© Jean-Bernard Caen 2005 & + 1 Powering up Economic Capital: Overcoming Barriers To Achieve...

21

© Jean-Bernard Caen 2005 & + 1 Powering up Economic Capital: Overcoming Barriers To Achieve Effective Implementation Jean-Bernard Caen – DEXIA Head of Economic Capital <This document presents the point of view of its author, which may differ from DEXIA’s. It supports an oral presentation and is incomplete without it. This support is protected by copyright laws.> July 27 th , 2005

-

date post

19-Dec-2015 -

Category

Documents

-

view

222 -

download

0

Transcript of © Jean-Bernard Caen 2005 & + 1 Powering up Economic Capital: Overcoming Barriers To Achieve...

© Jean-Bernard Caen 2005 & + 1

Powering up Economic Capital:

Overcoming Barriers To Achieve

Effective Implementation

Jean-Bernard Caen – DEXIA Head of Economic Capital

<This document presents the point of view of its author, which may differ from DEXIA’s.It supports an oral presentation and is incomplete without it.

This support is protected by copyright laws.>

July 27th, 2005

© Jean-Bernard Caen 2005 & + 2

DEXIA at a glance

World Leader in Public Finance• 620b€ (750b$) credit exposure in the USA (41%), Belgium

(14%), France (13%), Italy (12%)

A diversified Financial Group • A Retail network in Benelux• Investment Management Services in Luxembourg• Capital Market activities

Highly profitable• Net Income reached 1.8b€ (2.2b$) in FY 2004, 20% ROE• Market Capitalization is 20b€ (24b$) – 15th European bank

© Jean-Bernard Caen 2005 & + 3

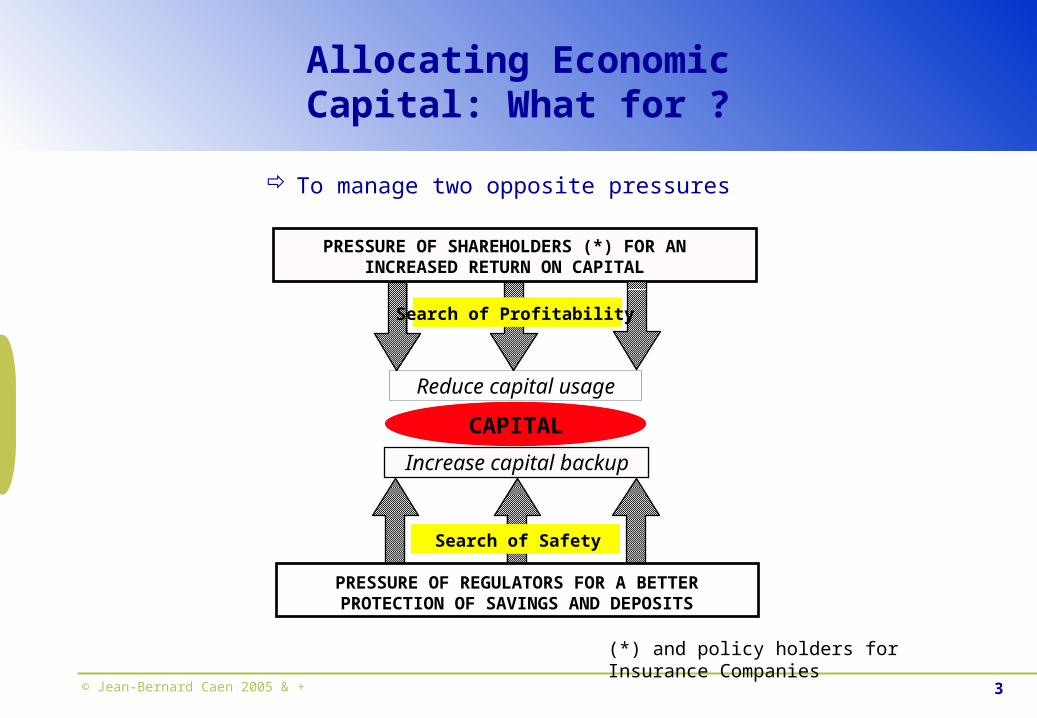

Allocating Economic Capital: What for ?

To manage two opposite pressures

Increase capital backup

Search of Safety

PRESSURE OF REGULATORS FOR A BETTERPROTECTION OF SAVINGS AND DEPOSITS

Reduce capital usage

CAPITAL

PRESSURE OF SHAREHOLDERS (*) FOR ANINCREASED RETURN ON CAPITAL

Search of Profitability

(*) and policy holders for Insurance Companies

© Jean-Bernard Caen 2005 & + 4

Maximal value creation requires optimal Capital allocation

√ Capital allocation supports long term value creation√ Explicit allocation of long term resources

High

Expected Return

Low

Areas of Excellence

Competitors Arena

HighLowRisk

CapitalAllocation

© Jean-Bernard Caen 2005 & + 5

ECAP potential benefits are huge

ECAP creates value• Better strategic development decisions• Incentives in line with shareholders interests

ECAP brings in higher returns• Effective external pricing policy• Effective internal funds transfer pricing

ECAP reduces risk• Reduction of Credit Concentration• Disclosures transparency reduces risk for shareholders

© Jean-Bernard Caen 2005 & + 6

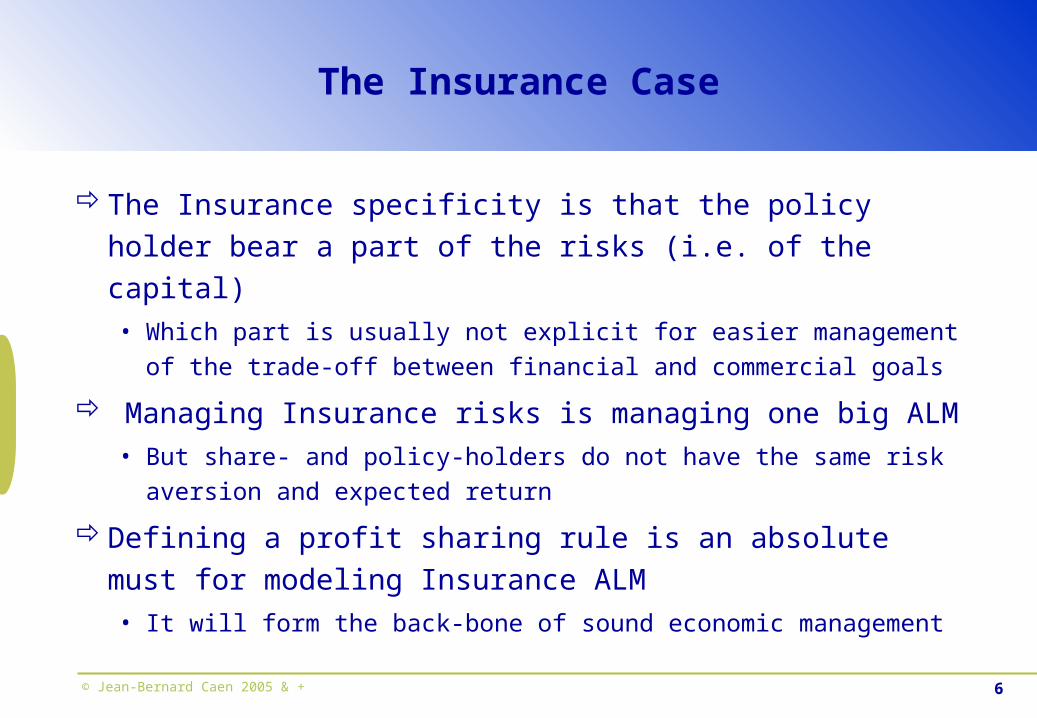

The Insurance Case

The Insurance specificity is that the policy holder bear a part of the risks (i.e. of the capital)• Which part is usually not explicit for easier management of

the trade-off between financial and commercial goals

Managing Insurance risks is managing one big ALM• But share- and policy-holders do not have the same risk

aversion and expected return

Defining a profit sharing rule is an absolute must for modeling Insurance ALM• It will form the back-bone of sound economic management

© Jean-Bernard Caen 2005 & + 7

The range and scope of Economic Capital (ECAP) potential uses are wide

1. Regulatory constraint

2. Common metrics for measuring risks

3. Limits

4. Performance measurement and value analysis

5. Effective pricing of risk

6. Credit Portfolio management

7. Reduction of Excess Capital

8. Managers compensation and incentives in line

with shareholders interest

9. External disclosure of risk profile

Why aren’t these functions implemented?

© Jean-Bernard Caen 2005 & + 8

The product has big potential benefits.Where can the production process be blocked?

ARE BIG POTENTIAL BENEFITS ENOUGH TO:• Start an Economic Capital function? YES

Finance or Risk line?

• Allocate adequate resources? MAY BE The ear of the boss

• Read the out coming results? MAY BE One more reporting…

• Make decisions based upon Economic Capital? NO Too new, too volatile, too strange, too technical Difficult to back-test, to handle, to pilot

THERE IS A REAL HAZARD TO BE STUCK AT THAT STAGE!!

© Jean-Bernard Caen 2005 & + 9

CAP…CAP…CAP…The hen house is noisy

CAPITAL has become a buzzword• One word with multiple meanings =>

Which CAPITAL: Accounting? Regulatory? Economic?• Three referential with many interactions

Which CAPITAL: Used? Required? Available?• Three natures of capital

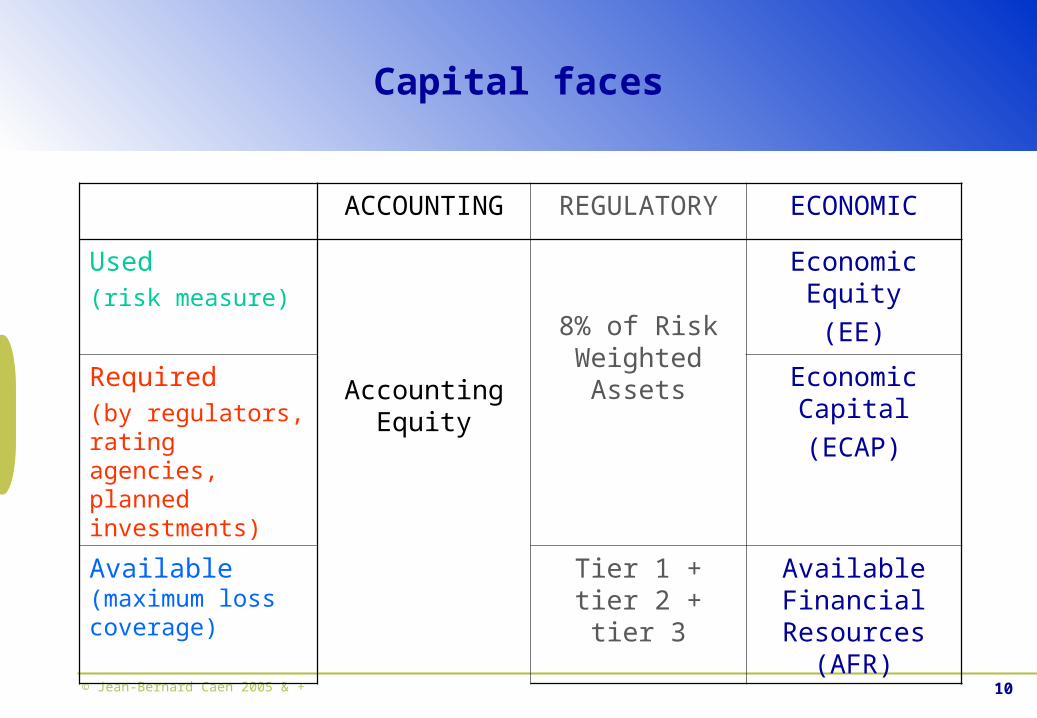

© Jean-Bernard Caen 2005 & + 10

Capital faces

ACCOUNTING REGULATORY ECONOMIC

Used(risk measure)

Accounting Equity

8% of Risk Weighted

Assets

Economic Equity(EE)

Required(by regulators, rating agencies, planned investments)

Economic Capital(ECAP)

Available (maximum loss coverage)

Tier 1 + tier 2 + tier 3

Available Financial

Resources (AFR)

© Jean-Bernard Caen 2005 & + 11

Different Economic Capital for different uses?

Economic Equity (Used)• Risk, measure, neutral metrics across risks and activities Performance assessment, pricing, compensation

Economic Capital (Required)• Resources for business development Strategic planning, M&A, investments

Available Financial Resources (Available)• Maximum loss coverage Capital raising, dividend policy, shares buy back

But … aren’t all these functions already performed without Economic Capital?

© Jean-Bernard Caen 2005 & + 12

Clearly, ECAP offers better decision making…

… than accounting or regulatory capital.But this does not please everybody

• Line managers loose free meals Tighter risk control, improved internal funds transfer pricing

• Basel2 project leaders loose power Regulatory capital not used for decision making

• Financial control looses control Finance people must make room to risk people for strategic planning

• Top management compensation is more volatile Quicker grasp of success … and failures

So … wouldn’t some internal marketing be

welcome?

© Jean-Bernard Caen 2005 & + 13

To whom may Economic Capital benefits be sold?

Sales people• For retail, well-rated counterparts, collateralized transactions,

ECAP-based RAROC leads to lower cost prices than regulatory-based RAROC

Shareholders• Prime beneficiaries if AFR is greater than ECAP

Difficult to reach; try Financial Communication people

Top ManagementLet’s follow up this promising track…

© Jean-Bernard Caen 2005 & + 14

ECAP potential hooks to management concerns

Shareholders• Analysts are quick to press for share buybacks or higher dividends if

they feel the excess capital becomes too high.• AFR follow-up allows the CFO to effectively manage excess capital

Rating agencies• The key to a reasonable cost of funding. Showing out an reasonable

excess capital can comfort rating agencies assessments. Regulators

• An unavoidable constraint to bankers and insurers “It is expected that sophisticated institutions will elect to use formal economic capital models” (Basel2).

Competitors• Most sophisticated banks do have ECAP tools and start using them.

Compensation• The toughest challenge but the sweetest pull. Issues of model

validation and transparency become critical to avoid tensions.

© Jean-Bernard Caen 2005 & + 15

Take over management tools to make ECAP a must

Risk Management reporting• Much of risk reporting focuses on exposures• Some info relates to risk factors (VaR for instance)

Add ECAP as a common metrics to compare risks and their evolutions

Activity reporting• Introduce Economic Profit besides more usual ROEs

Clarify risk/return issues through the analysis of EP changes

Regulatory reporting• Compare regulatory and economic capitals and ratios

Uncover and solve apparent regulatory mishaps

Strategic planning• Promote a framework to discuss growth vs. risk issues

Make friends with Financial Controllers and offer them new insights

© Jean-Bernard Caen 2005 & + 16

Search for leverage in key Committees

New products approvalRisk committees

• Credit : Big transactions• Market : Limit settings

Executive Committees• Investments• M&A

Finance Committees• Challenge strategic planning• Reassess ALM risk / return posture

© Jean-Bernard Caen 2005 & + 17

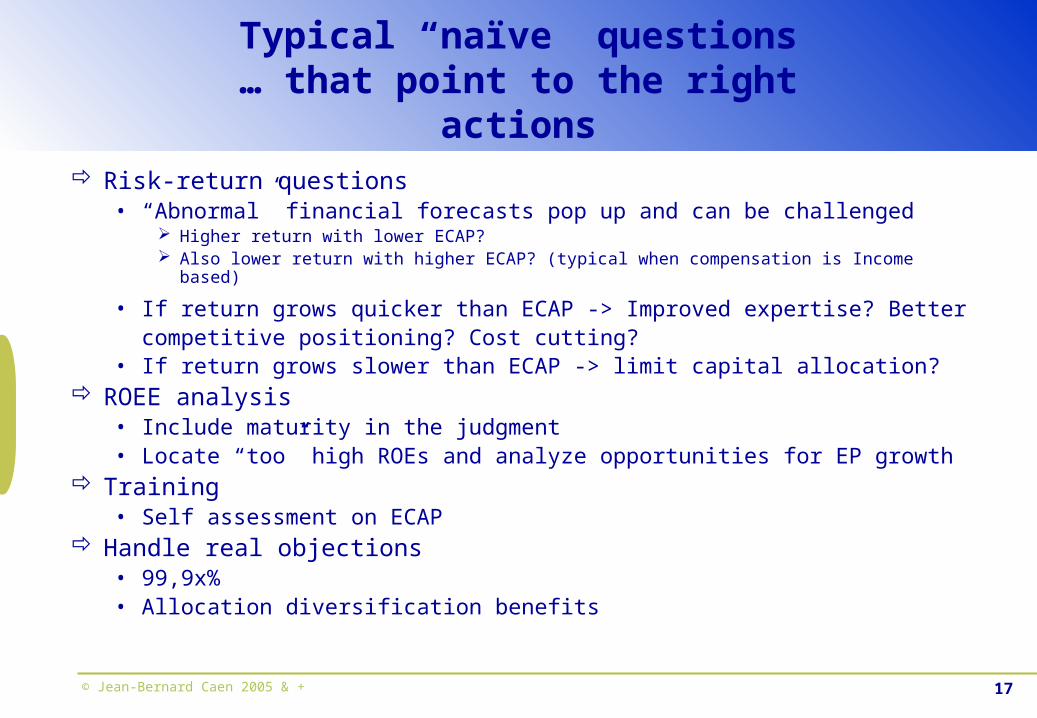

Typical “naïve” questions … that point to the right actions

Risk-return questions• “Abnormal” financial forecasts pop up and can be challenged

Higher return with lower ECAP? Also lower return with higher ECAP? (typical when compensation is Income based)

• If return grows quicker than ECAP -> Improved expertise? Better competitive positioning? Cost cutting?

• If return grows slower than ECAP -> limit capital allocation? ROEE analysis

• Include maturity in the judgment• Locate “too” high ROEs and analyze opportunities for EP growth

Training• Self assessment on ECAP

Handle real objections• 99,9x%• Allocation diversification benefits

© Jean-Bernard Caen 2005 & + 18

Capitalize on current issues(example: from Gaap to IFRS 1/2)

ASSETSFixed-income commercial loans 70Variable-income commercial loans 140Fixed-income mortgages 135Variable-income mortgages 15Consumer loans 40

TOTAL ASSETS 400

Given guaranties 60

LIABILITIES Sight deposits 130 Regulated deposits 105 Debt securities 85 Time deposits 30 Interbank 24 Equity and reserves 26

TOTAL LIABILITIES 400

Received guaranties 20

B/S were initially conceived to provide a reliable profit figure•To act as a robust base for taxation•Formal fitting was more important than economic reality•Historic value of assets and liabilities were adequate for that goal

© Jean-Bernard Caen 2005 & + 19

Capitalize on current issues(example: from Gaap to IFRS 2/2)

ASSETS Commercial loans AAA 70 Commercial loans A 70 Commercial loans BBB 70 Non securitizable mortgages 30 Securitizable mortgages 130 Consumer loans 40

TOTAL ASSETS 410

LIABILITIES AND EQUITY Sight deposits 130 Regulated deposits 105 Debt securities 85 Time deposits 30 Interbank 24 TOTAL LIABILITIES 374

IRB Equity 15 Available capital (IRB) 11 Capital gain 10 TOTAL EQUITY 36

Disclosures of risks and liquidity measuresExplicit elements of capital managementMore transparency and volatility

© Jean-Bernard Caen 2005 & + 20

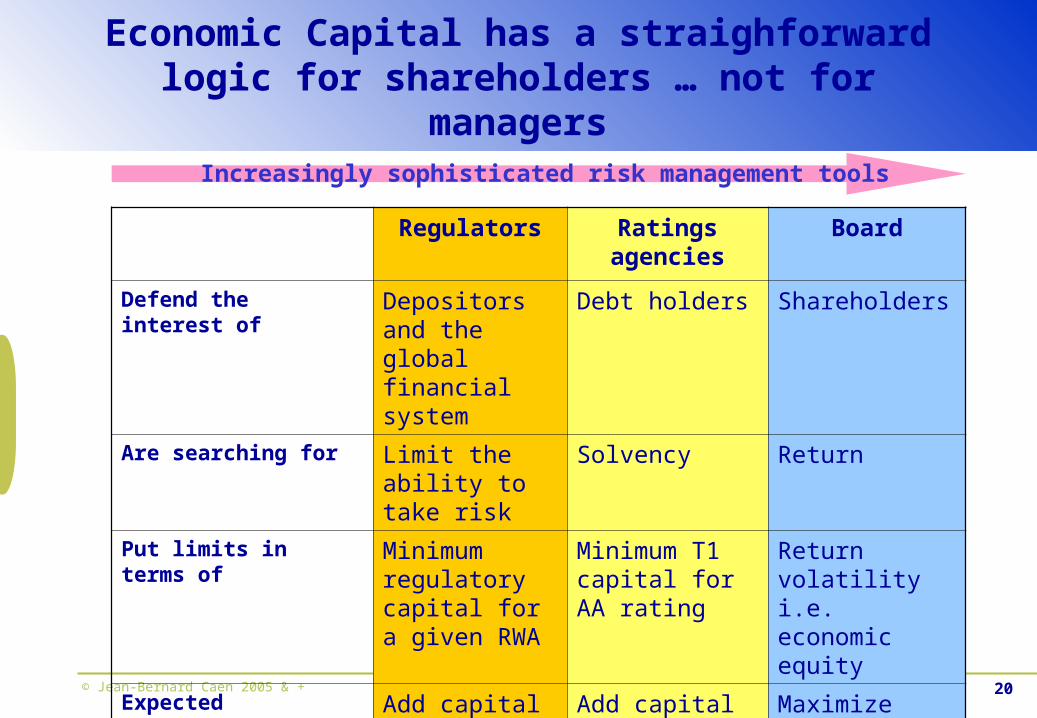

Economic Capital has a straighforward logic for shareholders … not for managers

Regulators Ratings agencies

Board

Defend the interest of Depositors and the global financial system

Debt holders Shareholders

Are searching for Limit the ability to take risk

Solvency Return

Put limits in terms of Minimum regulatory capital for a given RWA

Minimum T1 capital for AA rating

Return volatility i.e. economic equity

Expected management Add capital Add capital Maximize value creation

Increasingly sophisticated risk management tools

© Jean-Bernard Caen 2005 & + 21

Conclusion

A schopenhauer puts it:« ALL TRUTH GOES THROUGH THREE STEPS FIRST IT IS RIDICULED THEN IT IS OPPOSED TO FINALLY CONSIDER IT HAS ALWAYS BEEN OBVIOUS »

Do not consider resting when you reach the third step!• This is where it all begins…

Thank you for listening