… or in other words, we specialize in... The Alliance Group is an insurance marketing and field...

34

-

Upload

samson-green -

Category

Documents

-

view

213 -

download

0

Transcript of … or in other words, we specialize in... The Alliance Group is an insurance marketing and field...

… or in other words, we specialize in...

The Alliance Group is an insurance marketing and field underwriting

organization that represents certain insurance companies that are

particularly focused on income and asset preservation…

Estate Protection(Business and Personal)

When we say “Estate”, there is typically a partition between business and personal assets but it’s the liquid parts that keeps things moving

in a time of crisis.

Checking and Savings

401-K and IRA values

Equity in the Business/Home (potential lines of credit)

Statistically, which of the these events have the most negative impact to your Estate, especially your liquidity, when they occur?

Death?

Critical Illness?

Disability?

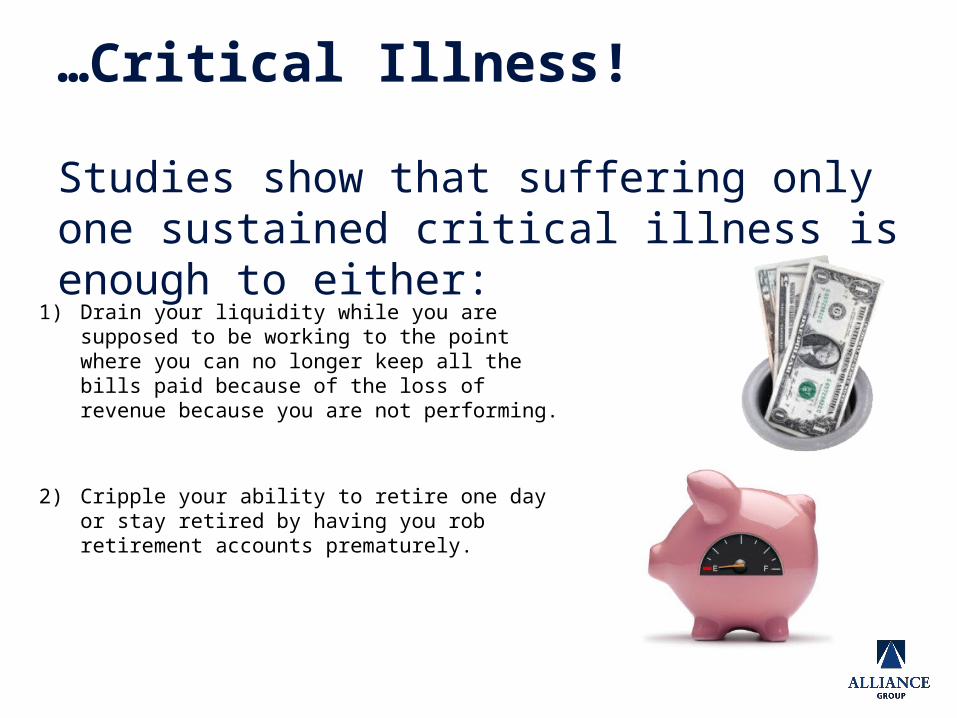

1) Drain your liquidity while you are supposed to be working to the point where you can no longer keep all the bills paid because of the loss of revenue because you are not performing.

2) Cripple your ability to retire one day or stay retired by having you rob retirement accounts prematurely.

…Critical Illness!

Studies show that suffering only one sustained critical illness is enough to either:

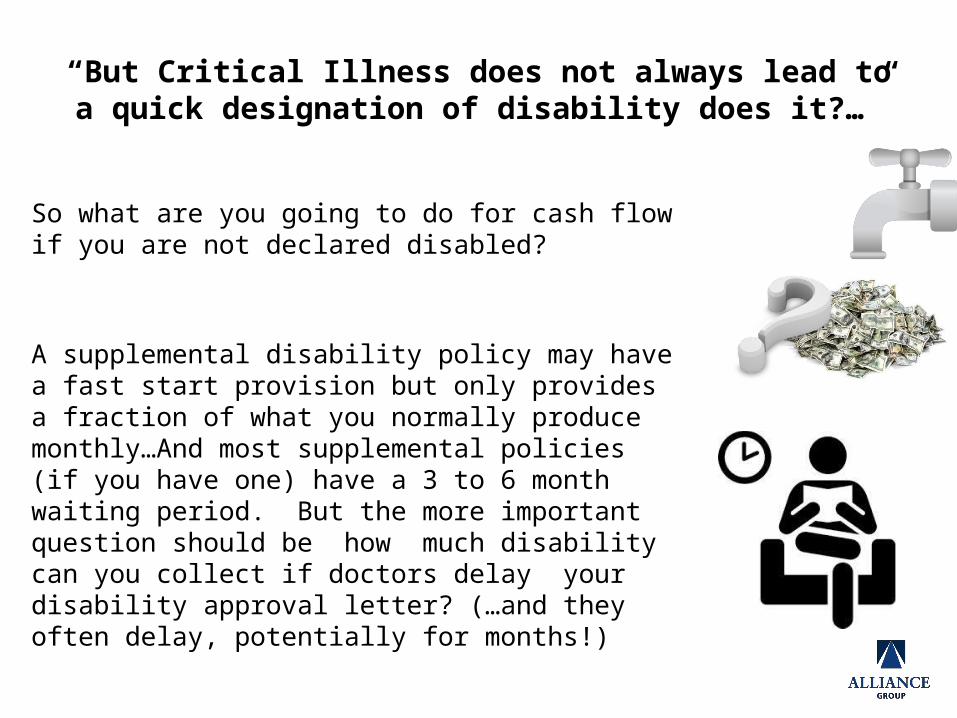

“But Critical Illness does not always lead to a quick designation of disability does it?…”

So what are you going to do for cash flow if you are not declared disabled?

A supplemental disability policy may have a fast start provision but only provides a fraction of what you normally produce monthly…And most supplemental policies (if you have one) have a 3 to 6 month waiting period. But the more important question should be how much disability can you collect if doctors delay your disability approval letter? (…and they often delay, potentially for months!)

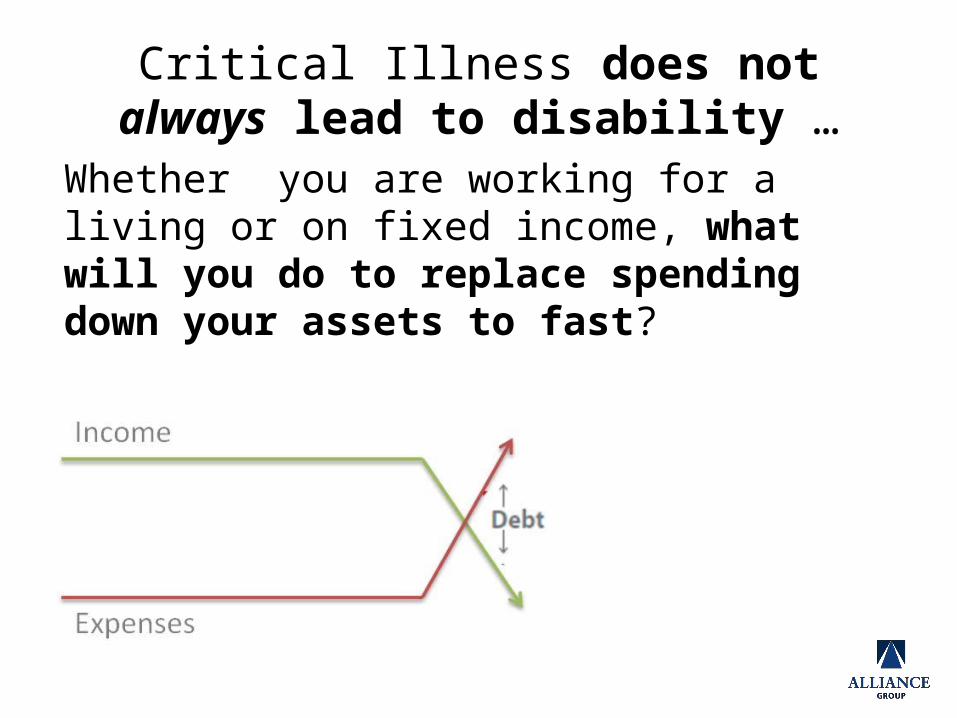

Critical Illness does not always lead to disability …

Whether you are working for a living or on fixed income, what will you do to replace spending down your assets to fast?

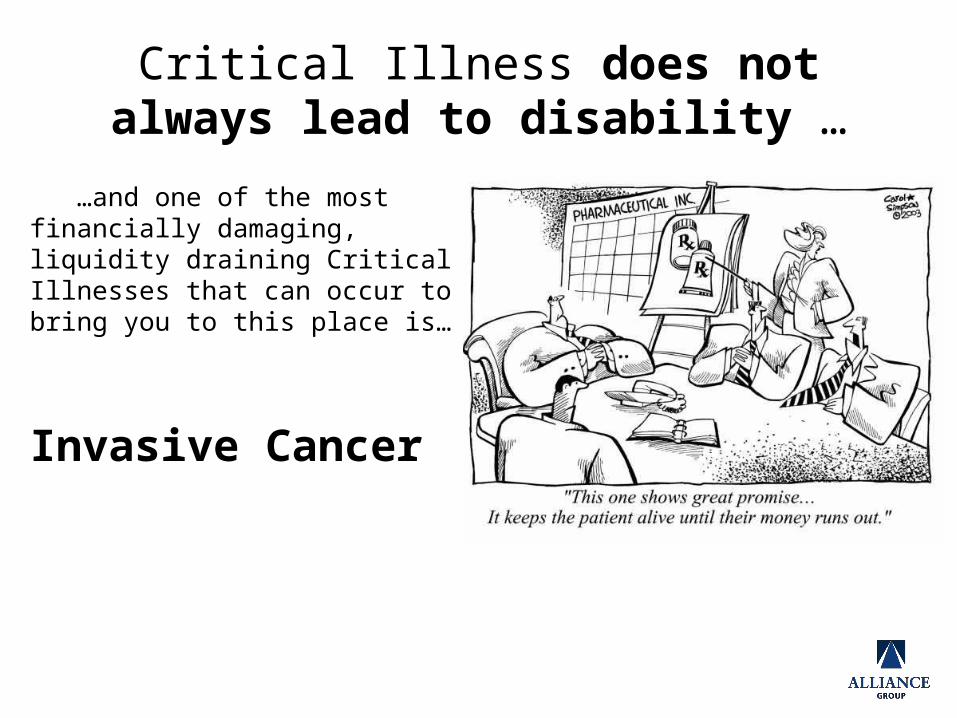

Critical Illness does not always lead to disability …

…and one of the most financially damaging, liquidity draining Critical Illnesses that can occur to bring you to this place is…

Invasive Cancer

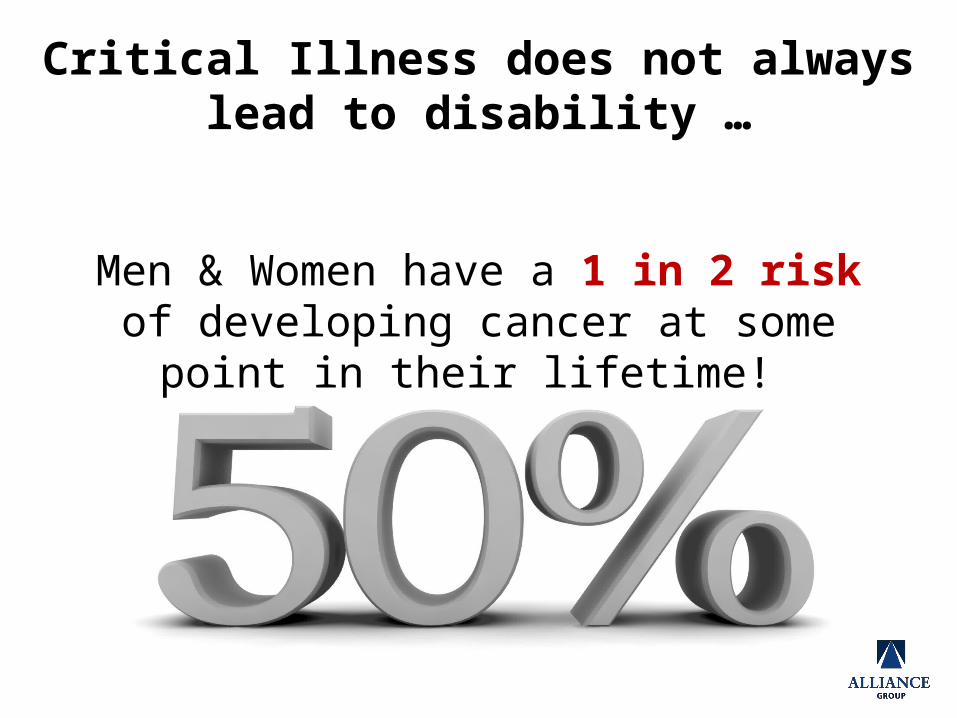

Critical Illness does not always lead to disability …

Source: “Cancer Facts and the War on Cancer “. LIMRA.2007

Men & Women have a 1 in 2 risk of developing cancer at some point in their lifetime!

Critical Illness does not always lead to disability …

Other Critical Illnesses can strike anyone at anytime…

…even if no current family members have fought a critical illness before.

Today’s chemically laced food and water supply are responsible for a growing number of health conditions.

Critical Illness does not always lead to disability …

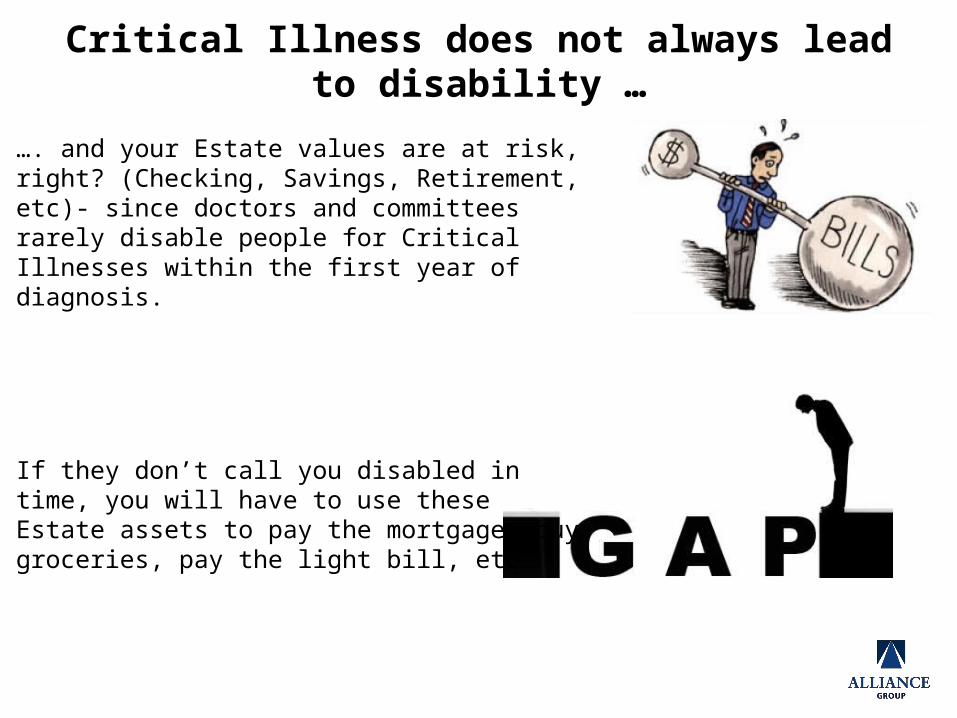

…. and your Estate values are at risk, right? (Checking, Savings, Retirement, etc)- since doctors and committees rarely disable people for Critical Illnesses within the first year of diagnosis.

If they don’t call you disabled in time, you will have to use these Estate assets to pay the mortgage, buy groceries, pay the light bill, etc…

Critical Illness does not always lead to disability …

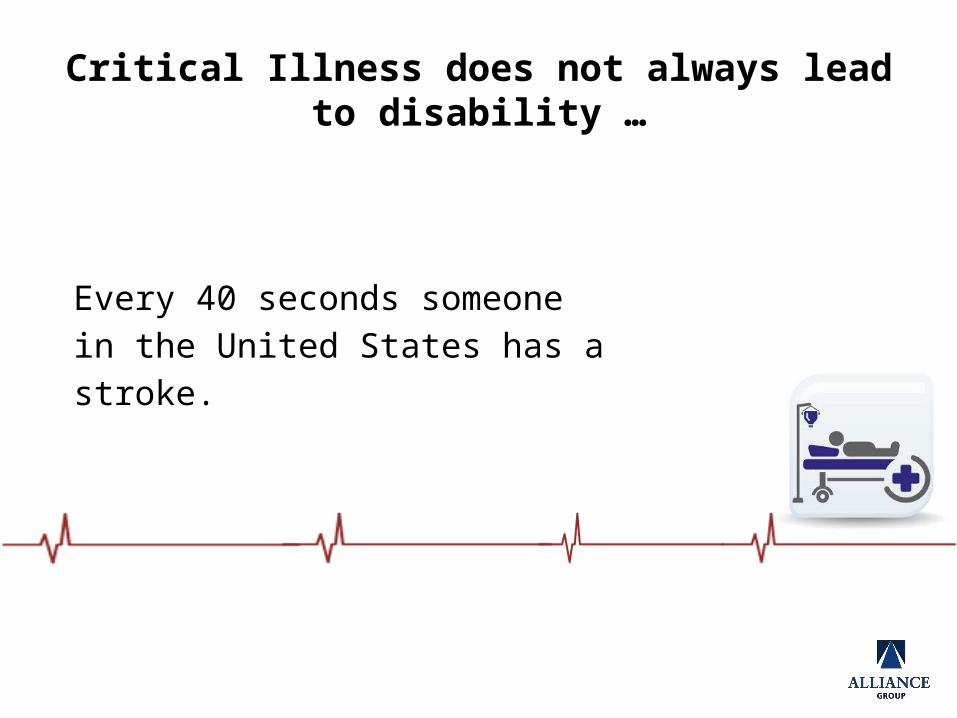

Every 40 seconds someone in the United States has astroke.

Source: American Heart Association. “Heart Disease and Stroke Statistics” 2009

Critical Illness does not always lead to disability …

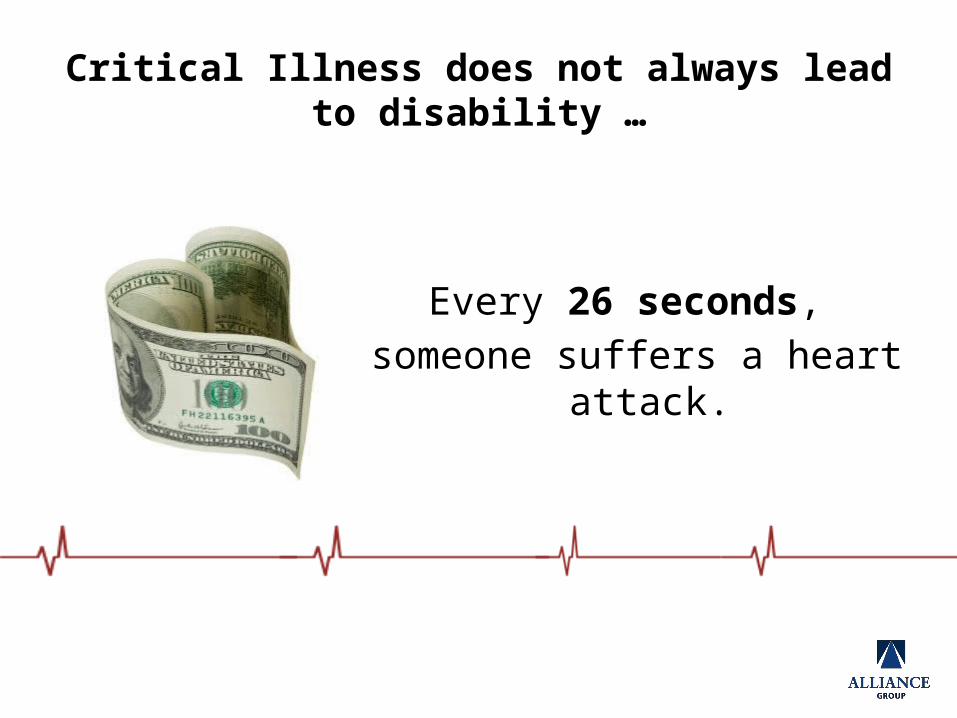

Source: American Heart Association. “Heart Disease and Stroke Statistics.” LIMRA. 2007

Every 26 seconds, someone suffers a heart attack.

Critical Illness does not always lead to disability …

About 45% of heart attack victims are UNDER age of 65.

Source: Nat’l Heart, Lung & Blood Institute. “AHA Statistical Update, 2013

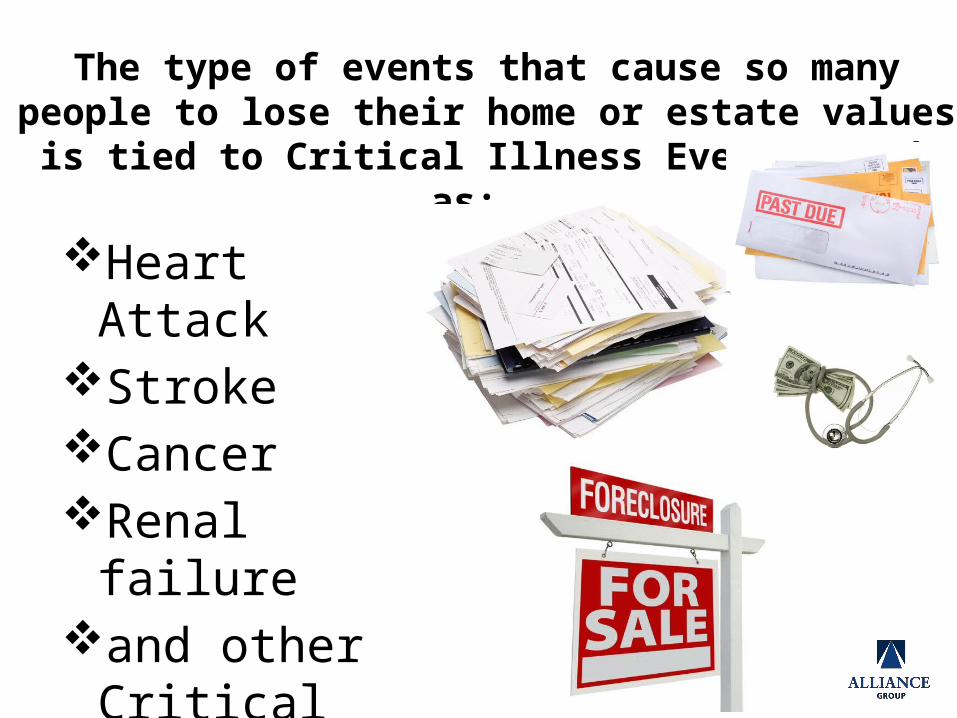

Heart AttackStrokeCancer Renal failureand other Critical

Events…

The type of events that cause so many people to lose their home or estate values is tied to Critical Illness Events, such as:

Many lose their health insurance during a Critical Illness…

The cost of health insurance will at the least double with Obama Care and experts believe it

will triple in the next 24 months.

No subsidies are available if your combined household income is over 94,000 based on

current threshold levels.

No one is giving you a helping hand so keeping this very important monthly obligation paid will

be difficult when cash flow is affected.

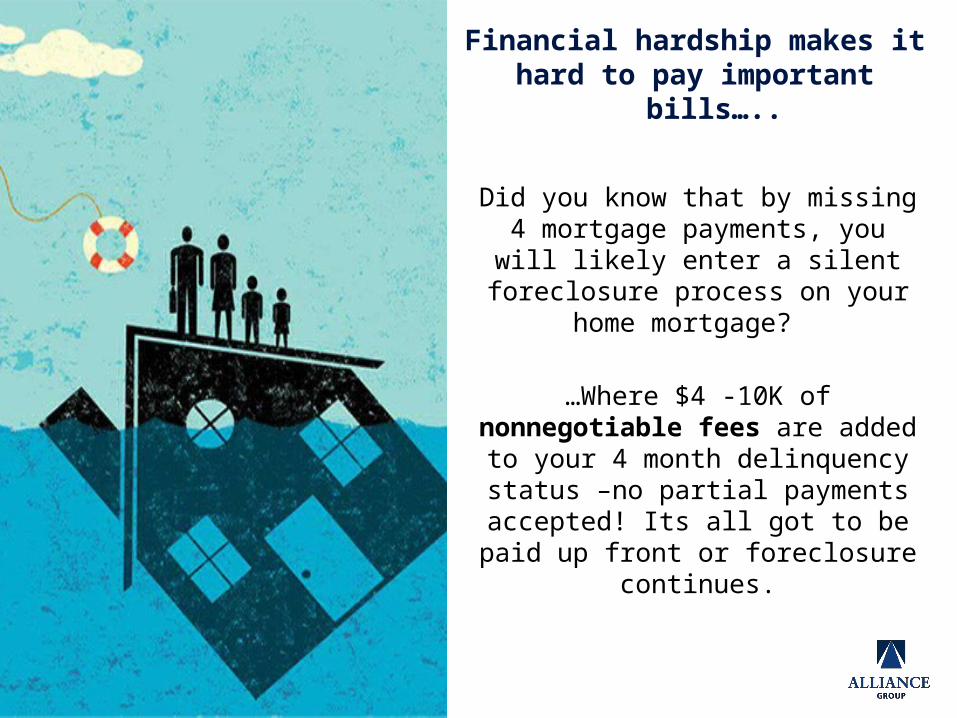

LEFT HIGH & DRY

Did you know that by missing 4 mortgage payments, you will likely

enter a silent foreclosure process on your home mortgage?

…Where $4 -10K of nonnegotiable fees are added to your 4 month delinquency status –no partial

payments accepted! Its all got to be paid up front or foreclosure

continues.

Financial hardship makes ithard to pay important bills…..

Source: http://content.healthaffairs.org/content/early/2005/02/02/hlthaff.w5.63.full.pdf+html

Approx. 56.5% (more than 1 out of 2) of all bankruptcies in the last 5 years were medically related.

70% (7 out of 10) of those bankruptcies actually had workplace benefits at the time of the critical event but lost them due to cash flow

problems afterwards.

So, we have talked about the problem. Now let’s talk about a

potential solution, assuming you can be approved for it.

The Solution Is To Have Coverage For Death -But Also For Critical Events.

#1 Our Estate Protection Life Insurance with Living Benefits does not require a doctor to declare you disabled, rather just declare there has been a life threatening critical or chronic illness including but not limited to heart attack, stroke, detection of life threating cancer and other covered critical or chronic illness events…

#2 You are about to see that it also pays a large up front amount instead of small monthly amounts especially helpful on Critical Illnesses, so you can have the money you need to help keep you in your “current” lifestyle .

One way to cover your business and personal Estate is with many separate policies…..

• Death= Policy #1• Cancer= Policy #2• Heart attack=Policy #3• Accident=Policy #4• Etc…..

PREMIUM DUE

PREMIUM DUE

PREMIUM DUE

PREMIUM DUEPREMIUM DUE

Let’s talk about funding options

…but also create up front serious cash benefits upon diagnosis of certain Critical Illnesses even if your doctor doesn’t call you “Disabled”.

These cash benefits are paid to preserve your estate and keep things running, all for about the cost of regular life insurance!

I am about to show you some custom illustrations on how we might cover you if you were to die…

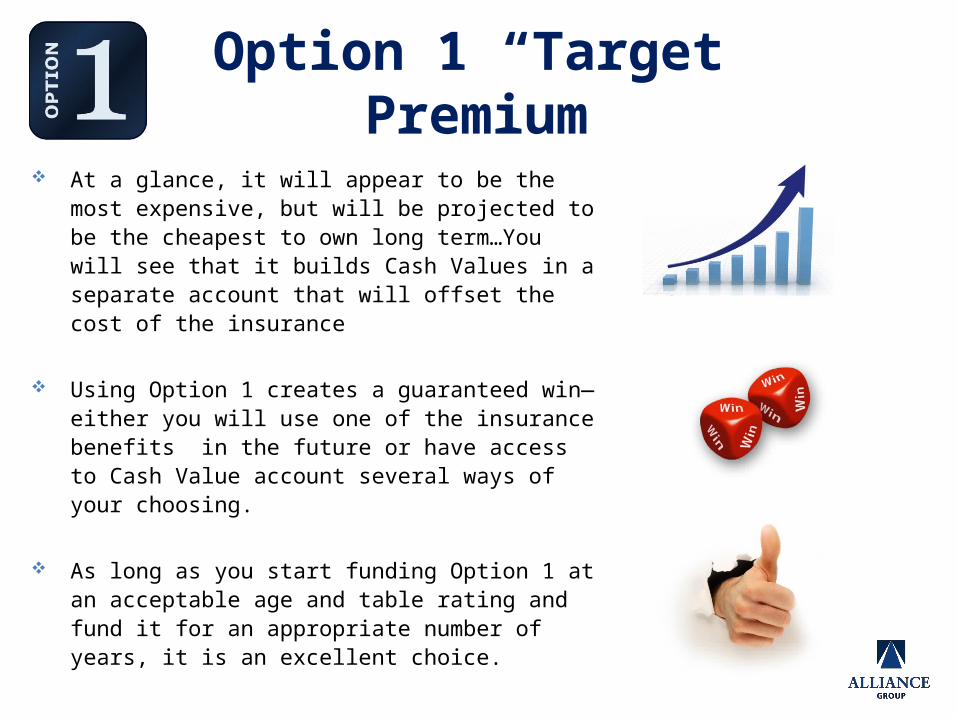

Option 1 “Target” Premium

At a glance, it will appear to be the most expensive, but will be projected to be the cheapest to own long term…You will see that it builds Cash Values in a separate account that will offset the cost of the insurance

Using Option 1 creates a guaranteed win—either you will use one of the insurance benefits in the future or have access to Cash Value account several ways of your choosing.

As long as you start funding Option 1 at an acceptable age and table rating and fund it for an appropriate number of years, it is an excellent choice.

As an example, after the first few years, many clients loan themselves money from the Cash Value in the policy and accelerate or even help to pay off their mortgage early,

saving thousands even multiple thousands of dollars in mortgage interest.

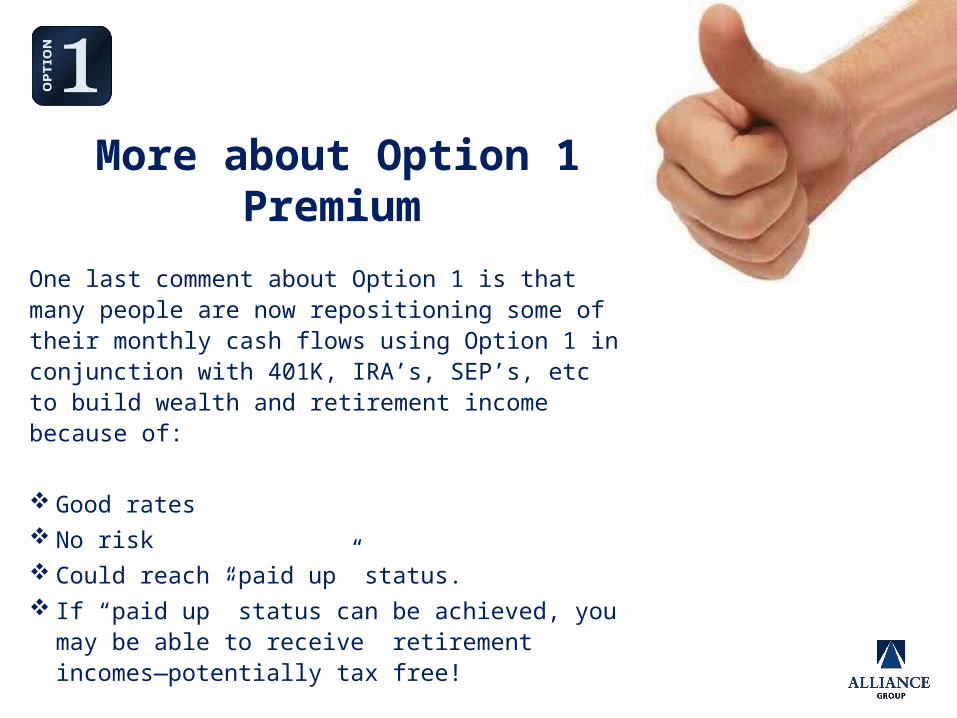

More about Option 1 Premium

One last comment about Option 1 is that many people are now repositioning some of their monthly cash flows using Option 1 in conjunction with 401K, IRA’s, SEP’s, etc to build wealth and retirement income because of:

Good rates No risk Could reach “paid up” status. If “paid up” status can be achieved, you may be

able to receive retirement incomes—potentially tax free!

More about Option 1 Premium

Option 2 “Specified” Premium

Option 2 has a lower monthly premium requirement since it will not be permanent or reach paid up status. It has same death and living benefits as Option 1 but has a predictable specified period of coverage allowing for lower premiums.

Option 2 cannot not achieve refund of premium or offer monthly income supplements in retirement--the focus is coverage for a certain period.

You can upgrade from Option 2 to Option 1 later under certain

circumstances

Option 3 “Minimum” Premium

Gives the same Death and Living Benefits as Option 1 and Option 2 but has a significantly reduced period of coverage, (typically 15 years protected rate.)

Like Option 2, no significant policy cash values for savings or retirement will build up at any time at this level—its’ just the coverage--just for a shorter duration policy period.

Purpose of this meeting…

The purpose of this meeting is to find a fit. It’s got to be a fit for you.

Then, we’ll see if it is a fit for the carrier.

Purpose of this meeting…

Remember, you can change it later, we just need to find a place to start and maybe take advantage of avoiding the blood and urine exam on certain coverage levels.

Purpose of this meeting…

Let’s now look at two or three funding options. Regardless which of these funding options you might try, the coverage is virtually the same.

We are looking for a place to help you “try”…Today will not be a “buy” because there is no policy available in this visit.

Let’s look at the Illustrations!