© Baker Tilly Virchow Krause, LLP Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an...

34

© Baker Tilly Virchow Krause, LLP Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. The Government Contracting Environment: Emerging Issues, Enforcement Trends, and Latest News Presented by: Bill Bressette, Principal Baker Tilly’s Government Contractor Advisory Services September 19, 2014

-

Upload

egbert-carroll -

Category

Documents

-

view

227 -

download

2

Transcript of © Baker Tilly Virchow Krause, LLP Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an...

© Baker Tilly Virchow Krause, LLPBaker Tilly refers to Baker Tilly Virchow Krause, LLP,

an independently owned and managed member of Baker Tilly International.

The Government Contracting Environment: Emerging Issues, Enforcement Trends, and

Latest News

Presented by:Bill Bressette, Principal

Baker Tilly’s Government Contractor Advisory Services

September 19, 2014

• Government Contracting Environment Environment, Budgets and Sequestration

Shifting Priorities and Procurement Trends

Impact to Contractors

Competition and Pricing

• Compliance and Enforcement Trends Environment

Regulatory Changes

Enforcement Activity

• Looking Ahead Thoughts for new and established

contractors

2

Agenda

Government Contracting Environment

3

General Environment

“I guess the question I'm asked the most often is: "When you were sitting in that capsule listening to the count-down, how did you feel?" Well, the

answer to that one is easy. I felt exactly how you would feel if you were getting ready to launch and knew you were sitting on top of two million parts -- all built by the lowest bidder on a government

contract.”

~ John Glenn

4

General Environment

Current Trends• Continued debate over government spending in general

• Concerns over size of debt and fiscal deficit

• Budget cuts and sequestration

• Wars winding down / focus is turning inward

• Contractors pressured to do more with less

• Competition over price pressure and not overall value (LPTA)

• High scrutiny on compliance related issues

5

Shrinking Budgets

6

2009 2010 2011 2012 20133.00

3.20

3.40

3.60

3.80

4.00

4.20

Total Budget Authority (in Trillions)

Government Fiscal Year

Shrinking Budgets

Budget Authority: Top 10 Contracting Agencies (in Millions)

7

Department/Unit FY2012 FY2013 Increase / Decrease

Department of Health and Human Services $ 874,458 $ 873,330 ↓Department of Defense 655,397 585,239 ↓Department of the Treasury 442,633 440,900 ↓Department of Veterans Affairs 124,030 135,984 ↑Department of Homeland Security 45,911 61,873 ↑Department of State 30,122 29,584 ↓Department of Justice 31,412 28,106 ↓Department of Energy 22,721 21,160 ↓NASA 17,773 16,868 ↓General Services Administration -977 -1,255 ↓

Defense Spending

• Defense spending projected to return to near pre-2001 levels

8

Sequestration

• Sequestration came into effect resulting from a compromise in the Budget Control Act of 2011

• Congress needed to produce a deficit reduction bill with at least $1.2 trillion in cuts by 2021 to raise the debt ceiling by the same amount

• Congress failed to put a plan in place, triggering across-the-board cuts called sequestrations

9

Annual and Cumulative Spending Cuts Under $1.2

Trillion BCA Sequester

Medicare

Other Mandatory

Defense Discretionary

Domestic Discretionary

Interest

2013 2014 2015 2016 2017 2018 2019 2020 2021

-$50B

-$100B

-$150B

$0B

OMB Advice

The Office of Management and Budget recommended that agencies:

• Consider de-scoping or terminating for convenience contracts that are no longer affordable

• Enter into new contracts or exercise options when they support high-priority initiatives or where failure to enter into the contract would expose the government to significantly greater costs in the future

• Utilize parts of contracts that allow for flexibility or any kind of termination

• Prioritize funds based on importance and long-term considerations

10

Sequestration

The Future of Sequestration• The 2014 Midterm Elections are being / will be watched closely by

government contractors

• Republicans taking control of the senate will give them the ability to pass a “clean” debt-ceiling bill in March of 2015

- Will likely include additional cuts to government spending

• Even with the sequester in effect, congress appropriated discretionary spending budgets will continue to increase

• This trend may reverse as mandatory spending on entitlement programs such as Social Security and Medicare continue to outpace discretionary spending

11

William Bressette

Clarify

Shifting Priorities

Information Technology• Traditional IT services are fading; movement towards the cloud

Homeland Security• Growth in areas that support protection against biological, nuclear and terrorist

threats

Cybersecurity• Focus on improving cybersecurity defense and readiness (e.g., protecting the

U.S. electrical grid)

R&D• Renewed focus on the United States as a global hub of innovation

Infrastructure• Investment in the aging infrastructure including roads, bridges, tunnels, and

airports

12

Procurement Trends

13

Department of the Treasury

Department of Justice

Department of State

GSA

Homeland Security

NASA

Veterans Affairs

Health and Human Services

Department of Energy

Department of Defense

0.0 50.0 100.0 150.0 200.0 250.0 300.0 350.0

6.9

7.1

7.3

8.5

12.7

15.6

18.2

19.9

23.9

308.0

2013 Contract Obligations (in billions)Top 10 Contracting Agencies

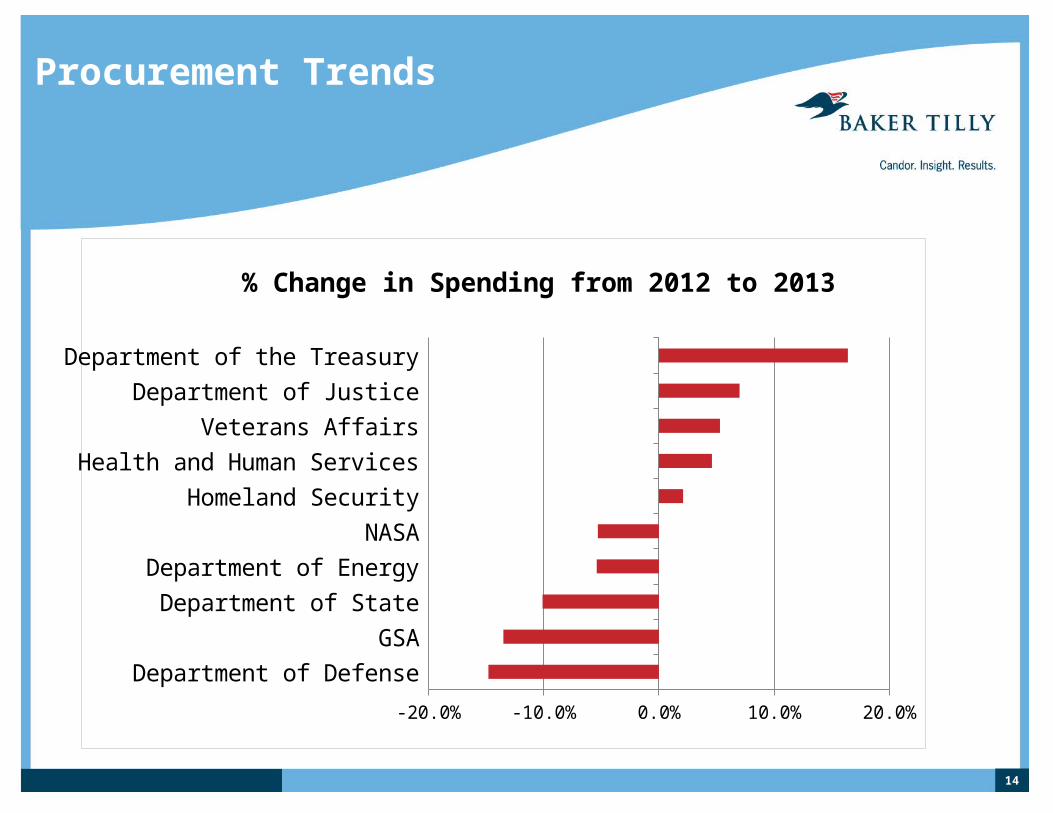

Procurement Trends

14

Department of Defense

GSA

Department of State

Department of Energy

NASA

Homeland Security

Health and Human Services

Veterans Affairs

Department of Justice

Department of the Treasury

-20.0% -10.0% 0.0% 10.0% 20.0%

% Change in Spending from 2012 to 2013

Procurement Trends

15

Category 2012 2013 % ChangeCarriers 82.6 75.3 -9%Knowledge Based Services 72.7 68.7 -6%Facility Related Services 63.0 60.8 -3%Technology 64.5 60.3 -7%Research & Development 50.7 43.8 -14%Medical Services & Supplies 33.1 33.1 0%Logistics & Equipment Services 31.8 27.0 -15%Transportation Services & Fuel 34.0 25.1 -26%Other 27.5 22.4 -19%Construction Services 23.9 18.4 -23%Weapons and Ammunition 18.4 18.2 -1%Food 11.8 6.7 -43%Drones 2.2 2.3 5%

Spending by Category (in billions)

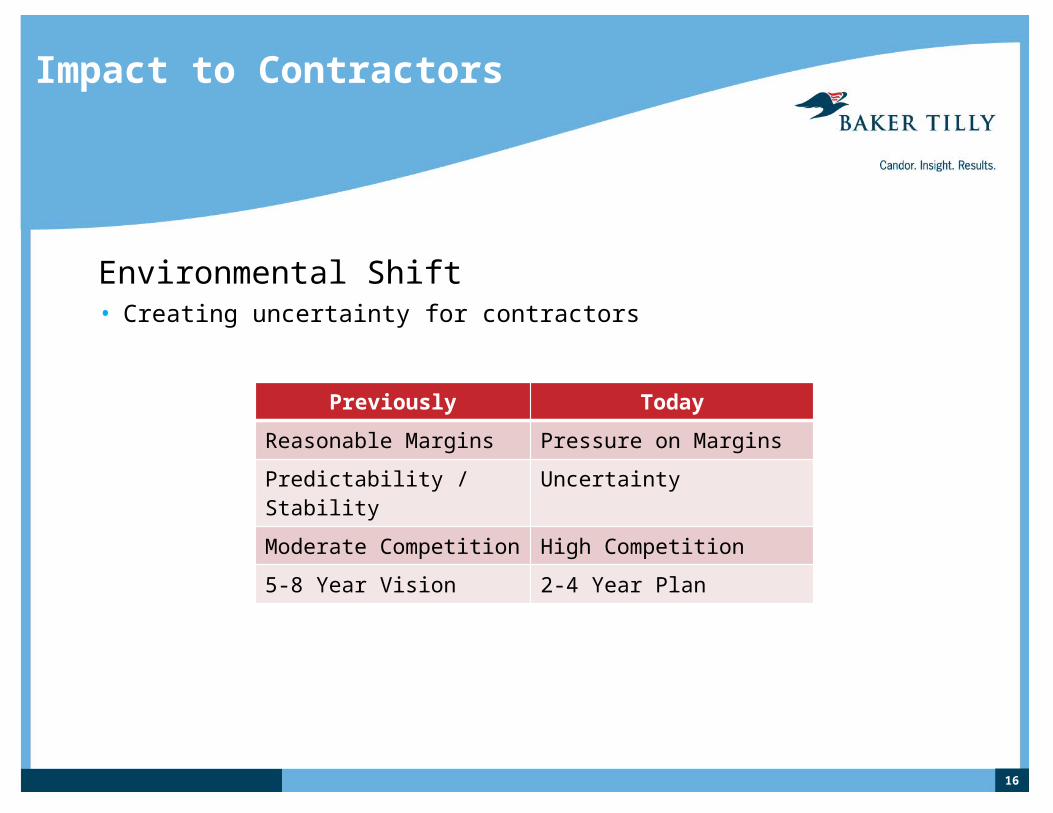

Impact to Contractors

Environmental Shift• Creating uncertainty for contractors

16

Previously Today

Reasonable Margins Pressure on Margins

Predictability / Stability Uncertainty

Moderate Competition High Competition

5-8 Year Vision 2-4 Year Plan

Impact to Contractors

Budget Pressure• Declining budgets have reduced profitability and forced companies to

reduce costs, often in contracts and compliance

• Intense competition in nearly every sector of the government contracts market

• Contractors are finding ways to leverage technology to reduce headcount

17

Impact to Contractors

Price Pressure• Competition driving increased pressure on prices

• Government increased use of lowest price technically acceptable (LPTA) source selection methods. This is a huge industry concern

• Increase in the number of claims and bid protests as a result

18

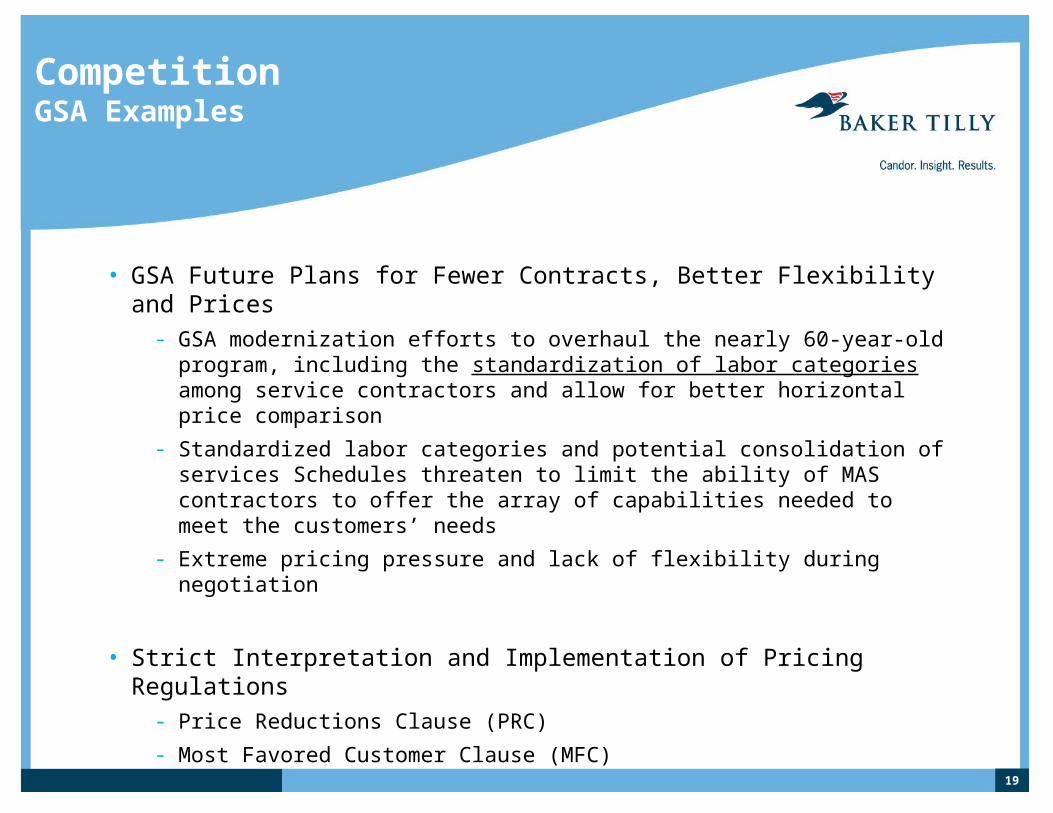

CompetitionGSA Examples

• GSA Future Plans for Fewer Contracts, Better Flexibility and Prices- GSA modernization efforts to overhaul the nearly 60-year-old program, including

the standardization of labor categories among service contractors and allow for better horizontal price comparison

- Standardized labor categories and potential consolidation of services Schedules threaten to limit the ability of MAS contractors to offer the array of capabilities needed to meet the customers’ needs

- Extreme pricing pressure and lack of flexibility during negotiation

• Strict Interpretation and Implementation of Pricing Regulations- Price Reductions Clause (PRC)

- Most Favored Customer Clause (MFC)

• GSA Reverse Auction- GSA Reverse Auction initiative intended to drive prices and costs down as a

result of sellers bidding to win business from agencies

19

Compliance and Enforcement Trends

20

Compliance

Increased Compliance Complexity• Increased oversight and scrutiny from government auditors

• Ability to make sense of all the new rules and guidance coming out from DCAA/DCMA

• Significant changes affecting supply-chain security

• Acquisition workforce demographics present a number of challenges (RFPs, Negotiation, Protests, Audits, Compliance & Enforcement)

21

22

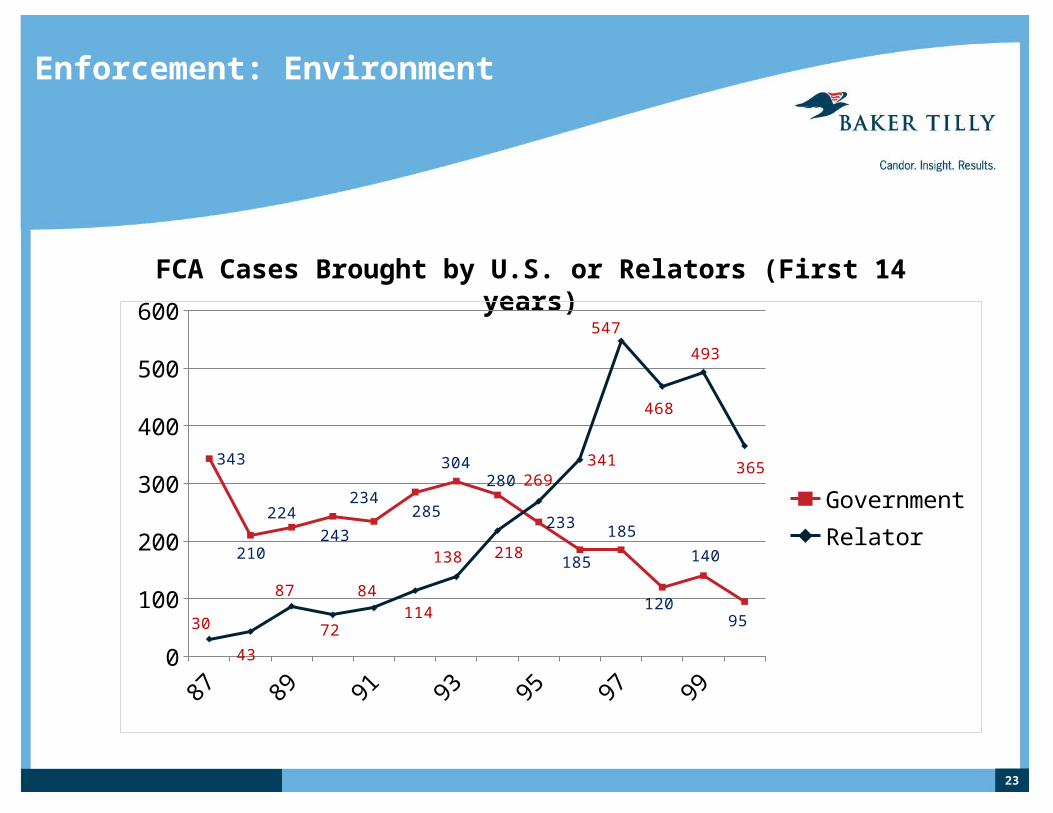

Enforcement: Environment

Government skepticism towards contractor products and pricing• As usual in a post-war environment, assumption that contractors and war-

profiteers are attempting to defraud the government

• Historically, stems back to the “Lincoln Law”- Enacted during the Civil War to combat fraud committed by companies selling supplies

to the Union Army

- Lincoln advocated passage of the False Claims Act (FCA), which contained “quit tam” provisions allowing citizens to sue, on the government’s behalf, companies and individuals defrauding the government – Passed by Congress on March 2nd, 1863

- Remained virtually unchanged until 1943, when amendments weakened the act and it fell into almost complete disuse

- FCA revisited in the mid-1980’s; DoD reported that 45 of the largest 100 defense contractors (including nine of the top 10) were under investigation for multiple fraud offenses

- Focus again shifted to the FCA more recently, with changes made in 2009 & 2010

Enforcement: Environment

23

FCA Cases Brought by U.S. or Relators (First 14 years)

87 88 89 90 91 92 93 94 95 96 97 98 9920000

100

200

300

400

500

600

343

210

224

243

234285

304280

233

185

185

120

140

9530

43

87

72

84114

138 218

269

341

547

468

493

365GovernmentRelator

Enforcement: Environment

24

FCA Cases Brought by U.S. or Relators (Last 13 years)

25

Enforcement: Regulatory Changes

Counterfeit Electronic Parts• Prevents the use of counterfeit electronic parts in products sold to the

government

• Current applicability thresholds:- Full or modified contractors covered under the Cost Accounting Standards (CAS)

- All subcontractors to CAS-covered prime contractors

- Commercial items and COTS items if those items are subcontracted by a CAS-covered contractor

- Counterfeit electronic parts, suspect electronic parts, and obsolete electronic parts, including any embedded software or firmware

Enforcement: Regulatory Changes

26

Counterfeit Electronic Parts• DoD passed a final ruling on May 6th, 2014 imposing new requirement that

contractors must “establish and maintain an acceptable counterfeit electronic part detection and avoidance system”

• On June 10th, 2014, the federal government proposed a new rule to expand coverage to include any product sold to the government

- Would apply to all prime and subcontractors regardless of CAS status

27

Enforcement: Enforcement Activity

Mandatory Disclosure Program• Requires all federal government contractors to report fraud and significant

overpayments in connection with their government contracts to the federal government

• Created by the DOJ and OIG community as an initiative to fight fraud with the knowledge of the limited benefits provided by voluntary disclosure

• Effective as of December 12, 2008

• As of June 2014, GSA OIG reports 134 disclosures, with approximately $47M in recovery

- Over one-third of disclosures relate to pricing issues

• DOD and GSA IG offices receiving the vast majority of disclosures- DOD OIG: 114 disclosures reported in the most recently reported six months

- GSA OIG: 131 disclosures total reported as of April 2014

• The resolution process has recently slowed

28

Enforcement: Enforcement Activity

Mandatory Disclosure Program (Continued)• Majority of disclosures to the GSA OIG to-date are related to contractors billing

over the contract price, or being in violation of defective pricing and the Price Reductions Clause (PRC)

• Majority of disclosures to the DOD OIG to-date are related to labor mischarging

• GSA and DOD are working together on multi-agency disclosures, while DCAA is often also getting involved

• All disclosures audited or investigated; some are more in-depth, which others are simply to ensure accurate repayment

• Contractors frustrated by overly aggressive nature of DCAA, lack of clarity regarding disclosure requirements, and increasing involvement of the US Attorney’s Office

29

Enforcement: Enforcement Activity

False Claims Act (FCA) Updates• Total recoveries under the FCA over the past five years is over $17B

• In FY2013, more than 846 new cases filed under the FCA- 752 of these case (or 89%) were filed by “qui tam” or whistleblowers

- More whistleblower lawsuits filed last year than in any year of the FCA’s history

• Relators have earned more than $387M in share awards over the past year

• Notable 2013 settlements and judgments included:- A $500M settlement with a pharmaceutical company accused of making false

statements to the FDA regarding the quality of its drugs

- A $473M settlement ($364M of which constituted damages under the FCA) with a provider of high-tech products and services to the global aerospace and building systems industries

Enforcement: Enforcement Activity

30

Total FCA Recoveries (in Millions)

Looking Ahead

31

A Few Thoughts

• New potential contractors looking expand into the Federal marketplace- Understand what you’re getting yourself into

• Established contractors- Stay abreast of new developments and enforcement activity

- Be thoughtful and think long-term when approaching cost reductions

• All Contractors- Focus on fundamentals of contracts management and compliance

32

Questions?

33

Bill Bressette, PrincipalGovernment Contractor Advisory Services

Baker TillyTel: (703) 923-8624,

DELETE THIS SLIDE

TO-Do’s

• Slide Notes• Depth on Sequestration and a couple other issues• Ditto for some examples (audit trends?)• Stories – highlight a few main points• Dry run it – might already be too long

34