ΣΕΜΙΝΑΡΙΟ Φ.Π.Α Neophytos Neophytou - ICPAC December 2013. Report on Cyprus by the...

48

ΣΕΜΙΝΑΡΙΟ Φ.Π.Α Neophytos Neophytou - ICPAC December 2013. Report on Cyprus by the Global Forum on Tax Transparency and Exchange of Information for Tax Purposes

-

Upload

roderick-washington -

Category

Documents

-

view

216 -

download

2

Transcript of ΣΕΜΙΝΑΡΙΟ Φ.Π.Α Neophytos Neophytou - ICPAC December 2013. Report on Cyprus by the...

ΣΕΜΙΝΑΡΙΟ Φ.Π.Α

Neophytos Neophytou - ICPAC

December 2013.

Report on Cyprus by the Global Forum on Tax Transparency and Exchange of Information

for Tax Purposes

What is the Global Forum

3

WHAT IS THE GLOBAL FORUM

The Global Forum has been the multilateral framework within which work in the area transparency and exchange of information has been carried out by both OECD and non- OECD economies since 2000.

The Global Forum was originally established in 2001 by OECD member countries along with a number of participating partners and has been a driving force behind the development of the international standard of transparency and exchange of information for tax purposes.

In response to the G20 Leaders’ call for jurisdictions to adopt high standards of transparency and information exchange in tax matters, the Global Forum was restructured as a consensus-based organisation where all members are on an equal footing. All OECD countries, G20 economies and jurisdictions participating in the existing Global Forum were invited to become members.

4

WHAT IS THE GLOBAL FORUMWith an ambitious agenda to improve transparency and exchange of information for tax purposes, the Global Forum agreed on a three-year mandate to promote the rapid implementation of the standard through the peer review of all its members and other jurisdictions relevant to its work.

The Global Forum now includes 120 member jurisdictions and the European Union, together with 12 observers, making it the largest tax group in the world.

Membership of the Global Forum is open to all jurisdictions willing to: (i) commit to implement the international standard on transparency and exchange of information, (ii) participate and contribute to the peer review process, and (iii) contribute to the budget. Its current membership includes all G20 countries, OECD member countries, off-shore financial centres and many developing countries, all of whom have committed to adhere to the international standard.

5

Peer Review Group (PRG)

All members of the Global Forum, as well as jurisdictions identified by the Global Forum as relevant to its work, undergo peer reviews of their legal and regulatory framework for the exchange of information in tax matters and the implementation of the standard in practice.

The peer review process is overseen by a 30-member Peer Review Group (PRG), which is chaired by Mr. François d’Aubert from France, assisted by four vice-chairs (India, Japan, Singapore and Jersey).

The PRG meets three to four times a year on average, and discusses the peer review reports that are finally adopted by Global Forum members.

6

Membership of PRG group

The full membership of the PRG is:

Argentina Bahamas, The Brazil

British Virgin Islands Cayman Islands China

France Germany India

Indonesia Isle of Man Italy

Japan Jersey Korea

Luxembourg Malaysia Malta

Mauritius Mexico Netherlands

Norway St. Kitts and NevisSamoa

Singapore South Africa Spain

Switzerland United Kingdom United States

7

EVALUATION PROCESS

The evaluation of a jurisdiction’s compliance to the standard is based on the Assessment Criteria. In all peer review reports, recommendations for remedial action can be made where relevant. During Phase 1 reviews, each of the ten elements receives a determination, which can be: “The element is in place”, “The element is in place, but certain aspects of the legal implementation of the element need improvement”, or “The element is not in place”.

Where a jurisdiction does not have in place elements which are crucial to it achieving effective exchange of information, the jurisdiction will not move to a Phase 2 review until it has acted on the recommendations made. During Phase 2 reviews, each of the essential element is rated as “compliant”, “largely compliant, “partially compliant”, or “noncompliant”. In addition, a jurisdiction that has completed both Phase 1 and Phase 2 reviews is assigned with an overall rating, assessing the general level of compliance with the standard.

FINDINGS DURING HE 1ST AND 2ND PHASE

REVIEW FOR CYPRUS

9

A AVAILABILITY OF INFORMATION

A.1. Jurisdictions should ensure that ownership and identity information for all relevant entities and arrangements is available to their competent authorities.

CYPRUS RATING – Partially Compliant

A.2. Jurisdictions should ensure that reliable accounting records are kept for all relevant entities and arrangements.

CYPRUS RATING – Non Compliant

A3. Banking information should be available for all account-holders.

CYPRUS RATING – Compliant

10

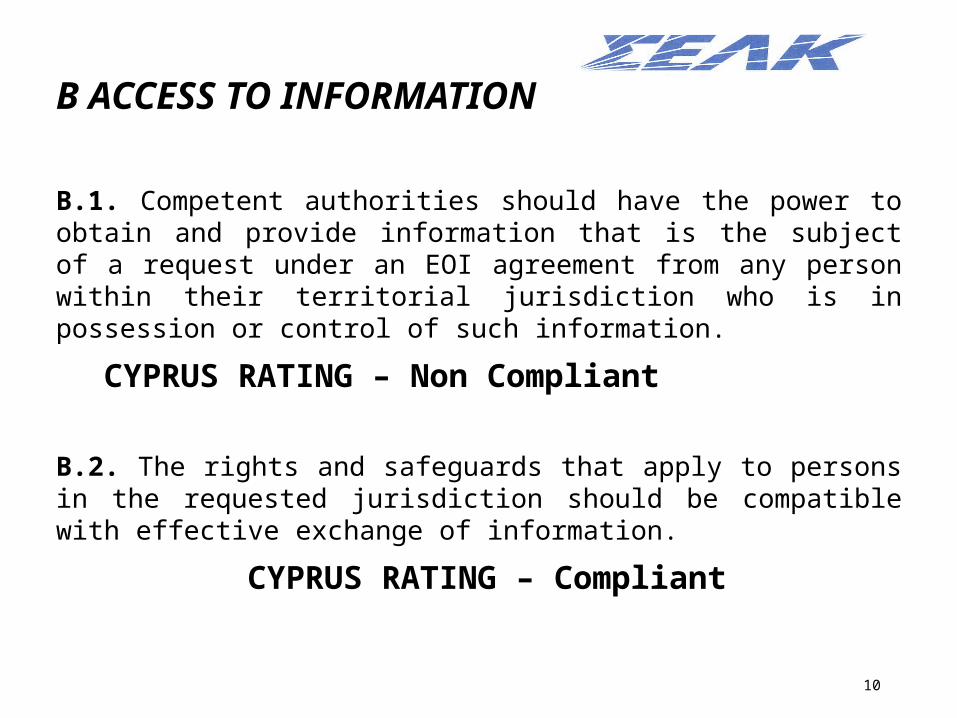

B ACCESS TO INFORMATION

B.1. Competent authorities should have the power to obtain and provide information that is the subject of a request under an EOI agreement from any person within their territorial jurisdiction who is in possession or control of such information.

CYPRUS RATING – Non Compliant

B.2. The rights and safeguards that apply to persons in the requested jurisdiction should be compatible with effective exchange of information.

CYPRUS RATING – Compliant

11

C EXCHANGING INFORMATION

C.1. EOI mechanisms should provide for effective exchange of information.

CYPRUS RATING – Compliant

C.2. The jurisdictions’ network of information exchange mechanisms should cover all relevant partners.

CYPRUS RATING – Largely Compliant

C.3. The jurisdictions’ mechanisms for exchange of information should have adequate provisions to ensure the confidentiality of information received.

CYPRUS RATING – Compliant

12

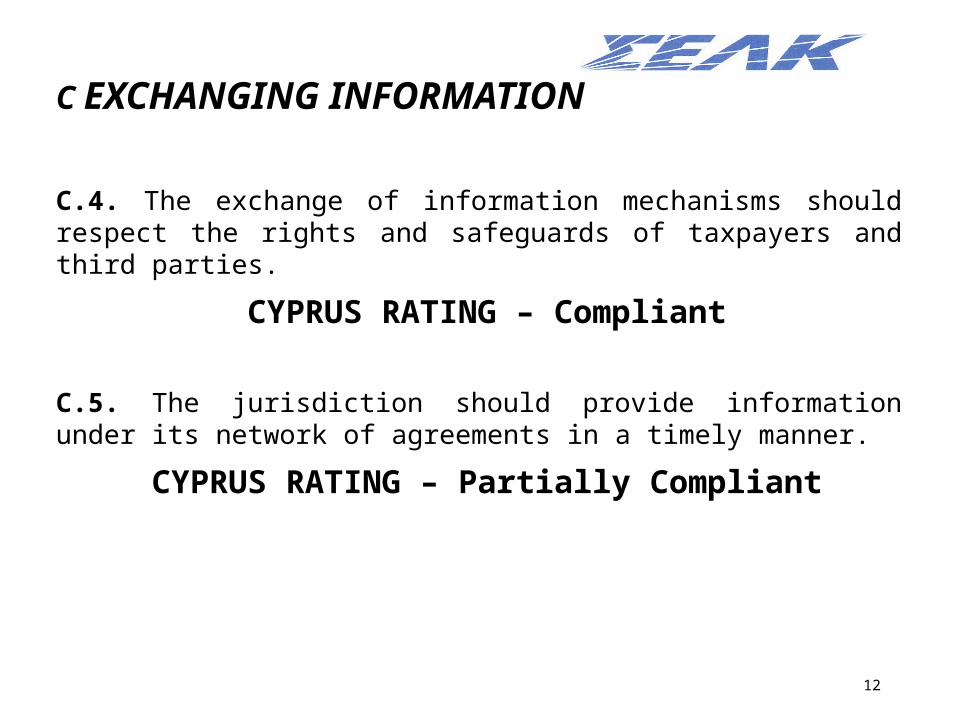

C EXCHANGING INFORMATION

C.4. The exchange of information mechanisms should respect the rights and safeguards of taxpayers and third parties.

CYPRUS RATING – Compliant

C.5. The jurisdiction should provide information under its network of agreements in a timely manner.

CYPRUS RATING – Partially Compliant

13

REASONS FOR THE RATING review period 1.7.2009 – 30.6.2012Appropriate legislation on certain matters not in place during the review period

Compliance rate for income tax return filings 35%

Compliance rate for annual returns filed with the Registrar of Companies 23%

Response time to exchange of information significantly out of the time allowed which is 90 days

Responses whether foreseeable relevant

14

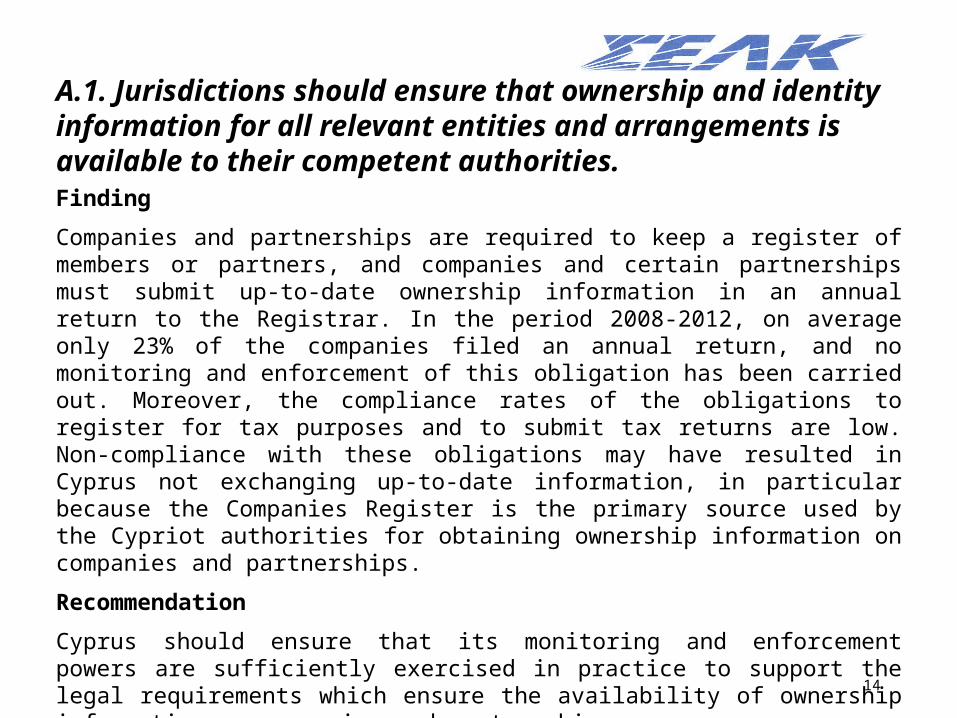

A.1. Jurisdictions should ensure that ownership and identity information for all relevant entities and arrangements is available to their competent authorities.Finding

Companies and partnerships are required to keep a register of members or partners, and companies and certain partnerships must submit up-to-date ownership information in an annual return to the Registrar. In the period 2008-2012, on average only 23% of the companies filed an annual return, and no monitoring and enforcement of this obligation has been carried out. Moreover, the compliance rates of the obligations to register for tax purposes and to submit tax returns are low. Non-compliance with these obligations may have resulted in Cyprus not exchanging up-to-date information, in particular because the Companies Register is the primary source used by the Cypriot authorities for obtaining ownership information on companies and partnerships.

Recommendation

Cyprus should ensure that its monitoring and enforcement powers are sufficiently exercised in practice to support the legal requirements which ensure the availability of ownership information on companies and partnerships

15

A.1. Jurisdictions should ensure that ownership and identity information for all relevant entities and arrangements is available to their competent authorities.Finding

A clear obligation on trustees to have information available on the other trustees, settlors and beneficiaries of the trust(s) with respect to which they act as a trustee, is only in force since 1 January 2013.

Recommendation

Cyprus should monitor the practical implementation of the recently introduced requirement on trustees to keep comprehensive identity information on trusts.

16

A.2. Jurisdictions should ensure that reliable accounting records are kept for all relevant entities and arrangements.Finding

Accounting records have not been available in a number of cases, in particular where the person required to keep the accounting records did not comply with its general obligations to submit tax returns and/or annual returns to the Companies Registrar.

Recommendation

Cyprus should ensure that reliable accounting records, including underlying documentation, are being kept by all relevant entities and arrangements for a period of at least five years.

17

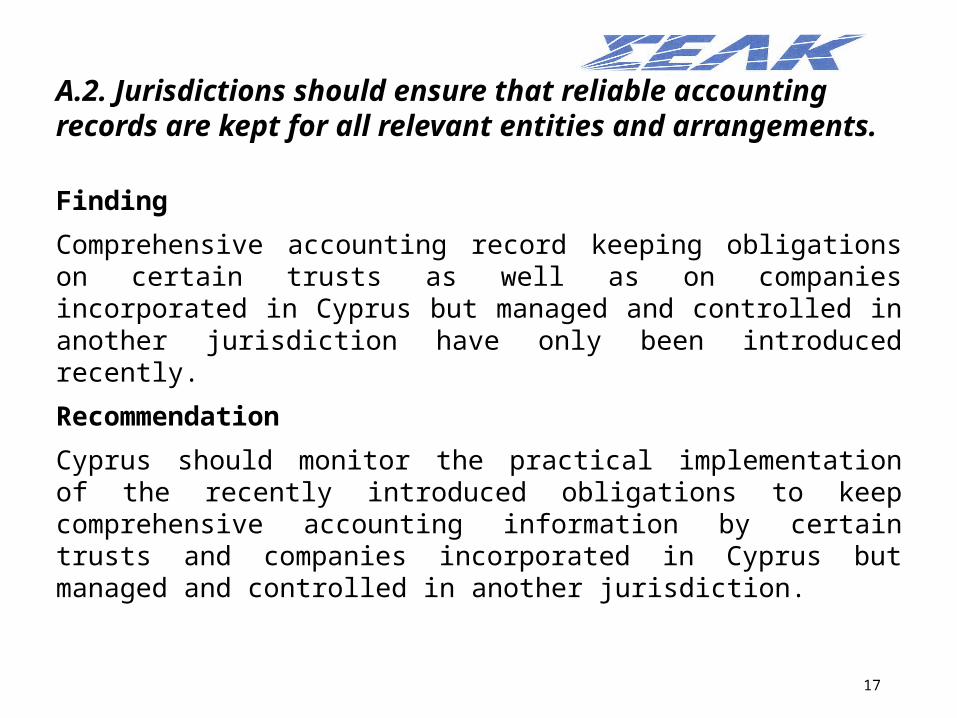

A.2. Jurisdictions should ensure that reliable accounting records are kept for all relevant entities and arrangements.Finding

Comprehensive accounting record keeping obligations on certain trusts as well as on companies incorporated in Cyprus but managed and controlled in another jurisdiction have only been introduced recently.

Recommendation

Cyprus should monitor the practical implementation of the recently introduced obligations to keep comprehensive accounting information by certain trusts and companies incorporated in Cyprus but managed and controlled in another jurisdiction.

18

B.1. Competent authorities should have the power to obtain and provide information that is the subject of a request under an EOI agreement from any person within their territorial jurisdiction who is in possession or control of such information.

Finding

The Cypriot competent authority did not use its specific information gathering powers to obtain information from ‘third parties’ other than banks, i.e. service providers such as lawyers, which may have had the information requested. In addition, these specific information gathering powers, which include the written consent of the Attorney-General, have been used to obtain information from a bank directly in only a limited number of cases. This may have contributed to delays in responding to EOI requests.

Recommendation

Cyprus should use its information gathering powers to obtain information from all potential information holders, including directly from banks and other third parties, where appropriate.

19

B.1. Competent authorities should have the power to obtain and provide information that is the subject of a request under an EOI agreement from any person within their territorial jurisdiction who is in possession or control of such information.Finding

The relatively high level of non-compliance by Cypriot taxpayers in responding to letters to provide information has not effectively been dealt with in terms of an effective use of the available compulsory powers. This may have specifically impacted the obtaining of bank information from Cypriot taxpayers.

Recommendation

Cyprus should exercise its compulsory powers more effectively in exchange of information cases where information is not produced, in particular in respect of bank information.

20

C.5. The jurisdiction should provide information under its network of agreements in a timely manner.Finding

During the three-year review period, Cyprus has been able to send final responses within 90 days in less than 10% of the cases, and almost 80% of the cases have been responded to after 180 days or are still outstanding. According to the Cypriot authorities, of the 929 requests received, 15% have not received a response at all during the three-year review period, while another 25% have received a partial response.

Recommendation

Cyprus should ensure that it responds to EOI requests in a complete and timely manner.

ACTIONS WHICH HAVE ALREADY BEEN TAKEN

BY CYPRUS

22

Legislation which has been introduced

A1 - Ownership and Identity Information The Companies Law which restricts the right of companies to issue bearer share warrants to only publicly listed companiesThe Service Providers Law which obliges trustees to have information on trustees, settlors and beneficiaries of trust

23

Legislation which has been introduced

A2 - Accounting RecordsTax legislation to include an obligation to keep books even in case of dividends and interest (thus to include trusts)Tax legislation on filing of tax returns by Cyprus incorporated but not Cyprus tax resident companies Tax Law and Company Law so that there is a specific obligation to keep underlying documentation and in the case of the Companies Law to keep the information for at least 6 years (the same as in the case of the tax laws)

24

B1 - Competent Authority’s Ability to Obtain and Provide Information

Request information from the taxpayer even if no tax returns have been filedUse of specific gathering powers to obtain information from third parties like banks, lawyers, service providers

ACTIONS WHICH STILL HAVE TO BE TAKEN BY

CYPRUS

26

Special Committee on Exchange of Information MattersConsists of Representatives of

Inland Revenue Department

Ministry of Finance

ICPAC

Bar Association

Cyprus Securities and Exchange Commission

CIPA

Registrar of Companies

An action plan was adopted on 6 December 2013 and has already been placed into effect

Continuous monitoring of implementation process

27

Actions to be taken – Reliable Statistics

Eliminate from tax Register of Taxpayers companies which have been liquidated or struck off (in cooperation with Registrar of Companies)

Place on a special list companies which have failed to pay the levy of €350 to the Registrar of Companies based on information to be received from the Registrar of Companies (IRD will manage tax compliance on these companies separately)

For all remaining companies which did not file tax returns upto the year 2011 IRD will send letters requesting compliance within 60 days otherwise legal action against the directors and the company

Simplified returns for companies which have no obligation to file tax returns because they had no income, as specified in the law

Simplified returns for Cyprus incorporated not tax resident companies

Specific actions for clients contact has been lost

28

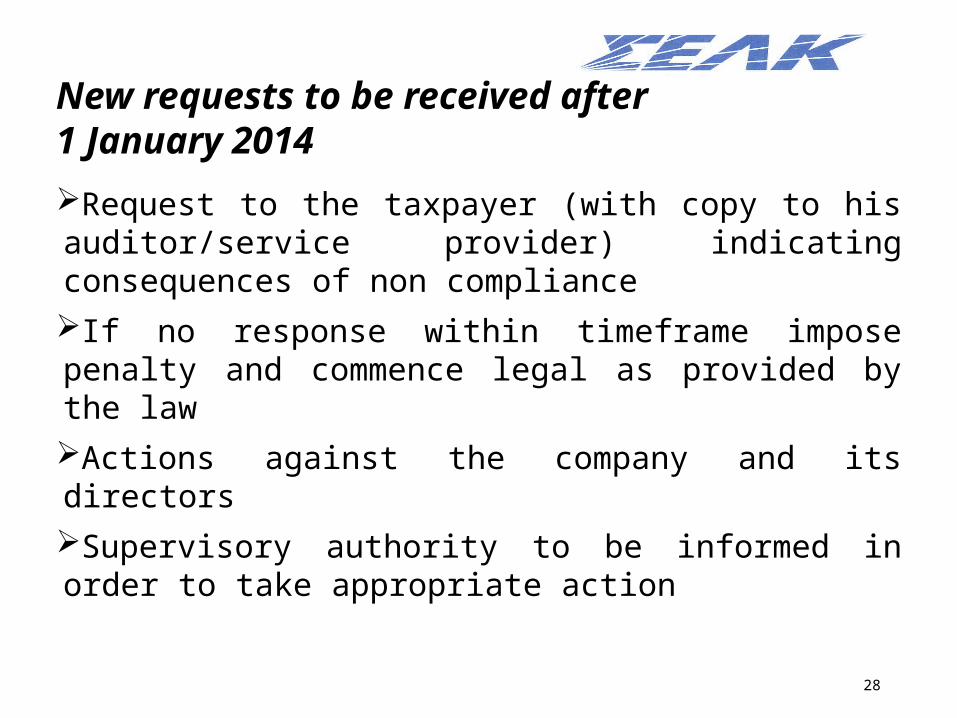

New requests to be received after 1 January 2014

Request to the taxpayer (with copy to his auditor/service provider) indicating consequences of non complianceIf no response within timeframe impose penalty and commence legal as provided by the lawActions against the company and its directorsSupervisory authority to be informed in order to take appropriate action

29

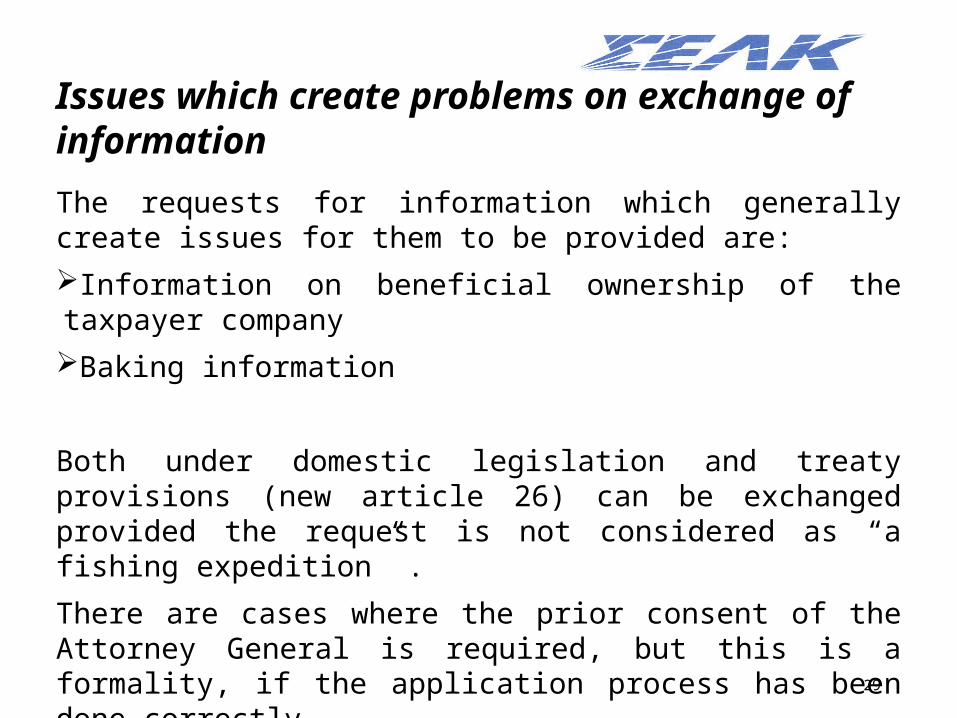

Issues which create problems on exchange of information

The requests for information which generally create issues for them to be provided are: Information on beneficial ownership of the taxpayer companyBaking information

Both under domestic legislation and treaty provisions (new article 26) can be exchanged provided the request is not considered as “a fishing expedition” .

There are cases where the prior consent of the Attorney General is required, but this is a formality, if the application process has been done correctly.

30

Foreseeable relevance and “fishing expedition”The standard of “foreseeable relevance” is intended to provide for exchange of information in tax matters to the widest possible extent and, at the same time, to clarify that Contracting States are not at liberty to engage in “fishing expeditions” or to request information that is unlikely to be relevant to the tax affairs of a given taxpayer.

In the context of information exchange upon request, the standard requires that at the time a request is made there is a reasonable possibility that the requested information will be relevant; whether the information, once provided, actually proves to be relevant is immaterial.

A request may therefore not be declined in cases where a definite assessment of the pertinence of the information to an ongoing investigation can only be made following the receipt of the information. The competent authorities should consult in situations in which the content of the request, the circumstances that led to the request, or the foreseeable relevance of requested information are not clear to the requested State.

However, once the requesting State has provided an explanation as to the foreseeable relevance of the requested information, the requested State may not decline a request or withhold requested information because it believes that the information lacks relevance to the underlying investigation or examination.

31

Foreseeable relevance and “fishing expedition”Where the requested State becomes aware of facts that call into question whether part of the information requested is foreseeably relevant, the competent authorities should consult and the requested State may ask the requesting State to clarify foreseeable relevance in the light of those facts. At the same time, paragraph 1 does not obligate the requested State to provide information in response to requests that are “fishing expeditions”, i.e. speculative requests that have no apparent nexus to an open inquiry or investigation.

As is the case under the Model Agreement on Exchange of Information on Tax Matters a request for information does not constitute a fishing expedition solely because it does not provide the name or address (or both) of the taxpayer under examination or investigation. The same holds true where names are spelt differently or information on names and addresses is presented using a different format. However, in cases in which the requesting State does not provide the name or address (or both) of the taxpayer under examination or investigation, the requesting State must include other information sufficient to identify the taxpayer.

Similarly, paragraph 1 does not necessarily require the request to include the name and/or address of the person believed to be in possession of the information. In fact, the question of how specific a request has to be with respect to such person is typically an issue falling within the scope of subparagraphs a) and b) of paragraph 3 of Article 26.

32

Foreseeable relevance and “fishing expedition”The standard of “foreseeable relevance” can be met both in cases dealing with one taxpayer (whether identified by name or otherwise) or several taxpayers (whether identified by name or otherwise). Where a Contracting State undertakes an investigation into a particular group of taxpayers in accordance with its laws, any request related to the investigation will typically serve “the administration or enforcement” of its domestic tax laws and thus comply with the requirements of paragraph 1, provided it meets the standard of “foreseeable relevance”.

However, where the request relates to a group of taxpayers not individually identified, it will often be more difficult to establish that the request is not a fishing expedition, as the requesting State cannot point to an ongoing investigation into the affairs of a particular taxpayer which in most cases would by itself dispel the notion of the request being random or speculative.

In such cases it is therefore necessary that the requesting State provide a detailed description of the group and the specific facts and circumstances that have led to the request, an explanation of the applicable law and why there is reason to believe that the taxpayers in the group for whom information is requested have been non-compliant with that law supported by a clear factual basis. It further requires a showing that the requested information would assist in determining compliance by the taxpayers in the group.

33

Foreseeable relevance and “fishing expedition”As illustrated in example (h) of paragraph 8, in the case of a group request a third party will usually, although not necessarily, have actively contributed to the non-compliance of the taxpayers in the group, in which case such circumstance should also be described in the request.

Furthermore, and as illustrated in example (a) of paragraph 8.1, a group request that merely describes the provision of financial services to non-residents and mentions the possibility of non-compliance by the non-resident customers does not meet the standard of foreseeable relevance.

34

The tax authorities of State A conduct a tax investigation into the affairs of Mr. X. Based on this investigation the tax authorities have indications that Mr. X holds one or several undeclared bank accounts with Bank B in State B. However, State A has experienced that, in order to avoid detection, it is not unlikely that the bank accounts may be held in the name of relatives of the beneficial owner. State A therefore requests information on all accounts with Bank B of which Mr. X is the beneficial owner and all accounts held in the names of his spouse E and his children K and L.

Cases where information must be exchanged

35

Cases where information must be exchangedState A has obtained information on all transactions involving foreign credit cards carried out in its territory in a certain year. State A has processed the data and launched an investigation that identified all credit card numbers where the frequency and pattern of transactions and the type of use over the course of that year suggest that the cardholders were tax residents of State A. State A cannot obtain the names by using regular sources of information available under its internal taxation procedure, as the pertinent information is not in the possession or control of persons within its jurisdiction. The credit card numbers identify an issuer of such cards to be Bank B in State B.

Based on an open inquiry or investigation, State A sends a request for information to State B, asking for the name, address and date of birth of the holders of the particular cards identified during its investigation and any other person that has signatory authority over those cards. State A supplies the relevant individual credit card numbers and further provides the above information to demonstrate the foreseeable relevance of the requested information to its investigation and more generally to the administration and enforcement of its tax law.

36

Cases where information must be exchangedCompany A, resident of State A, is owned by foreign unlisted Company B, resident of State B. The tax authorities of State A suspect that managers X, Y and Z of Company A directly or indirectly own Company B. If that were the case, the dividends received by Company B from Company A would be taxable in their hands as resident shareholders under country A’s controlled foreign company rules. The suspicion is based on information provided to State A’s tax authorities by a former employee of Company A. When confronted with the allegations, the three managers of Company A deny having any ownership interest in Company B.

The State A tax authorities have exhausted all domestic means of obtaining ownership information on Company B. State A now requests from State B information on whether X, Y and Z are shareholders of Company B. Furthermore, considering that ownership in such cases is often held through, for example, shell companies and nominee shareholders it requests information from State B on whether X, Y and Z indirectly hold an ownership interest in Company B. If State B is unable to determine whether X, Y or Z holds such an indirect interest, information is requested on the shareholder(s) so that it can continue its investigations.

37

Situations where Contracting States are not obligated to provide information in response to a request for information, assuming no further information is provided (a) Bank B is a bank established in State B. State A taxes its residents on the basis of their worldwide income. The competent authority of State A requests that the competent authority of State B provide the names, date and place of birth, and account balances (including information on any financial assets held in such accounts) of residents of State A that have an account with, hold signatory authority over, or a beneficial interest in an account with Bank B in State B. The request states that Bank B is known to have a large group of foreign account holders but does not contain any additional information.

38

Situations where Contracting States are not obligated to provide information in response to a request for information, assuming no further information is provided (b) Company B is a company established in State B. State A requests the names of all shareholders in Company B resident of State A and information on all dividend payments made to such shareholders. The requesting State A points out that Company B has significant business activity in State A and is therefore likely to have shareholders resident of State A. The request further states that it is well known that taxpayers often fail to disclose foreign source income or assets.

39

UK actions- Ensuring that we know who really owns and controls UK companies At the UK-chaired G8 Summit in June, the UK committed to introduce new rules requiring companies to obtain and hold information on who owns and controls them; implement a central registry of company beneficial ownership information; and to review the use of bearer shares (which do not require the identity of the holder to be entered in the company’s publicly available register of members) and nominee directors (which can be used to conceal the identity of the person really controlling the company).

We propose that the registry should hold information on the beneficial owners (i.e. on individuals with significant control or influence) of all UK companies, but consider whether companies already subject to stringent disclosure rules should be exempt.

We consider options to enhance transparency around the use of nominee directors; and whether companies should be prohibited from being appointed company directors, i.e. whether we should ban corporate directors.

Substance/Beneficial

Ownership/ related Issues

41

Management and control issues

All strategic (and preferably day-to-day) management decisions are taken in Cyprus by the directors exercising their duties from Cyprus. This is achieved by having meetings of the Board of Directors take place in Cyprus and signing resolutions, contracts, agreements and other relevant company documents relating to the management, control and administrative functions of the company in Cyprus.

The majority of the directors of the company are tax resident in Cyprus and exercise their office from Cyprus. However,

‘’’the tax residency of the company directors themselves is only an indication of where the decisions affective the company are taken by company directors and it is not the only or determining factor .

Nevertheless, the simple or ordinary residence of the directors could be taken into account as an indication of where the decisions affecting the company are taken’’

42

Management and control issues -What should be done and what not to be doneThe only acts of management and control were the making of the board

resolutions and the signing or execution of documents in accordance with those resolutions.

We do not consider that the mere physical acts of signing resolutions or documents suffice for actual management. Nor does the mental process which precedes the physical act.

What is needed is an effective decision as to whether or not the resolution should be passed and the documents signed or executed and such decisions require some minimum level of information. The decisions must at least to some extent be informed decisions.

Merely going through the motions of passing or making resolutions and signing documents does not suffice. Where the geographical location of the physical acts of signing and executing documents is different from the place where the actual effective decision that the documents be signed and executed is taken, we consider that the latter place is where ‘the central management and control actually abides.’”

43

Management and control issues - What should be done and what not to be doneIn seeking to determine where “central management and control” of a company incorporated outside the United Kingdom lies, it is essential to recognise the distinction between cases where management and control of the company is exercised through its own constitutional organs (the board of directors or the general meeting) and cases where the functions of those constitutional organs are “usurped” - in the sense that management and control is exercised independently of, or without regard to, those constitutional organs.

And, in cases which fall within the former class, it is essential to recognise the distinction (in concept, at least) between the role of an “outsider” in proposing, advising and influencing the decisions which the constitutional organs take in fulfilling their functions and the role of an outsider who dictates the decisions which are to be taken. In that context an “outsider” is a person who is not, himself, a participant in the formal process (a board meeting or a general meeting) through which the relevant constitutional organ fulfils its functions.

44

Management and control issues – What should be done and what not to be done“What is needed is an effective decision as to whether or not the resolution should be passed and the documents signed or executed and such decisions require some minimum level of information. The decisions must at least to some extent be informed decisions.”

If directors of an overseas company sign documents mindlessly, without even thinking what the documents are, I accept that it would be difficult to say that the national jurisdiction in which the directors do that is the jurisdiction of residence of the company. But if they apply their minds to whether or not to sign the documents, the authorities . . . indicate that it is a very different matter. . . .”

45

Other measures which demonstrate substanceAn actual administrative office is maintained in rented premises with all facilities and employment of staffBank accounts of the company wherever located are operated from CyprusHard copies of commercial documentation are stored in the office facilities of the companyAccounting records of the company are prepared and kept in Cyprus

46

New rules in Greece about tax residency of companiesA legal person is considered a tax resident in Greece, among others, if the place of exercise effective management is at any time during the tax year in Greece. The place of exercise effective management of the entity can be considered as located in Greece, assessing the facts and circumstances, taking into account in particular the following criteria:

The place of exercise daily administration

The place of strategic decision making

The place of the annual general meeting of shareholders or members,The place bookkeeping and data

The place of board meetings or where other executive management

The residence of members of the board or any other executive management

The residence of the majority of shareholders or partners (which may be considered in conjunction with the above criteria)

47

New Controlled Foreign Corporation (CFC) rules in Greece

Under the new provisions in the new tax laws in Greece it is expected that undistributed earnings of an entity resident of another country, n cases where the person (natural or legal) located in Greece participates in majority in this or receives a significant percentage of the profits of that legal person. In particular , the conditions for application of that provision are cumulatively the following :

The person (natural or legal ) alone or together with related persons participate directly or indirectly more than 50 % in the share capital or receive more than 50 % of the profits of a foreign legal entity

The foreign legal person is subject to tax in a non-cooperative country or in a state with privileged status (with substantially lower tax level)

48

New Controlled Foreign Corporation (CFC) rules in Greece

More than 30% of net income before taxes earned by the foreign legal person from one or more of the following types of income, provided that more than 50% of any type is derived from transactions with the taxpayer in Greece (natural or legal persons) and persons connected with them:

Interest (or any other income generated from financial assets)

Royalties (or other income derived from intellectual property)

Dividends and income from transfer of shares

Movable assets and real estate

Banking, insurance and other financial activities

It is not a foreign legal person, whose principal class of shares is traded on a regulated market

![Hossein Karamitaheri , Neophytos Neophytou Mahdi Pourfath3 ... · arXiv:1203.2032v1 [cond-mat.mtrl-sci] 9 Mar 2012 Engineering Enhanced Thermoelectric Properties in Zigzag Graphene](https://static.fdocuments.us/doc/165x107/5ffedf8dae2cd772937b541a/hossein-karamitaheri-neophytos-neophytou-mahdi-pourfath3-arxiv12032032v1.jpg)