$$ Entrepreneurial Finance, 5th Edition Adelman and Marks PRENTICE HALL ©2010 by Pearson Education,...

65

$$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ Entrepreneurial Finance, 5th Edition Adelman and Marks PRENTICE HALL ©2010 by Pearson Education, Inc. Upper Saddle River, NJ 11-1 Chapter 11 Personal Finance

-

Upload

suzanna-jacobs -

Category

Documents

-

view

219 -

download

4

Transcript of $$ Entrepreneurial Finance, 5th Edition Adelman and Marks PRENTICE HALL ©2010 by Pearson Education,...

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-1

Chapter 11

Personal Finance

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-2

Learning Objectives Understand the overall nature of risk as it pertains to both

individuals and businesses. Distinguish between speculative and pure risk. Identify the programs employed by individuals and

businesses in managing risk. Understand the role that insurance plays in the transfer of

risk. Understand the role of capital accumulation in achieving

financial success.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-3

Learning Objectives (continued)

Analyze and determine which investment vehicles to select in order to accumulate and preserve capital efficiently.

Understand the importance of retirement planning. Distinguish between the various retirement programs and

strategies available to the business owner and the individual.

Understand the importance that estate planning plays for the individual and business owner in the transfer of wealth.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-4

Risk

Risk is the uncertainty of future outcomes.› Speculative risk is that in which there is a possible gain or loss.

– Uninsurable› Pure risk involves only a chance of loss or experiencing a theft or

fire.

– Insurable

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-5

Risk Criteria for an Insurable Loss

Potential losses must be reasonably predictable. The loss must be accidental. The loss should be beyond the control of the insured. The loss should not be catastrophic to the insurance

company.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-6

Identification of Risk Exposure

Marketing risk Credit risk Loss of service due to death or disability of the owner Business interruption risk

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-7

Management of Risk

Risk management involves performing the management planning function in a manner that will reduce uncertainty. Methods include:› Risk reduction› Risk avoidance› Risk transfer› Risk assumption

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-8

Risk reduction includes programs that reduce risk. Examples are:› Sprinkler systems› Giving up smoking› Investing in government securities

Risk avoidance is avoiding any hazard which exposes the business to risk. An example is:› Cash-only sales policy

Management of Risk (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-9

Risk transfer is transferring risk to another party, usually a factor or insurance company.

Risk assumption occurs when you believe that the loss you might incur is less than the cost of risk avoidance or risk transfer.

Management of Risk (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-10

Types of Insurance

Life insurance is a method of transferring risk from the insured to the insurance company. Two basic types are:› Term insurance assumes that you pay the premium for pure life

insurance.› Permanent, or whole-life insurance allocates part of the

premium to building equity or cash value that can be used upon retirement or borrowed against in case of an emergency.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-11

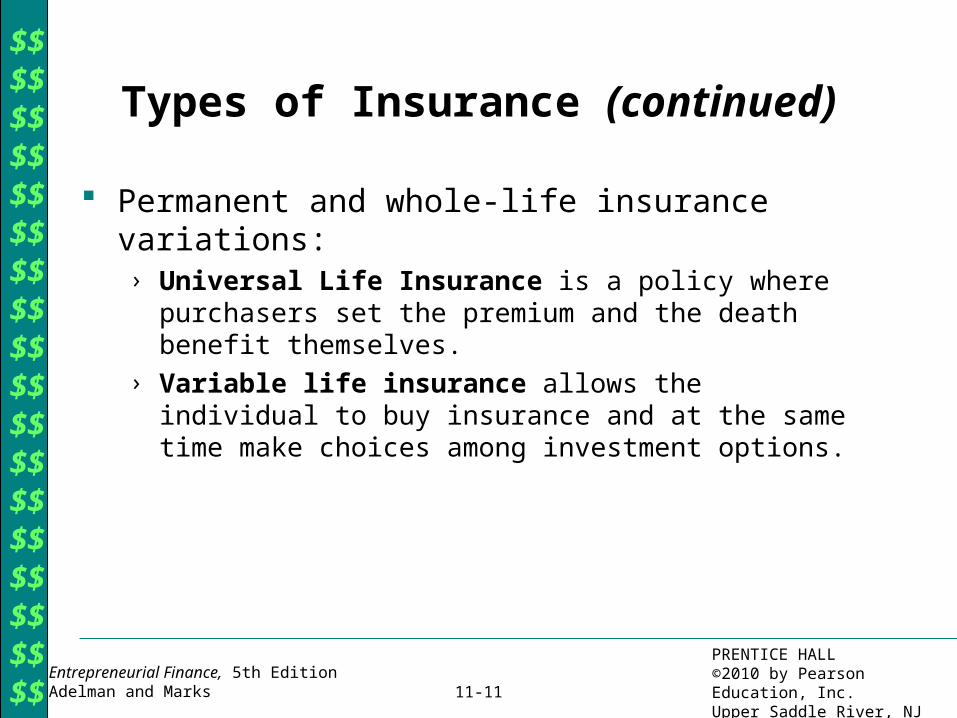

Permanent and whole-life insurance variations:› Universal Life Insurance is a policy where purchasers set the

premium and the death benefit themselves. › Variable life insurance allows the individual to buy insurance

and at the same time make choices among investment options.

Types of Insurance (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-12

› Health insurance is purchased to alleviate the cost of an illness or other health problem.

– Health Maintenance Organizations (HMO) use their doctors, specialists and hospitals.

– Preferred Provider Organizations (PPO) choice of doctors, hospitals, laboratories and medical facilities within PPO network.

– Medicare is federal health insurance.• All citizens 65 or older• Disability for at least 24 months

Types of Insurance (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-13

Medicare (continued)

Medicare has four distinct parts.› Part A covers most expenses and the hospital if medically

necessary. › Part B helps cover doctor services, outpatient care and other items

not covered in Part A. Requires monthly premium.› Part C consists of Medicare Supplemental insurance plans or

Medicare Advantage Plans that provide coverage not covered by Part A & B.

› Part D is federal government’s prescription drug program.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-14

Types of insurance (continued)

› Disability insurance is purchased to replace lost income when an employee is unable to do the job due to a physical or mental handicap.

› Long-term care insurance provides for all of the assistance one needs if one has a chronic illness or disability for an extended period of time.

› Liability insurance is used to transfer the risk of property damage and personal injury that might result from your business operation or individual actions.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-15

Financial Planning Goals

To achieve financial success in life, we must:› Establish goals that are realistic and obtainable› Begin with the acquisition stage of capital accumulation › Preserve capital by investing in vehicles that provide us a return

greater than the inflation rate› Consider individual tolerance for risk › Distribute capital through retirement income or estate transfer

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-16

Investments Investment vehicles are the specific financial instruments

that we use to generate growth and income. › Cash equivalents› Certificates of deposit› Bonds› Stock› Mutual funds› Real estate› Precious metals› Collectibles

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-17

Cash equivalents are liquid assets that are invested in savings accounts or brokerage money market accounts. › Money market consists of:

– Treasuries

– Banker’s acceptances

– Certificates of deposit

– Repurchase agreements

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-18

Certificates of deposit, or CDs, are promissory notes whereby a bank promises to pay the purchaser the principal amount plus interest after a stipulated period of time.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-19

Bonds are contractual agreements that are made between a borrower and a lender of financial capital.› U. S. Treasury bonds

– T-bills

– T-notes

– Federal bonds› Municipal bonds

– General revenue bonds

– General obligation bonds› Corporate bonds

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-20

U. S. Treasury bonds› T-bills (or treasury bills) are risk-free investments that mature in

less than one year, typically in three or six months.› T-notes are bonds that mature in 10 years or less, typically 10

years, 5 years and 2 years. › Federal bonds mature in periods that are greater than 10 years

and range up to 30 years.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-21

Municipal bonds are issued by a government agency other than the federal government.› General revenue bonds are issued to build specific projects for

the municipality that will use the income from the project to pay the bondholder.

› General obligation bonds are used to build projects that do not normally generate revenue such as public schools and roads.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-22

Corporate bonds are issued by a public corporation that wants to borrow money to invest in assets that will help it earn revenue. › Secured debt refers to the fact that the corporation pledges

specific assets to guarantee the bonds.› When the bond is not backed by secured debt, it is referred to as a

debenture.

– Debenture bondholders have a claim on the remaining assets of a company.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-23

Bond terminology:› Par value (face value or principal value) of the bond.

– Denomination of $1,000, paid to the bondholder at maturity (the due date of the bond).

› Coupon rate (quoted rate or stated rate) is the rate of interest that the issuer agrees to pay to the lender on an annual basis.

› Current market interest rate the prevailing rate in the market on the date we decide to sell the bond.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-24

Bond terminology (continued):› Premium: Bonds that are sold at a value above par ($1,000)› Discount: Bonds that are sold at a value below par ($1,000)› Junk bond (high-income yielding): A corporate bond having a

rating of ‘B’ or less (this bond by definition is a high-risk investment)

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-25

Bond valuation:› Using current interest rates, find the present value of the bond’s

interest payments paid over the remaining life of the bond.› Using current interest rates, find the present value of the $1,000

maturity value (par) of the bond.› Add the two together to get the price of the bond.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-26

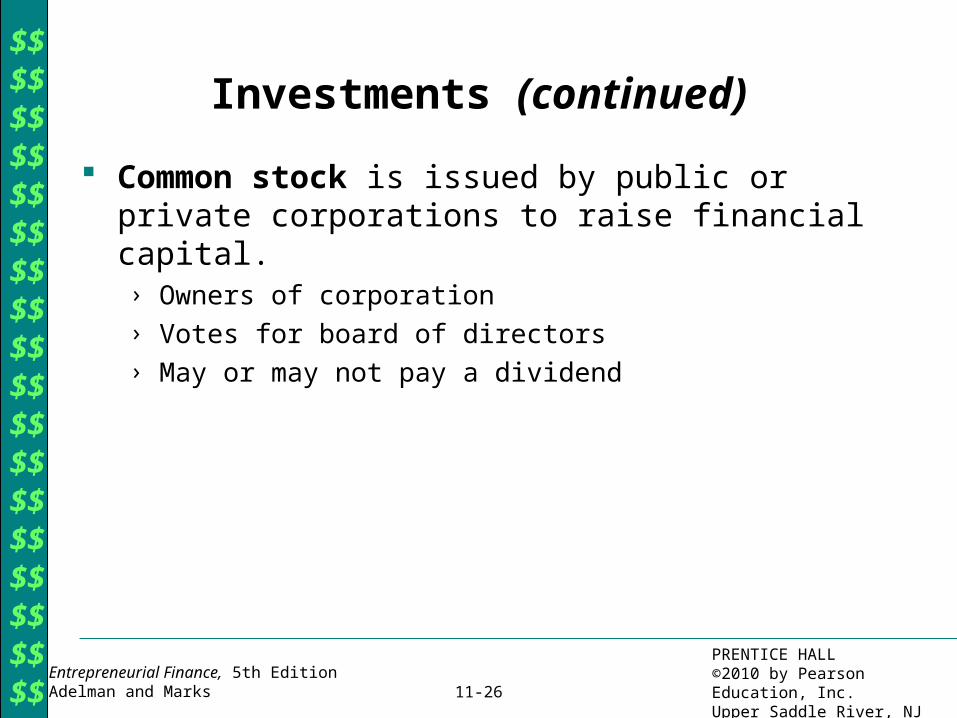

Common stock is issued by public or private corporations to raise financial capital. › Owners of corporation› Votes for board of directors› May or may not pay a dividend

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-27

Stock terminology:› Par value is an arbitrary dollar amount that is used for accounting

purposes to determine the number of shares of stock that have been sold by the corporation.

› The book value of the stock is the total stockholder’s equity that is carried on the corporate balance sheet. Contains three factors:

– Stock at par

– Additional paid-in capital

– Retained earnings

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-28

Stock terminology (continued):

Investments (continued)

goutstandinstock common of shares ofNumber

equity sr'stockholdecommon Totalstockcommon of shareper Book value

Book value per share:

Market value is the price at which the owners of current shares are buying and selling the stock at the time that a share is actually traded.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-29

Factors affecting market value of a share of stock:› Supply and demand for shares› Actual earnings and anticipation of earnings› Book value of stock and number of shares outstanding› General economic conditions

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-30

Preferred stock is issued by a corporation to raise financial capital but it occupies an intermediate position between common stock and bonds.› Quasi-owners of corporation› No voting rights› Guaranteed a specific return on investment if corporation pays a

dividend

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-31

› Types of preferred stock:

– Cumulative preferred stock has the following important feature:

• When the corporation decides to pay a dividend, the preferred stockholder will receive back dividends, or dividends in arrears.

– Convertible preferred stock is preferred stock that may be exchanged for shares of common stock.

– Callable preferred stock is preferred stock that can be called back by the company at some specified price.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-32

Stock terminology (continued):› Dividend is a payment made by the corporation to each

shareholder of a class of stock.› Dividends are paid on a per-share basis.› Preferred stock dividends are paid first, the remainder is paid to

common shareholders.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-33

Company has 1 million shares of common and 10,000 shares of $100, 7% preferred stock, and declares a $1 million dollar dividend.

Investments (continued)

stockcommon of shareper 93.0$000,000,1

000,930$ shareper dividendstock Common

goutstandinstock common of shares ofnumber Total

dividendstock common Total shareper dividendstock Common

$930,000 dividendstock common Total

$70,000-$1,000,000dividendstock common Total

shares) preferred 0($7)(10,00 - $1,000,000 dividendstock common Total

dividend preferred Total - dividend Total dividendstock common Total

dividendstock common Total dividend preferred Total dividend Total

shares

Dividends are calculated as follows:

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-34

Mutual funds are companies that are involved in collecting the funds of investors and using these funds to purchase large blocks of stocks, bonds, or other investment vehicles. › Each fund is established with a specific goal and risk objective.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-35

Investments (continued)

Types of mutual funds:› Growth funds invest primarily in common stock of publicly held

corporations and have capital appreciation as their objective. › Income funds specialize in corporate and government bonds. › Growth and income funds, or balanced funds, invest in both

stocks and bonds.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-36

Types of mutual funds (continued):› A mutual fund family is an investment group that may have

mutual fund portfolios in all of the preceding categories.

– No-load funds do not charge commissions on the amount invested.

– Load funds charge a commission on the initial investment, but have no sales charges when you sell the shares.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-37

Types of mutual funds (continued):› Global and international funds are funds that invest in stocks

and bonds of companies primarily outside of the United States. › Money market funds primarily invest in short-term, highly liquid

investments such as CDs, short-term government treasuries, commercial paper, repurchase agreements, and banker’s acceptances.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-38

Investments (continued)

Types of mutual funds (continued):› Real estate is an investment in land and buildings.

– Owner-occupied residential real estate is any kind of building in which people live.

• It is limited by law to your primary residence and one additional vacation home.

– Non-owner–occupied residential real estate is property that can be leased by the owner to the tenant for the purpose of generating income.

• Property may be in the form of houses, apartments, motels, or hotels.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-39

Real estate:› Commercial real estate is both land and improved property that

is used by the owner to generate income.

– Examples are commercial office buildings, shopping centers, factories, and warehouses.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-40

Real estate (continued):› Real estate investment trusts (REITs) provide the investor with

the opportunity to participate in the commercial and nonresidential real estate market.

– A REIT is a pooling of individual investor funds, much like a mutual fund.

Investments (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-41

Investments (continued)

Precious metals fall into the area of commodity trading. › They are primarily gold, silver, and platinum.› Considered to be hedges against inflation.

Collectibles are items that become valuable or appreciate with time because of their scarcity. › Examples include coins, paintings, sculptures, antiques, stamps,

and even baseball cards and comic books.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-42

Investments (continued)

Short-Term Investment Strategies include:› Buying stock on margin› Selling short› Option trading

Long-Term Investment Strategies include:› Buy and hold› Dollar cost averaging

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-43

Pension Planning Pension planning consists of making plans to guarantee a

system of conserving future income for the time when you choose to retire or are forced into retirement due to circumstances beyond your control.› Three main sources of retirement income

– Social Security

– Employee Sponsored Retirement Plans

– Personal savings

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-44

Pension Planning (continued)

Types of retirement plans:› Contribution-oriented plans provide benefits to the retiree based

on the account balance that has been accumulated during the working life of the pensioner.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-45

› Benefit-oriented plans provide a defined benefit to the retiree at retirement, which is generally a percentage of the compensation paid to the employee during the last several years of employment and the total term of employment. An example would be military retirement pay.

› Combined plans are retirement plans designed by individuals or employers.

– Deferment of salaries into a retirement plan

– Employer contributions into a retirement plan

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-46

Individual retirement accounts, or IRAs, are plans that allow us to contribute current annual income into retirement accounts. › Deductible IRAs› Non-deductible IRAs› Roth IRAs› Educational IRAs

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-47

Pension Planning (continued) IRAs (continued):

Deductible IRAs are those in which you can contribute pretax dollars up to an amount specified by current law.

Nondeductible IRAs allow you to contribute the same amounts as do deductible IRAs, but the contribution is after-tax dollars.

For both of the above, returns accumulate tax-free until withdrawn.

YearsMaximum Annual Contribution

Maximum Annual

Contribution Age 50 and

older2002-2004 3,000$ 3,500$ 2005-2007 4,000$ 5,000$ 2008 5,000$ 6,000$ 2009-2010 $5,000 indexed $6,000 indexedS o u r c e : IRS Publication 3998 (Rev. 2004)

Table 11-2 IRA Contribution Limits

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-48

IRAs (continued):› Roth IRAs will allow you to contribute up to $5,000 of after-tax

dollars by 2008 as shown in Table 11-2.

– If the funds are held in the account for at least five years, there are no taxes due.

– Your original contributions can be withdrawn tax-free at any time.

– Can roll a current IRA into a Roth IRA provided you pay tax on current IRA.

– Can withdraw $10,000 tax-free and penalty-free to purchase first home if IRA is more than 5 years old.

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-49

IRAs (continued):› Roth IRAs (continued):

– Does not have age limit with regard to mandatory withdrawal.• Traditional IRAs have an age 70 1/2 mandatory

withdrawal age limit.

– All gains are tax-free forever.

– Roth IRAs can be passed on to heirs tax-free.

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-50

Coverdell Education Savings Account (Educational IRAs) allow for an non-deductible contribution of up to $2,000 for any child under the age of 18. › Income accumulates tax-free and remains tax-free as long as it is

used for the child’s higher educational expenses. › Funds must be used before the student is 30.

› The account can be transferred between family members.

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-51

Pension Planning (continued) Section 529 plans include both prepaid tuition and savings

plans.› Funds in both prepaid and savings plans grow tax-free.› Contribution limit depends on plan and vary from state to state

($100,000 to $305,000).› Withdrawals are tax-free if used for qualified expenses:

– Tuition, fees, and room and board at qualified higher educational institutions.

› Accounts can be assigned to any family members including cousins.

› Penalty to non-qualified withdrawals is that withdrawal is taxed as ordinary income and there is a 10 percent penalty.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-52

Simplified Employee Pension (SEP) Plans are pension plans that are funded by employers.› Employer-established› All employees must agree› Common for self-employed› Contributions can be up to the lesser of $46,000 or 25 percent of

the participants’ compensation.

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-53

Pension Planning (continued)

SIMPLE plan. SIMPLE (Savings Incentive Match Plan for Employees) is a pension plan established by an employer who has fewer than 100 employees. Current legislation defines contribution limits as shown below:› Match employee contribution dollar for dollar to 3 percent of

salary.› Maximum:

– $10,500 for 2007 & 2008

– If age 50+ $12,500

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-54

Tax-sheltered annuities (TSAs 403b plans) are plans that allow employees of not-for-profit organizations (churches, public schools, charitable organizations, etc.) to establish a retirement fund that is purchased and approved by the employer.

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-55

Keogh plans are for self-employed individuals in sole proprietorships, partnerships, and LLCs. › Contribute up to the lesser of 100% of earned income or $46,000

for 2008.› Maximum deductible contribution is up to 25% of compensation.› Define both contribution and benefit amounts derived from the

account.› $185,000 limit on annual retirement benefit for 2008.

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-56

Profit-sharing plans are established by employers who have determined that a portion of each dollar in profit will be allocated to the employees of the company.› Annual contributions to these plans vary drastically because

profits fluctuate due to economic, industry, and specific company health.

› Never stand alone but are incorporated into other types of retirement plans.

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-57

401k plans are retirement plans established to accept employee contributions. › Based on salary reduction› Employer may match a portion of employee contribution on some

basis› Allows for pretax contributions up to $15,000 per year. $20,000

for individuals 50 and above.› Cannot favor highly compensated employees

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-58

SIMPLE 401k is a modification of the 401k plan

› Limited to firms with fewer than 100 employees› Employee contribution limited to $15,000 per year, $20,000 if age

50 or older.› Employer can contribute up to 3% of worker’s compensation› Plan has to be the only plan the business offers› Employers are spared from discrimination testing

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-59

Pension Planning (continued)

Roth 401k plan.› Must be established by an employer.› Grows tax-free.› Uses after-tax money.› Max contribution is $15,000 in 2006 and $20,000 if age 50 or

older.› All funds passed on the beneficiaries tax-free.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-60

Money purchase plans are defined contribution plans that are established by the employer to contribute a fixed percentage of payroll into a retirement fund for the employees. › Maximum contribution is 25% of payroll› Employee does not contribute› Employer must contribute even if company makes no profit

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-61

Stock bonus plans are similar to profit-sharing plans, except that the employer contributes shares of stock, rather than money, into the retirement account.› Employer gets a deduction for the value of the stock.› Contribution is pre-tax dollars.

Pension Planning (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-62

Retirement Strategies

Establish a goal, or minimum, income level that you desire when you retire.

Do not wait until you believe you can afford to start a retirement account.

Plan for capital preservation and continued growth. Invest in instruments that provide you with a degree of risk

that is comfortable to you.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-63

Try to invest the maximum amount, but never less than the amount that the employer uses to calculate profit-sharing or matching contributions.

Consider opening a Roth IRA even if you have an employer-sponsored plan.

Retirement Strategies (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-64

Estate Planning

Estate planning a method of planning for use, conservation, and transfer of wealth as efficiently as possible.› Wills are written documents that provide direction to others as to how

you want your wishes carried out after death.› Probate is a legal court process that addresses and focuses in on the will

and the probate estate.

– Removing items from probate:

1. Joint Ownership with right of survival (temporary removal) NOTE: The author recommend that children should not normally be part of Joint ownership with right of survival.

2. Trusts (permanent removal)

3. Gifts – reducing the value of the estate.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

PRENTICE HALL©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

11-65

Trusts are legal arrangements that actually divide legal and beneficial interests among two or more people.

– When a trust is set up during the life of the trustor, it is referred to as a living trust.

– When a trust is established at death, it is referred to as a testamentary trust.

– A revocable trust is one in which the trustor has the right to cancel the trust during his or her lifetime.

– An irrevocable trust is one that is unalterable during a person’s lifetime.

Estate Planning (continued)