - 2.6 1.7 3.0 2.8 2.2 8.5

Profit before Tax & Interest,as % of Capital Employed 11.30 il.93 11 .9 13 i3 - - 6.30 7.00 10.00 12.13 12.95 16.75

Net Profit/Equity (31) 13.0 11.5 3.S 7.3* 4.5 4.2 7.2 8.7* 7.9 15.5*

Sales/Capital Employed 1.07 1.48 1.51 j.74* 1.17 1.47* 0.84 1.08 1.57 2.05* 1.65 1.54*

Value Added/Capital Employed 0.36 0.50 0.37 0.40* 0.37 0.45 0.27 0.336 0.44 0.55 0.41 0.47

Value Added/Fixed Assets 0.73 1.11 0.86 1.02 0.62 0.72 0.36 0.52 1.18 1.14 0.82 0.94

Value Added/Employee (Rs/Employee) 13,100 20,000 17,600 '8,500 n.a. n.a. 13,100 13,900 15,900 18,900 n.a. 12,100

Value Added/Rs.of Labor Cost 2.62 '.67 C0( 2.5? 1.39 1.37 2.80 2. 4 2.20C 1.92 :3.18 3.36

SlesiTnv.entori es 2.93 2.68 3.60 2.43 2.63 2.95 2.52 2.38 4.55 4.23 2.79 2.46

Current Assets/Current Liabilities 3.0 2.6 1.9 2.7* 2.7 3.4* 2.5 2.4 2.6 1.9* 3.4 3.0*

Debt/Equity 65/35 60/40 '35/65 35/r 5 60/40 59/41* 52/48 55/45 66/34 '7,/35* 70/30 47/53

* For 1370/71L.

- 18 -

3.32 Inventories of raw materials and components are generally high.

Inventory turnover ranged from about 2.4 (Hindustan) to 4.2 (Mahindra & Mahin-

dra) which is very low when compared to turnover rates of at least 6 in this

industry in developed countries. Furthermore, the situation seems to have de-

teriorated recently probably due to -- among other reasons -- increased uncer-

tainty regarding the availability of foreign aid. Inventories consist mainly

of materials and bought-out components (about 70% of inventories); stores (5-10%1); and semi-finished goods (20-25%). Considering the backlog of orders,little or no finished product inventory is necessary. The reasons for highinventory levels are: (1) small-scale of production, which means that purchases

buch domestic and import have to be made in relatively large lots; (2) uncer-tainties regarding foreign exchange availability and import licensing; (3) un-

balanced plants resulting in high in-process material inventory; (4) uncertainty

about local supply of components which under present procedures cannot be made

up bv timely imports; and (5) poor materials management.

3.33 Manufacturers pointed out that inventory levels could be reduced

if a more regular flow of materials and components were assured. This objective

could be partially achieved if some portion of import licenses were "freed",i.e. usable without regard to the banned list. Thus, rather than maintain highinventory levels of a large number of components as a hedge against disruption

of domestic supply, free import licenses could be utilized in immediate responseto a sudden shortage of any item. It is estimated, for example, that if 25% of

import replenishment entitlements or 5% of the Actual Users licenses were tobh '"freed".. inventories of bought-out components could be reduced by 10-15%.Since the carrying cost of inventories is about 15-20% of the value (11% interest

on working canital nlus handling and obsolescense), the estimated reduction in

carrying costs for the industry would be Rs. 2.5-5.0 million per annum equiva-lent tn a cnst rP6urtion of Rs. 75-150/truck.

3 34 T-t im estimrted that this mArainal liberalization of import licensingwould "free" about Rs. 10-15 million per year compared to the annual ancillaryindustries output of RsB. 3 b hillifnn Tn other words; the mechanism suegested

might shift no more than 0.3 - 0.5% of the ancillary producers' market to foreignsources: -- . Again.t th4i pnasibhlp nealigaqlhe temnorarv contraction of the in-

digenous market must be weighed the benefits, including: (i) rapid alleviationof tempora,ry shortages of co-onents causedc by strikes pnower and transport fail-

ures, etc. and more reliable delivery of finished vehicles, (ii) reduced inven-tores, (i444 4m.roveme.nt in. quality of eorted v-ehirles bhv inrlitsinn of romno-

nents requiring stricter international standards; and (iv) relieving managementandiu DTnJVL personr.el from ti4me-cons-4ng p-pe rk.r-1 and negoVrt-iat4onsQ

1/ It might be argued that freeing Rs. 10-15 million/year can drive some of the

least efficient firms out of business. However, it must be pointed out that

even if those inefficient firms lose the original equipment (O.E.) market, they

would still retain the replacement market. Hopefully, the loss of the O.E.

market, or the threat thereof, would induce those inefficient producers toimprove their products and operations.

- 19 -

3.35 Starting in April 1973 the Government has allowed exporters to use5% of their REPs for importing any industrial requirement without having to ob-tain the "indigenous angle" clearance, subject to a limit of Rs. 10,000 per itemin each licensing year. Exporters who have doubled their exports in 1972/73would be granted an additional 5%. Other proposals are also being consideredand these efforts are significant steps forward. However, the restrictionsimposed on the marginal liberalization measures adopted tend to vitiate theirbenefits. Reliance on existing tariffs rather than quantitative restrictionsto protect domestic industry against marginal import liberalization would bemuch more effective in achieving the benefits mentioned in the previous para-graph.

3.36 Related to the above discussion, there is within the general prob-lem area of import constraints; the need to accelerate and rationalize the en-tire import licensing system. Computer processing of the masses of data submittedby manufarturers as well asl coTrrmnuter monitnring of licenses issued and usedwould not only speed up the licensing process but would provide timely and essen-tial dta to assist short and long range planning, deaIs on-making and fast reac-tion to unforeseen trends in available foreign exchange. The computer dataprocessing -ro-ram. is current!- under review and should be imp1nepmentpe aR soon

as possible.

3.37 There has been a general deterioration in working capital over thepast' thL ree years; but the liquid4ty position of all co "anieS is st,ll sat-

factory even taking into account inflated current assets on account of undulvhigh inve r.torie. CapitalizatLon 4i. temLs 0fI the relat4 o.shi.p

debt and equity ranges from 35/65 for Ashok Leyland to 65/35 for Mahindra &IiLLLUL Sir.Lce thle 'Latter alUso hLlas th,e -weakest liquidity position its over-

all financial position appears to be strained.

E. Economic Costs and Benefits

3.38 As was mentioned previously, the principal instruments used to ir-plement the Government's strategy for growth and indigenizatLon are ind-ustriallicensing, indigenous content commitments, restrictive import licensing (quan-

titative restrictions on i'mport'ng iLtems mLanulfacturedU ±n IndiaU andU price COn=

trol. In addition, exports are encouraged by incentives including, inter-aliaduty draw-backs, cash assistance (oonuses paid on exports), special import re-plenishment entitlements (REP's) and relaxation of industrial licensing con-straints on t'larger" houses exporting a determined share of their output.

3.39 The purpose of this section is to evaluate the degree of protectionimplied by the above set of measures and the current cost competitiveness of theindustry. The concepts which are used in this section to measure the extent ofprotection and cost competitiveness are simple price difference between the do-mestic and similar imported vehicle; adjusted price difference with inputs atinternational prices; effective rate of protection; and domestic resource costof foreign exchange. These concetts are defined in Annex 11.

3.40 The indices quantifying the Drotection and cost competitiveness cal-culated for six important product lines are given below:

- 20 -

Indices of Protection and Cost Comnetitiveness of Commercial Vehicles

Simnle AdiustedPrice Price Effective Rate Domestic Resource

Difference Difference of Protertinn 1/ Cost of Fnr Fzrch.2,- (%) (%) (Rs./US$)

Tmnort TmnortSubsti- Substi-tut- on Exort tuti o n .Eor-t

Medium/HeavyTELCO (7-1/2 torns) -11 -18 -38 -44 6A33 0n.5Ashok Leyland (7-1/2 + 1 - 8 -34 -22 6.90 10.05

to-s)

T -4 .-4,

Bajaj Tempo (1 ton) +32 + 6 +23 -20 9.46 12.8BaJaJ4 Te,n,o (1=1/2) ton) L)7 L A -L1 -16 Q. tl 2.0

Jeep + 4 - 6 -20 -22 7.28 10.1Teep TrucLks = 9 =1 =55, 6. 12.2

1/ The percentage excess of value added by the manufacturer obtainable bv reason01 LarrllS anu otner proLecLive (promoiLon) measures on Lte proaucL ana i.sinputs over value added in a trade situation.

2/ The domestic resource cost, direct and indirect, of a product over the dif-ference between c.i.t. value of imports (or f.o.b. value of exports) and theforeign exchange expenditure, direct and indirect, for domestic production.

The items in the table above account for about 93% of the output in mediumiheavy vehicles, 60% of light commercial vehicles, and 100% of the jeeps andjeep trucks and include all product lines for which reliable data are available.These figures show that there is a wide range in the current cost competitivenessand protection given to the various products.

1. Medium/Heavy Commercial Vehicles

3.41 The simple price differences calculated for TELCO and Ashok Leylandshow that the ex-factory cost of the domestic product compares quite favorablywith the estimated c.i.f. price of comparable imports, i.e., 11% less than thec.i.f. price for the TELCO product and 1% more than the c.i.f. price for theAshok Leyland product. The adjusted price difference indicates that the productswould be even more competitive if the manufacturers were able to procure inputsat prices that would obtain under free trade conditions. TELCO's and Leyland'sex-factory prices would drop respectively to 18% and 8% below c.i.f. prices ofcomparable imports.

- 21 -

3.42 Both firms are subiect to negative effective rates of protectionfor their import substituting activities (-38% and -34°' respectively for TELCOand Ashok Leyland) and export activities (-44% and -22% resnectively). Desnitethis negative rate of protection, gross profit before tax and interest (on totalcapital employed) is 14% for TELCO and 15.5% for Leyland: iwhich is a reasonablereturn on investment. The small difference between the effective rate of pro-tection for import substitutine activities and exnort activities implies thatexport incentives are adequate. TELCO's lower rate of effective protection forexDorts (-44%,V is based on sales to Egvnt; where data were available; and mayhe attributed to the low f.o.b. export price. This price is equal to 657 of thedomestic ex-factorv cost and ig deemed neressarv to rompensate for the hibh trans-portation cost. As part of a long-range market penetration strategy, the low.export nrice apnears Justifiable-

3.43 The domestic resouirce rnost of a unit of fore-if n exchange for the im-port substitution activities of TELCO and Ashok Leyland indicates that productionof reditim-heruv veh4r1el in TnMn for the domestIc market 4s definitely an econo-mic activity for these two firms. This competitiveness is essentially due to(i) the ability of TInd4an mannfact-uirerQ to atnnAarei7e produrtion of chassito two or three models; (ii) relatively low labor cost; and (iii) the hightransportat-ion cost- Plement in imports. The dome-tl re-urce cost fjgures

for the export activities are higher due to the lower prices of exports whichare necessary for market penetration. NevertlMl- if --- ----- the pro-

position that the opportunity cost of foreign exchange in India is about ".s.i - U - i't "" ,e n"'he exor ac-U-le v s are eLIUIIL VoIIo nL eveLa ""s erV

stage of export experience.

3.44 lie can thus conclude (a) that the medium/heavy commercial vehiclesmanufactured by the t.wo more efficient producers in India are competitivedespite the relatively high price of inputs and levies and that they wouldb-e even more compyetiti-ve if the Jrice of0 indigenous inputs were to drop tothe c.i.f. value of comparable imports; (b) that the production of medium/hleavy -vehicles both for export and une aomestic market at T1ET.IO-s and AsnokTeyland's scales of production is economic; (c) that there is very littlehias aaciLnst teuArtgLL1II L.LV1LeSj andti tIxAis i1U nexuart incentives are adequaue.

2. Light CoT-ii-i-iercial Veh'c'es

3.4, D)espite the ract that Bajaj Tempo mav be consinered the most efficientmanufacturer of commercial vehicles in India, the ex-factorv nrice is about 307higher than the c.i.r. value of an equivalent import. IThis is due to the factthat -- as pointed out in para. 3.24 -- cost of materials and bought-out partsare high primuarily because of tne smaii scaie or operation ann in additionthe manufacturer has unutilized capacitv due to unavailability of castings.IL thlis rirm were to obtain raw materials and components at internationalprices, its product prices would drop to about 5% above the c.i.f. price ofequivalent imports at today's level ot production. It production were toincrease from 3,500 to 8,000-9,000 vehlicles a vear, it is estimated that theprice of a vehicle would be about 3%o below the c.i.f. price of comparableimposts.

3.A6 Effective rates of protection for the im,pnort substituiting. activ-ities are 23% and 11% for the 1 and 1-112 tons trucks respectively and ther,qnpqti- rpmnsnrce oncts n,cr tnIt rof foreiern exchangp saved iF Ps. 9.46 undPs5;. .3nl respectivelv. For a relatively recent undertakinc, and at thie rtcr-rnr e rsale of nrnilirrinn- theqe are reasonabhle nrntprtcrn an(! cdomestic

resource cost levels and one can conclude that tinder nrevailing conditionsthe import subcticttting arlrity is ernnnnircally soundi The evnnrt nrtivxirx'on the other hand, does not fare as well. Domestic resource costs per initof foreIgn e-change earned ranae between Ps. 12.0 to 12.9 for both mTodels

rrl'ich is hligoher than the assuimed opportunitv cost of foreign exchange.uesnite-, ,-nort incen*tivs', the effect nrntnrtInn i^ -?' f-h'h i .far

less than thze effective protection afforded to thc irort sulh-titution activ-4tes(20.'". ThoIls does -ot miean th.at incre.ase3? 0ex,r.!r nc8-vsae1eJ

sinace the domestic resource cost ner unit of foreItgn excYlnge earned bin' ex-*ri,- vebi .c'esO ts QLCV onj the hi/41 ^hn I/a'. ilcA- 4tL does tOCiean is that as

long as the light cormmercial vehicle sector consists of small-scale producerr,,/roduct,,,zl~~Ve 4z ;ehic_ for exr,ort wil' 11 sl 4 SI-4 cost a..tSI-4t

T- -ep - n - J ITeep 'Pruc'-s

''-7 ThC nr0A.uC,4o of 4ecel-s an-d Jeep triucl.,s for thie lotrestufc markeet

is xtiite corinetitive at current levels of production and technology and furtlhercost reUL L . LUon o li aLk1:VOC1 bv i ,r ini JrtLL/V iAI"A tLIUL 1 *'!-L[Ii/thd . hI,Jw VtL

the product designs are at least 25 Years old and hhave little export potential.

F. Exports --

2 .4. The conmercial vehicle industry has made a nronising beginning inea.ri n g foreign exchange. Over the 1ls- tr-1--.,,- _4 --e ._ r~O CCIL CC Iil~C V L CI- IaO -L//LO :voit L -II-, -/, IL-I '0 Ut L A p U LL O IL L _ /ItI?~

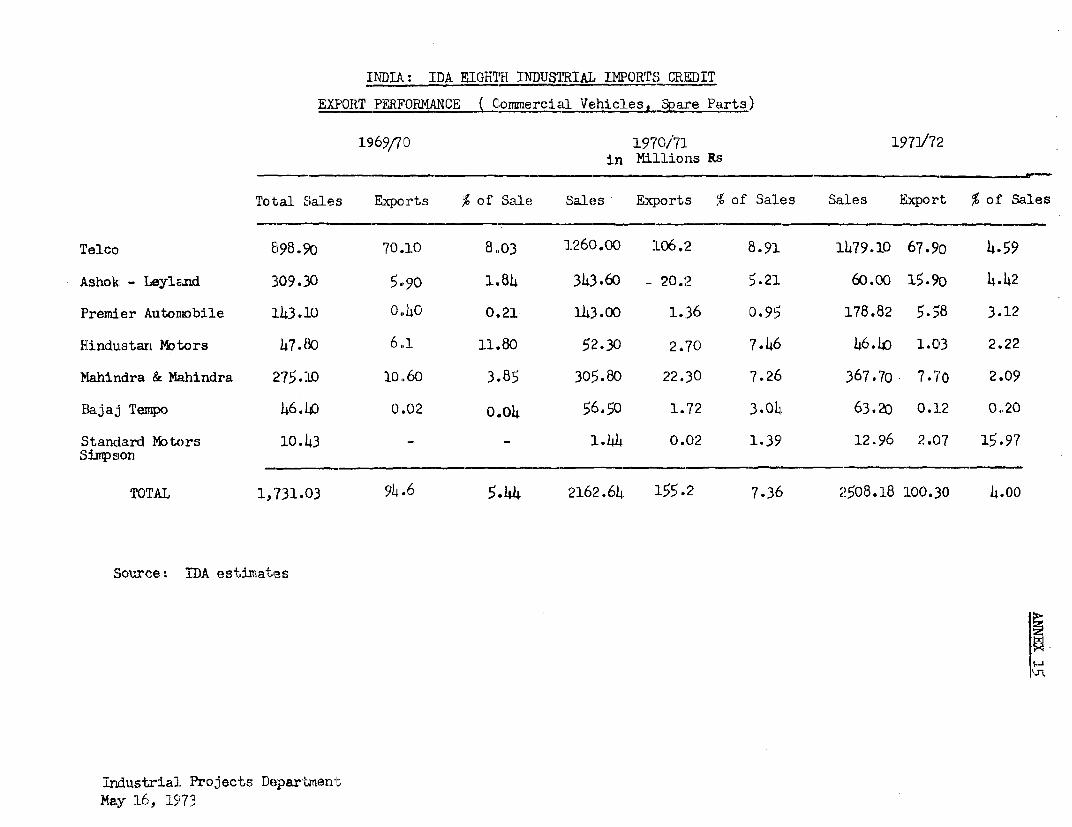

total output of commercial vehicles Is estimated at 5.5% covering over half oft te tct foeg 0±511 rqieLsoQe sUeLcLtLo r f Lor imports. r LarL C1ng

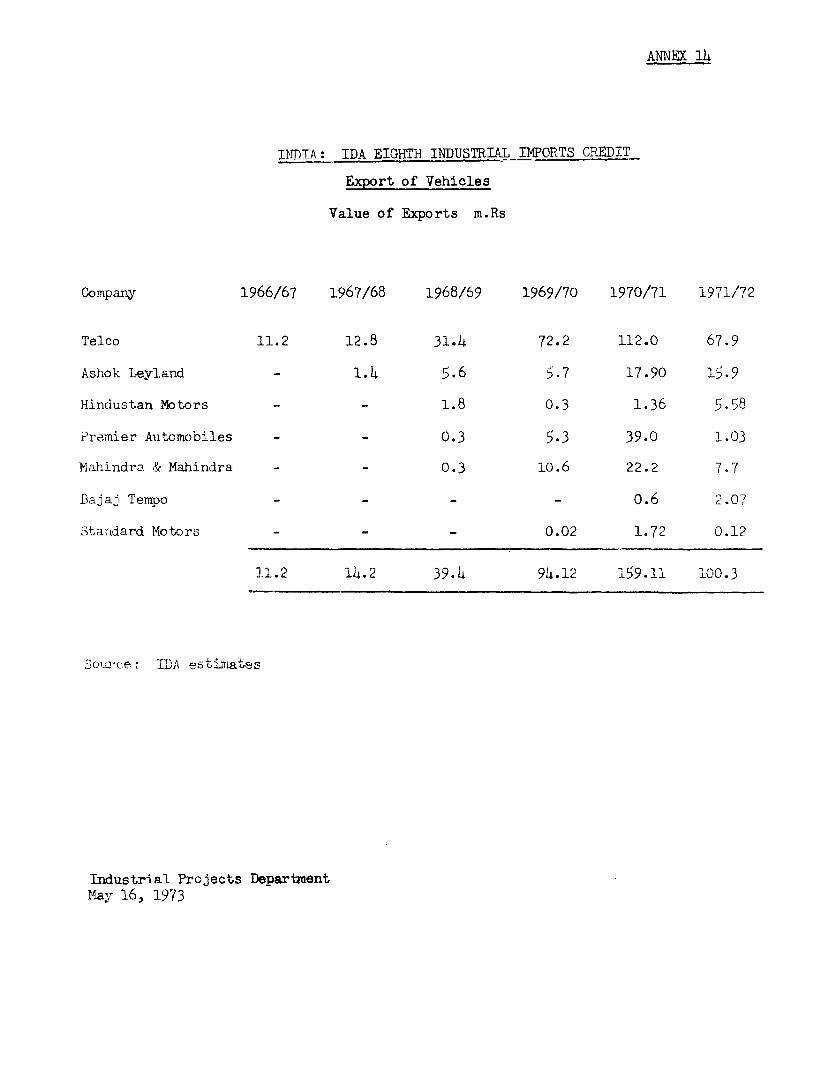

frorm about Es. 2 m7illion in 1964/65, exports reached a neok of some Rs. 160m illion in 1970/71 but dropped to Rs. 100 million in ll "MU" due to delays inrenewin- a trade agreement with Egypt, the largest importer of Indian trucks.Exnorts have been directed to over 20 countries in Arrica. Asia, tne MiddieEast and Eastern Europe. Over the period 1969-1972, four cotntries accountedfor about 33% or indian exports, Egypt (31.2%); Ceylon (26.30): Yugoslavia(13.7%') ; and Nigeria (11.7%). ks a rtule exports are made under bilateraltrade agreements. tELCO, Mahindra & Mahindra and kshok l.eyland account forabout 95% of all vehicle exports and TELCO is bv far the leading exnorterwn rh more than 70% of the total.

3.49 Export prices range trom ?() to 400/ below the domestic ex-factoryprices (Annex 13). In addition to the f.o.b. price, the exnorting firm receivesthe dutv and. excise tax draw-backs of about 13-167, the cash assistance bonuis

1/ See also Annexes 12, 13, 14, and 15.

- 23 -

of between ?0f-95-, snd thp preomfiim value of REP'P _/ rof ahbout i0nT The reali-zation from exports, therefore, is between 83% and 103% of the domestic ex-factorv nrire As wnasdiscussed in paras. 3.41 and 3.46 it 4, doubtful thatthere is anv economic justification for increasing the export incentivesalready in effect- Further export growth should he bae natrci>customers through improved design, better qxality and adherance to deliverypromises, stepped up .m-arketing efforts, better assessment of customer needas well as through price-reductions by improved operational efficiency ofthe vehicle manufacturers and ancillartes.

'i rn A1lthugh actlon_s ~1___ 1Us "ne _. @ t1 reur.. som t__r to ta'-e._..AX L 5 i 1 L X .' W1 1. ' L i t tu e: t U t L1!1 LU Ld'

effect, the three manufacturers which account for the bulk of India's vehicleexports -TJ. O ,AshokI l-;ln adI iahindria Ca 1'[1.LIda) ar-e J1t:'VL[e1lesS opti-

mistic about their ability to further penetrate markets abroad and have proV-e etheir e..c-norts to grow as follows:

Projected Exports of Commercial Vehicles, 9l72-i'ai7(in Rs. million)

1970/71 1l72/73 1974/75 1978/79 % of estimated Gross(actual) (est.) (prol.) (proj.) Prodiwtion (197j/79)

TELCO 106 110 150 210 10Ashok Levlan.,i 20) 1 8 25 40 8.TahIndra & Mahindra 22 12 15 20 3Others 7 10 15 30 5

Total 155 150 2-05 30n 3.3 (average)

3.5i E'Exports of Indian trucks and buses can assuredly be increasedfurther and economically at that. Not only are the three major exporters, par--ticularly TELCO, already quite competitive, but Indian vehicles have a nunmber ofother advantages in developing countries vis-a-vis competitive products fromindustrialized countries. Firstlv, the Indian market pattern for commercialvehicles and the most important components largely coincide with the pattern inin developing countries; secondly, the conditions in most developing countriesare similar to Indian conditions -- overloading, noor roads, severe climate --and thirdly. Indian vehicles are able to stand up well to extraordinary stresses.India also rates high as a manufacturer and user of those types and sizes oftrucks and buses that are the most popular in developing countries (Bedford,Dodge, Fargo, Leyland and Mercedes Benz).

2/ It miglht be argued that firms like TELCO that don't sell their REP's donot realize the resale premium of 50. T.he fact that L .LCO prefers toutilize the REP's for their own needs implies that to TELCO they areworth at least as muchU a probably more tnan thne resale value when usedto provide scarce imported inputs (thereby enhancing the exportabilityof their products). It seems reasonable, therefore, in trying to quantifythe incentive method provided by the REP's to assign a 50% premium above

teUnom.inal value -whether resold or'utilized by the recipient.

3.52 Any increase in exports will of course have to be closely coordinate(dwith plans to exp~and prouct'on to neet duomestic demand; these plans are dis-cussed further beloxw (paras. 4.01-4.04). At present the three major vehicleexporters have LLttle or uo excess capacity. Although exports are only marginal-ly attractive financially, it was gratifying to learn that company managementsiunderstana tue national need to earn foreign exchange and are more than willingto cooperate to the extent possible. Thus, for example, TELCO has accepted theobligation to export 2070 or its recently license(d incremental capacity and AsshnkLevyand has made a similar commitment.

3.53 In addition to the export Potential of complete vehicles in develop-ing countries, there are good opporttnitles for exporting components to developedcountries, esnecially for discontinued mnodels requiring relatively short pro-luction runs rhich are uneconomical to produce in developed countries. A numberof Indian producers are competitive both as to quality and price in castings,forgings and machined parts which have a high skilled labor content. The mainimpediment up to now seems to have been a lack of marketing effort. There isa worldwide shortage of castings and forgings andi large manufacturers both inthe U.S. and Europe are searching for new sources. The fact that there appearsto be no strong interest in India yet indicates that India has not seized theopportunity to make potential buvers awiare of Indian prices ond qualitv. Indi.nTrade Promotion Offices -- perhaps one in Detroit and one in Europe to start --cotild act as two-way channels promoting both the export of Indian vehicle com-nonents as well, as a flow of technical- assistance to India.

3.! 5A Finally, while there seems to be no need to fujrther increase exportincentive.s, thev could certainly be rendered more effective. The cash assistancescheme appears nowq to be operating; much more smoothlv than in the past; of thl'amouniit due, 7n7 is now remitted against shinping bills and thie balance againstforeir,n ex:change receipts. But there are considerable nroblems with the diit)-dIraw-T,nach, The exporter has to ne-otiate for each shinment the amount of dl!ti'esand excise ' txes eligible for recovery. This is time-consumiTng and results i.nconsiderable delays in obtaining the drawback. Tt would be desirable to esta--blish an ad valorem rate for commercial vehicles i7hich could be negotiatedannually.

TV. FYPASTlN PLT.TS

.I1 The expected demand and sunply for commercia,,l voehicl.es through 1'79are pro-jected in Annexes 16 and 17 an(d are briefly summarizer' in this section.

P,. VMedium/ev Vehicles