© 2008 The Brattle Group Developments and Issues in Utility Energy Efficiency – 2008 Presentation...

19

© 2008 The Brattle Group Developments and Issues in Utility Energy Efficiency – 2008 Presentation to Consumer Affairs Committee National Association of Regulatory Utility Commissioners February 17, 2008 Peter Fox-Penner Co-Chairman and Principal The Brattle Group 1850 M Street, NW Suite 1200 Washington, DC 20036 202.955.5050 www.brattle.com Note: This presentation does not represent the complete views of The Brattle Group or its clients.

-

Upload

edward-parrish -

Category

Documents

-

view

216 -

download

2

Transcript of © 2008 The Brattle Group Developments and Issues in Utility Energy Efficiency – 2008 Presentation...

© 2008 The Brattle Group

Developments and Issues inUtility Energy Efficiency – 2008

Presentation toConsumer Affairs Committee

National Association of Regulatory Utility Commissioners

February 17, 2008

Peter Fox-PennerCo-Chairman and Principal

The Brattle Group1850 M Street, NW

Suite 1200Washington, DC 20036

202.955.5050www.brattle.com

Note: This presentation does not represent the complete views of The Brattle Group or its clients.

2 © 2008

The Brattle Group/Personal Bio

• Independent economic and financial consultancy founded in 1991 in Cambridge, Massachusetts - 175 staff in five offices – U.S. and Europe

• Brattle is a frequent consultant to all segments of energy industry – primarily IOUS. Also consultant to EEI on energy efficiency policy.

• Dr. Fox-Penner is former DOE Senior official in Energy Efficiency and Renewable Energy and former G.O.C.S.

• Dr. Fox-Penner is also a Vice-Chairman of ENpartners/Daylight Technologies (energy efficiency company) and a member of the Board for Enviance, Inc. (GHG tracking software.)

• All opinions expressed and errors are personal – but thanks to ICF and RAP

3 © 2008

Why Greater Energy Efficiency Is Essential

• Reduces large rate increase impacts that are going to arise from

► Fuel price increases► Demand growth ► Enormous construction cost increases► Climate change

• Also reduces riskiness and volatility in future resource plans

• Good economic policy in recessionary times

• Good environmental policy

4 © 2008

What is needed?

Electric Infrastructure Investments (2007 – 2016)

• Generation ~$ 53 Billion

• Transmission ~$ 85 Billion

• Distribution ~$145 Billion

• Environmental ~$30-60 Billion• Excludes potential cost of climate legislation

• Other cost factors• Critical infrastructure protection, RTOs, pension funds, health care,

disaster recovery, end of rate freezes, RPS, fuel

CapEx ~$750 – 900 Billion w/o climate changeWith climate change > $1.2 Trillion

Statistics courtesy of Edison Electric Institute (EEI)

5 © 2008

New Generation Capacity by Fuel Type, 1950 - 2007

Source: Henwood Energy Consulting

6 © 2008

Resurgence of Rate Cases

0

2

4

6

8

10

12

14

16

18

20

Courtesy of Edison Electric Institute (EEI), December 2007

Number of Cases Filed, 1990 - 2007

7 © 2008

Role of Energy Efficiency in Combating Climate Change

Coal

w/CCS

Gas

w/CCS Nuclear

Hydro

Wind

SolarOil

Demand Reduction

Demand with No Policy

Biomass

Full Portfolio

(economic allocation)

8

7

6

5

4

3

2

1

02000 2010 2020 2030 2040 2050

Tri

llio

n k

Wh

per

Ye

ar

8

7

6

5

4

3

2

1

02000 2010 2020 2030 2040 2050

Limited Portfolio

(economic allocation)

Coal

Gas

Nuclear

WindHydro

Biomass

Coal

Coal with CCS

Gas

Nuclear

HydroWind

Courtesy of Electric Power Research

Institute (EPRI)

8 © 2008

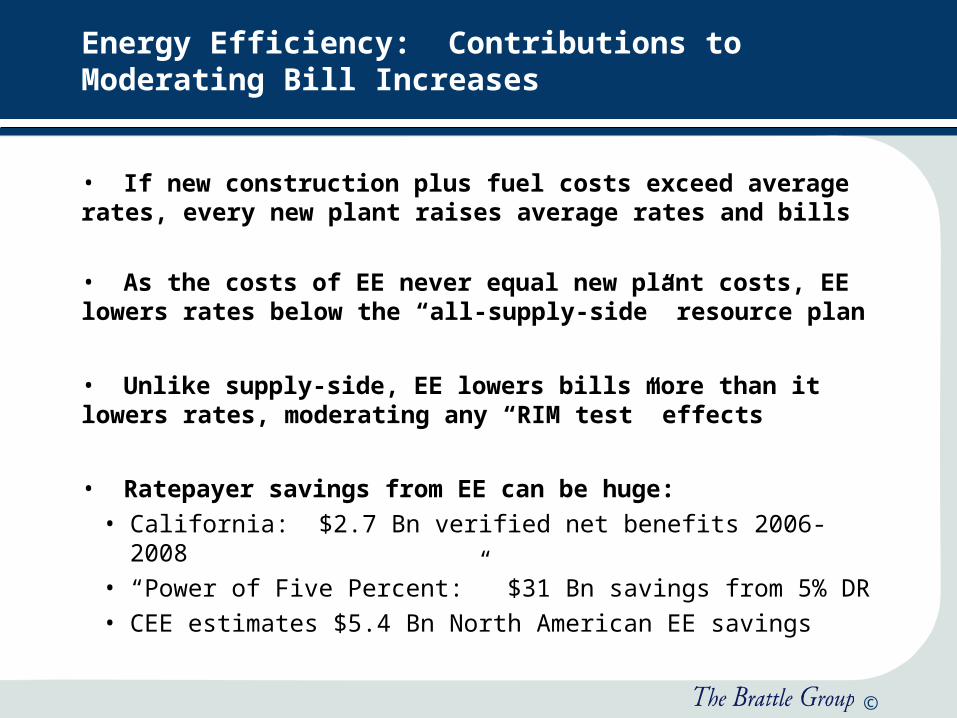

Energy Efficiency: Contributions to Moderating Bill Increases

• If new construction plus fuel costs exceed average rates, every new plant raises average rates and bills

• As the costs of EE never equal new plant costs, EE lowers rates below the “all-supply-side” resource plan

• Unlike supply-side, EE lowers bills more than it lowers rates, moderating any “RIM test” effects

• Ratepayer savings from EE can be huge:• California: $2.7 Bn verified net benefits 2006-2008• “Power of Five Percent:” $31 Bn savings from 5% DR• CEE estimates $5.4 Bn North American EE savings

9 © 2008

Enormous Energy Efficiency Activity Already Underway

• National Action Plan for Energy Efficiency (NAPEE)

• State EERS, GHG cap and trade

• 2007 Federal Energy Bill

• Electric and Gas Utility IRP and DSM► Better resource plans, potential studies, and forecasts► Growing EE programs► Decoupling and energy efficiency incentives► Expanded DR and Smart Grid programs

10 © 2008

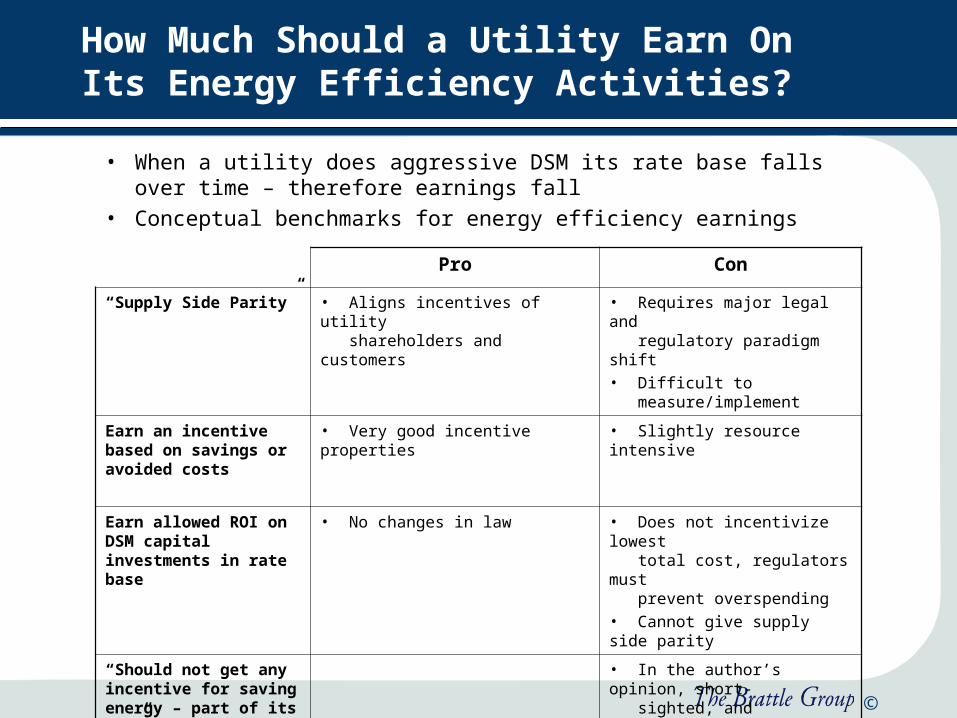

How Much Should a Utility Earn On Its Energy Efficiency Activities?

• When a utility does aggressive DSM its rate base falls over time – therefore earnings fall

• Conceptual benchmarks for energy efficiency earnings

Pro Con

“Supply Side Parity” • Aligns incentives of utility shareholders and customers

• Requires major legal and regulatory paradigm shift• Difficult to measure/implement

Earn an incentive based on savings or avoided costs

• Very good incentive properties • Slightly resource intensive

Earn allowed ROI on DSM capital investments in rate base

• No changes in law • Does not incentivize lowest total cost, regulators must prevent overspending• Cannot give supply side parity

“Should not get any incentive for saving energy – part of its job”

• In the author’s opinion, short- sighted, and counterproductive: “ sticks alone don’t work nearly as well as carrots and sticks”

11 © 2008

Action Items for the Regulatory Community

• Improved information practices – toolkits in IRP, DSM, DR► Integrating utility and other EE efforts► Potential, technology, economic data

• Staffing-Education-Resource management within your organization

• Energy efficiency – incentives and oversight

• Stakeholder education/communication

12 © 2008

• Judy Chang 617.234.5630 [email protected]

• Robert Earle 415.217.1016 [email protected]

• Ahmad Faruqui 415.217.1026 [email protected]

• Phil Hanser 617.234.5671 [email protected]

• Matthew McCaffree 202.419.3314 [email protected]

• Joe Wharton 415.217.1015 [email protected]

Additional Brattle Contacts for Energy Efficiency

13 © 2008

Appendix

14 © 2008

PRISM Analysis Details

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation

No Existing Plant Upgrades

40% New Plant Efficiency by 2020–2030

150 GWe Plant Upgrades

46% New Plant Efficiency by 2020; 49% in 2030

Carbon Capture & Sequestration

None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by

2017; 2%/yr Thereafter

DER< 0.1% of Base Load in

20305% of Base Load in 2030

Source: EPRI

EIA Base Case 2007

* Achieving all targets is very aggressive, but potentially feasible.

15 © 2008

ACEEE Scenarios

Source: Jeff Schlegal, Energy Efficiency and Global Warming: What Must be Done, ACEEE Energy Efficiency as a Resource Conference

16 © 2008

The Status of Cost Recovery, Decoupling & Performance Incentives

States Direct Cost Recovery

Rate Case Arizona, California, Colorado, District of Columbia, Hawaii, Idaho, Illinois, Indiana, Iowa, Minnesota, Missouri, Montana, Nevada, New Mexico, Pennsylvania, Texas, Utah, Wisconsin

SBC Arizona, California, Connecticut, Maine, Massachusetts, Montana, New Hampshire, New Jersey, New York, Ohio, Oregon, Rhode Island, Vermont, Wisconsin

Tariff Rider/ surcharge Florida, Idaho, Iowa, Kentucky, Ohio, Utah, Washington

Lost Margin Recovery

Decoupling Electric: California, Idaho, New York, Rhode Island, Minnesota, Maryland. Proposed Electric: Delaware, DC, New Jersey. Gas: California, Indiana, Maryland, Missouri, Nevada, New Jersey, New York, North Carolina, Ohio, Oregon, Rhode Island, Utah. Proposed Gas: Arkansas, Arizona, Colorado, Delaware, Illinois, Michigan, Minnesota, Pennsylvania, Tennessee, Virginia, Wisconsin

Lost Margin Recovery Mechanism

Connecticut, Indiana, Kentucky

Performance Incentives

Arizona, California, Connecticut, Hawaii, Idaho, Indiana, Kansas, Kentucky, Massachusetts, Minnesota, Montana, Nevada, New Hampshire, Rhode Island, Vermont.

Courtesy of Val Jensen, ICF

17 © 2008

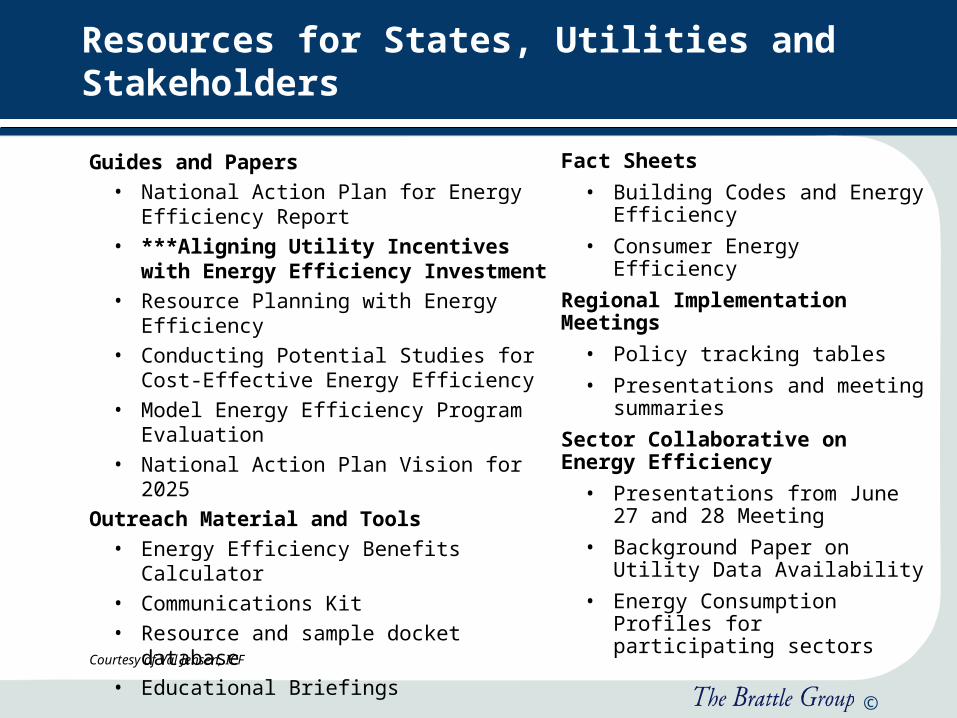

Resources for States, Utilities and Stakeholders

Guides and Papers • National Action Plan for Energy Efficiency

Report • ***Aligning Utility Incentives with

Energy Efficiency Investment• Resource Planning with Energy Efficiency • Conducting Potential Studies for Cost-

Effective Energy Efficiency • Model Energy Efficiency Program

Evaluation • National Action Plan Vision for 2025

Outreach Material and Tools• Energy Efficiency Benefits Calculator • Communications Kit • Resource and sample docket database• Educational Briefings

Fact Sheets

• Building Codes and Energy Efficiency

• Consumer Energy Efficiency

Regional Implementation Meetings

• Policy tracking tables

• Presentations and meeting summaries

Sector Collaborative on Energy Efficiency

• Presentations from June 27 and 28 Meeting

• Background Paper on Utility Data Availability

• Energy Consumption Profiles for participating sectors

Courtesy of Val Jensen, ICF

18 © 2008

National Action Plan for Energy Efficiency Addresses Utility Barriers

Released on July 31, 2006 at the National Association of Regulatory Utility Commissioners meeting

Goal: To create a sustainable, aggressive national commitment to energy efficiency through gas and electric utilities, utility regulators, and partner organizations

Over 50 member public-private Leadership Group developed five recommendations and commits to take action

Additional commitments to energy efficiency – exceeds 90 organizations

National Action Plan for Energy Efficiency

Recommendations

1. Recognize energy efficiency as a high-priority energy resource.

2. Make a strong, long-term commitment to implement cost-effective energy efficiency as a resource.

3. Broadly communicate the benefits of and opportunities for energy efficiency.

4. Provide sufficient, timely and stable program funding to deliver energy efficiency where cost-effective.

5. Modify policies to align utility incentives with the delivery of cost-effective energy efficiency and modify ratemaking practices to promote energy efficiency investments.

Courtesy of Val Jensen, ICF

19 © 2008

For More Information on NAPEE

Stacy [email protected](202) 343-9606

Joe [email protected](202) 343-9631

Larry Mansueti

(202) 586-2588

www.epa.gov/eeactionplan

Courtesy of Val Jensen, ICF