Michigan State University, 2010 Sponsored by New Economy Initiative Hosted by Detroit Regional...

101

Michigan State University, 2010 Sponsored by New Economy Initiative Hosted by Detroit Regional Chamber of Commerce and Michigan State University Supply Chain Opportunity Assessment: Economic Development for SE Michigan Final Report May 31, 2010

-

date post

21-Dec-2015 -

Category

Documents

-

view

216 -

download

1

Transcript of Michigan State University, 2010 Sponsored by New Economy Initiative Hosted by Detroit Regional...

Michigan State University, 2010

Sponsored by

New Economy Initiative

Hosted by

Detroit Regional Chamber of Commerce

and

Michigan State University

Supply Chain Opportunity Assessment:Economic Development for SE MichiganSupply Chain Opportunity Assessment:Economic Development for SE Michigan

Final Report

May 31, 2010

Final Report

May 31, 2010

Michigan State University, 2010- 2 -

Presentation OutlinePresentation Outline

• Project Background • Project Objectives and Workshop Deliverables• SCM Strategy, Targeted Industries, and

Economic Impact• Economic Development Policies and

Collaboration and Communications• Recommendations and Next Steps

Michigan State University, 2010- 3 -

Opportunity Assessment HistoryOpportunity Assessment History

• The Gateway Funnel• The Detroit Region’s NAFTA Advantage• Border Crossings and Network Flows• Cities with SCM Capabilities• Regional Economic Opportunity• I-75, I-69 and I-94 Corridor• A Connected Region and Economy

Michigan State University, 2010- 4 -

The Gateway Funnel

Michigan State University, 2010- 5 -

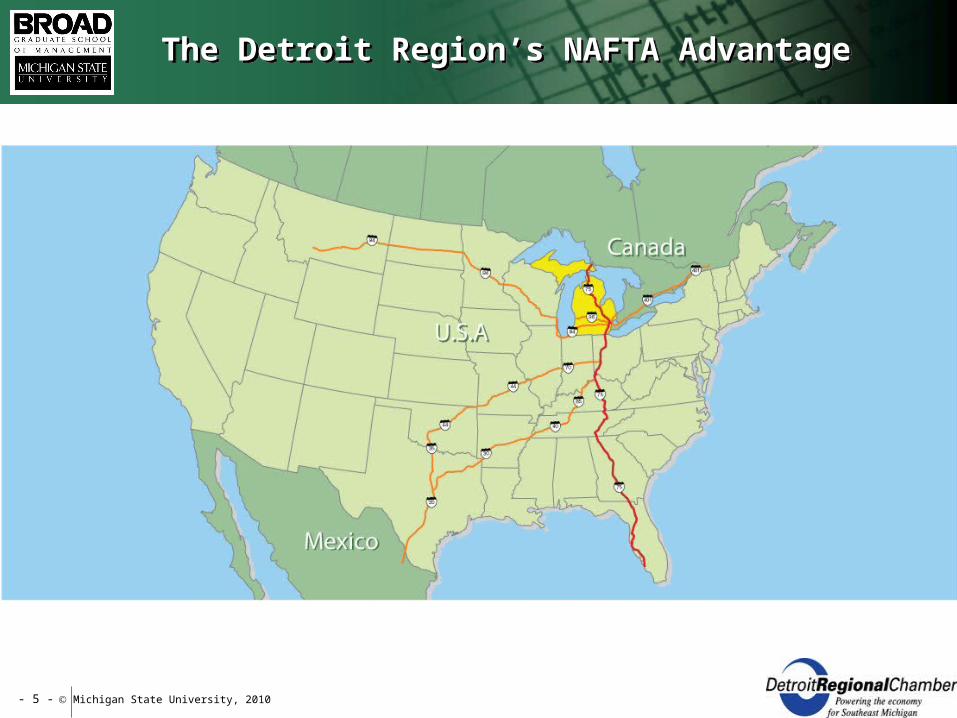

The Detroit Region’s NAFTA Advantage The Detroit Region’s NAFTA Advantage

Michigan State University, 2010- 6 -

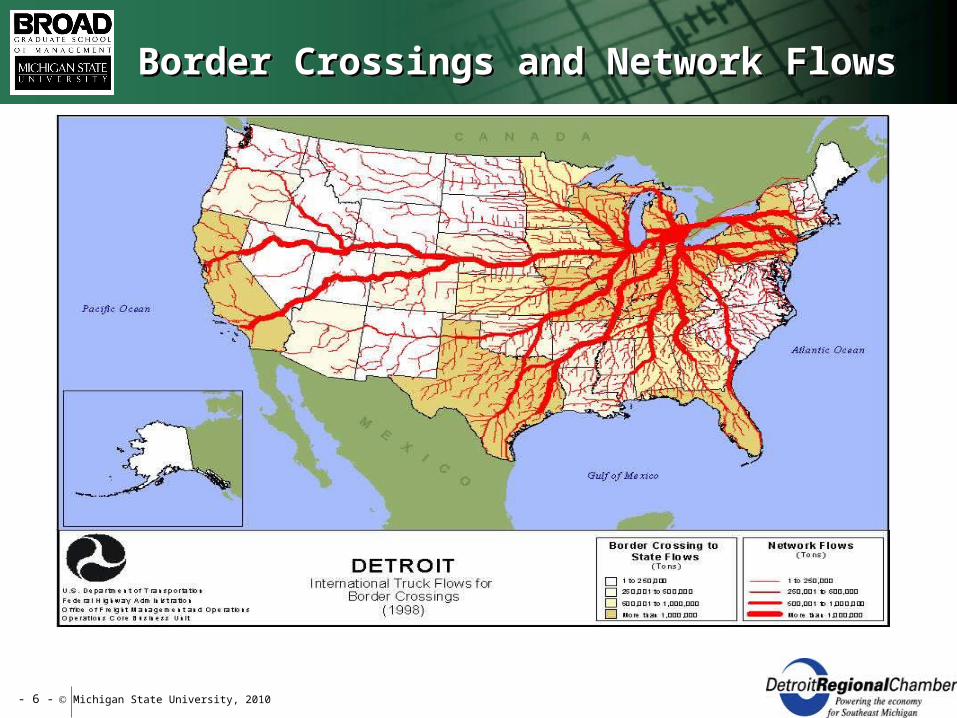

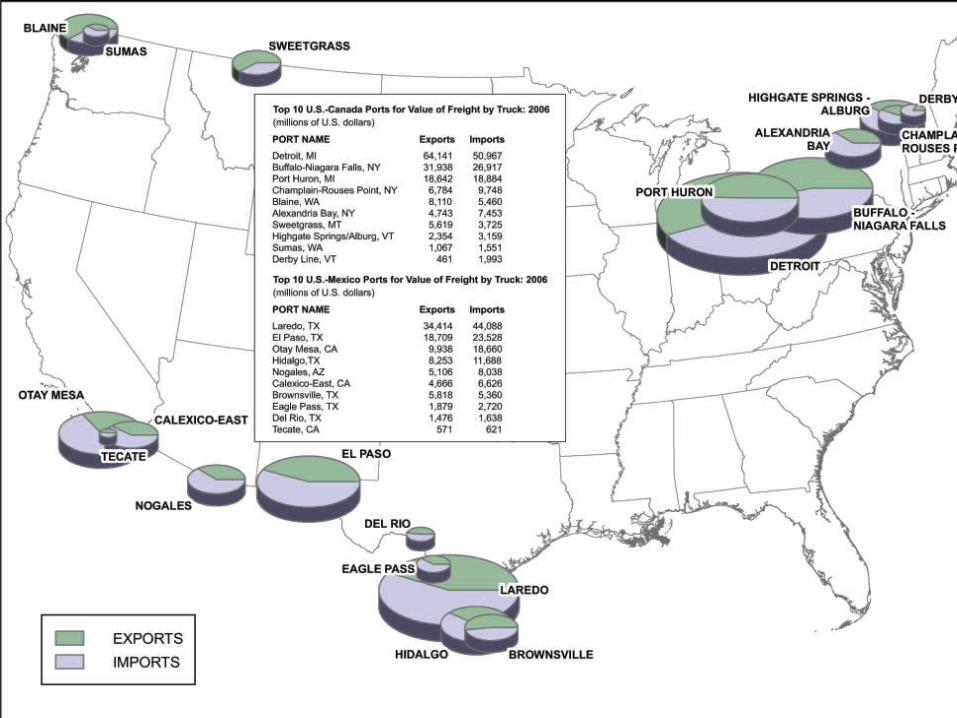

Border Crossings and Network FlowsBorder Crossings and Network Flows

Michigan State University, 2010- 7 -

Michigan State University, 2010- 8 -

Geographic Scope of Project: SEMI/NWOH/SWONGeographic Scope of Project: SEMI/NWOH/SWON

• The geographic scope of the project included the region of Southeast Michigan and neighboring regional locations which would benefit from the creation of a regional supply chain hub

• The neighboring regional locations included Northwest Ohio and Southwest Ontario

• The region or geographic scope of the project is Southeast Michigan, Northwest Ohio and Southwest Ontario and the hub is referred to as the SEMI/NWOH/SWON regional hub

Michigan State University, 2010- 9 -

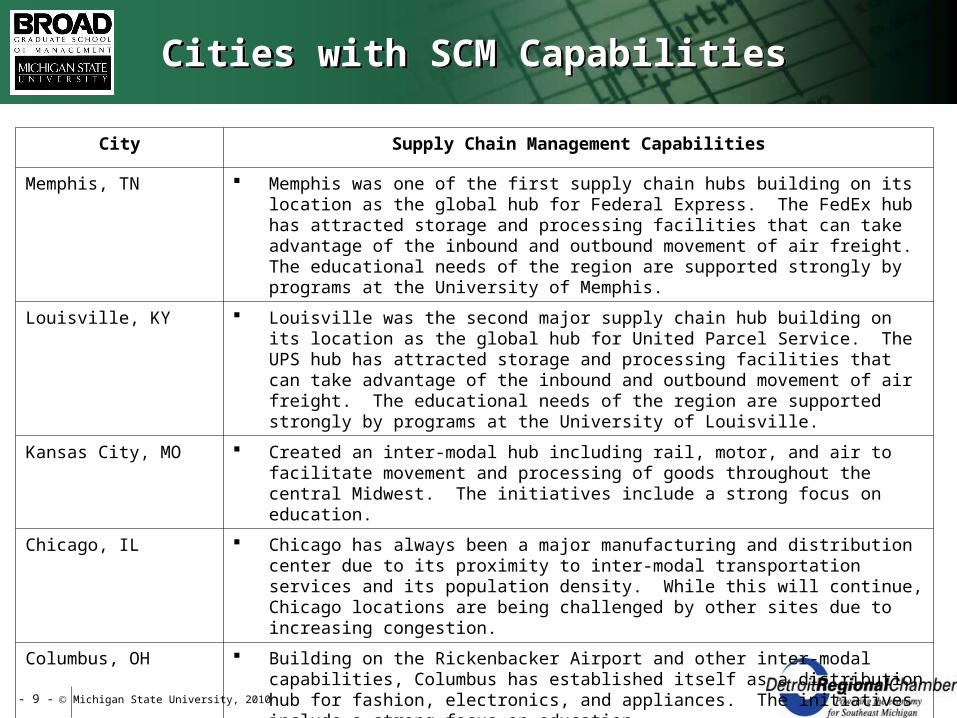

Cities with SCM CapabilitiesCities with SCM Capabilities

City Supply Chain Management Capabilities

Memphis, TN Memphis was one of the first supply chain hubs building on its location as the global hub for Federal Express. The FedEx hub has attracted storage and processing facilities that can take advantage of the inbound and outbound movement of air freight. The educational needs of the region are supported strongly by programs at the University of Memphis.

Louisville, KY Louisville was the second major supply chain hub building on its location as the global hub for United Parcel Service. The UPS hub has attracted storage and processing facilities that can take advantage of the inbound and outbound movement of air freight. The educational needs of the region are supported strongly by programs at the University of Louisville.

Kansas City, MO Created an inter-modal hub including rail, motor, and air to facilitate movement and processing of goods throughout the central Midwest. The initiatives include a strong focus on education.

Chicago, IL Chicago has always been a major manufacturing and distribution center due to its proximity to inter-modal transportation services and its population density. While this will continue, Chicago locations are being challenged by other sites due to increasing congestion.

Columbus, OH Building on the Rickenbacker Airport and other inter-modal capabilities, Columbus has established itself as a distribution hub for fashion, electronics, and appliances. The initiatives include a strong focus on education.

Indianapolis, IN Indianapolis is positioning itself as a less congested alternative for Chicago as a distribution hub particularly for electronics and parts. Indianapolis is focusing on cross-country rail and truck movements. This initiative has some focus on education but not to the degree that Memphis, Louisville, Kansas City, and Columbus have.

SEMI/NWOH/SWON ?????????????????????????????

Michigan State University, 2010- 10 -

Michigan SCM CapabilitiesMichigan SCM Capabilities

• U.S. – Canada location and border system• Airport facilities and services• Relative capacity and congestion levels• Strong rail/intermodal facilities and services• Appropriate business taxation forms and levels• Reasonable regulatory systems• Critical mass of SCM customers, service

providers, and professional SCM staff• OTHERS?????

Michigan State University, 2010- 11 -

Regional Economic OpportunityRegional Economic Opportunity

Michigan State University, 2010- 12 -

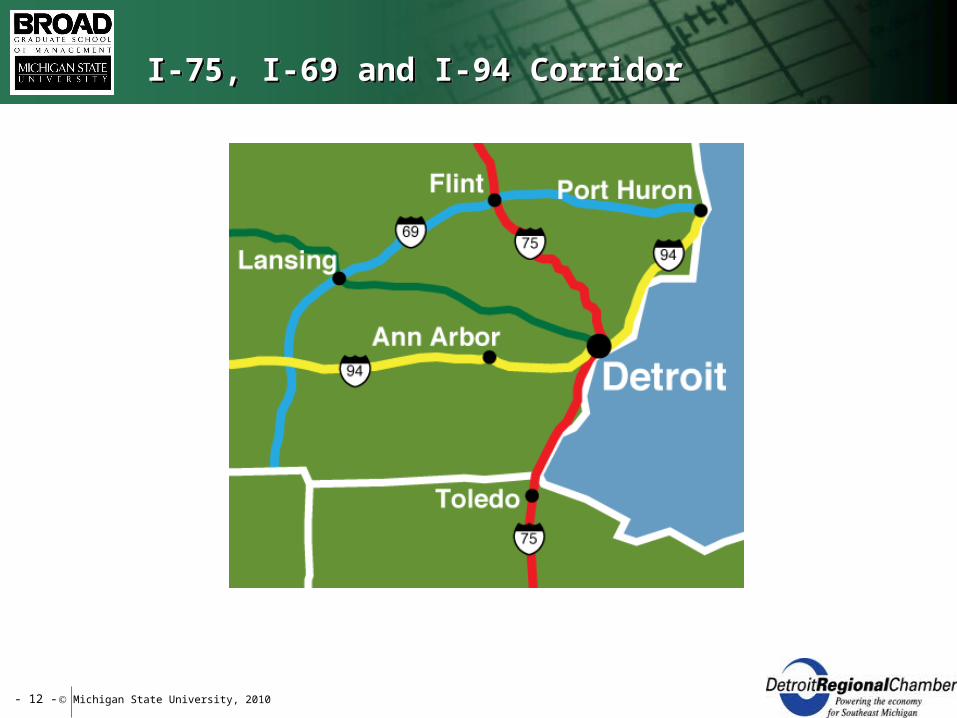

I-75, I-69 and I-94 CorridorI-75, I-69 and I-94 Corridor

Michigan State University, 2010- 13 -

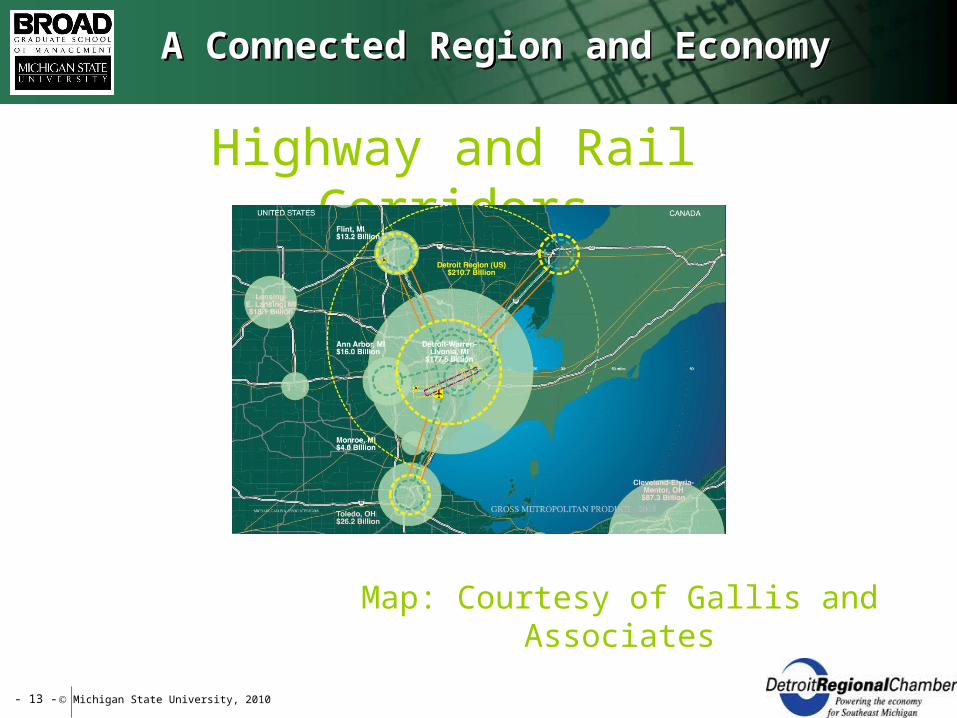

A Connected Region and EconomyA Connected Region and Economy

Highway and Rail Corridors

Map: Courtesy of Gallis and Associates

Michigan State University, 2010- 14 -

Presentation OutlinePresentation Outline

• Project Background • Project Objectives and Workshop

Deliverables• SCM Strategy, Targeted Industries, and

Economic Impact• Economic Development Policies and

Collaboration and Communications• Recommendations and Next Steps

Michigan State University, 2010- 15 -

Introduction to the Opportunity Introduction to the Opportunity

• Grow cross-border trade and increase the demand for trade services supported by both the public and private sector;

• Develop the human capital to design, guide and operate a 21st Century global supply chain hub by providing education and training to build a world class workforce;

• Advocate for policy changes at the local, federal and state levels to provide business incentives, improve the region’s transportation infrastructure, and support smooth operation while assuring border security;

• Develop a research agenda and clearinghouse for related research to assist companies and policy makers; and

• Increase the number of jobs in the sector.

Michigan State University, 2010- 16 -

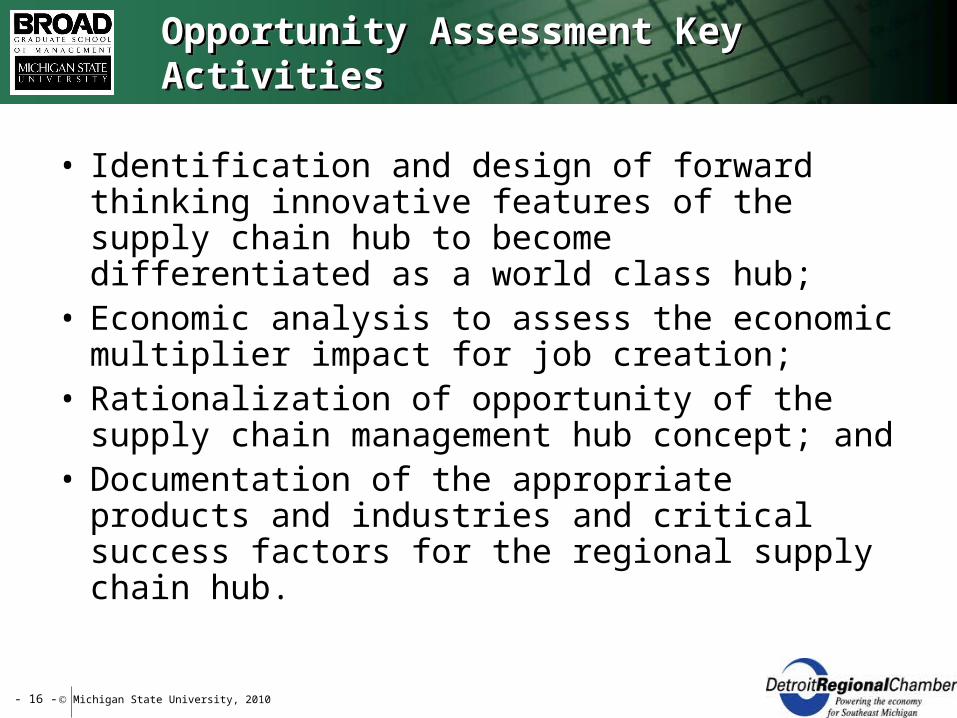

Opportunity Assessment Key ActivitiesOpportunity Assessment Key Activities

• Identification and design of forward thinking innovative features of the supply chain hub to become differentiated as a world class hub;

• Economic analysis to assess the economic multiplier impact for job creation;

• Rationalization of opportunity of the supply chain management hub concept; and

• Documentation of the appropriate products and industries and critical success factors for the regional supply chain hub.

Michigan State University, 2010- 17 -

Supply Chain Opportunity Assessment:Workshop One RecapSupply Chain Opportunity Assessment:Workshop One Recap

• Increase awareness of Supply Chain Opportunities for SEMI/NWOH/SWON

• Determine capabilities and benefits to be incorporated into the Supply Chain Hub for SEMI/NWOH/SWON

• Determine the industries and associated cargo volumes which would be attracted to utilize the Supply Chain Hub for SEMI/NWOH/SWON

Michigan State University, 2010- 18 -

Supply Chain Opportunity Assessment:Workshop Two RecapSupply Chain Opportunity Assessment:Workshop Two Recap

• Validate SCM design dimensions and attributes for the supply chain hub for SEMI/NWOH/SWON

• Determine the SCM policies to enable implementation of the SCM design dimensions

• Assess the economic potential of the supply chain related industry types for SEMI/NWOH/SWON

Michigan State University, 2010- 19 -

Supply Chain Opportunity Assessment:Workshop Three RecapSupply Chain Opportunity Assessment:Workshop Three Recap

• Validate SCM strategy, targeted industries, and economic impact for SEMI/NWOH/SWON

• Determine economic development policies necessary for successful implementation of the SCM strategy

• Agree on next steps to assure project momentum continues

Michigan State University, 2010- 20 -

Presentation OutlinePresentation Outline

• Project Background • Project Objectives and Workshop Deliverables• SCM Strategy, Targeted Industries, and

Economic Impact• Economic Development Policies and

Collaboration and Communications• Recommendations and Next Steps

- 21 -

Supply Chain Hub Strategy CreationSupply Chain Hub Strategy Creation

Strategy and SCM Strategy Elements

- 22 -

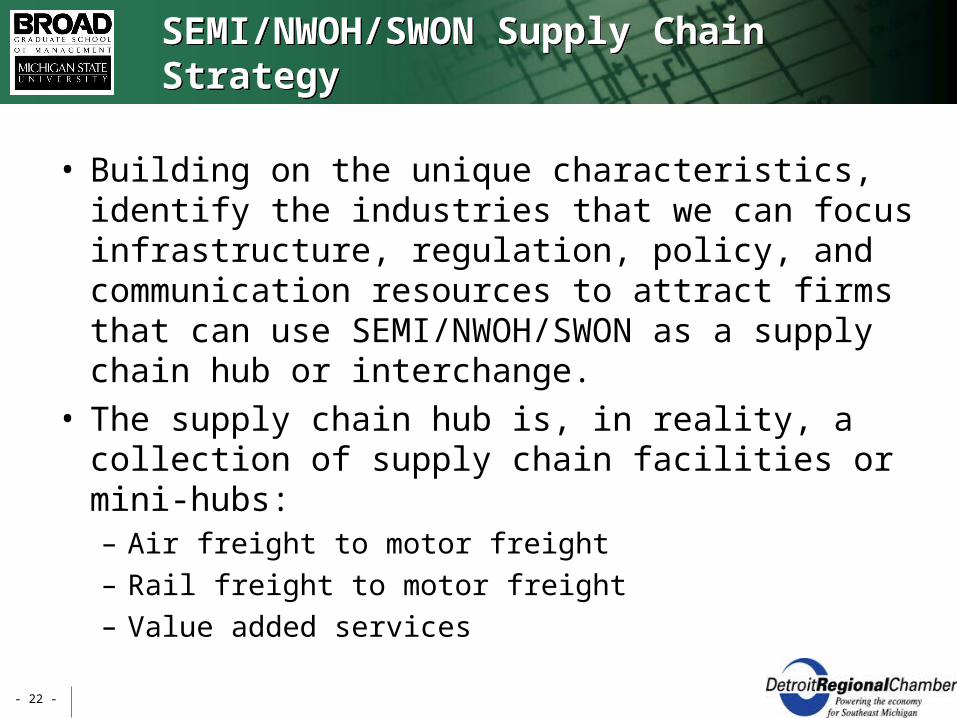

SEMI/NWOH/SWON Supply Chain StrategySEMI/NWOH/SWON Supply Chain Strategy

• Building on the unique characteristics, identify the industries that we can focus infrastructure, regulation, policy, and communication resources to attract firms that can use SEMI/NWOH/SWON as a supply chain hub or interchange.

• The supply chain hub is, in reality, a collection of supply chain facilities or mini-hubs:– Air freight to motor freight – Rail freight to motor freight– Value added services

- 23 -

SEMI/NWOH/SWON Supply Chain StrategySEMI/NWOH/SWON Supply Chain Strategy

• The SCM Strategy involves multiple areas:– Build differentiated supply chain hub(s) which will

stimulate economic growth and job creation– Attract industries to the supply chain hub

• Industries with a heavy manufacturing focus• Industries with a light manufacturing focus• Industries with a distribution and value added services focus

– Facilitate development of hub with private/public sector partnership

• The SCM Strategy Elements (design dimensions) outline the necessary and the differentiated capabilities of the SCM Strategy

- 24 -

SCM Strategy ElementsSCM Strategy Elements

• Ability to serve global markets• Infrastructure and support capabilities• Government regulations• Competitive tax climate• Availability of human, land, supplier, and financial capital• Economic competitiveness and lowest total cost to serve• Supply chain sustainability• Collaboration and partnership

- 25 -

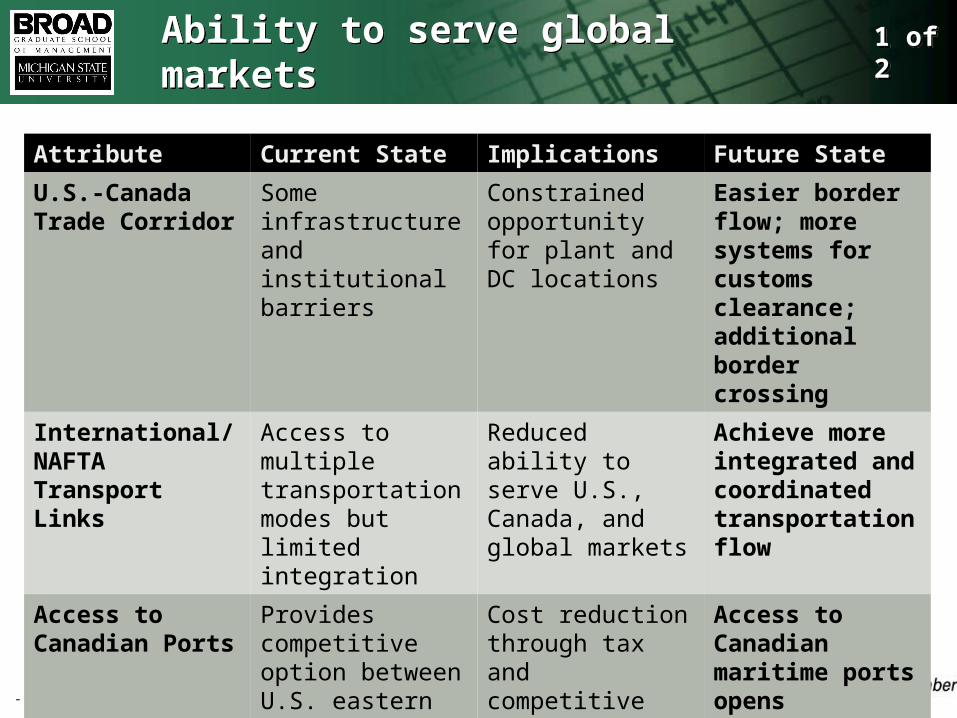

SCM Strategy ElementsSCM Strategy Elements

• Ability to serve global markets– U.S.-Canada trade corridor– International/NAFTA transport links– Access to Canadian ports– Customs house, forwarding, and related services– Foreign trade zone facilities

- 26 -

Ability to serve global marketsAbility to serve global markets

Attribute Current State Implications Future State

U.S.-Canada Trade Corridor

Some infrastructure and institutional barriers

Constrained opportunity for plant and DC locations

Easier border flow; more systems for customs clearance; additional border crossing

International/ NAFTA Transport Links

Access to multiple transportation modes but limited integration

Reduced ability to serve U.S., Canada, and global markets

Achieve more integrated and coordinated transportation flow

Access to Canadian Ports

Provides competitive option between U.S. eastern ports and Canada

Cost reduction through tax and competitive advantages

Access to Canadian maritime ports opens competitive option for SE MI

1 of 21 of 2

- 27 -

Ability to serve global marketsAbility to serve global markets

Attribute Current State Implications Future State

Customs house, forwarding, and related services

Services already in place but benefits not fully realized

Stronger than competing regions

Extend competitive advantage

Foreign trade zone facilities

High quality, underutilized capability

Reduced duties and fees

Extend competitive advantage

2 of 22 of 2

- 28 -

SCM Strategy ElementsSCM Strategy Elements

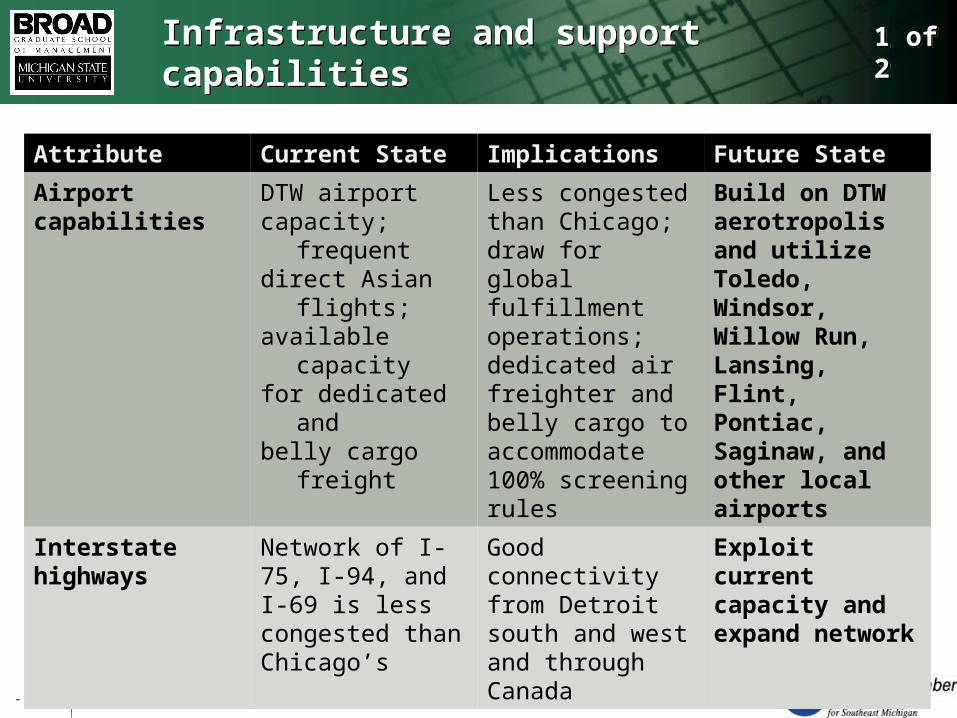

• Ability to serve global markets• Infrastructure and support capabilities

– Airport capabilities– Interstate highways– Railroad network– Intermodal transportation capacity– Distribution facilities

- 29 -

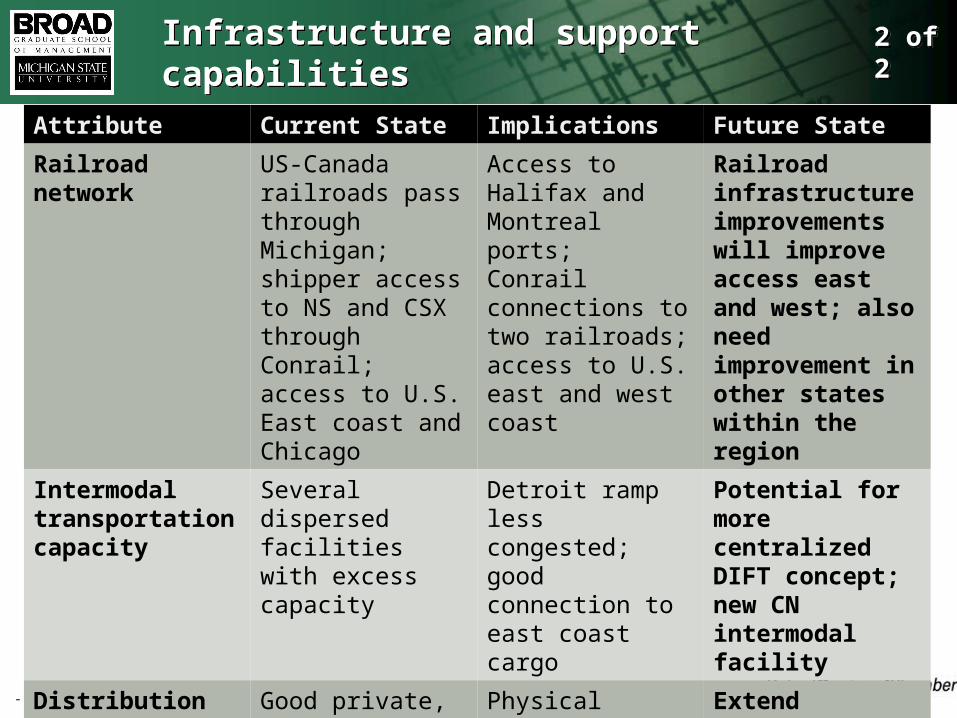

Infrastructure and support capabilitiesInfrastructure and support capabilities

Attribute Current State Implications Future State

Airport capabilities

DTW airportcapacity; frequent direct Asian flights;available capacityfor dedicated andbelly cargo freight

Less congested than Chicago; draw for global fulfillment operations;dedicated air freighter and belly cargo to accommodate 100% screening rules

Build on DTW aerotropolis and utilize Toledo, Windsor, Willow Run, Lansing, Flint, Pontiac, Saginaw, and other local airports

Interstate highways

Network of I-75, I-94, and I-69 is less congested than Chicago’s

Good connectivity from Detroit south and west and through Canada

Exploit current capacity and expand network

1 of 21 of 2

- 30 -

Infrastructure and support capabilitiesInfrastructure and support capabilities

Attribute Current State Implications Future State

Railroad network US-Canada railroads pass through Michigan; shipper access to NS and CSX through Conrail; access to U.S. East coast and Chicago

Access to Halifax and Montreal ports; Conrail connections to two railroads; access to U.S. east and west coast

Railroad infrastructure improvements will improve access east and west; also need improvement in other states within the region

Intermodal transportation capacity

Several dispersed facilities with excess capacity

Detroit ramp less congested; good connection to east coast cargo

Potential for more centralized DIFT concept; new CN intermodal facility

Distribution facilities

Good private, leased, and public warehouse capacity

Physical capacity and labor available for newbusiness activity

Extend competitive advantage; Build consol/deconsol, cross-dock centers

2 of 22 of 2

- 31 -

SCM Strategy ElementsSCM Strategy Elements

• Ability to serve global markets• Infrastructure and support capabilities• Government regulations

– Higher weight limits– Carrier permitting process

- 32 -

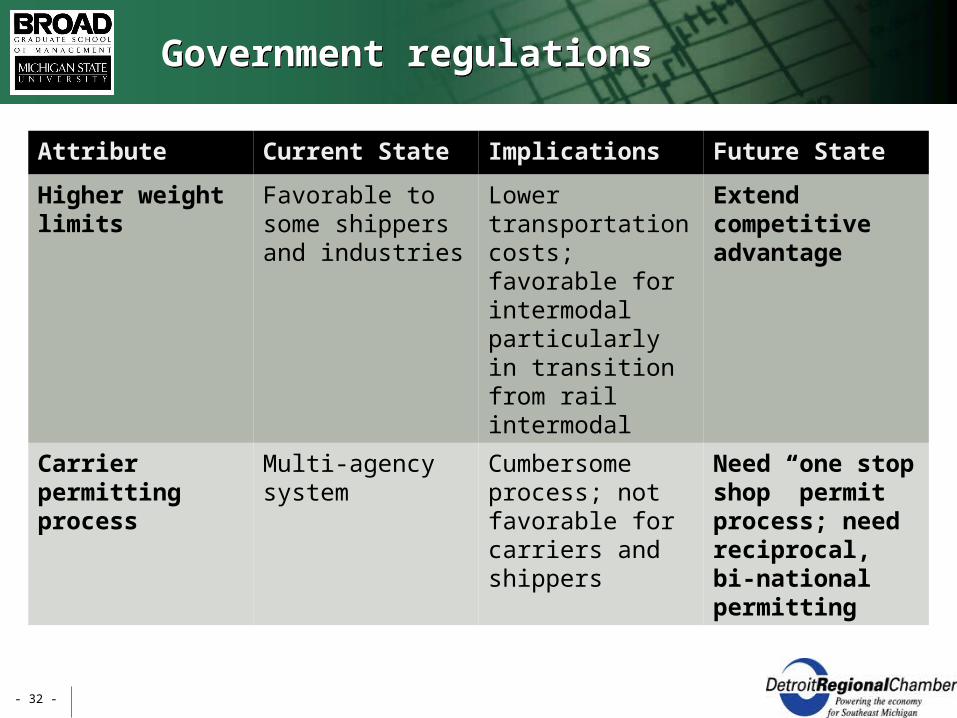

Government regulationsGovernment regulations

Attribute Current State Implications Future State

Higher weight limits

Favorable to some shippers and industries

Lower transportation costs; favorable for intermodal particularly in transition from rail intermodal

Extend competitive advantage

Carrier permitting process

Multi-agency system

Cumbersome process; not favorable for carriers and shippers

Need “one stop shop” permit process; need reciprocal, bi-national permitting

- 33 -

SCM Strategy ElementsSCM Strategy Elements

• Ability to serve global markets• Infrastructure and support capabilities• Government regulations• Competitive tax climate

– Michigan Business Tax– Personal property taxes on equipment– Personal income tax– Tax abatements and incentives

- 34 -

Need for competitive tax climateNeed for competitive tax climate

Attribute Current State Implications Future State

Michigan business tax

Gross receipts intensity and surcharge issues

Negative effect on Michigan businesses

Reduce gross receipts intensity and eliminate surcharge

Personal property taxes on equipment

Relatively high Discourages investment in Michigan

Reduce personal property taxes

Personal income taxes

Relatively low and flat

Advantage for Michigan

Extend competitive advantage

Tax abatements and incentives

Competitive, targeted

Allows Michigan to compete for specific projects but results in higher general rates

Targeted application

- 35 -

SCM Strategy ElementsSCM Strategy Elements

• Ability to serve global markets• Infrastructure and support capabilities• Government regulations• Competitive tax climate• Availability of human, land, supplier, and financial capital

– Supply chain expertise– Supply chain skilled labor– Technology enablers– Land and facility availability– Financial capital– Supplier and support capabilities

- 36 -

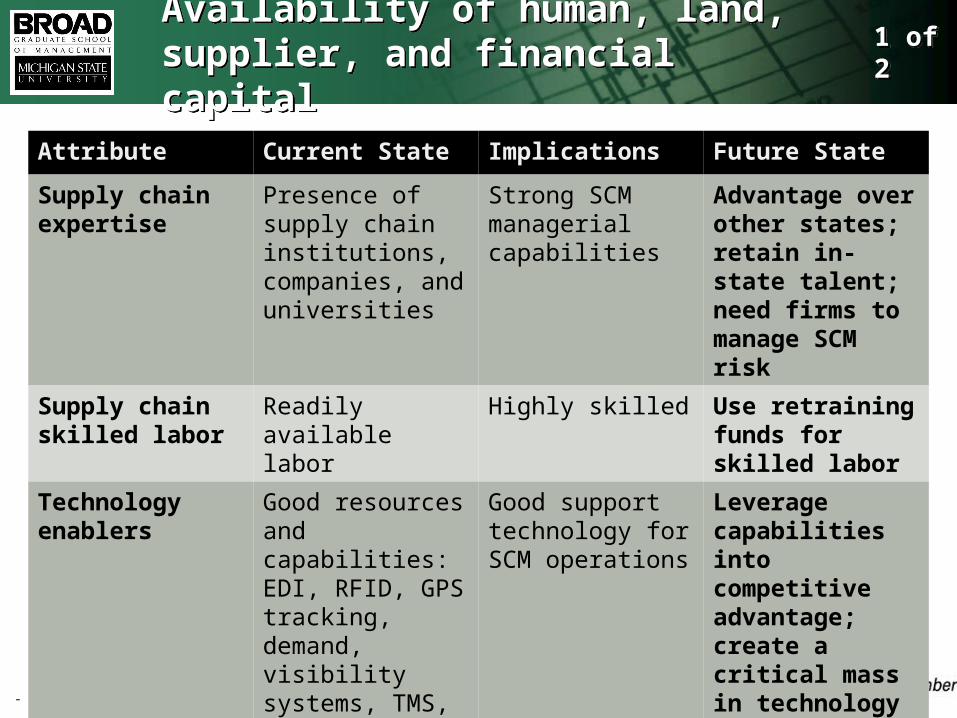

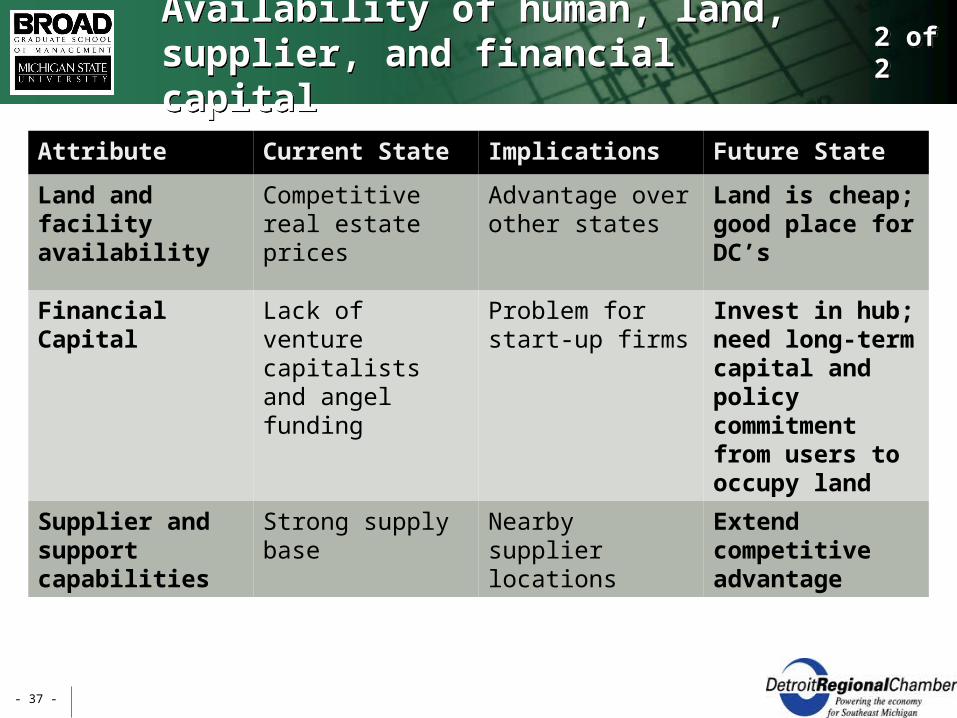

Availability of human, land, supplier, and financial capitalAvailability of human, land, supplier, and financial capital

Attribute Current State Implications Future State

Supply chain expertise

Presence of supply chain institutions, companies, and universities

Strong SCM managerial capabilities

Advantage over other states; retain in-state talent; need firms to manage SCM risk

Supply chain skilled labor

Readily available labor

Highly skilled Use retraining funds for skilled labor

Technology enablers

Good resources and capabilities: EDI, RFID, GPS tracking, demand, visibility systems, TMS, WMS, trade mgmt systems skills

Good support technology for SCM operations

Leverage capabilities into competitive advantage; create a critical mass in technology sector

1 of 21 of 2

- 37 -

Availability of human, land, supplier, and financial capitalAvailability of human, land, supplier, and financial capital

Attribute Current State Implications Future State

Land and facility availability

Competitive real estate prices

Advantage over other states

Land is cheap; good place for DC’s

Financial Capital Lack of venture capitalists and angel funding

Problem for start-up firms

Invest in hub; need long-term capital and policy commitment from users to occupy land

Supplier and support capabilities

Strong supply base Nearby supplier locations

Extend competitive advantage

2 of 22 of 2

- 38 -

SCM Strategy ElementsSCM Strategy Elements

• Ability to serve global markets• Infrastructure and support capabilities• Government regulations• Competitive tax climate• Availability of human, land, supplier, and financial capital• Economic competitiveness and lowest total cost to serve

– Hub operations cost– Hub service levels– Outbound empty trucks

- 39 -

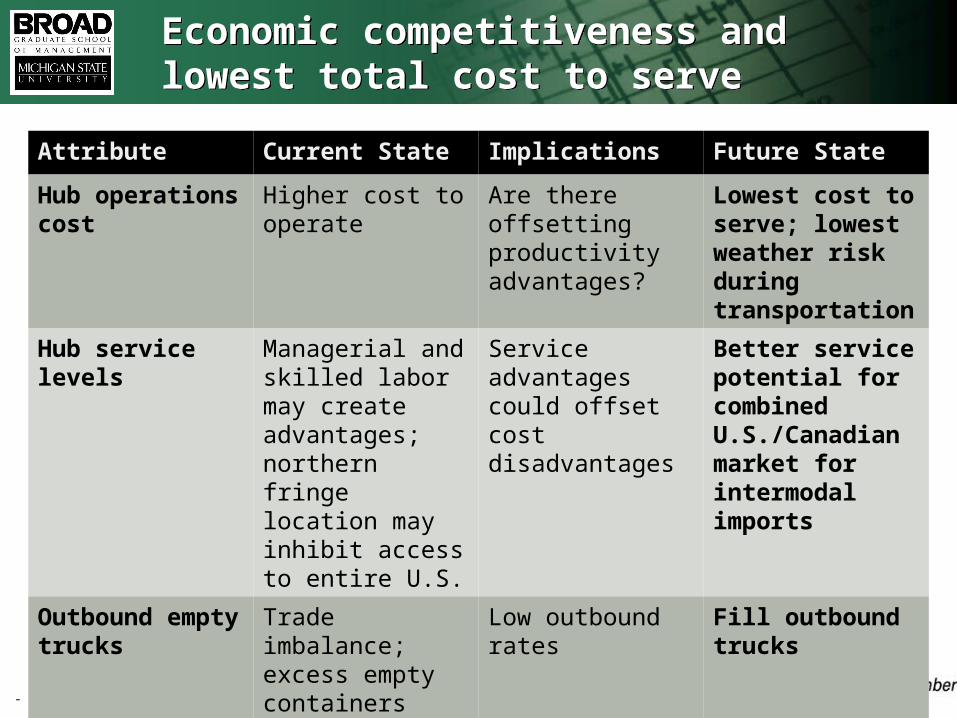

Economic competitiveness and lowest total cost to serveEconomic competitiveness and lowest total cost to serve

Attribute Current State Implications Future State

Hub operations cost

Higher cost to operate

Are there offsetting productivity advantages?

Lowest cost to serve; lowest weather risk during transportation

Hub service levels

Managerial and skilled labor may create advantages;northern fringe location may inhibit access to entire U.S.

Service advantages could offset cost disadvantages

Better service potential for combined U.S./Canadian market for intermodal imports

Outbound empty trucks

Trade imbalance;excess empty containers

Low outbound rates

Fill outbound trucks

- 40 -

SCM Strategy ElementsSCM Strategy Elements

• Ability to serve global markets• Infrastructure and support capabilities• Government regulations• Competitive tax climate• Availability of human, land, supplier, and financial capital• Economic competitiveness and lowest total cost to serve• Supply chain sustainability

– Customer service and reliability– Security– Green/environmental aspects– Reliable weather

- 41 -

Supply chain sustainabilitySupply chain sustainability

Attribute Current State Implications Future State

Customer service and reliability

Increased uncertainty due to congestion

Increased cost and reduced service

Customers requiring more reliability and closer suppliers to lower cost and improve service

Security Consumers and regulators expecting increased security

Increased freight monitoring

Need technology and facilities to monitor freight

Green/ environmental aspects

Firms strongly focus on low cost suppliers

Firms looking for suppliers who can minimize environmental impact

Firms looking for closer suppliers or transporters that have less environmental impact

- 42 -

SCM Strategy ElementsSCM Strategy Elements

• Ability to serve global markets• Infrastructure and support capabilities• Government regulations• Competitive tax climate• Availability of human, land, supplier, and financial capital• Economic competitiveness and lowest total cost to serve• Supply chain sustainability• Collaboration and partnership

– Teamwork with government stakeholders– Develop common value-based SCM message– Partnership with private sector and targeted industries

- 43 -

Attribute Current State Implications Future State

One integrated regional plan

Regional support from all stakeholders of the integrated SCM plan

Champion Need a “champion” or major player to act as an anchor; early investment and commitment

Collaboration and partnershipCollaboration and partnership

- 44 -

Synthesis of Strengths and Weaknesses of SCM Strategy ElementsSynthesis of Strengths and Weaknesses of SCM Strategy Elements

• Strengths– Good potential for cross-border

distribution hub away from congestion of Chicago-Toronto

– Good potential for trans-loading heavy imports from Halifax or Prince Rupert

– Good airport and highway infrastructure with limited congestion

– While wage rates are high, skilled management and labor talent is readily available

– Land and facilities readily available

– Relatively inexpensive outbound motor carrier capacity

• Weaknesses– Located on peninsula unless

cross-border is considered– Perceived or real high union

wage scale– Perceived or real high gross

receipts and personal property taxes

– Infrastructure barriers and custom processes, particularly at border

– Current industry sectors in recession

– Poor perception of current capabilities

– Lack of public/private partnership authority

– Absence of regional government authority to coordinate and promote supply chain initiatives

- 45 -

Supply Chain Hub Strategy CreationSupply Chain Hub Strategy Creation

Strategy and SCM Strategy Elements

Industries offering

Value Add Potential

- 46 -

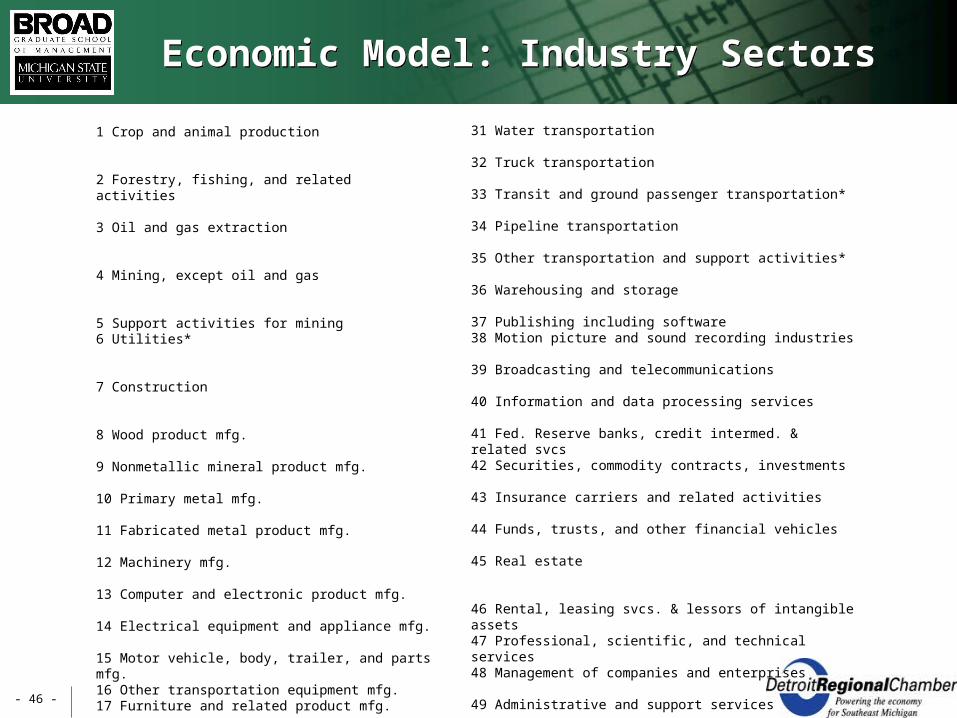

Economic Model: Industry SectorsEconomic Model: Industry Sectors

1 Crop and animal production 2 Forestry, fishing, and related activities 3 Oil and gas extraction 4 Mining, except oil and gas 5 Support activities for mining6 Utilities* 7 Construction 8 Wood product mfg. 9 Nonmetallic mineral product mfg. 10 Primary metal mfg. 11 Fabricated metal product mfg. 12 Machinery mfg. 13 Computer and electronic product mfg. 14 Electrical equipment and appliance mfg. 15 Motor vehicle, body, trailer, and parts mfg. 16 Other transportation equipment mfg. 17 Furniture and related product mfg. 18 Miscellaneous mfg. 19 Food, beverage, and tobacco product mfg. 20 Textile and textile product mills 21 Apparel, leather, and allied product mfg. 22 Paper mfg. 23 Printing and related support activities 24 Petroleum and coal products mfg. 25 Chemical mfg. 26 Plastics and rubber products mfg. 27 Wholesale trade 28 Retail trade 29 Air transportation 30 Rail transportation

31 Water transportation 32 Truck transportation 33 Transit and ground passenger transportation* 34 Pipeline transportation 35 Other transportation and support activities* 36 Warehousing and storage 37 Publishing including software 38 Motion picture and sound recording industries 39 Broadcasting and telecommunications 40 Information and data processing services 41 Fed. Reserve banks, credit intermed. & related svcs 42 Securities, commodity contracts, investments 43 Insurance carriers and related activities 44 Funds, trusts, and other financial vehicles 45 Real estate 46 Rental, leasing svcs. & lessors of intangible assets 47 Professional, scientific, and technical services 48 Management of companies and enterprises 49 Administrative and support services 50 Waste management and remediation services 51 Educational services 52 Ambulatory health care services 53 Hospitals and nursing and residential care facilities 54 Social assistance 55 Performing arts, museums, and related activities 56 Amusements, gambling, and recreation 57 Accommodation 58 Food services and drinking places 59 Other services* 60 Households

- 47 -

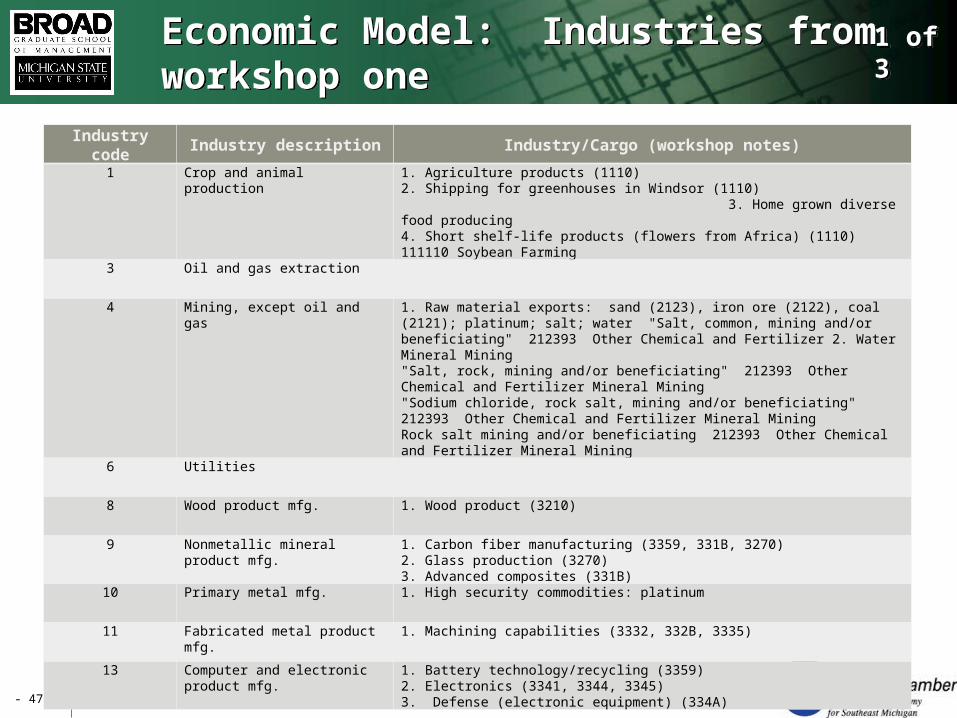

Economic Model: Industries from workshop oneEconomic Model: Industries from workshop one

1 of 31 of 3

Industry code Industry description Industry/Cargo (workshop notes)

1 Crop and animal production 1. Agriculture products (1110)2. Shipping for greenhouses in Windsor (1110) 3. Home grown diverse food producing4. Short shelf-life products (flowers from Africa) (1110) 111110 Soybean Farming

3 Oil and gas extraction

4 Mining, except oil and gas 1. Raw material exports: sand (2123), iron ore (2122), coal (2121); platinum; salt; water "Salt, common, mining and/or beneficiating" 212393 Other Chemical and Fertilizer 2. Water Mineral Mining"Salt, rock, mining and/or beneficiating" 212393 Other Chemical and Fertilizer Mineral Mining"Sodium chloride, rock salt, mining and/or beneficiating" 212393 Other Chemical and Fertilizer Mineral MiningRock salt mining and/or beneficiating 212393 Other Chemical and Fertilizer Mineral Mining

6 Utilities

8 Wood product mfg. 1. Wood product (3210)

9 Nonmetallic mineral product mfg. 1. Carbon fiber manufacturing (3359, 331B, 3270)2. Glass production (3270)3. Advanced composites (331B)

10 Primary metal mfg. 1. High security commodities: platinum

11 Fabricated metal product mfg. 1. Machining capabilities (3332, 332B, 3335)

13 Computer and electronic product mfg.

1. Battery technology/recycling (3359)2. Electronics (3341, 3344, 3345)3. Defense (electronic equipment) (334A)

- 48 -

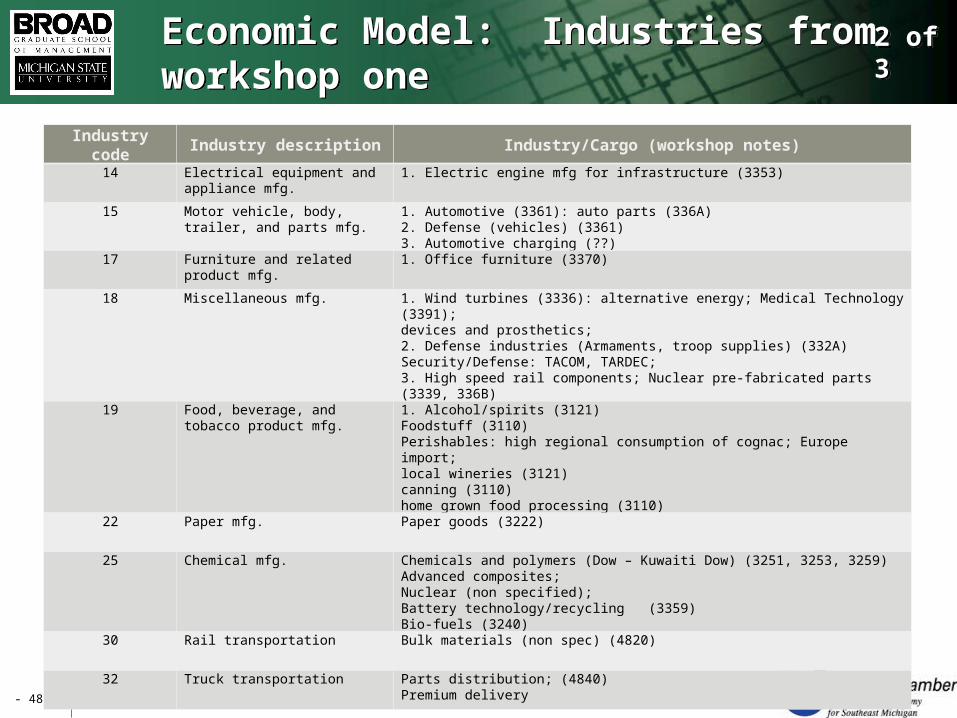

Economic Model: Industries from workshop oneEconomic Model: Industries from workshop one

2 of 32 of 3

Industry code Industry description Industry/Cargo (workshop notes)

14 Electrical equipment and appliance mfg.

1. Electric engine mfg for infrastructure (3353)

15 Motor vehicle, body, trailer, and parts mfg.

1. Automotive (3361): auto parts (336A)2. Defense (vehicles) (3361)3. Automotive charging (??)

17 Furniture and related product mfg. 1. Office furniture (3370)

18 Miscellaneous mfg. 1. Wind turbines (3336): alternative energy; Medical Technology (3391); devices and prosthetics; 2. Defense industries (Armaments, troop supplies) (332A)Security/Defense: TACOM, TARDEC; 3. High speed rail components; Nuclear pre-fabricated parts (3339, 336B)

19 Food, beverage, and tobacco product mfg.

1. Alcohol/spirits (3121)Foodstuff (3110)Perishables: high regional consumption of cognac; Europe import; local wineries (3121)canning (3110)home grown food processing (3110)

22 Paper mfg. Paper goods (3222)

25 Chemical mfg. Chemicals and polymers (Dow – Kuwaiti Dow) (3251, 3253, 3259) Advanced composites; Nuclear (non specified); Battery technology/recycling (3359) Bio-fuels (3240)

30 Rail transportation Bulk materials (non spec) (4820)

32 Truck transportation Parts distribution; (4840)Premium delivery

- 49 -

Economic Model: Industries from workshop oneEconomic Model: Industries from workshop one

3 of 33 of 3

Industry code Industry description Industry/Cargo (workshop notes)

35 Other transportation and support activities

Heavy aircraft maintenance (3364); Aircraft parts distribution (3364); Recruit supply chain service industries to relocate to Detroit area (ex: Indy): inbound for consumer goods, retail distribution, containerized cargo, flexible containers, deconsolidation, cross-dock, add-on services, labeling, rework, consolidating services, demand aggregation and disaggregation, common shipments across industries, home delivery, data warehouse for shipping data, fulfillment centers, mfg goods that require sub-assembly (4930)

36 Warehousing and storage Distribution facilities; (4930)

47 Professional, scientific, and technical services

Plant science (research, not a product)

50 Waste management and remediation services

Recycling/reclaiming (5620); Waste paper/metal/scrap (5621, 5622, 5629)

- 50 -

Detroit Regional Chamber – Target IndustriesDetroit Regional Chamber – Target Industries

• Transportation & logistics • Alternative energy • Aerospace • Medical devices • Homeland Security and Defense• Advanced Manufacturing

- 51 -

MEDC - Target IndustriesMEDC - Target Industries

• Alternative Energy • Automotive Engineering • Life Sciences • Homeland Security and Defense • Advanced Manufacturing • Film Industry

- 52 -

Target Industries: Synthesized from Workshop TwoTarget Industries: Synthesized from Workshop Two

• Automotive Renewal• Alternative energy

– Battery technology– Bio fuels– Wind– Solar panels

• Beverage and alcohol distribution• Carbon fiber manufacturing• Chemical processing• Defense• Electronics - industrial• Food processing• Medical technologies• Retail importing and value add• Water technologies• Waste Management

- 53 -

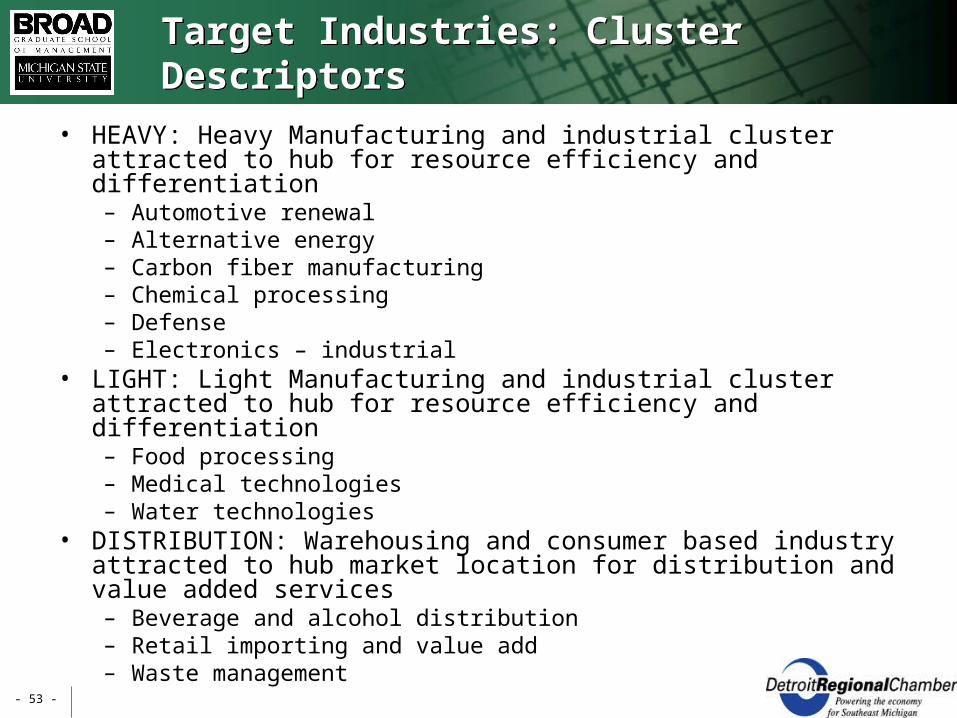

Target Industries: Cluster DescriptorsTarget Industries: Cluster Descriptors

• HEAVY: Heavy Manufacturing and industrial cluster attracted to hub for resource efficiency and differentiation– Automotive renewal– Alternative energy– Carbon fiber manufacturing– Chemical processing– Defense– Electronics – industrial

• LIGHT: Light Manufacturing and industrial cluster attracted to hub for resource efficiency and differentiation– Food processing– Medical technologies– Water technologies

• DISTRIBUTION: Warehousing and consumer based industry attracted to hub market location for distribution and value added services– Beverage and alcohol distribution– Retail importing and value add– Waste management

- 54 -

Value Propositions by Industry ClusterValue Propositions by Industry Cluster

SCM Element Heavy Manufacturing

Light Manufacturing

Distribution

Ability to serve and be served by global markets

Technical skill and global air-motor-rail interface

Technical skill and global air-motor interface

Technical skill and global air-motor-rail interface

Infrastructure and support capabilities

Infrastructure and labor skill

Government regulations

Load limits Load limits

Competitive tax climate Ideal for heavy manufacturing

Availability of human, land, supplier, and financial capital

Technical talent and global SC skills

Technical talent and global SC skills

Technical talent and global SC skills

Available DC capacity

Economic competitiveness and lowest total cost to serve

Reduced cost of uncertainty due to less congestion

Reduced cost of uncertainty due to less congestion

Reduced cost of uncertainty due to less congestion

Supply chain sustainability

Minimal uncertainty

Reliable weather

Minimal uncertainty Reliable weather

Minimal uncertainty Reliable weather

Collaboration and partnership

Strong private sector message

- 55 -

Supply Chain Hub Strategy CreationSupply Chain Hub Strategy Creation

Strategy and SCM Strategy Elements

Industries offering

Value Add Potential

Economic and Job Creation Impact

- 56 -

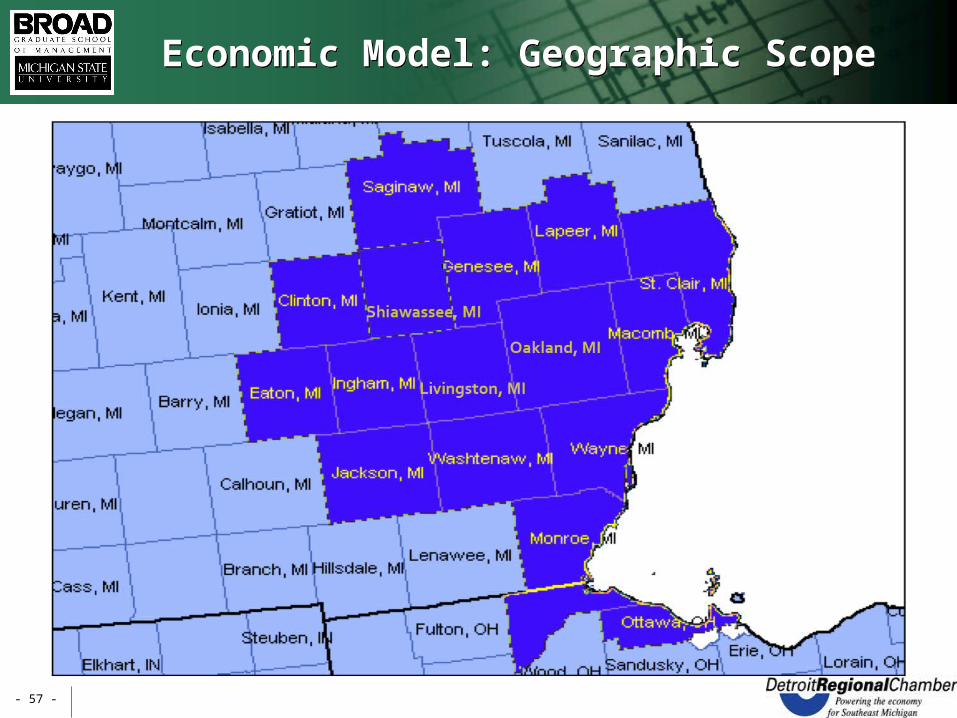

Geographic Scope of Economic ModelingGeographic Scope of Economic Modeling

• The region or scope of the project is the SEMI/NWOH/SWON regional hub

• Canadian data for the economic modeling activity required a long lead time to secure and thus was not available for the economic analysis

• The economic modeling results reflect the impact on the SEMI/NWOH region only

• Including SWON data into the analysis at a later date will increase the positive economic results of the project

- 57 -

Economic Model: Geographic Scope Economic Model: Geographic Scope

- 58 -

Three Stages of SCM Economic ActivityThree Stages of SCM Economic Activity

Stage 1 (Current)

Economic activity associated with SCM

Stage 2 (+3 years)

Economic activity associated with SCM

following recovery

Stage 3 (+7 to10 years)

Enhanced economic activity associated with SCM scale

and industry attraction

- 59 -

What Does it Take to Go from Stage 2 to Stage 3?What Does it Take to Go from Stage 2 to Stage 3?

Stage 2 (+3 years)

Economic activity associated with SCM

following recovery

Stage 3 (+7 to10 years)

Enhanced economic activity associated with SCM scale

and industry attraction

Stage 1 (Current)

Economic activity associated with SCM

- 60 -

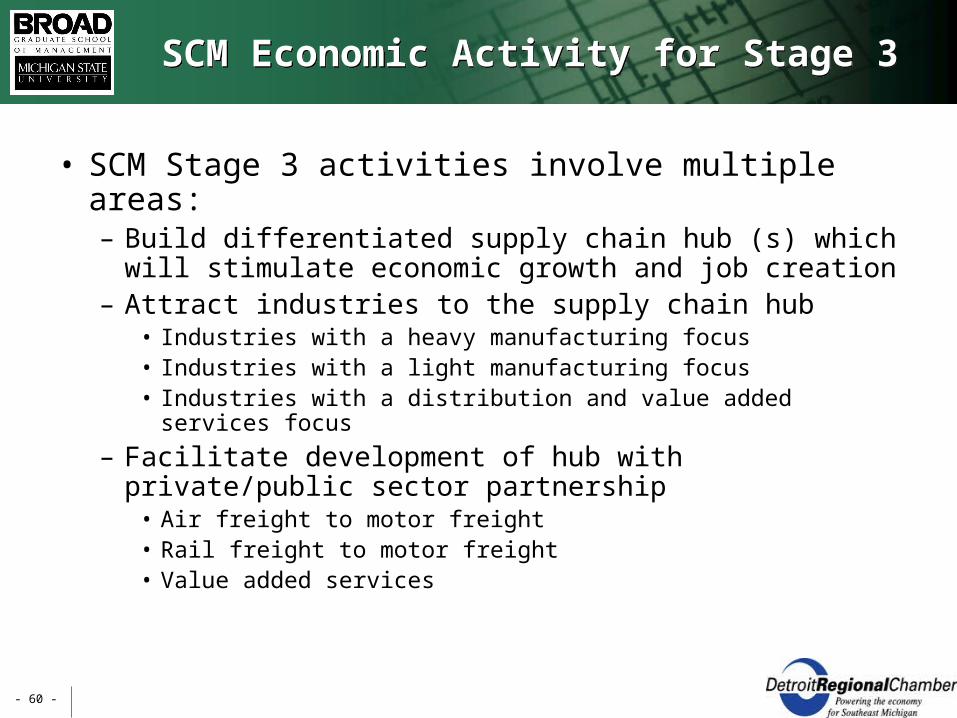

SCM Economic Activity for Stage 3SCM Economic Activity for Stage 3

• SCM Stage 3 activities involve multiple areas:– Build differentiated supply chain hub (s) which will

stimulate economic growth and job creation– Attract industries to the supply chain hub

• Industries with a heavy manufacturing focus• Industries with a light manufacturing focus• Industries with a distribution and value added services focus

– Facilitate development of hub with private/public sector partnership

• Air freight to motor freight • Rail freight to motor freight• Value added services

- 61 -

Economic and Job ProjectionsEconomic and Job Projections

• U.S. base economic activity level in dollars (Source: IBISWorld Industry Market Research Reports)

• Determine Great Lakes regional activity (Source: IBISWorld)

• Determine Michigan economic activity based on relative population

• Establish base Michigan economic activity level (economic and jobs) – Stage 2

• Estimate economic growth potential based on Michigan share of industry (economies of scale) and growth (attraction) – Stage 3

- 62 -

Target Industry EvaluationTarget Industry Evaluation

• Growth Opportunity:– Organic: New growth from existing industries– Opportunistic: Growth resulting from market share shift– Innovative: New growth from industry innovations

• Growth potential – dependent on historical growth (5 years), projected growth (5 years), current share, and potential for locational synergy – 1.00 would be neutral growth

• Change perception– Increase probability of success– Emphasize competitive strategy elements– Define common and consistent strategy– Communicate strategy

- 63 -

Industry Forecasts – Heavy ManufacturingIndustry Forecasts – Heavy Manufacturing

Industry Growth Opportunity Growth Potential

Automotive renewal Organic and Innovative 1.20-1.30

Alternative energy Organic and Innovative 1.08-1.65

Carbon fiber manufacturing Opportunistic and Innovative 1.30

Chemical processing Organic and Innovative 1.11

Defense Opportunistic and Innovative 1.13

Electronics - industrial Opportunistic and Innovative 1.19-1.40

- 64 -

Economic Evaluation: Heavy ManufacturingEconomic Evaluation: Heavy Manufacturing

Industry Stage 2 Economic

Forecast ($M)

Stage 3 Economic

Forecast with Hub

($M)

Increase Resulting from Hub

($M)

Stage 2 Job

Activity (000)

Stage 3 Job

Activity with Hub

(000)

Increase Resulting from Hub

(000)

Automotive renewal

5,084 6,609 1,525 62.7 81.5 18.8

Alternative energy

757 1,056 299 4.0 5.5 1.5

Chemical processing

6,682 7,717 1,035 56.6 65.4 8.8

Defense 3,739 4,461 722 24.0 28.7 4.7

Electronics -Industrial

4,069 5,250 1,181 22.0 28.4 6.4

Forestry and bio-fuels

919 1,231 312 2.8 3.8 1.0

Total 21,250 26,324 5,074 172.1 213.3 41.2

- 65 -

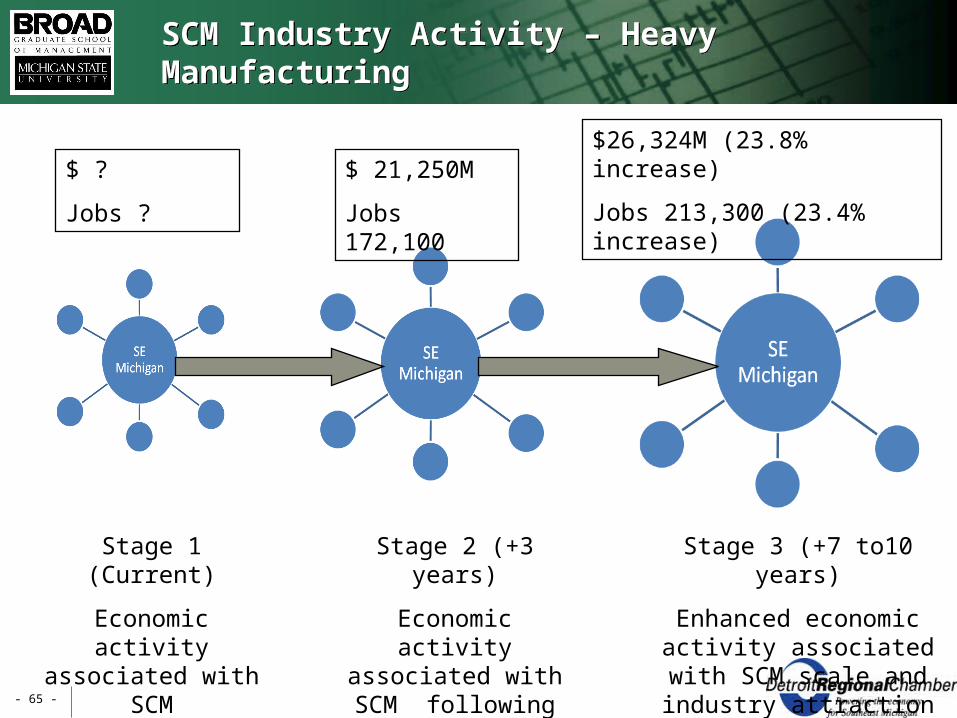

SCM Industry Activity – Heavy ManufacturingSCM Industry Activity – Heavy Manufacturing

$ ?

Jobs ?

$ 21,250M

Jobs 172,100

$26,324M (23.8% increase)

Jobs 213,300 (23.4% increase)

Stage 1 (Current)

Economic activity associated with SCM

Stage 2 (+3 years)

Economic activity associated with SCM

following recovery

Stage 3 (+7 to10 years)

Enhanced economic activity associated with SCM scale

and industry attraction

- 66 -

Industry Forecasts – Light ManufacturingIndustry Forecasts – Light Manufacturing

Industry Growth Opportunity Growth Potential

Food processing Organic, Opportunistic, and Innovative

0.87-1.11

Medical technologies Innovative 1.23

Water technologies Innovative 1.19

- 67 -

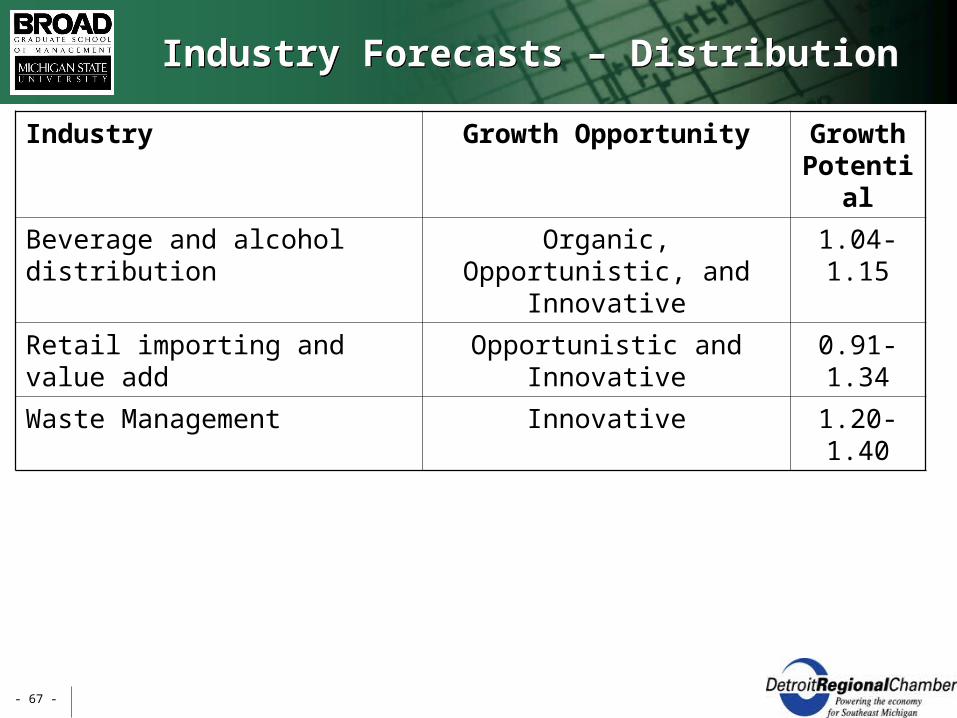

Industry Forecasts – DistributionIndustry Forecasts – Distribution

Industry Growth Opportunity Growth Potential

Beverage and alcohol distribution

Organic, Opportunistic, and Innovative

1.04-1.15

Retail importing and value add Opportunistic and Innovative 0.91-1.34

Waste Management Innovative 1.20-1.40

- 68 -

Economic Evaluation: Light Manufacturing, DistributionEconomic Evaluation: Light Manufacturing, Distribution

Industry Stage 2 Economic

Forecast ($M)

Stage 3 Economic

Forecast with Hub

($M)

Increase Resulting from Hub

($M)

Stage 2 Job

Activity (000)

Stage 3 Job

Activity with Hub

(000)

Increase Resulting from Hub

(000)

Food, beverage

9,550 10,285 735 82.6 89.0 6.4

Wholesale trade

4,573 6,127 1,554 20.0 26.8 6.8

Retail trade 5,123 6,864 1,741 15.1 20.3 5.2

Warehouse & storage

3,659 4,902 1,243 11.1 14.9 3.8

Waste management

2,946 3,572 626 15.2 18.5 3.3

Total 25,851 31,750 5,476 144.0 169.5 25.5

- 69 -

SCM Industry Activity – Light Manufacturing/DistributionSCM Industry Activity – Light Manufacturing/Distribution

$ ?

Jobs ?

$ 25,851 M

Jobs 144,000

$ 31,750 M (22.8% increase)

Jobs 169,500 (17.7% increase)

Stage 1 (Current)

Economic activity associated with SCM

Stage 2 (+3 years)

Economic activity associated with SCM

following recovery

Stage 3 (+7 to10 years)

Enhanced economic activity associated with SCM scale

and industry attraction

- 70 -

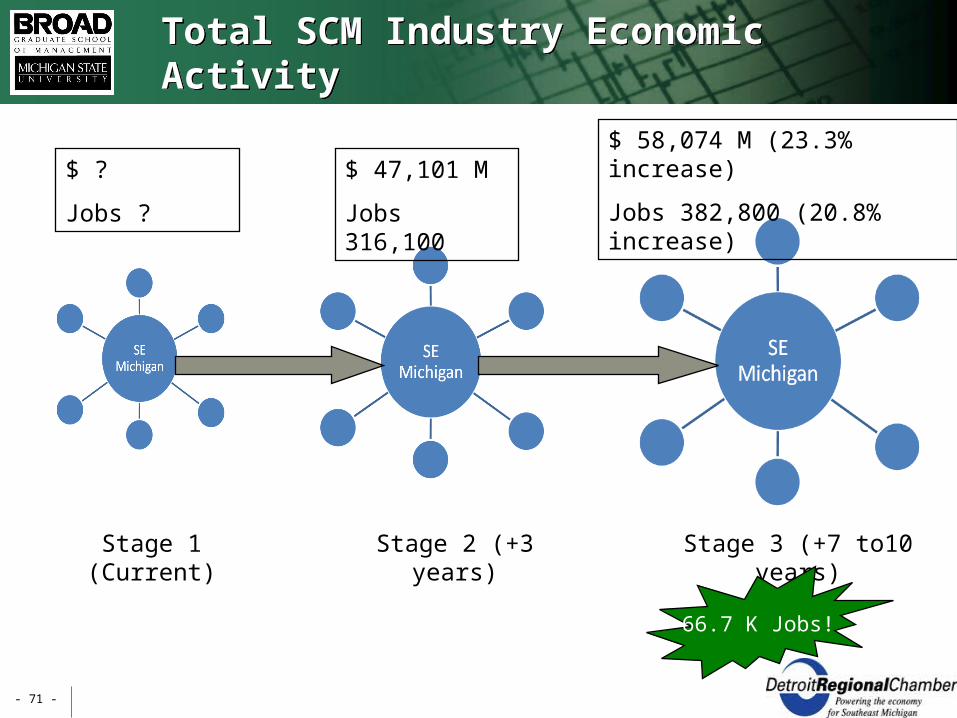

Total SCM Industry Economic ActivityTotal SCM Industry Economic Activity

$ ?

Jobs ?

$ 47,101 M

Jobs 316,100

$ 58,074 M (23.3% increase)

Jobs 382,800 (20.8% increase)

Stage 1 (Current)

Economic activity associated with SCM

Stage 2 (+3 years)

Economic activity associated with SCM

following recovery

Stage 3 (+7 to10 years)

Enhanced economic activity associated with SCM scale

and industry attraction

- 71 -

Total SCM Industry Economic ActivityTotal SCM Industry Economic Activity

$ ?

Jobs ?

$ 47,101 M

Jobs 316,100

$ 58,074 M (23.3% increase)

Jobs 382,800 (20.8% increase)

Stage 1 (Current) Stage 2 (+3 years) Stage 3 (+7 to10 years)

66.7 K Jobs!

- 72 -

Supply Chain Hub Strategy CreationSupply Chain Hub Strategy Creation

Strategy and SCM Strategy Elements

Industries offering

Value Add Potential

Economic and Job Creation Impact

Economic Development

- 73 -

Presentation OutlinePresentation Outline

• Project Background • Project Objectives and Workshop Deliverables• SCM Strategy, Targeted Industries, and

Economic Impact• Economic Development Policies and

Collaboration and Communications• Recommendations and Next Steps

- 74 -

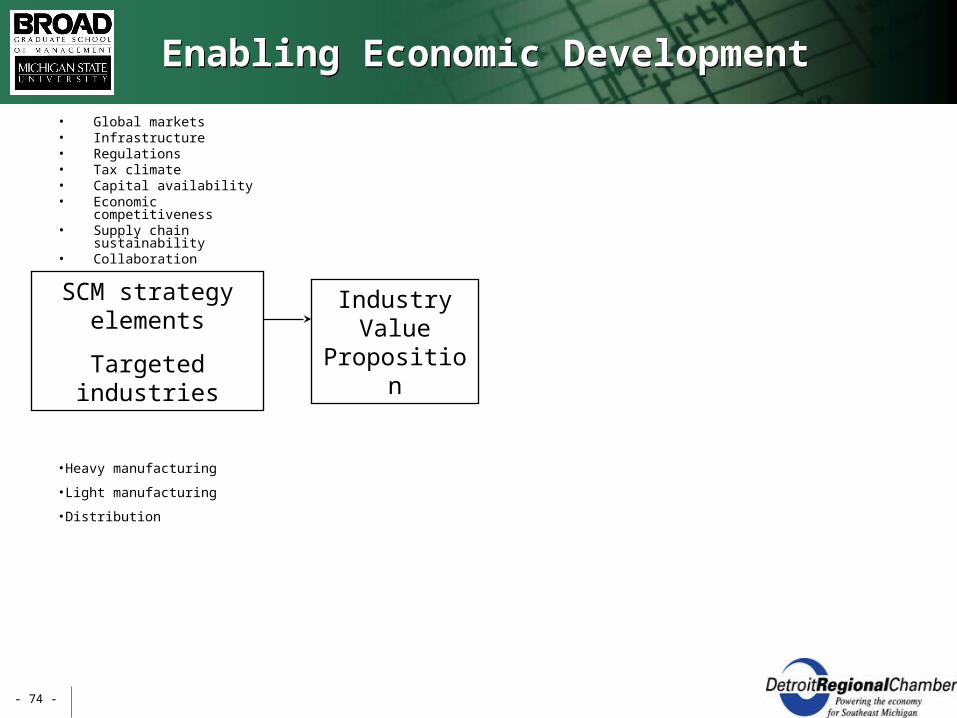

Enabling Economic DevelopmentEnabling Economic Development

SCM strategy elements

Targeted industries

Industry Value

Proposition

• Global markets• Infrastructure• Regulations• Tax climate• Capital availability• Economic competitiveness• Supply chain sustainability• Collaboration

•Heavy manufacturing

•Light manufacturing

•Distribution

- 75 -

Enabling Economic DevelopmentEnabling Economic Development

SCM strategy elements

Targeted industries

Industry Value

Proposition

Economic development

Job creation

• Global markets• Infrastructure• Regulations• Tax climate• Capital availability• Economic competitiveness• Supply chain sustainability• Collaboration

•Heavy manufacturing

•Light manufacturing

•Distribution

66.7 K Jobs!

- 76 -

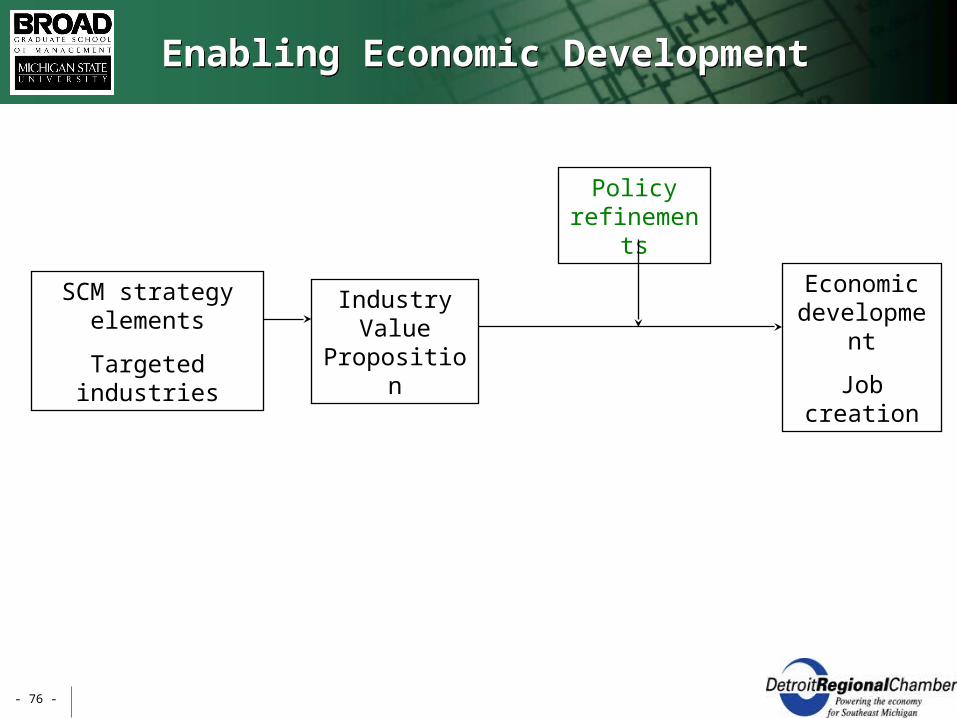

Enabling Economic DevelopmentEnabling Economic Development

SCM strategy elements

Targeted industries

Industry Value

Proposition

Economic development

Job creation

Policy refinements

- 77 -

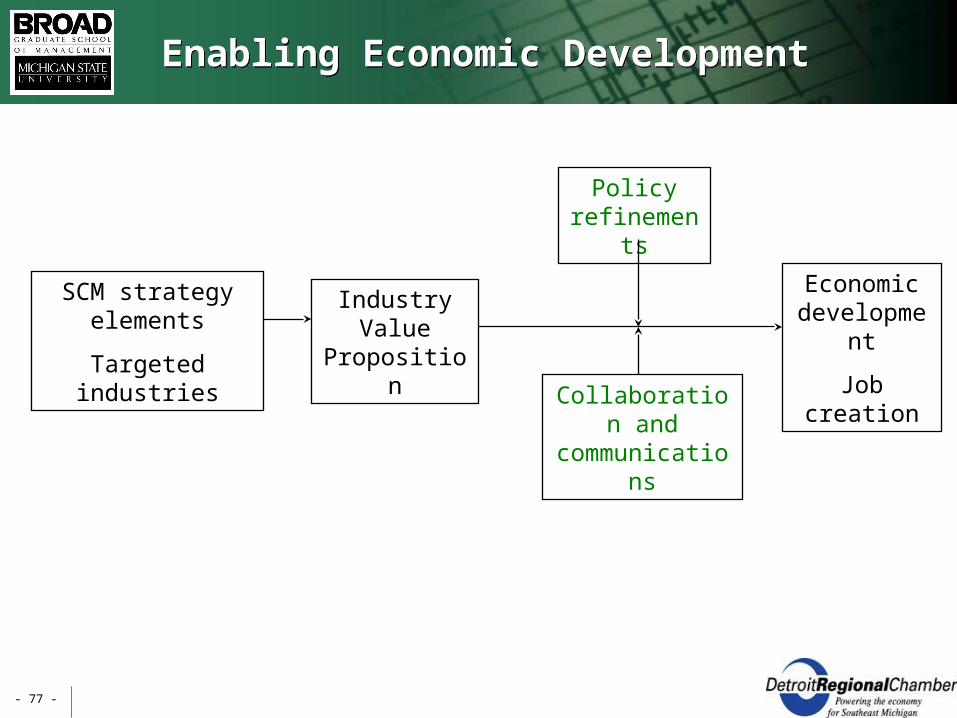

Enabling Economic DevelopmentEnabling Economic Development

SCM strategy elements

Targeted industries

Industry Value

Proposition

Economic development

Job creation

Policy refinements

Collaboration and

communications

- 78 -

Enabling Economic Development: Policy RefinementsEnabling Economic Development: Policy Refinements

SCM strategy elements

Targeted industries

Industry Value

Proposition

Economic development

Job creation

Policy refinements

- 79 -

Policies to Enable Economic DevelopmentPolicies to Enable Economic Development

• Ability to serve global markets• Infrastructure and support capabilities• Streamlined government environment• Competitive tax climate• Availability of human, land, supplier, and

financial capital• Economic competitiveness and lowest total

cost to serve• Supply chain sustainability

- 80 -

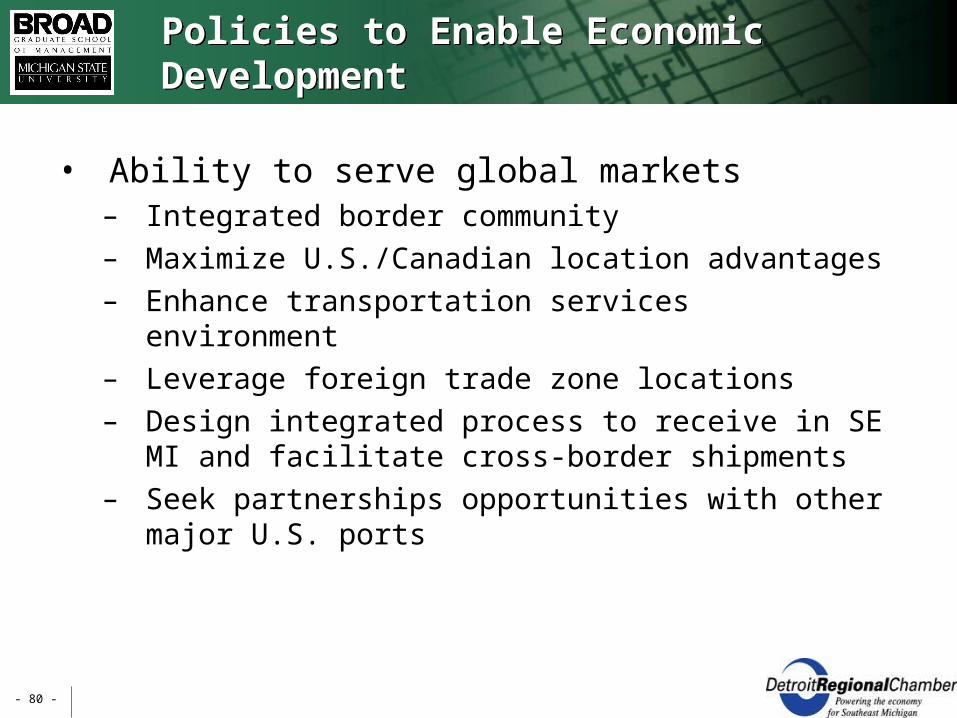

Policies to Enable Economic DevelopmentPolicies to Enable Economic Development

• Ability to serve global markets– Integrated border community– Maximize U.S./Canadian location advantages– Enhance transportation services environment– Leverage foreign trade zone locations– Design integrated process to receive in SE MI and

facilitate cross-border shipments– Seek partnerships opportunities with other major

U.S. ports

- 81 -

Policies to Enable Economic DevelopmentPolicies to Enable Economic Development

• Ability to serve global markets• Infrastructure and support capabilities

– Create development incentives associated with transportation assets

– Tie economic development and site location to transportation assets

– Allow private investment in transport infrastructure– Coordinate between all modes of transportation

- 82 -

Policies to Enable Economic DevelopmentPolicies to Enable Economic Development

• Ability to serve global markets• Infrastructure and support capabilities• Streamlined government environment

– Incentivize use of brownfield properties for transportation and distribution

– “One stop permitting”– Neutral entity to implement and drive logistics in SE

MI, SW Ontario, and NW Ohio

- 83 -

Policies to Enable Economic DevelopmentPolicies to Enable Economic Development

• Ability to serve global markets• Infrastructure and support capabilities• Streamlined government environment• Competitive tax climate

– Reduce corporate tax burden– Equalize local tax structures– Block implementation of state service tax on B2B

transactions

- 84 -

Policies to Enable Economic DevelopmentPolicies to Enable Economic Development

• Ability to serve global markets• Infrastructure and support capabilities• Streamlined government environment• Competitive tax climate• Availability of human, land, supplier, and

financial capital– Enhance commercialization of Michigan university

supply chain talent– Connect trained workforce directly to employers

- 85 -

Policies to Enable Economic DevelopmentPolicies to Enable Economic Development

• Ability to serve global markets• Infrastructure and support capabilities• Streamlined government environment• Competitive tax climate• Availability of human, land, supplier, and financial

capital• Economic competitiveness and lowest total cost to

serve– Reduce costs to transportation industry– Maintain advantage with state load limits– Promote advantages of integrated cross-border service

potential

- 86 -

Policies to Enable Economic DevelopmentPolicies to Enable Economic Development

• Ability to serve global markets• Infrastructure and support capabilities• Streamlined government environment• Competitive tax climate• Availability of human, land, supplier, and financial

capital• Economic competitiveness and lowest total cost to

serve• Supply chain sustainability

– Emphasize role that reduced uncertainty and more proximate sourcing can have on enterprise sustainability

– Provide incentives for lower and reduced environmental impact for shippers and carriers

- 87 -

Enabling Economic Development:Collaboration and CommunicationsEnabling Economic Development:Collaboration and Communications

SCM strategy elements

Targeted industries

Industry Value

Proposition

Economic development

Job creation

Policy refinements

Collaboration and

communications

- 88 -

Collaboration and Communication to Enable Economic DevelopmentCollaboration and Communication to Enable Economic Development

• Collaboration and communication– Communicate the benefits of reduced SC operating

uncertainty in Midwest– Communicate common and credible voice to policy

makers with an industry perspective– Create an operational SCM Development entity to

be a single voice to coordinate, promote, facilitate, and advance SE MI supply chain initiatives (e.g., Georgia, Columbus, Indianapolis, Kansas City, and Virginia)

- 89 -

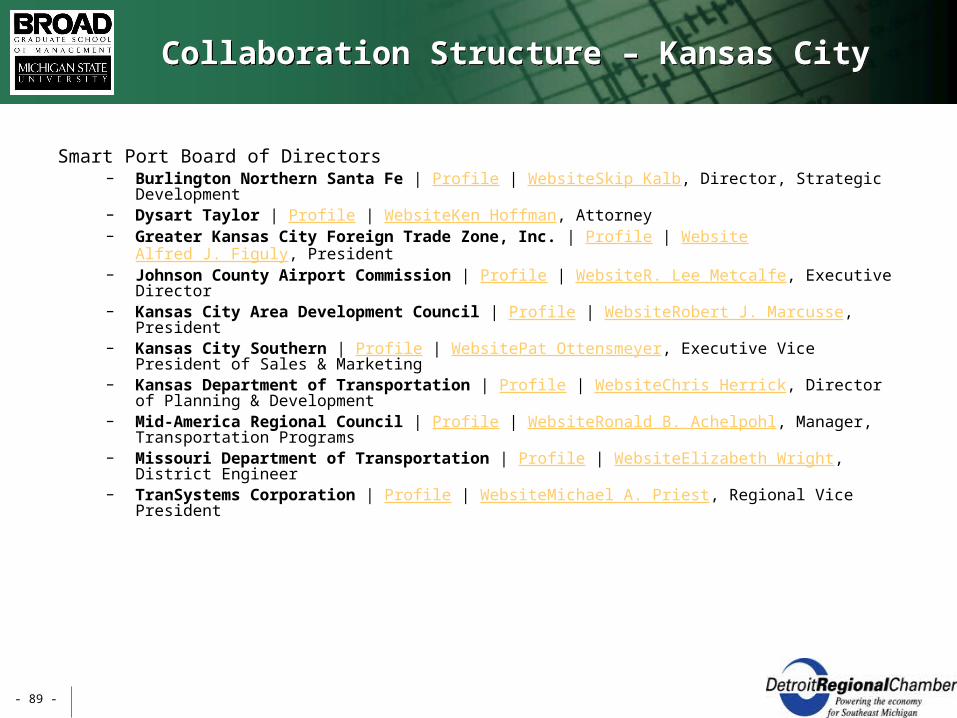

Collaboration Structure – Kansas CityCollaboration Structure – Kansas City

Smart Port Board of Directors– Burlington Northern Santa Fe | Profile | WebsiteSkip Kalb, Director, Strategic Development– Dysart Taylor | Profile | WebsiteKen Hoffman, Attorney– Greater Kansas City Foreign Trade Zone, Inc. | Profile | WebsiteAlfred J. Figuly, President – Johnson County Airport Commission | Profile | WebsiteR. Lee Metcalfe, Executive Director – Kansas City Area Development Council | Profile | WebsiteRobert J. Marcusse, President – Kansas City Southern | Profile | WebsitePat Ottensmeyer, Executive Vice President of Sales & Marketing – Kansas Department of Transportation | Profile | WebsiteChris Herrick, Director of Planning &

Development – Mid-America Regional Council | Profile | WebsiteRonald B. Achelpohl, Manager, Transportation Programs – Missouri Department of Transportation | Profile | WebsiteElizabeth Wright, District Engineer– TranSystems Corporation | Profile | WebsiteMichael A. Priest, Regional Vice President

- 90 -

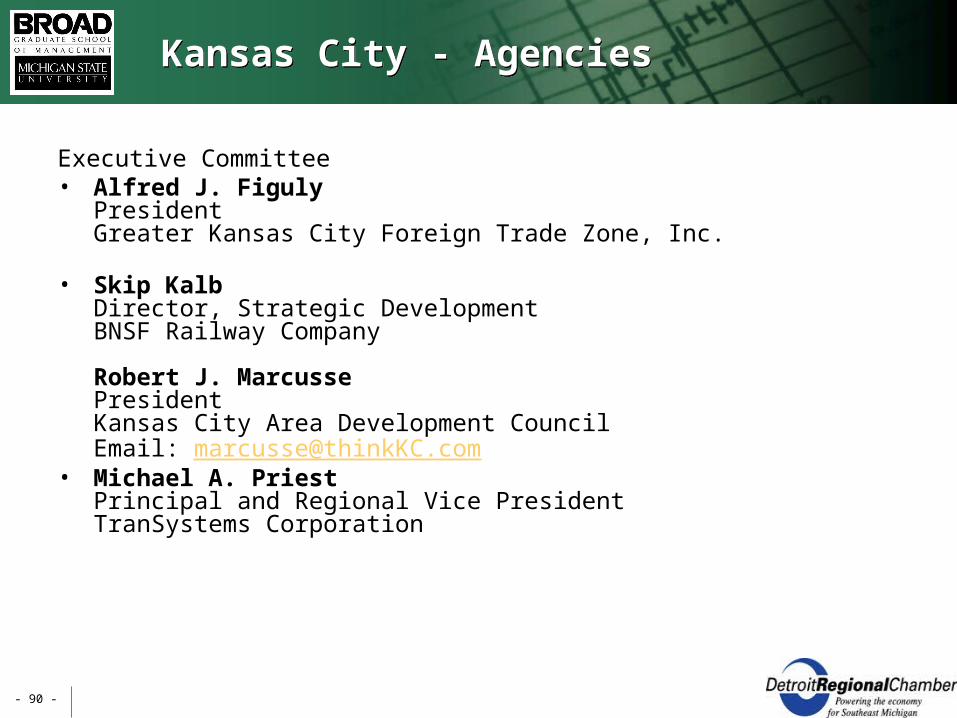

Kansas City - AgenciesKansas City - Agencies

Executive Committee• Alfred J. Figuly

President Greater Kansas City Foreign Trade Zone, Inc.

• Skip Kalb Director, Strategic DevelopmentBNSF Railway Company

Robert J. MarcussePresident Kansas City Area Development Council Email: [email protected]

• Michael A. Priest Principal and Regional Vice President TranSystems Corporation

- 91 -

Collaboration Structure – Columbus, OHColumbus Region Logistics Council Collaboration Structure – Columbus, OHColumbus Region Logistics Council

ODW LogisticsBattelle Memorial InstituteColumbus ChamberAbbott NutritionBig LotsCardinal HealthColumbus Regional Airport AuthorityColumbus State Community CollegeCSX IntermodalDB Schenker Logistics

DSW ShoesExelHonda of America Mfg., Inc.KraftLimited BrandsMcGraw HillNorfolk SouthernPacer InternationalSpartan LogisticsSterling CommerceThe Ohio State UniversityThe Pizzuti CompaniesUPS

- 92 -

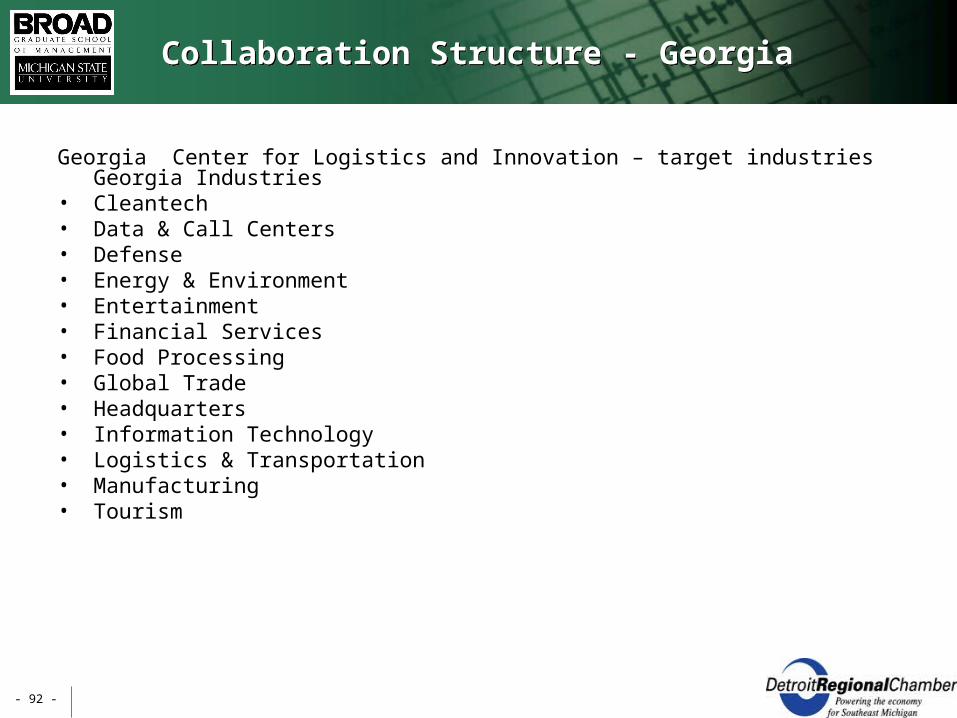

Collaboration Structure - GeorgiaCollaboration Structure - Georgia

Georgia Center for Logistics and Innovation – target industries Georgia Industries• Cleantech • Data & Call Centers • Defense • Energy & Environment • Entertainment • Financial Services • Food Processing • Global Trade • Headquarters • Information Technology • Logistics & Transportation • Manufacturing • Tourism

- 93 -

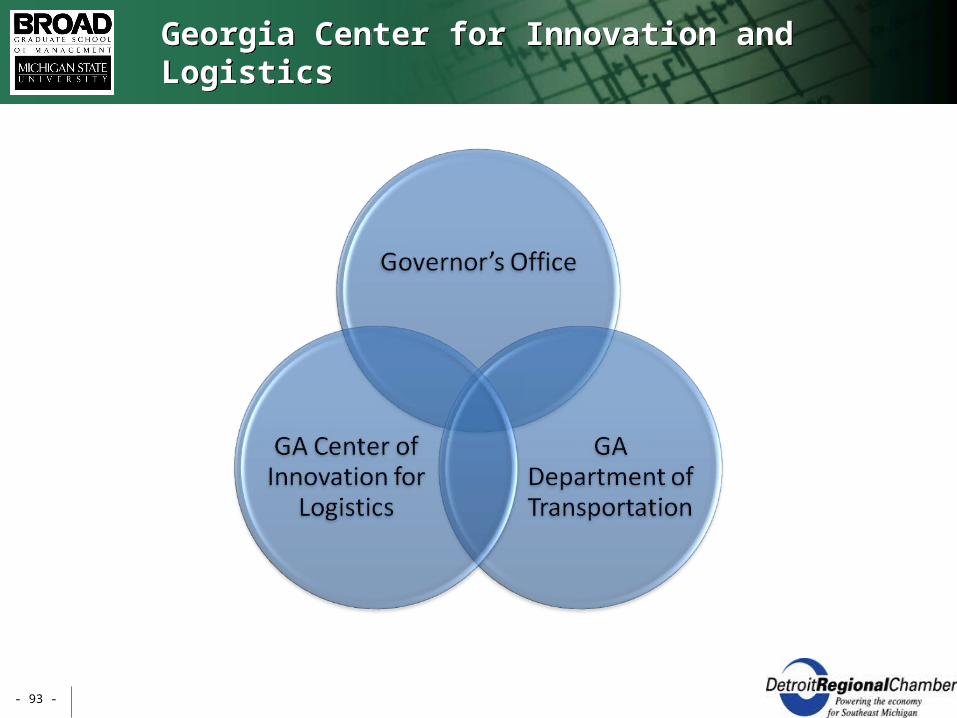

Georgia Center for Innovation and LogisticsGeorgia Center for Innovation and Logistics

- 94 -

Georgia Center for Innovation and LogisticsGeorgia Center for Innovation and Logistics

• Wide range of stakeholders to address logistics issues. problem holder–problem solver model.

• "Problem Holders" come from logistics, shipping and transportation entities. Driven by real-world experiences, they bring complex challenges and opportunities to the table.

• "Problem Solvers" come from the worlds of academia and technology, from entrepreneurial to established companies. They contribute a unique technological perspective and can often provide the most objective analysis of an industry issue.

• Logistics is comprised of many firms operating independently and interdependently; and all are reliant upon a common infrastructure - in essence, a "logistics ecosystem."

• The Center of Innovation for Logistics is focused on identifying a structure from which everyone can work: a unique set of resources detailing the composition and impact of logistics throughout Georgia.

- 95 -

Why is Collaboration and Communication Necessary to increase Scale and Attractiveness?Why is Collaboration and Communication Necessary to increase Scale and Attractiveness?

• Reduces likelihood of redundant infrastructure investments

• Increases potential for critical scale through effective investments, borrowing, and grants

• Communicates the message in context of supply chain performance benefits to the firm rather than economic development benefits for the region

• Communicates a common, consistent message to potential clients

- 96 -

Presentation OutlinePresentation Outline

• Project Background • Project Objectives and Workshop Deliverables• SCM Strategy, Targeted Industries, and

Economic Impact• Economic Development Policies and

Collaboration and Communications• Recommendations and Next Steps

- 97 -

Project Findings and RecommendationsProject Findings and Recommendations

• Opportunity Assessment has re-enforced the economic development potential for the Hub– 66,000 new jobs created– Doing nothing may run the risk of additional jobs lost

• Hub organizational model should include all impacted stakeholders; both public and private stakeholders

• Key Hub competencies should include supply chain expertise, economic development, collaboration, and grantsmanship

• Maintaining momentum over the next few months will be critical to project success

- 98 -

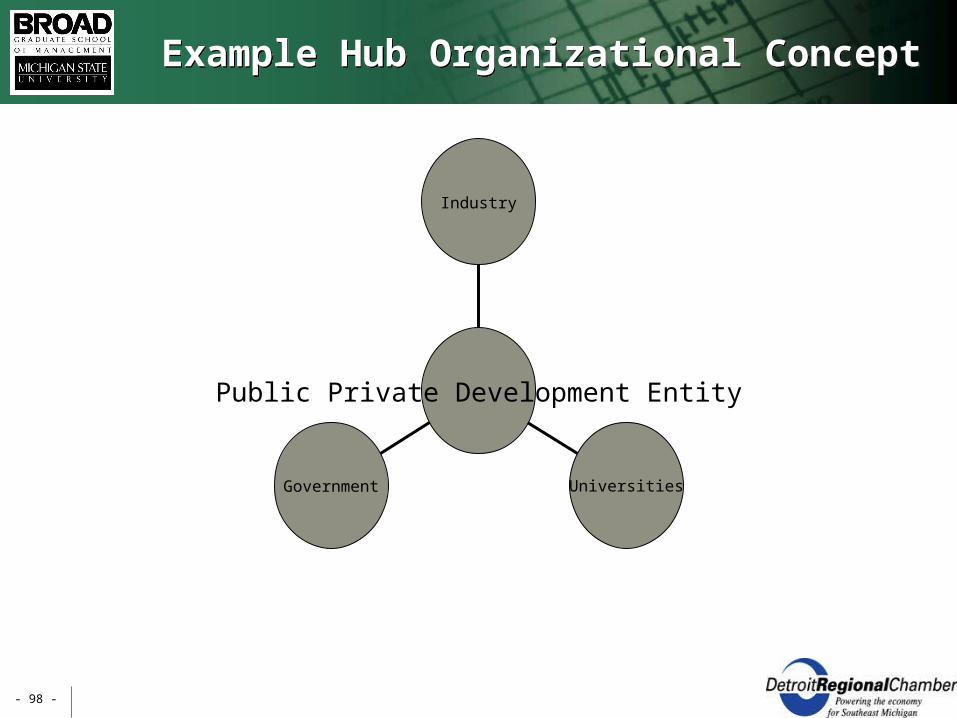

Example Hub Organizational ConceptExample Hub Organizational Concept

Government Universities

Industry

Public Private Development Entity

- 99 -

Key Hub CompetenciesKey Hub Competencies

• Supply Chain Expertise– Design of supply chain solutions for Industry– Monitoring to assure effective implementation of solutions for

industry• Economic Development

– Marketing and communications of supply chain solutions to targeted industry

– Creation of industry partner communities• Collaboration

– Collaboration scope is regional, multi-state, and international– Stakeholders work together to design, market and implement

supply chain solutions– Monitor results to assure hub success; Jobs created and value

created for industry• Grantsmanship

– Design of the regional physical infrastructure footprint for the supply chain hub(s)

– Pursue funding to finance the infrastructure improvements

- 100 -

Supply Chain Opportunity Assessment:Next StepsSupply Chain Opportunity Assessment:Next Steps

• Identify key public and private stakeholders who will be critical for project implementation

• Continue with workshop meetings to implement project findings and recommendations

• Identify leader organization and governance to implement the supply chain and economic development strategies

• Pilot the implementation of the strategy by designing and implementing a supply chain solution for an industry

- 101 -

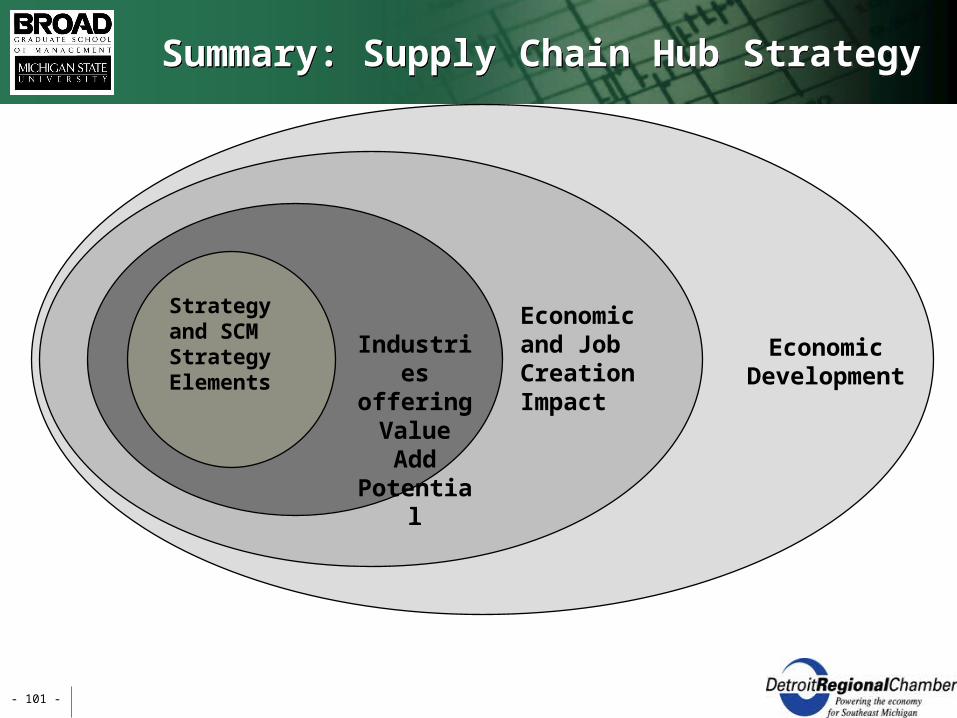

Summary: Supply Chain Hub StrategySummary: Supply Chain Hub Strategy

Strategy and SCM Strategy Elements

Industries offering

Value Add Potential

Economic and Job Creation Impact

Economic Development