© Adler & Colvin Fiscal Sponsorship Doing it Right! October 8, 2013 Stephanie L. Petit Adler &...

39

© Adler & Colvin Fiscal Sponsorship Doing it Right! October 8, 2013 Stephanie L. Petit Adler & Colvin www.adlercolvin.com www.nonprofitlawmatters.com

-

Upload

victoria-gilbert -

Category

Documents

-

view

222 -

download

0

Transcript of © Adler & Colvin Fiscal Sponsorship Doing it Right! October 8, 2013 Stephanie L. Petit Adler &...

© Adler & Colvin

Fiscal SponsorshipDoing it Right!

October 8, 2013

Fiscal SponsorshipDoing it Right!

October 8, 2013

Stephanie L. PetitAdler & Colvinwww.adlercolvin.comwww.nonprofitlawmatters.com

October 2013© Adler & Colvin

2

What is Fiscal Sponsorship?What is Fiscal Sponsorship?

• It is not in the Internal Revenue Code

• It is not in any corporations code

• It is a tool, a practical construct!

October 2013© Adler & Colvin

3

What is Fiscal Sponsorship?What is Fiscal Sponsorship?

Usually refers to an arrangement between a 501(c)(3) public charity and a project in which, typically, the charity receives and expends funds to advance the project while retaining discretion and control over the funds.

October 2013© Adler & Colvin

4

Not Fiscal AgencyNot Fiscal Agency

• Fiscal Agency – wrong term

• Fiscal Sponsorship – right term

• Why?

October 2013© Adler & Colvin

5

Two Main Ways to Do It RightTwo Main Ways to Do It Right

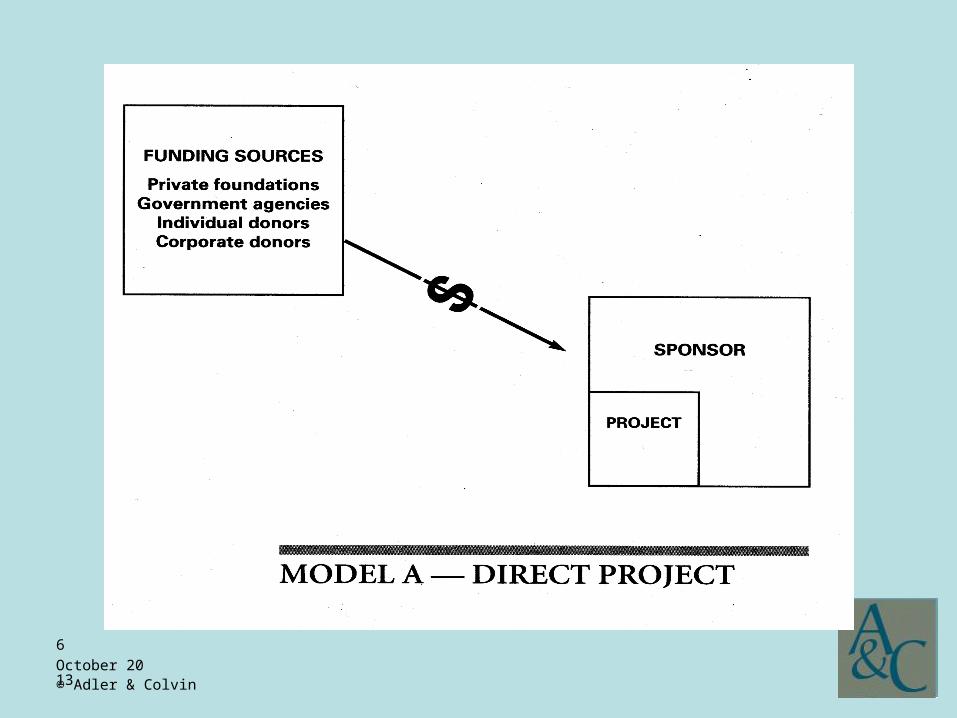

• Direct Project (“Model A”)

• Pre-Approved Grant (“Model C”, “Indirect”)

October 2013© Adler & Colvin

6

October 2013© Adler & Colvin

7

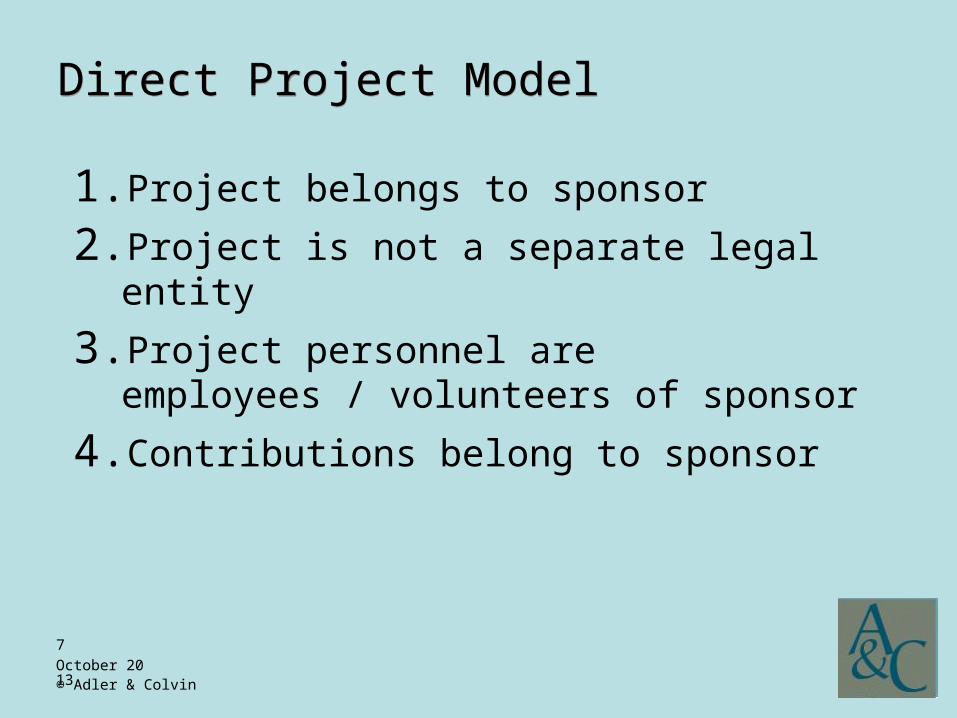

Direct Project ModelDirect Project Model

1. Project belongs to sponsor

2. Project is not a separate legal entity

3. Project personnel are employees / volunteers of sponsor

4. Contributions belong to sponsor

October 2013© Adler & Colvin

8

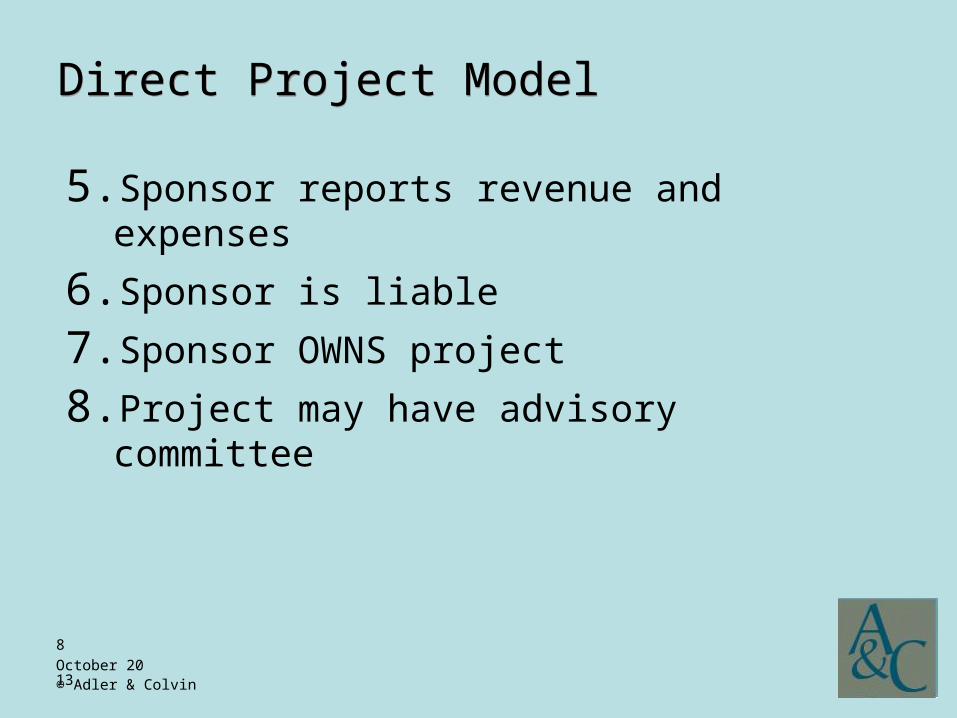

Direct Project ModelDirect Project Model

5. Sponsor reports revenue and expenses

6. Sponsor is liable

7. Sponsor OWNS project

8. Project may have advisory committee

October 2013© Adler & Colvin

9

Main Legal StepsMain Legal Steps

• Project director or directors establish a contract with sponsor.

• Sponsor’s board has already approved an FS program or approves now.

October 2013© Adler & Colvin

10

October 2013© Adler & Colvin

11

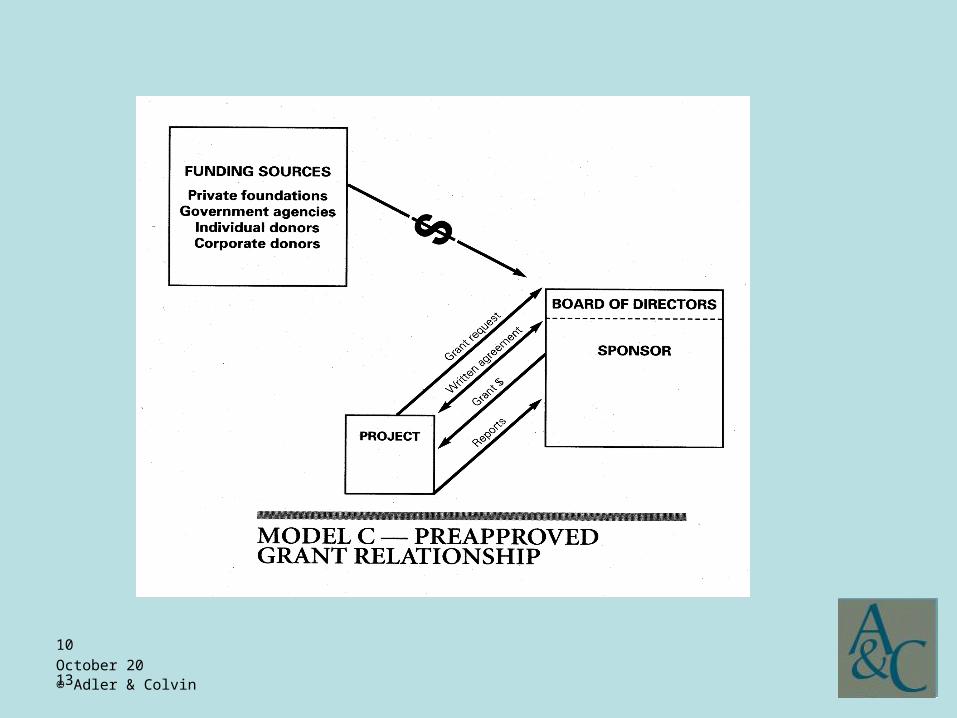

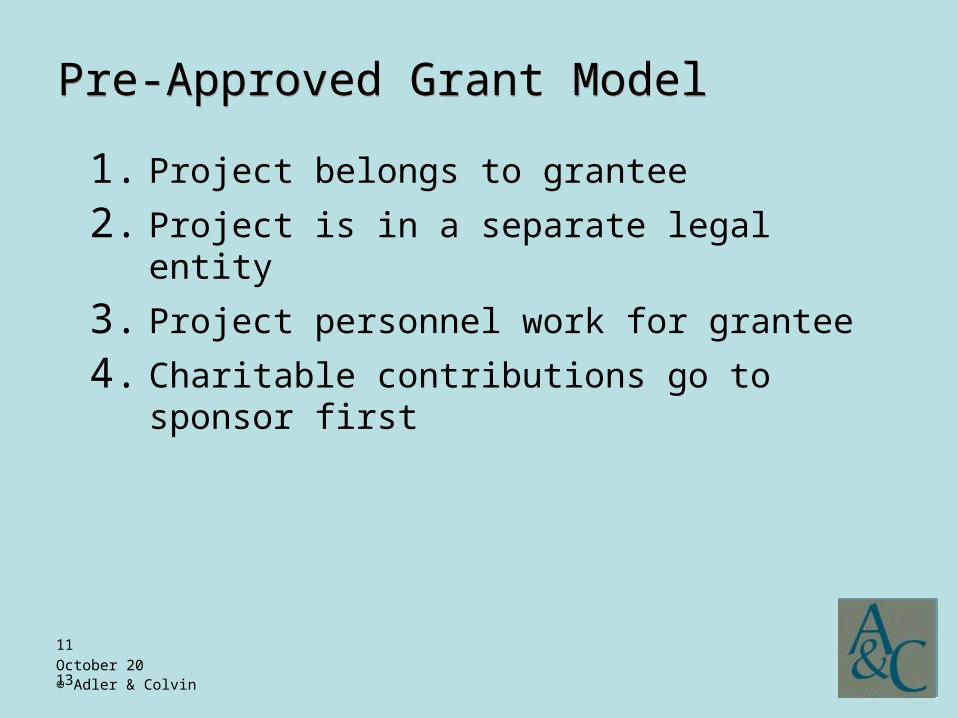

Pre-Approved Grant ModelPre-Approved Grant Model

1. Project belongs to grantee

2. Project is in a separate legal entity

3. Project personnel work for grantee

4. Charitable contributions go to sponsor first

October 2013© Adler & Colvin

12

Pre-Approved Grant ModelPre-Approved Grant Model

5. Sponsor retains “variance power” (discretion and control)

6. Sponsor reports contributions in and grants out

7. Grantee is liable for project

8. Grantee reports grant in and expenses out

October 2013© Adler & Colvin

13

Pre-Approved Grant StepsPre-Approved Grant Steps

1. Written grant proposal from project

2. Sponsor evaluation of proposal

3. Sponsor Board approval

4. Written grant agreement

5. Proper solicitation of funds

6. Proper accounting for funds

7. Reports from grantee to sponsor

October 2013© Adler & Colvin

14

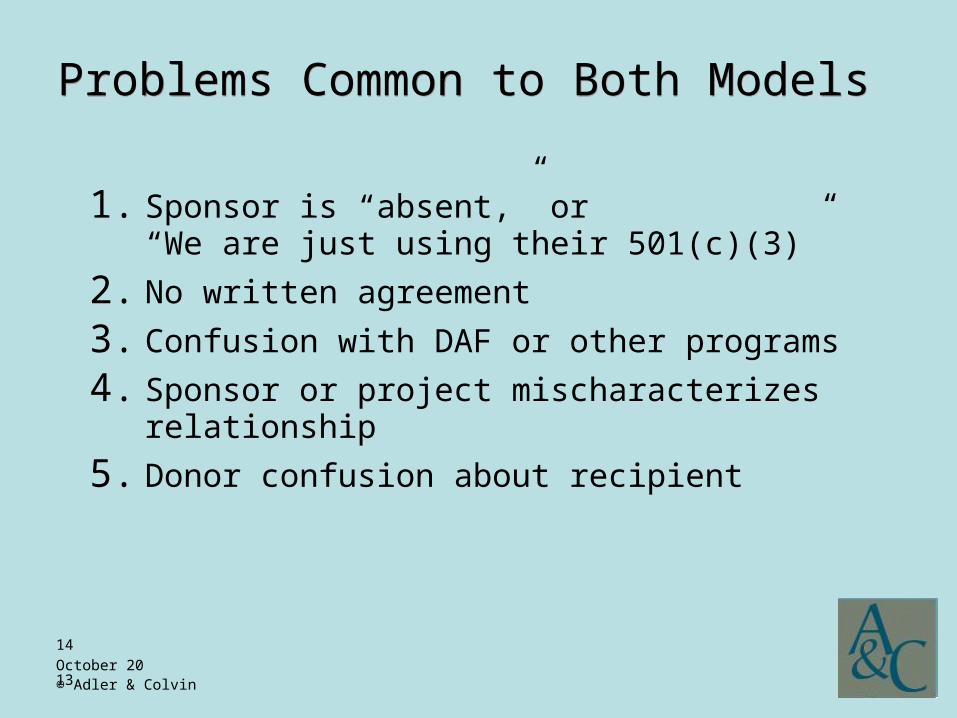

Problems Common to Both ModelsProblems Common to Both Models

1. Sponsor is “absent,” or “We are just using their 501(c)(3)”

2. No written agreement

3. Confusion with DAF or other programs

4. Sponsor or project mischaracterizes relationship

5. Donor confusion about recipient

October 2013© Adler & Colvin

15

Direct Project ProblemsDirect Project Problems

1. Sponsor fails to plan for liability

2. No pre-nuptial agreement• Dealing with the break-up

3. Ownership of intellectual property

4. Project spends more than it has

5. Treatment of employees

October 2013© Adler & Colvin

16

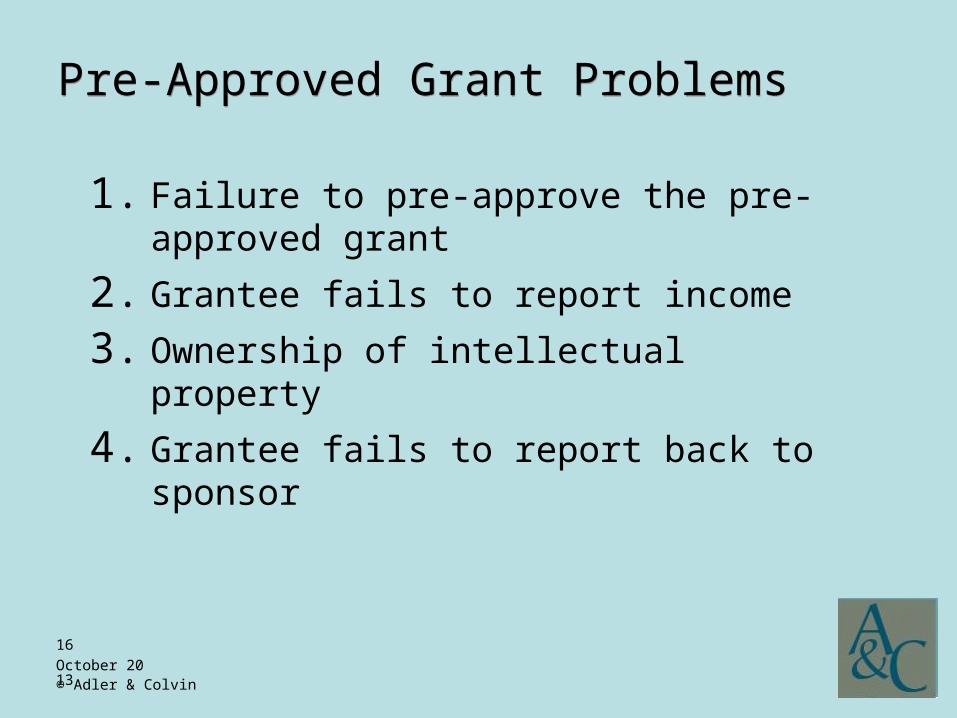

Pre-Approved Grant ProblemsPre-Approved Grant Problems

1. Failure to pre-approve the pre-approved grant

2. Grantee fails to report income

3. Ownership of intellectual property

4. Grantee fails to report back to sponsor

October 2013© Adler & Colvin

17

October 2013© Adler & Colvin

18

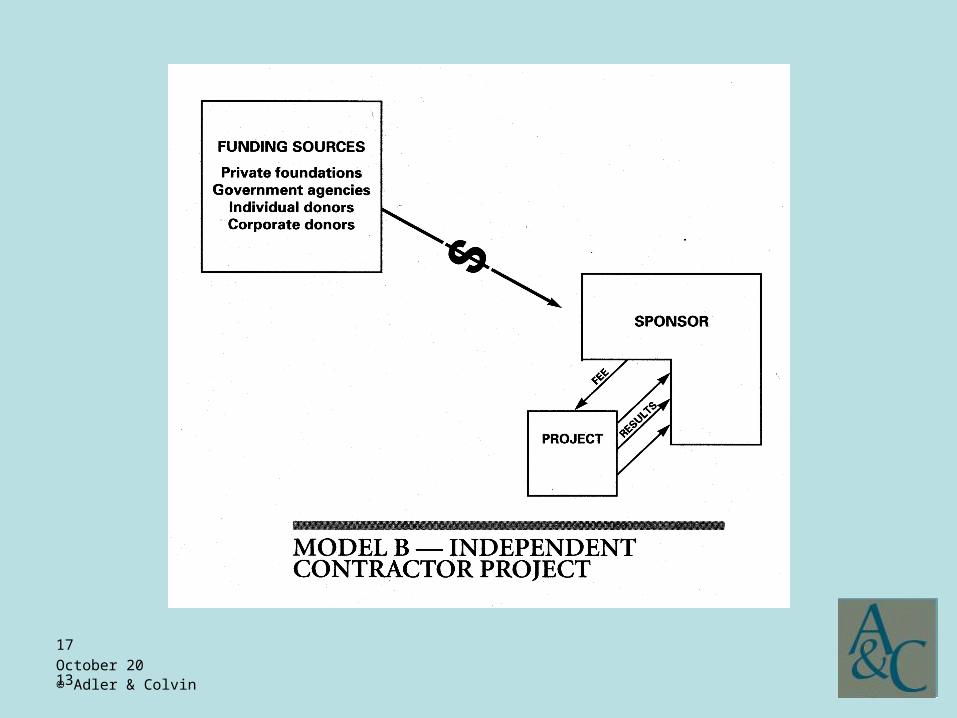

Model B – A Mashup?Model B – A Mashup?

• Like Model C – another entity conducts project

• Like Model A – sponsor more than just a grantor

October 2013© Adler & Colvin

19

October 2013© Adler & Colvin

20

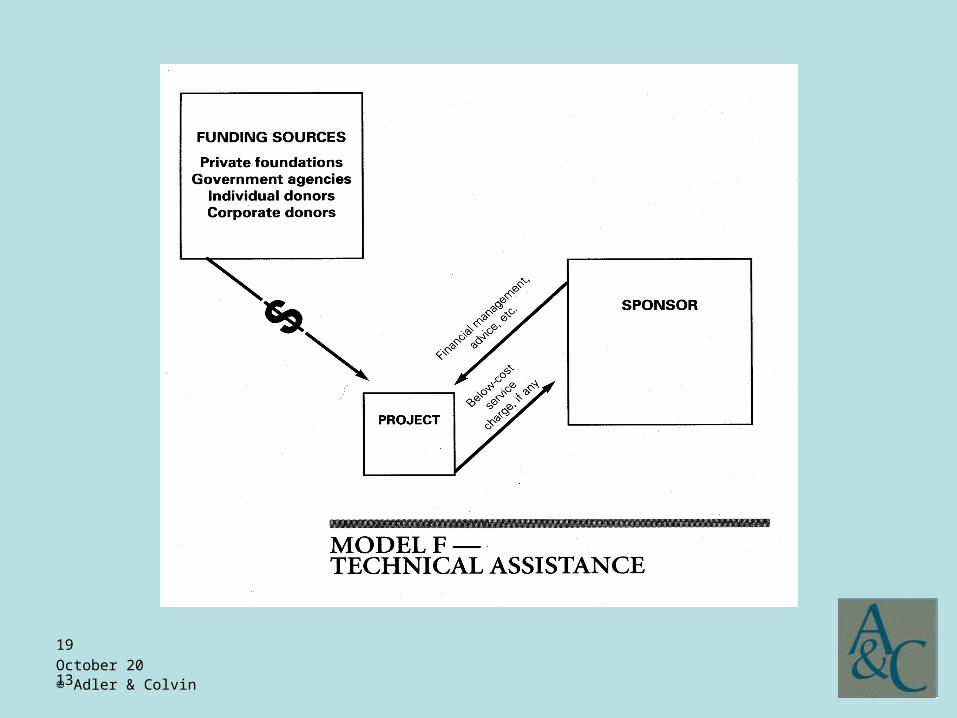

Model FModel F

• Purely administrative – no “discretion and control”

• Project in driver’s seat

- Not always considered fiscal sponsorship

• For-profit can do

• For exempt organizations, beware possible unrelated business income tax

October 2013© Adler & Colvin

21

October 2013© Adler & Colvin

22

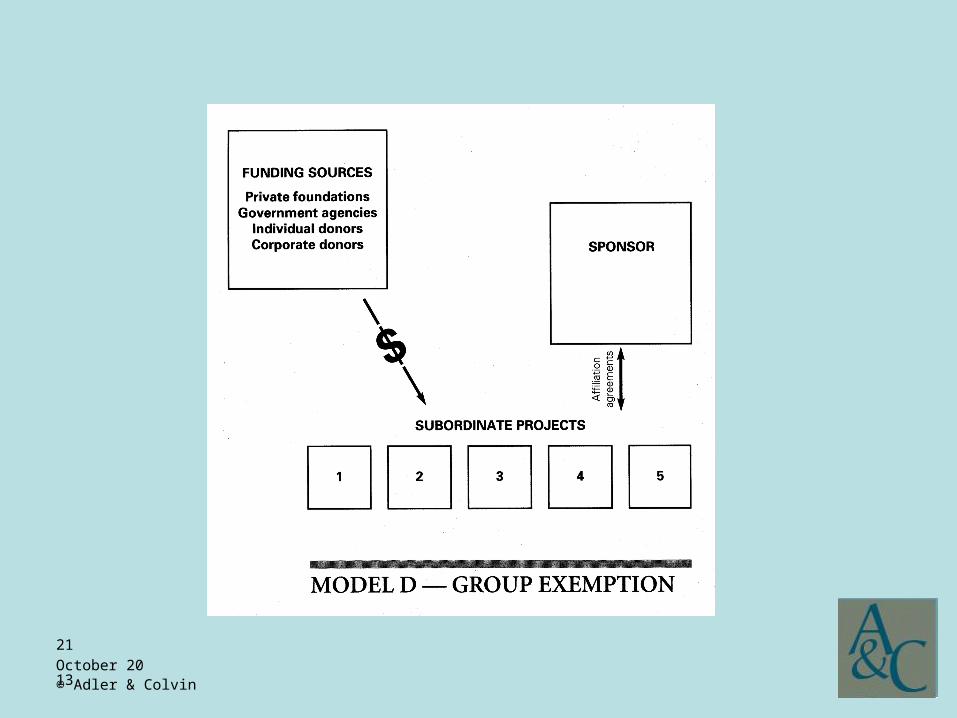

Group ExemptionGroup Exemption

• Procedure where a 501(c)(3) obtains ruling from IRS that it is the “central” organization or “head” of a group ruling

• Head organization steps into shoes of IRS to determine if organizations with whom affiliated meet 501(c)(3) and public charity standard (“subordinates”)

• Common for churches, groups with local / regional affiliates

October 2013© Adler & Colvin

23

Group ExemptionGroup Exemption

• May – or may not – involve provision of administrative services

• Contribution to subordinates need not go to head organization

• Resource: IRS Publication 4573

October 2013© Adler & Colvin

24

October 2013© Adler & Colvin

25

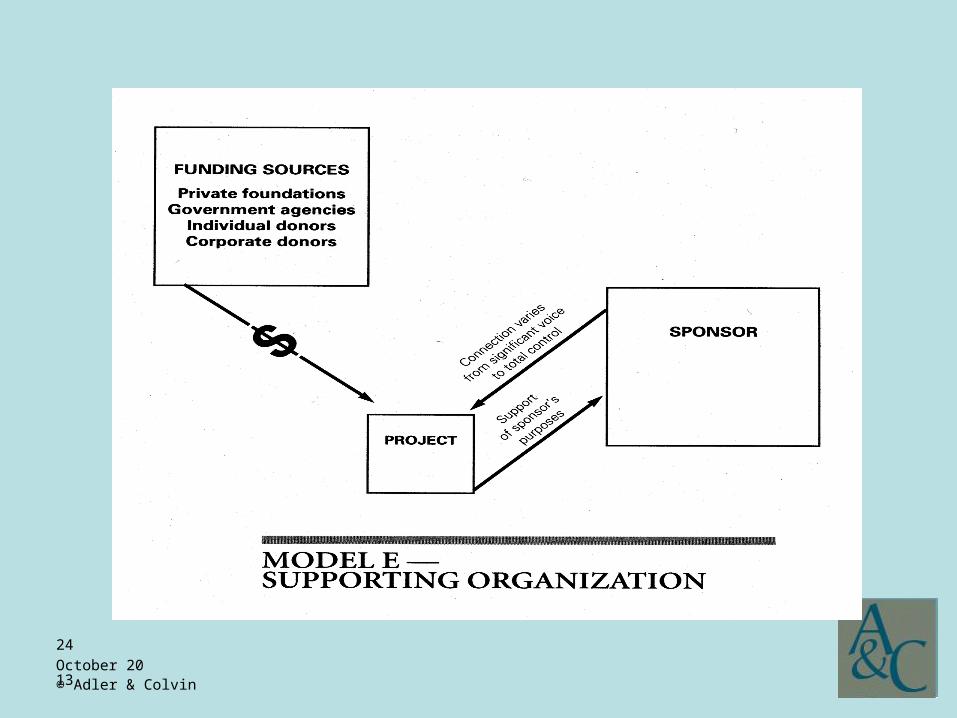

Supporting OrganizationSupporting Organization

• A 501(c)(3) public charity (not a private foundation) that has public charity status by virtue of its relationship with another public charity

• Tests (relationship, organizational, operational, lack of donor control)

October 2013© Adler & Colvin

26

Supporting OrganizationSupporting Organization

• May – or may not – involve provision of administrative services

• Contributions to supporting organization need not go to supported organization (typically, would not)

• Resource: http://www.irs.gov/Charities-&-Non-Profits/Charitable-Organizations/Supporting-Organizations-Requirements-and-Types

October 2013© Adler & Colvin

27

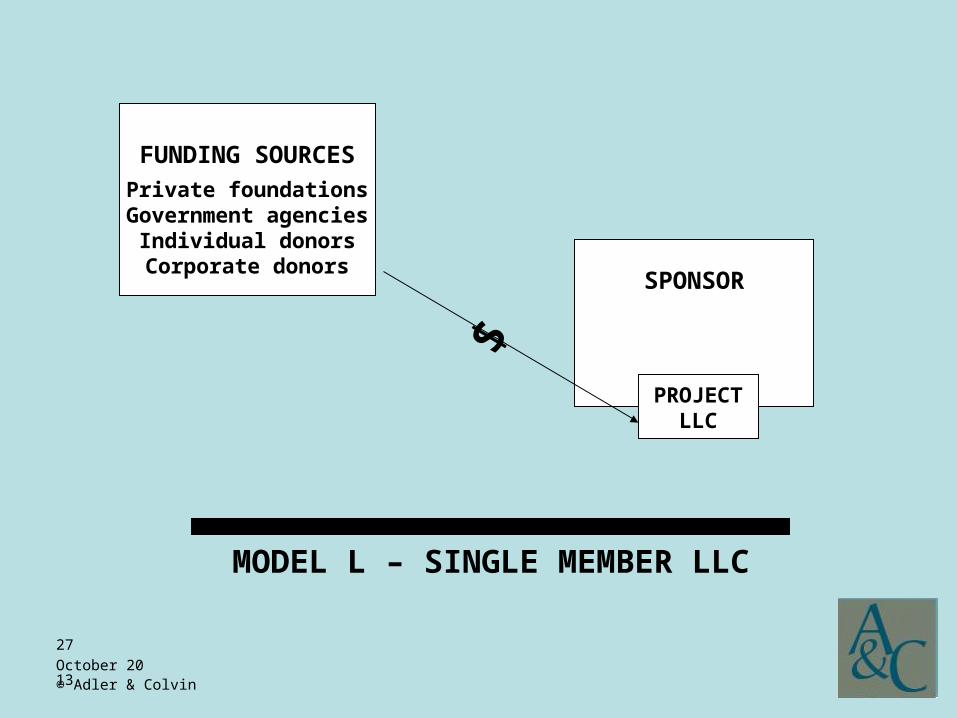

FUNDING SOURCES

Private foundationsGovernment agencies

Individual donorsCorporate donors

SPONSOR

PROJECTLLC

MODEL L – SINGLE MEMBER LLC

$

October 2013© Adler & Colvin

28

Model L – Single Member LLCModel L – Single Member LLC

• Sponsor is sole member (owner)

• LLC disregarded for federal tax purposes but liabilities separate from sponsor’s under state law

• Substitute for Model A if high liability

October 2013© Adler & Colvin

29

Legal StepsLegal Steps

• LLC is organized with Sponsor as sole member and executes an LLC operating agreement

• Sponsor and LLC may enter into a service or sponsorship agreement

October 2013© Adler & Colvin

30

IRS Notice 2012-52, allowing 501(c)(3)s to have subsidiary LLCs for liability protection, receiving deductible donations directly from the public. See:

http://www.nonprofitlawmatters.com/2012/08/09/irs-issues-guidance-on-the-deductibility-of-donations-to-llc-subsidiaries-of-section-501c3-organizations/

IRS CommentsIRS Comments

October 2013© Adler & Colvin

31

Resource for Model LResource for Model L

“The Use of LLCs in Fiscal Sponsorship – a New Model” available at “publications” page of www.adlercolvin.com or http://www.adlercolvin.com/resources/basic-resources.php#tab_publications

October 2013© Adler & Colvin

32

Recent Developments

October 2013© Adler & Colvin

33

IRS-Related CommentsIRS-Related Comments

• 2012 ACT (Advisory Committee on Tax Exempt and Government Entities) report to the IRS recommends fiscal sponsorship in some circumstances and also asks for guidance (http://t.co/5YdOln4m)

• Post-Hurricane Sandy IRS encourages use of existing organizations instead of setting up new charity (announcement IR-2012-87)

October 2013© Adler & Colvin

34

Increased attention to charitable trust doctrine under state law.

State Charitable Trust LawState Charitable Trust Law

October 2013© Adler & Colvin

35

“Because the restricted fund is held under the charitable trust doctrine for the purposes of the Project as understood by and with funding sources, the parties intend that assets in the restricted fund shall not be subject to the claims of any creditor or to legal process resulting from activities of Sponsor unrelated to the Project.”

Using State Charitable Trust Law to Protect Project AssetsUsing State Charitable Trust Law to Protect Project Assets

October 2013© Adler & Colvin

36

• International Humanities Center(http://www.nonprofitlawmatters.com/2012/02/16/doing-right-by-the-projects-fiscal-sponsorship-after-ihc-2/)

• Other examples (e.g. Help is Here)

Fiscal Sponsor CollapsesFiscal Sponsor Collapses

October 2013© Adler & Colvin

37

• Effective January 1, 2013

• California Government Code Section 12599.8

Legislation in California: AB 2327Legislation in California: AB 2327

October 2013© Adler & Colvin

38

“For any year that the balance sheet of a charitable organization shows that it holds restricted net assets, while reporting negative unrestricted net assets, the organization shall provide an explanation of its compliance with its charitable trust responsibilities and proof of directors' and officers' liability insurance coverage to the Attorney General's Registry of Charitable Trusts.”

New California Government Code Section 12599.8New California Government Code Section 12599.8

October 2013© Adler & Colvin

39

ResourcesResources

• Fiscal Sponsorship: 6 Ways To Do It Right, 2005 edition

• www.fiscalsponsorship.com

• www.fiscalsponsordirectory.org

• National Network of Fiscal Sponsors:www.fiscalsponsors.org

![Web viewClaudette Colvin : twice toward justice [ Book ] B COLVIN Hoose, Phillip M., 1947- Published 2009](https://static.fdocuments.us/doc/165x107/5aaefeac7f8b9a190d8ccd5e/web-viewclaudette-colvin-twice-toward-justice-book-b-colvin-hoose-phillip.jpg)