© Corporate Renaissance Group 1 Using costing of services to improve performance-oriented budgeting...

30

© Corporate Renaissance Group 1 Using costing of services to improve performance-oriented budgeting By Jim McCrindell and Vijay Jog

-

Upload

juniper-patrick -

Category

Documents

-

view

215 -

download

0

Transcript of © Corporate Renaissance Group 1 Using costing of services to improve performance-oriented budgeting...

© Corporate Renaissance Group1

Using costing of services to improve performance-oriented budgeting

By

Jim McCrindell and Vijay Jog

Using costing of services to improve performance-oriented budgeting

By

Jim McCrindell and Vijay Jog

© Corporate Renaissance Group2

CopyrightCopyright

Corporate Renaissance Groupwww.crgroup.com

613-232-4295All rights reserved.

This document may not, in whole or in part, be copied, photocopied, reproduced, translated, or reduced to any electronic medium or machine-readable form without prior consent in writing from Corporate Renaissance Group. We are grateful for the use of some copyrighted material from our strategic partner - Cost Technology Inc.

© Corporate Renaissance Group3

Let us start with an exampleLet us start with an example

• We have secured funding for a project to improve overall health of children in a designated area by providing health services

• We are interested in ensuring that the funding is making an impact and with right financial controls

© Corporate Renaissance Group4

Management Information Management Information

Health services$500,000

Health services$500,000

• Goal/objective: Improve the health of the local population by reducing incidents of disease

• Budget/spending authority: • $500,000 for wages and material• Measurement/control: money went to

health related service for wages and material

• Report card: money was correctly spentDisease levels hard to quantify

© Corporate Renaissance Group5

We have management informationWe have management information

• It can be audited and reported• Financial control system needs are met

But not sufficient for some important management questions?

What did we get from the $500,000 budget?

© Corporate Renaissance Group6

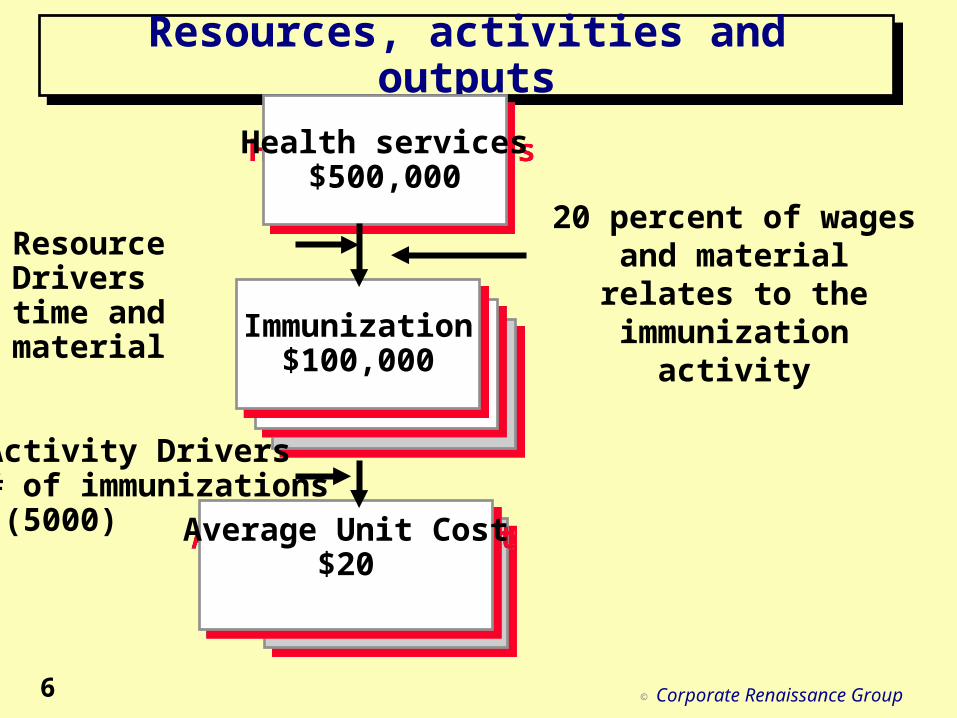

Resources, activities and outputsResources, activities and outputs

Health services$500,000

Health services$500,000

Immunization$100,000

Immunization$100,000

Resource Drivers time and material

Activity Drivers# of immunizations (5000) Average Unit Cost

$20Average Unit Cost

$20

20 percent of wages and material relates to

the immunization activity

© Corporate Renaissance Group7

Now we have better informationNow we have better information

• how much efforts went in immunization? (Activity)

• what was the cost of the activity “immunization”? (Activity cost)

• How many immunizations were done? (output)• what was the cost per immunization?

(efficiency)• How to use this information for work load

management, linking to objectives, bench marking, decision making?

Qu: can we know more?

© Corporate Renaissance Group8

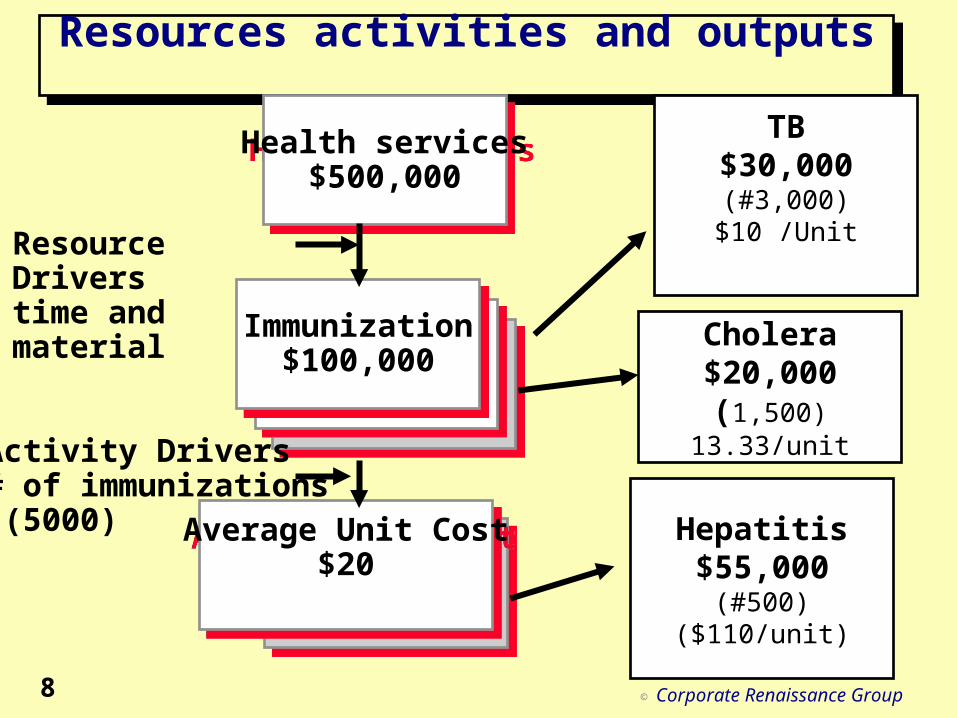

Resources activities and outputs Resources activities and outputs

Health services$500,000

Health services$500,000

Immunization$100,000

Immunization$100,000

Resource Drivers time and material

Activity Drivers# of immunizations (5000) Average Unit Cost

$20Average Unit Cost

$20

TB$30,000(#3,000)$10 /Unit

Cholera$20,000(1,500)

13.33/unit

Hepatitis$55,000

(#500)($110/unit)

© Corporate Renaissance Group9

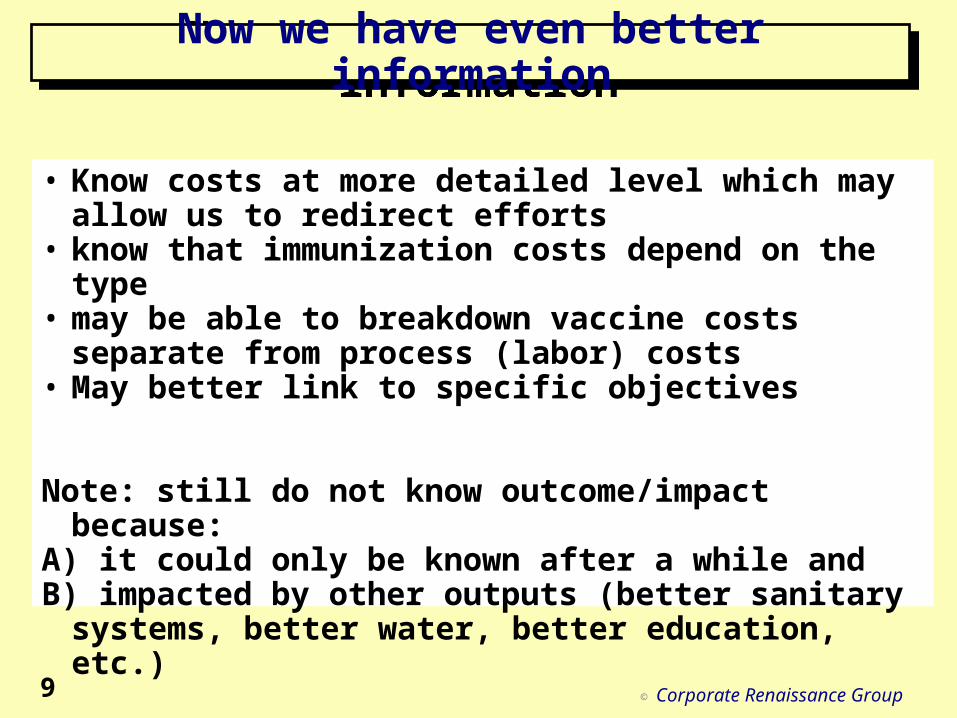

Now we have even better informationNow we have even better information

• Know costs at more detailed level which may allow us to redirect efforts

• know that immunization costs depend on the type • may be able to breakdown vaccine costs separate from

process (labor) costs• May better link to specific objectives

Note: still do not know outcome/impact because:A) it could only be known after a while andB) impacted by other outputs (better sanitary systems,

better water, better education, etc.)

© Corporate Renaissance Group10

What more we would like to know?What more we would like to know?

Percentage of children immunized how much time it takes to get immunized (waiting list and

time)Quality of immunization service (?????)

© Corporate Renaissance Group11

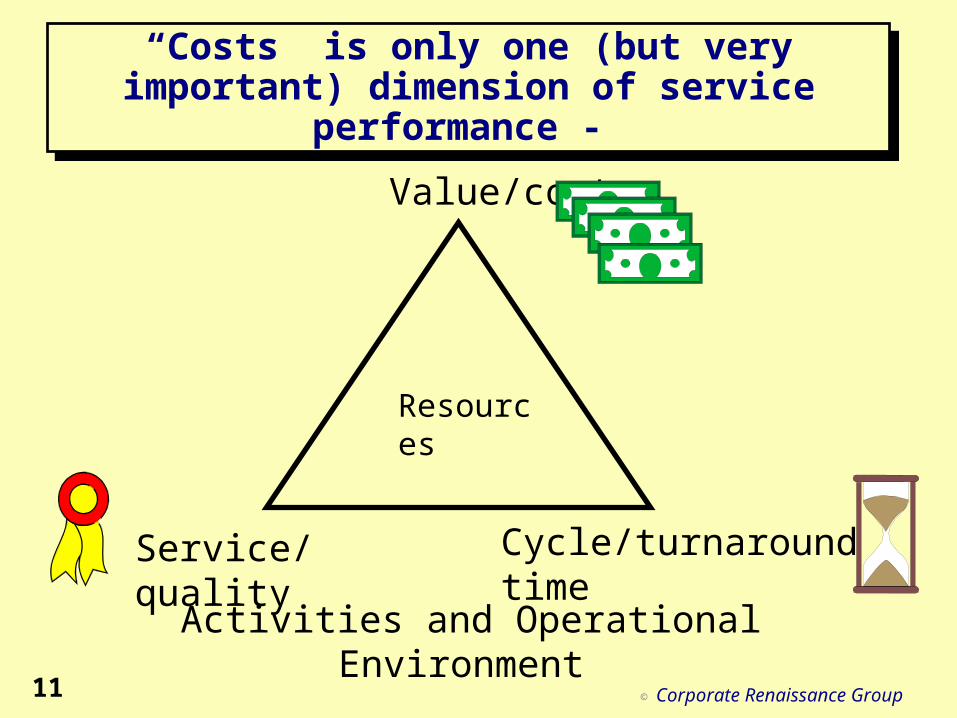

“Costs” is only one (but very important) dimension of service performance -

“Costs” is only one (but very important) dimension of service performance -

Value/cost

Service/quality Cycle/turnaround time

Resources

Activities and Operational Environment

© Corporate Renaissance Group12

From example to concepts From example to concepts

© Corporate Renaissance Group13

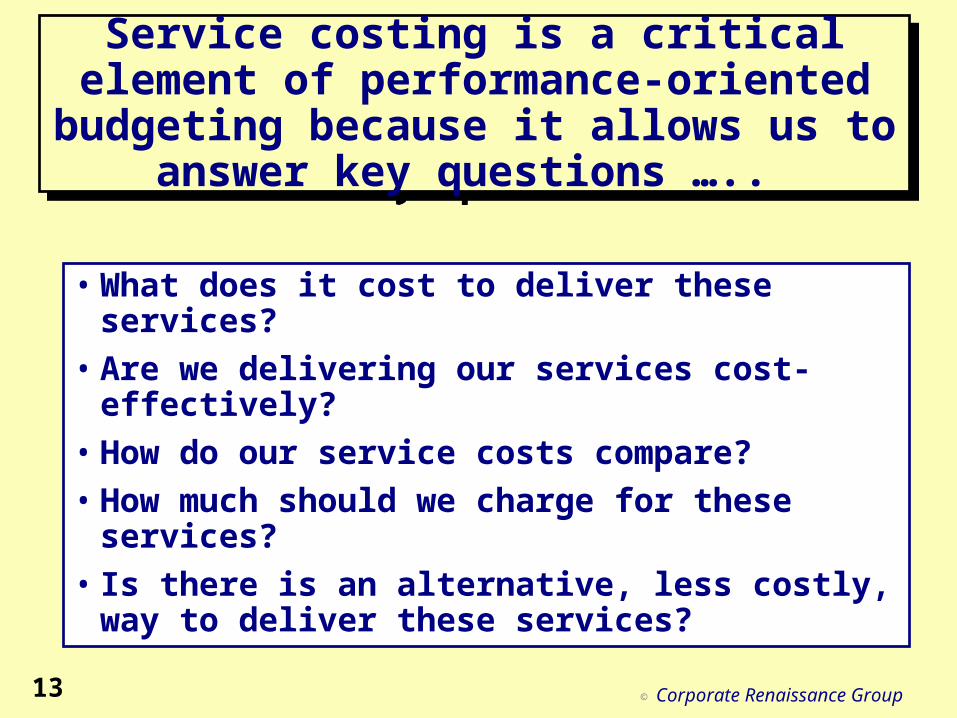

Service costing is a critical element of performance-oriented budgeting because it allows us to answer key questions …..

Service costing is a critical element of performance-oriented budgeting because it allows us to answer key questions …..

• What does it cost to deliver these services?

• Are we delivering our services cost-effectively?

• How do our service costs compare?

• How much should we charge for these services?

• Is there is an alternative, less costly, way to deliver these services?

© Corporate Renaissance Group14

Hence: Activity-Based Costing (ABC)Hence: Activity-Based Costing (ABC)

The basic assumption of ABC is very simple.

ABC assumes that services create need for outputs which create the demand for activities which, in turn, consume resources.

By tracing costs to services/outputs according to the activities required to provide them, ABC provides a more accurate picture of costs and performance.

© Corporate Renaissance Group15

The ABC Cross

RESOURCES

$ used to do work

RESOURCES

$ used to do work

Objects of Work(or outcomes)

To what, or for whom,work is done

Objects of Work(or outcomes)

To what, or for whom,work is done

Resource Drivers

Activity Drivers

The ProcessView or ABM

Performance MeasuresHow well the work

is done?CostTime

Quality

Performance MeasuresHow well the work

is done?CostTime

Quality

Activities

Work

Activities

Work

Cost Drivers

Why work is done

Cost Drivers

Why work is done

The Cost AssignmentView or ABCFinancial

system

© Corporate Renaissance Group16

Knowledge of Costs enhances accountabilityKnowledge of Costs enhances accountability

CostingCosting of of ServicesServices

© Corporate Renaissance Group17

ABC provides a multi-dimensional cost view of the organization

ABC provides a multi-dimensional cost view of the organization

Organization•Departments•Branches•Divisions•Regions Resources

•Salaries•Supplies•Travel•Depr.•etc.

Activities•Processing claims•Paying pensions•Teaching•Nursing•Maintaining buildings•etc

Activity Costs and Activity Based costs of services

© Corporate Renaissance Group18

xxxxx xxxxx xxxxxxxxxx xxxxx xxxxxxxxxx xxxxx xxxxxxxxxx xxxxx xxxxxxxxxx xxxxx xxxxxxxxxx xxxxx xxxxxxxxxx xxxxx xxxxx

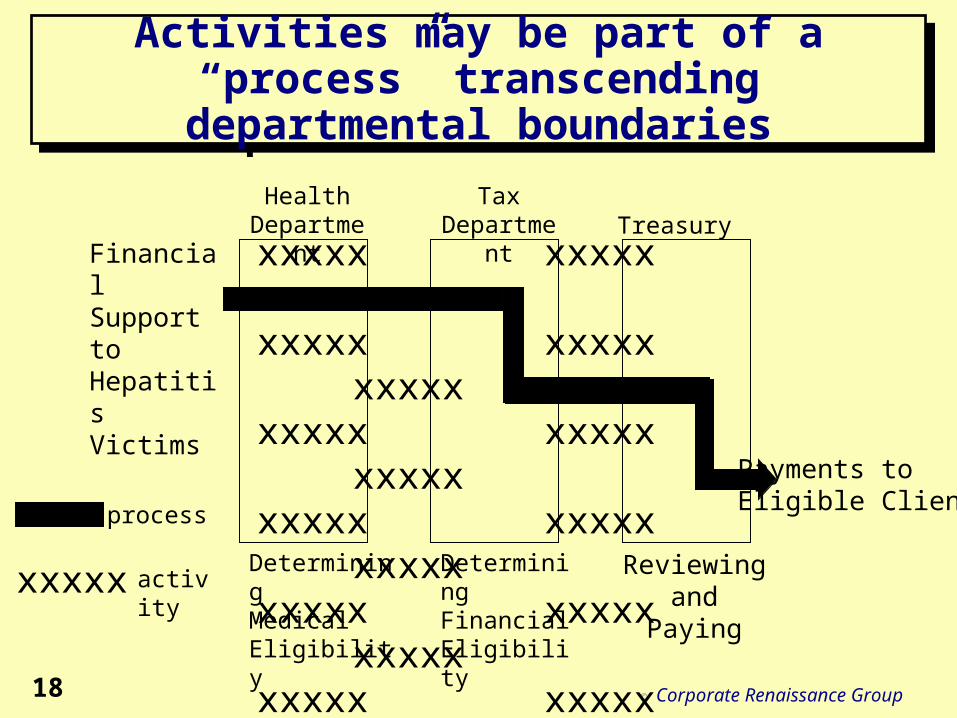

Activities may be part of a “process” transcending departmental boundariesActivities may be part of a “process”

transcending departmental boundaries

HealthDepartment

TaxDepartment Treasury

Payments toEligible Clients

xxxxx

process

activity

Financial Support to Hepatitis Victims

DeterminingMedical Eligibility

DeterminingFinancialEligibility

Reviewingand Paying

© Corporate Renaissance Group19

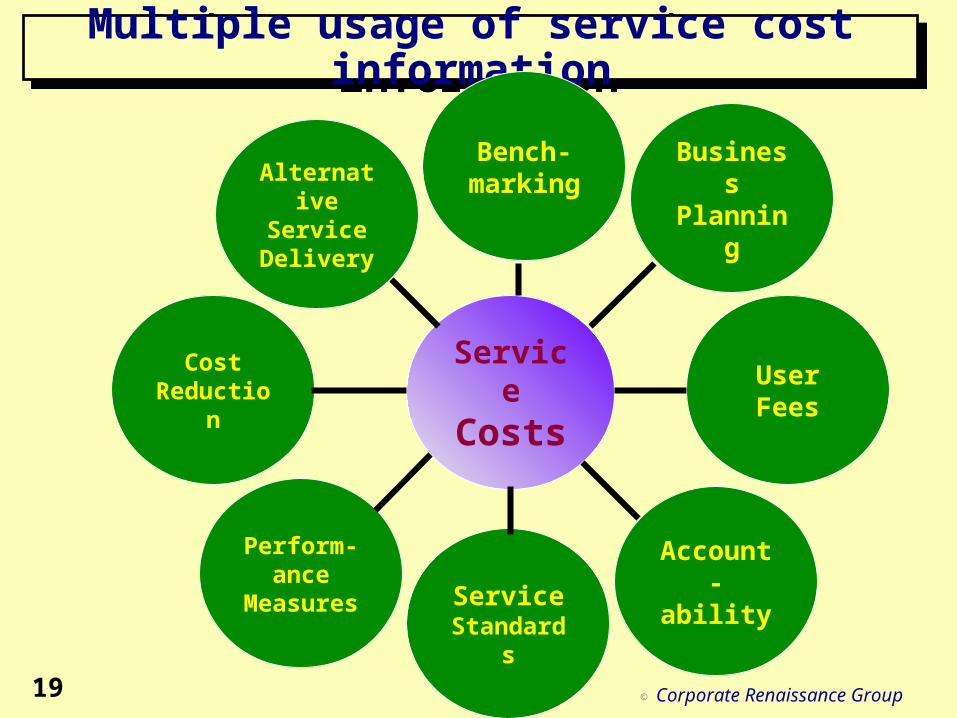

Multiple usage of service cost informationMultiple usage of service cost information

ServiceCosts

UserFees

Account-ability

Perform-ance

Measures ServiceStandards

CostReduction

Bench-marking Business

PlanningAlternative

ServiceDelivery

© Corporate Renaissance Group20

Dealing with Direct Payments and Transfers

Dealing with Direct Payments and Transfers

• Some government service costs consist mainly of direct payments to persons and organizations, e.g.,

–pensions

–grants and contributions

• Activity costs relate to the cost of administering such services.

• Thus, the total cost of the services provided can be identified along with the efficiency of providing the services (e.g., cost of processing pension payments per dollar of pension payment or per cheque)

© Corporate Renaissance Group21

From concepts to implementation …. From concepts to implementation ….

• Implementing of ABC and ABM requires a different approach to resource allocation, management reporting, financial system design/usage and incentive/promotion systems.

© Corporate Renaissance Group22

Note …. Note ….

• Traditional financial systems are mainly tracking systems - they only tell us how much was spent by line item (salaries, benefits, travel, etc.) and organization but not: what was done with these resources?

• In these systems, variance from budget drives performance evaluation rather than what was done with the resources given

• Performance measures on quality, delivery time as well as on satisfaction and effectiveness are typically not available or not an integral part of the budgeting process

© Corporate Renaissance Group23

The Big Picture The Big Picture

© Corporate Renaissance Group24

Implementing an ABC System...Implementing an ABC System...

Identify objectives, and organizational structure, resources, products and services

Identify activitieswithin each cost/Responsibility centre

Integrate with existing financial and operational systems

Build ABC model

Process for Continuous Improvement and Refocus

Post-implementation

challenges

Senior management

buy in

Story boarding

Systems experience

ABC software

Process experience

© Corporate Renaissance Group25

ABC implementations do not require sophisticated systems architecture and

networks

ABC implementations do not require sophisticated systems architecture and

networks

• If the organization has a G/L (line item reporting), then implementing of ABC and PM systems is not very costly or time consuming after the initial activity and service maps

• Activity (process) and non-financial performance data be developed through consultation with relevant managers and employees (often exists informally).

• In initial development minimize numbers of activities/indicators (significant ones)

© Corporate Renaissance Group26

Premises/solutions (continued)Premises/solutions (continued)

• ABC systems are periodic - they are not transactional. Thus, Off-line ABC systems are better. ABC systems also require operational data on outputs

• In the absence of these systems, organizations do not have the basic information on their performance

© Corporate Renaissance Group27

Incorporating ABC/PM into a Performance-oriented budgeting

system

Incorporating ABC/PM into a Performance-oriented budgeting

system

• Link financial system to ABC and Performance Measurement Systems and then allocate/manage budgets

FinancialSystem

(ResourceInfo.)

ABCResources

to Activities to outputs

PM

Organization-wide

Performance Measures

Budget

Planning and Resource Management

© Corporate Renaissance Group28

FinancialSystem

Cost centre Costs

Activity Costs

Unit costs

Performance measures

ABC Costs to cost object

•ABC modelling•Activity mapping

Operational systems

ABC System

The PM System

© Corporate Renaissance Group29

Success criteria for Implementing Costing and Performance Measurement

Systems

Success criteria for Implementing Costing and Performance Measurement

Systems

• Political and Senior Bureaucrat Support

• Reflected in organizational vision and “values”

• Embedded in planning, decision-making, reporting and incentive systems

• Seen as strategic and tactical “management” tools

• Driven by need for improved performance measurement and accountability

• Ready to accept approximately right rather than precisely wrong information

© Corporate Renaissance Group30

Questions and AnswersQuestions and Answers