© 2000, 2003 Six Sigma Academy Valuing Intangible Projects November, 2003.

23

© 2000, 2003 Six Sigma Academy Valuing Intangible Projects November, 2003

-

Upload

poppy-blake -

Category

Documents

-

view

214 -

download

1

Transcript of © 2000, 2003 Six Sigma Academy Valuing Intangible Projects November, 2003.

© 2000, 2003 Six Sigma Academy

Valuing Intangible Projects

November, 2003

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 2

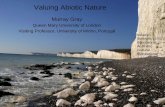

Examples Of Intangible Projects

• Sales & Marketing

- Telemarketing

- Direct Mail

- Sales Force Effectiveness

• Engineering/R&D

- New Product Design

- New/Improved product features

• Manufacturing/Production

- Cost reduction (passed on to customer as price reduction)

- Product quality/consistency

- Expanded capacity (to meet customer needs)

• Installation & delivery

- Options (expedited, etc.)

- Accuracy (shipping)

- Cost to customer

• Maintenance/Support and service- Scheduling (Cable TV maintenance call)- Availability (and cost) of parts

• Billing/Collections- Invoice accuracy

Customer Facing/Customer Satisfaction

Other• General R&D

- New Technology- Non-Product Specific

• Employee Satisfaction- Telecommuting- Flex-Hours- Employee Self-Serve Projects

• Safety• Regulatory Legislated

- EEOC- Tax- OSHA

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 3

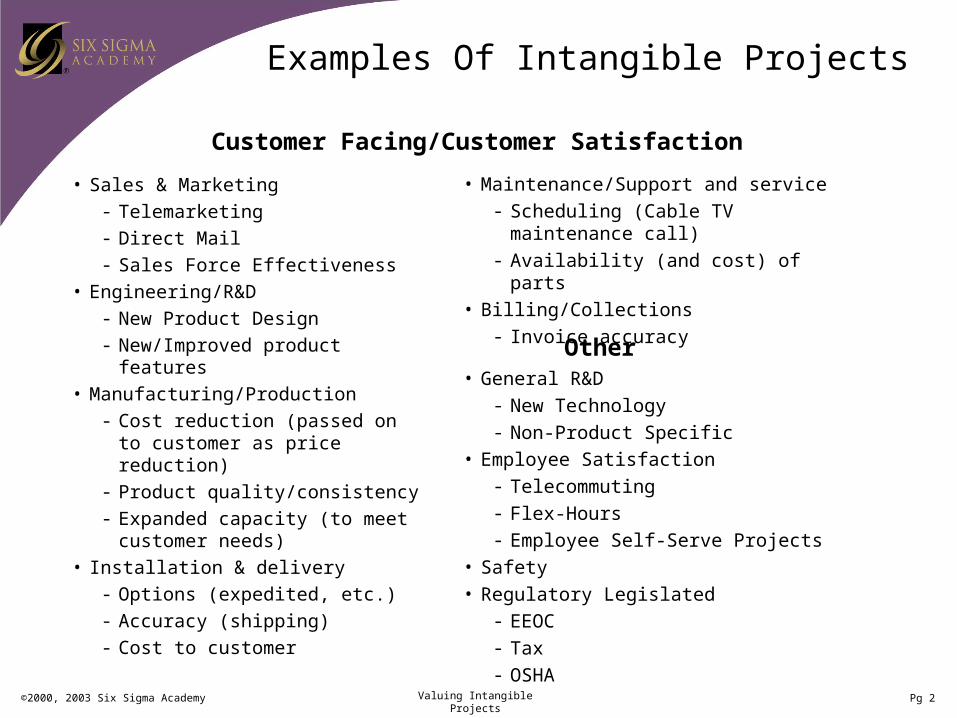

Measurement And Valuation

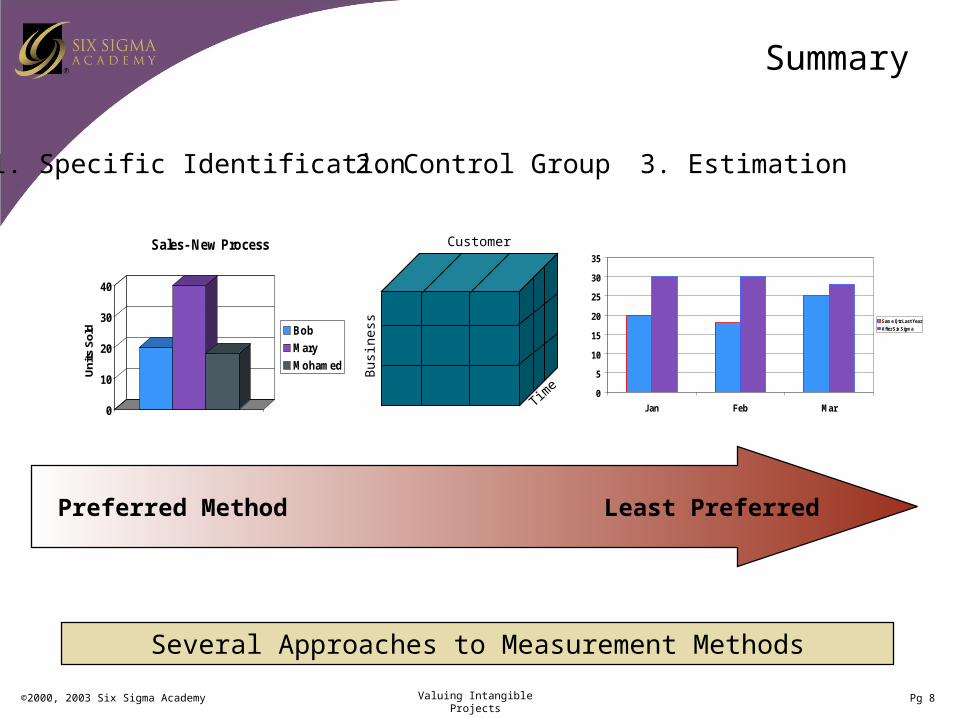

Measurement:1.Specific identification

• Counting Volume of increased sales units• Number of safety events• Specific price increases• Number of customers selecting “options”

2.Control Group Comparative analysis• Sales person to Sales person comparison• Region to Region comparison

3.Estimation:• Business expert opinion• Market Data• Competitive Analysts

IDOpportunity

DetermineMeasurement

Method

ImproveProcess

MeasureImprovement

Benefits Determination (dollars to defects):1.Accounting Method (benefits identified at account level)2.Present Value/ WACC (same as accounting method plus

consideration for time-value or investment value of money)3.Market or Utility Value (what is it worth in today's market?):

• Business Expert Opinion • Market research supporting customer purchasing habits

4.Replacement Value (What would you pay an outside firm to complete the project?)

BenefitsDetermination

Method

ValueThe

Improvement

ImplementControl

Plan

EstablishBaseline

Project Valuation is a combination of Measurement, Benefits Determination and ROI Calculation.

RO

I C

alcu

latio

n

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 4

Measurement Methods

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 5

1. Specific Identification

• Sales Force Effectiveness Project

• Control Plan Implemented

• Sales force records and specifically identifies sales closed as a result of new process – cross-validated with customer survey data

Example:

Identify and record each sale attributable to new process.

Sales – New Process

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 6

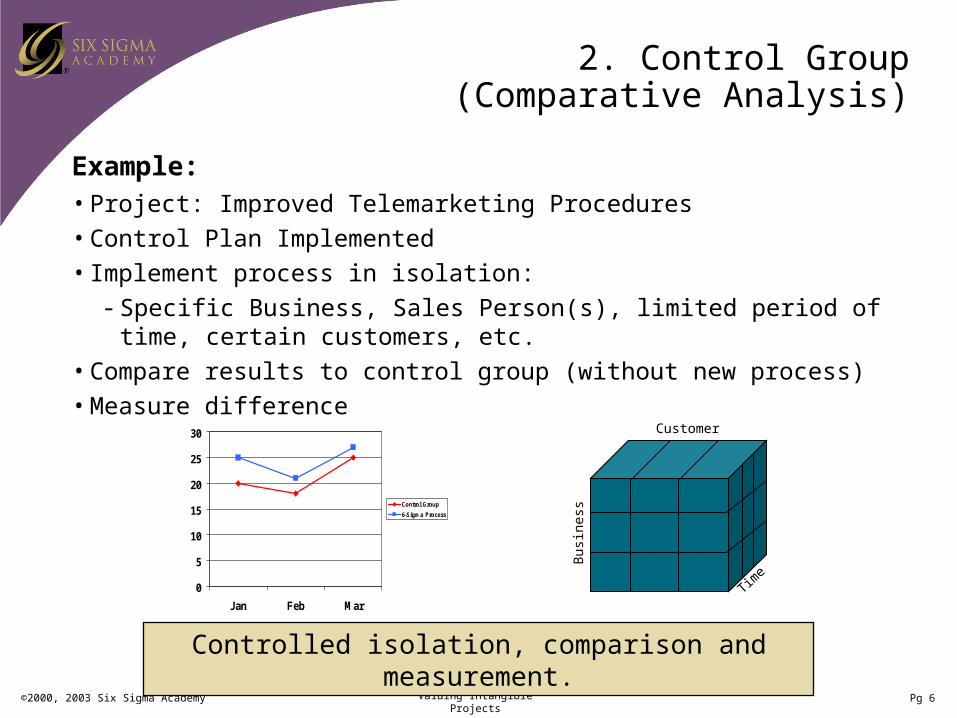

2. Control Group(Comparative Analysis)

• Project: Improved Telemarketing Procedures

• Control Plan Implemented

• Implement process in isolation:

- Specific Business, Sales Person(s), limited period of time, certain customers, etc.

• Compare results to control group (without new process)

• Measure difference

Example:

Controlled isolation, comparison and measurement.

Customer

Time

Bus

ines

s0

5

10

15

20

25

30

Jan Feb Mar

Control Group

6-Sigma Process

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 7

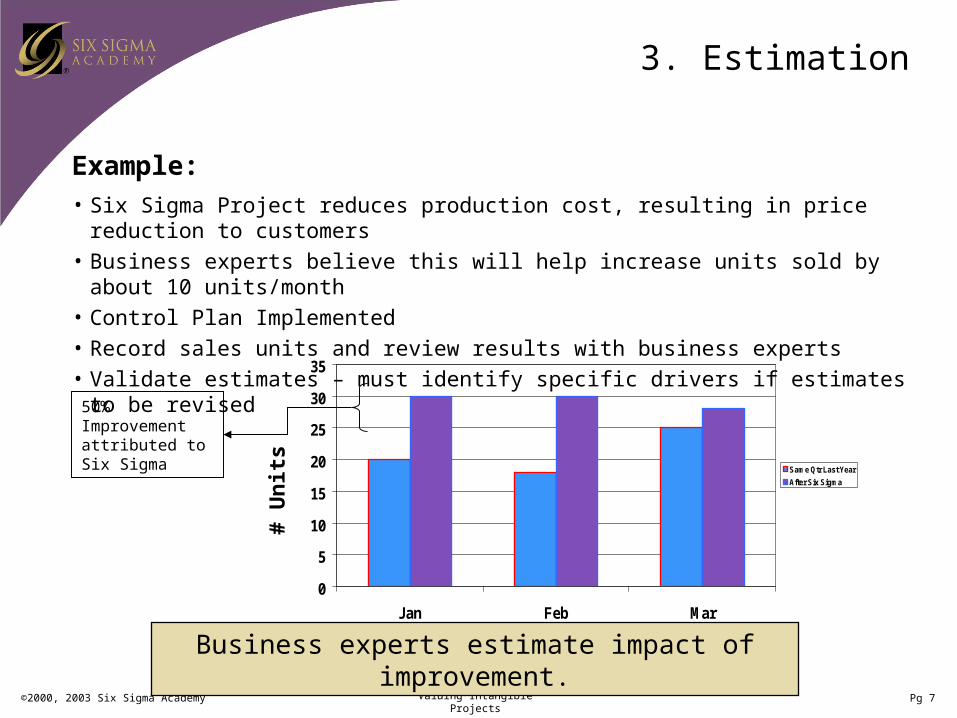

3. Estimation

• Six Sigma Project reduces production cost, resulting in price reduction to customers• Business experts believe this will help increase units sold by about 10 units/month• Control Plan Implemented• Record sales units and review results with business experts• Validate estimates – must identify specific drivers if estimates to be revised

Example:

Business experts estimate impact of improvement.

0

5

10

15

20

25

30

35

Jan Feb Mar

Same Qtr Last Year

After Six Sigma

50% Improvement attributed to Six Sigma

# U

nit

s

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 8

Summary

0

10

20

30

40

Uni

ts S

old

Sales- New Process

Bob

Mary

Mohamed

Customer

Time

Bus

ines

s

0

5

10

15

20

25

30

35

Jan Feb Mar

Same Qtr Last Year

After Six Sigma

1. Specific Identification 2. Control Group 3. Estimation

Preferred Method Least Preferred

Several Approaches to Measurement Methods

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 9

Benefits Determination

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 10

Benefits Determination

Method Benefits Determination Comments

1. Accounting Method Direct contribution to Operating Income* (OI) Preferred method, accurate & simple. E.g. Increase sales of 1,000 units over the next year at the current price of $8,000 will result in an increase to revenue of $8M. At the current OI contribution rate of 15% this will translate to an OI contribution of $1.2M

2. Present Value/WACC Cash inflows less Cash outflows over time with time-value of money consideration. Also consider use of Weighted Average Cost Of Capital (WACC)

Various versions. See controller for appropriate/required calculation and interest/ WACC assumptions.

3. Utility Value Rely on market, expert and/or competitive price & value to estimate potential value to company

Use this input to calculate ROI and/or prepare business case

4. Replacement Value Determine the maximum amount you would pay (value) an outside firm to complete the project successfully

Should be prepared to actually pay for this service

Should approach project valuation with the same rigor, thoroughness and accountability as any “investment” decision.

* Your Company may use EBIT, Net Income or other measure instead of Operating Income

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 11

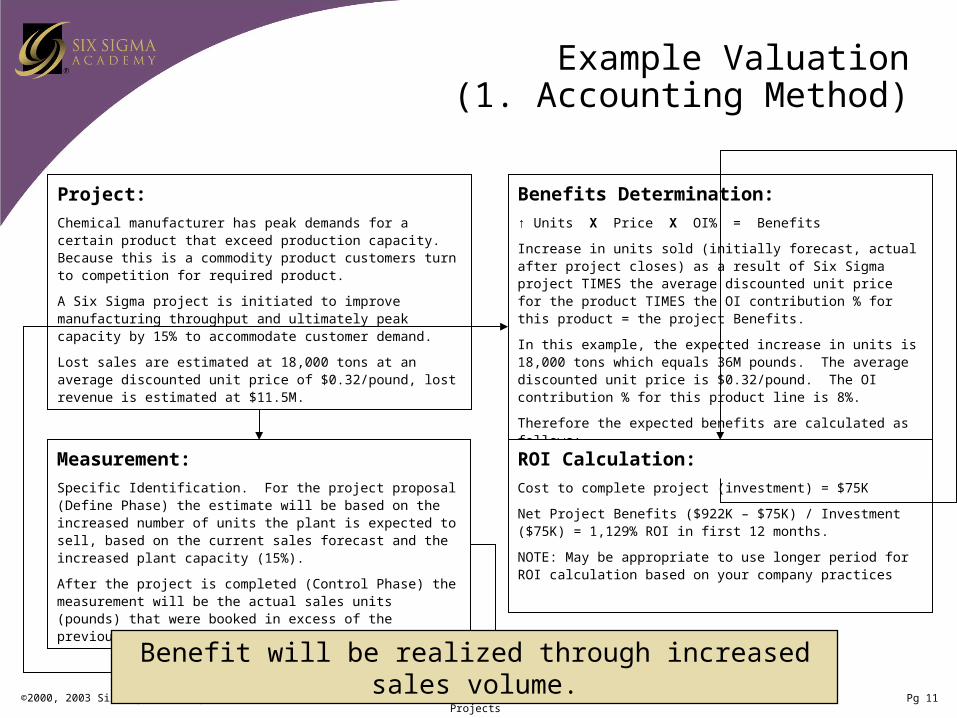

Example Valuation(1. Accounting Method)

Project:

Chemical manufacturer has peak demands for a certain product that exceed production capacity. Because this is a commodity product customers turn to competition for required product.

A Six Sigma project is initiated to improve manufacturing throughput and ultimately peak capacity by 15% to accommodate customer demand.

Lost sales are estimated at 18,000 tons at an average discounted unit price of $0.32/pound, lost revenue is estimated at $11.5M.

Measurement:

Specific Identification. For the project proposal (Define Phase) the estimate will be based on the increased number of units the plant is expected to sell, based on the current sales forecast and the increased plant capacity (15%).

After the project is completed (Control Phase) the measurement will be the actual sales units (pounds) that were booked in excess of the previous plant capacity.

Benefits Determination:

↑ Units X Price X OI% = Benefits

Increase in units sold (initially forecast, actual after project closes) as a result of Six Sigma project TIMES the average discounted unit price for the product TIMES the OI contribution % for this product = the project Benefits.

In this example, the expected increase in units is 18,000 tons which equals 36M pounds. The average discounted unit price is $0.32/pound. The OI contribution % for this product line is 8%.

Therefore the expected benefits are calculated as follows:

36,000,000 X $0.32 X 8% = $922K annual OI

ROI Calculation:

Cost to complete project (investment) = $75K

Net Project Benefits ($922K – $75K) / Investment ($75K) = 1,129% ROI in first 12 months.

NOTE: May be appropriate to use longer period for ROI calculation based on your company practices

Benefit will be realized through increased sales volume.

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 12

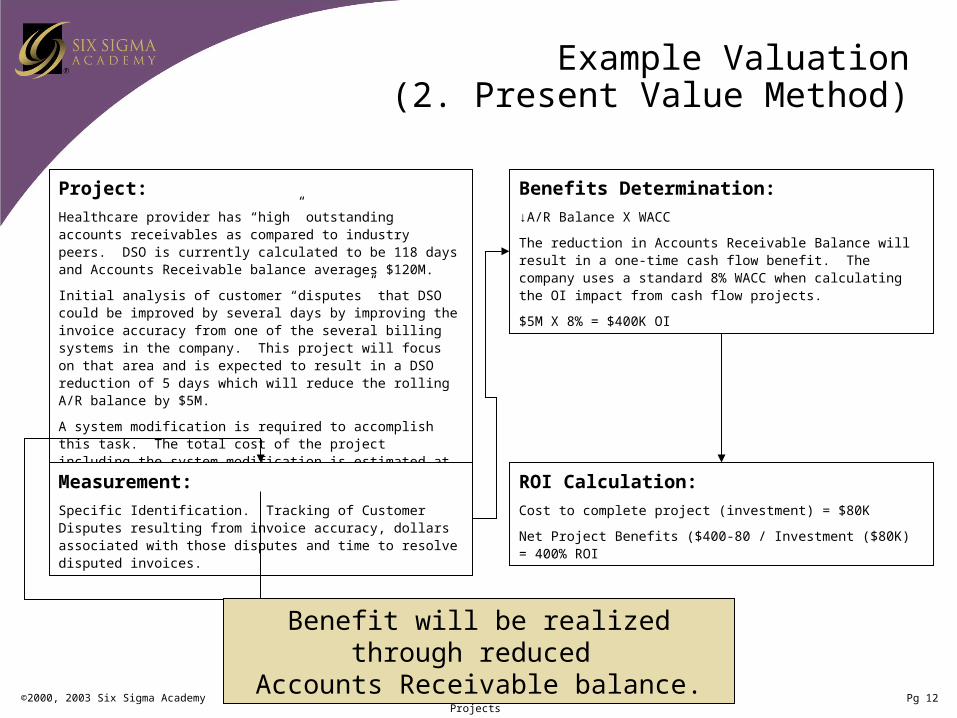

Example Valuation(2. Present Value Method)

Project:

Healthcare provider has “high” outstanding accounts receivables as compared to industry peers. DSO is currently calculated to be 118 days and Accounts Receivable balance averages $120M.

Initial analysis of customer “disputes” that DSO could be improved by several days by improving the invoice accuracy from one of the several billing systems in the company. This project will focus on that area and is expected to result in a DSO reduction of 5 days which will reduce the rolling A/R balance by $5M.

A system modification is required to accomplish this task. The total cost of the project including the system modification is estimated at $80K

Measurement:

Specific Identification. Tracking of Customer Disputes resulting from invoice accuracy, dollars associated with those disputes and time to resolve disputed invoices.

Benefits Determination:

↓A/R Balance X WACC

The reduction in Accounts Receivable Balance will result in a one-time cash flow benefit. The company uses a standard 8% WACC when calculating the OI impact from cash flow projects.

$5M X 8% = $400K OI

ROI Calculation:

Cost to complete project (investment) = $80K

Net Project Benefits ($400-80 / Investment ($80K) = 400% ROI

Benefit will be realized through reduced Accounts Receivable balance.

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 13

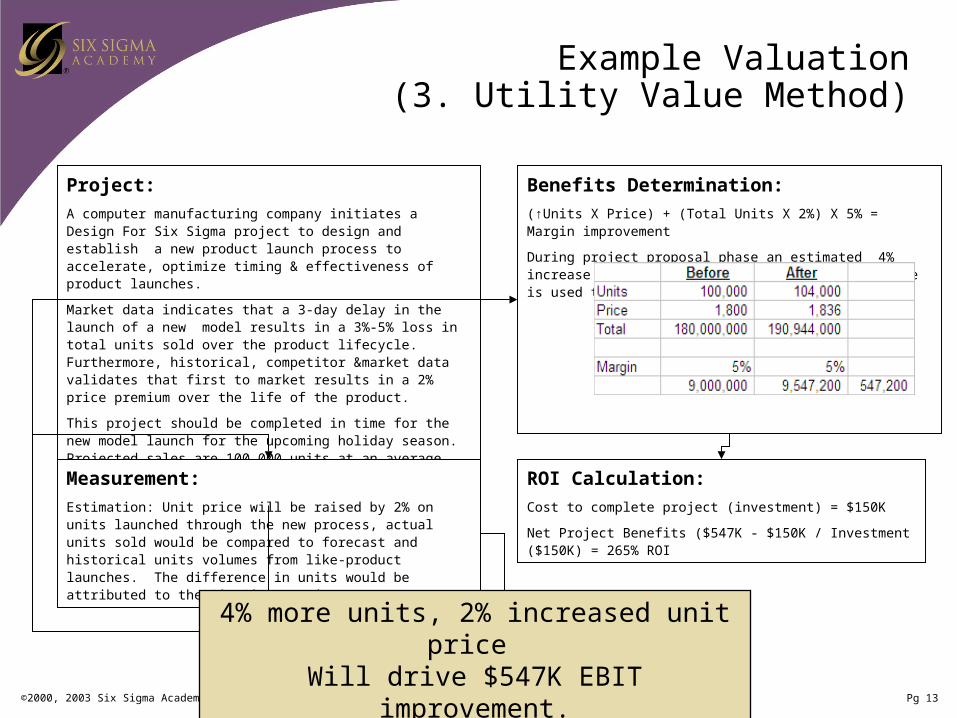

Benefits Determination:

(↑Units X Price) + (Total Units X 2%) X 5% = Margin improvement

During project proposal phase an estimated 4% increase in units and a 2% increase in unit price is used to estimate increase in revenue.

Example Valuation(3. Utility Value Method)

Project:

A computer manufacturing company initiates a Design For Six Sigma project to design and establish a new product launch process to accelerate, optimize timing & effectiveness of product launches.

Market data indicates that a 3-day delay in the launch of a new model results in a 3%-5% loss in total units sold over the product lifecycle. Furthermore, historical, competitor &market data validates that first to market results in a 2% price premium over the life of the product.

This project should be completed in time for the new model launch for the upcoming holiday season. Projected sales are 100,000 units at an average units price of $1,800/unit. EBIT % for these products is 5%.

Measurement:

Estimation: Unit price will be raised by 2% on units launched through the new process, actual units sold would be compared to forecast and historical units volumes from like-product launches. The difference in units would be attributed to the Six Sigma project.

ROI Calculation:

Cost to complete project (investment) = $150K

Net Project Benefits ($547K - $150K / Investment ($150K) = 265% ROI

4% more units, 2% increased unit price Will drive $547K EBIT improvement.

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 14

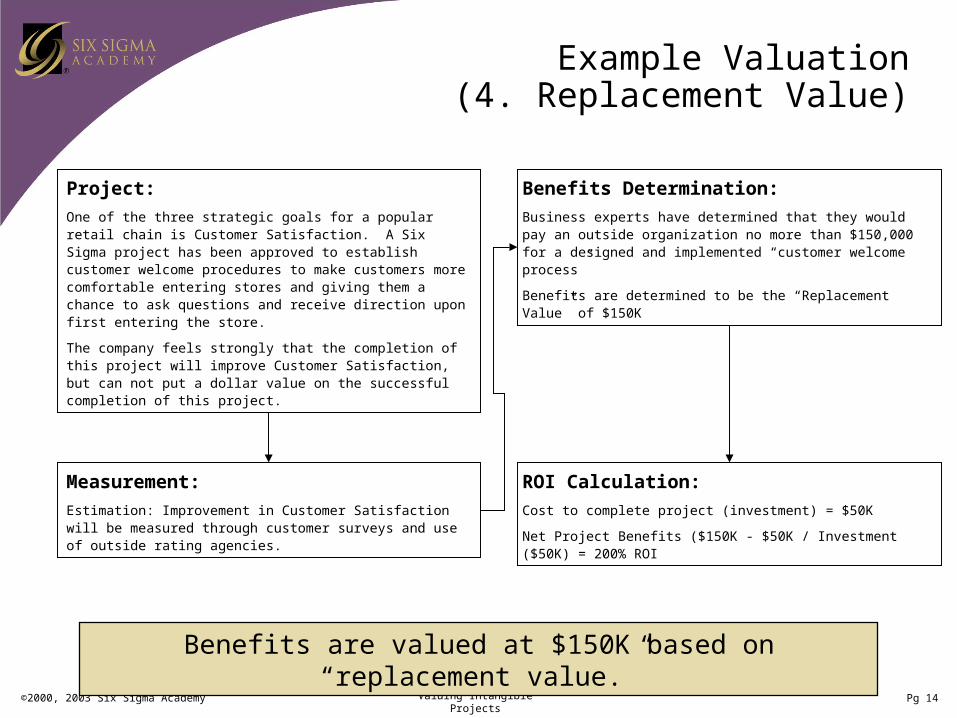

Benefits Determination:

Business experts have determined that they would pay an outside organization no more than $150,000 for a designed and implemented “customer welcome process”

Benefits are determined to be the “Replacement Value” of $150K

Example Valuation(4. Replacement Value)

Project:

One of the three strategic goals for a popular retail chain is Customer Satisfaction. A Six Sigma project has been approved to establish customer welcome procedures to make customers more comfortable entering stores and giving them a chance to ask questions and receive direction upon first entering the store.

The company feels strongly that the completion of this project will improve Customer Satisfaction, but can not put a dollar value on the successful completion of this project.

Measurement:

Estimation: Improvement in Customer Satisfaction will be measured through customer surveys and use of outside rating agencies.

ROI Calculation:

Cost to complete project (investment) = $50K

Net Project Benefits ($150K - $50K / Investment ($50K) = 200% ROI

Benefits are valued at $150K based on “replacement value.”

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 15

R&D And Engineering Project Examples

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 16

R&D Projects – Relationship To Financials

Sales 100 Cost of Goods Sold 60 Gross Profit 40

SG&A 12 R&D 5 Other Expenses 3

EBIT 20

Tax 11

Net Income 9

• Increase in Volume (# of units sold)

• Price Increase (price per unit)

• Reduction in Product Cost (Cost Of Goods Sold)

R&D projects primarily impact sales and cost of goods sold.

Target Contributions: Financial Statement (P&L)

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 17

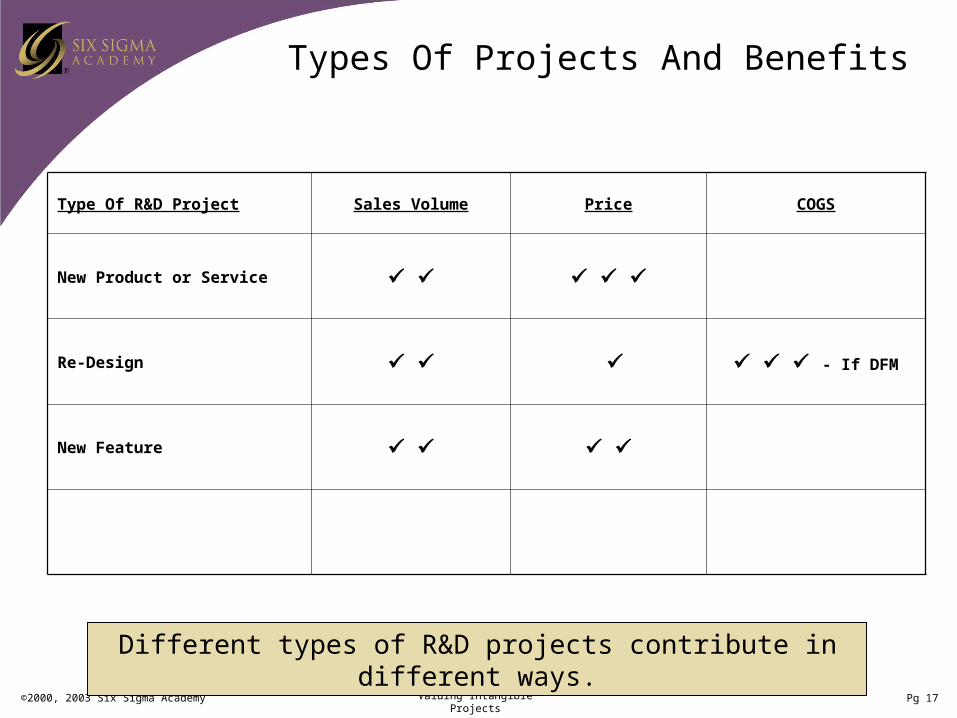

Types Of Projects And Benefits

Type Of R&D Project Sales Volume Price COGS

New Product or Service

Re-Design - If DFM

New Feature

Different types of R&D projects contribute in different ways.

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 18

Sources Of Additional Sales Volume

Your Co.

Co. 2

Co. 3

Co.4

1. Take market share from competition

2. Increase overall marketYour Co.

Co. 2

Co. 3

Co.4

3. Create new market

Various ways to increase sales volume.

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 19

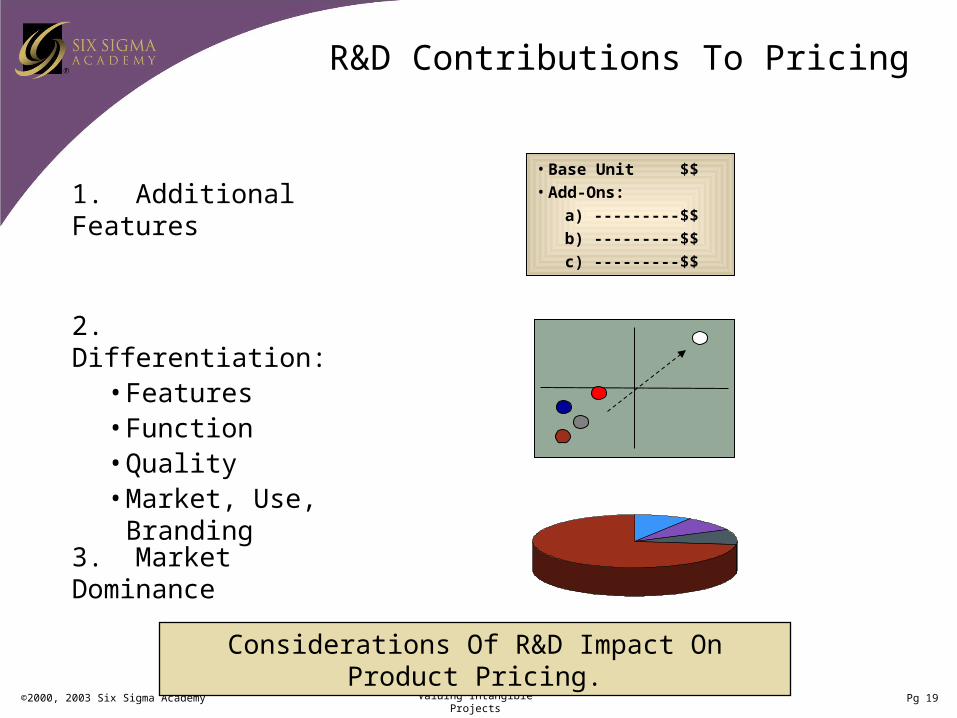

R&D Contributions To Pricing

1. Additional Features• Base Unit $$• Add-Ons:

a) --------- $$

b) --------- $$

c) --------- $$

2. Differentiation:• Features• Function• Quality• Market, Use,

Branding

3. Market Dominance

Considerations Of R&D Impact On Product Pricing.

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 20

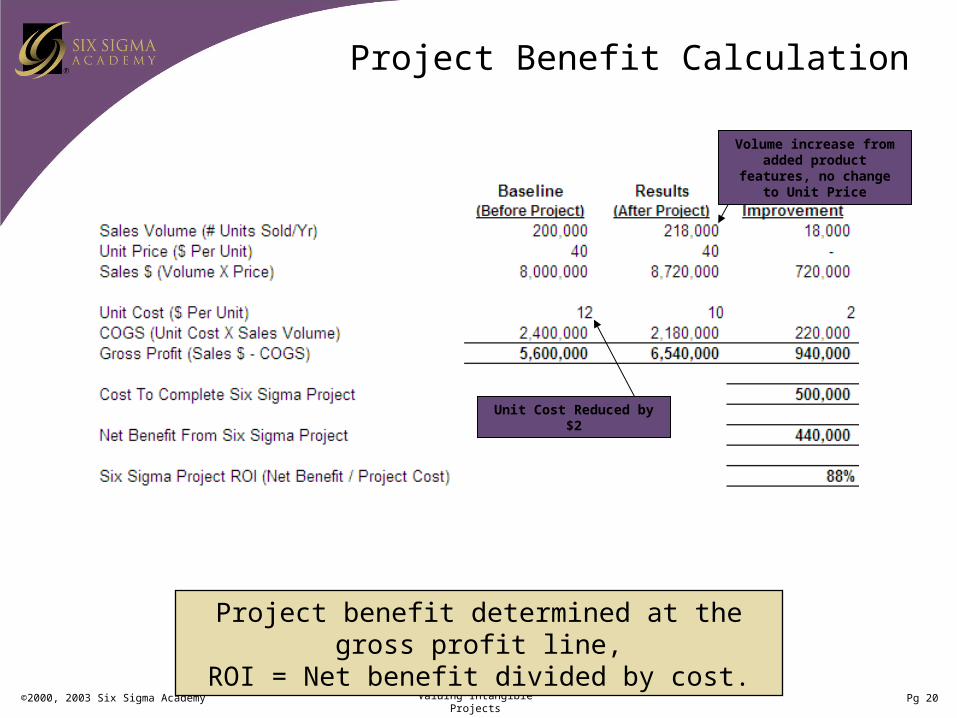

Project Benefit Calculation

Project benefit determined at the gross profit line,ROI = Net benefit divided by cost.

Volume increase from added product features, no

change to Unit Price

Unit Cost Reduced by $2

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 21

Summary

• Identify business opportunity (must establish project value proposition)

• Decide on appropriate measurement for project

• Determine project valuation method (dollars to defects)

• Baseline performance, value current performance

• Improve process, value improvement

Treat projects as funding requests, develop business case.

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 22

Trademarks And Service Marks

Six Sigma is a federally registered trademark of Motorola, Inc.

SigmaFlow is a trademark of Compass Partners, Inc.

MINITAB is a trademark of Minitab, Inc.

VarTran is a trademark of Taylor Enterprises.

The following are trademarks of Six Sigma Academy as of October 2003 (alphabetical):Breakthrough DesignBreakthrough Software DesignBreakthrough DiagnosisBreakthrough ExecutionBreakthrough LeanBreakthrough Sigma LeanBreakthrough Six SigmaBreakthrough Strategy®

Breakthrough Value ServicesFASTARTINTELLEQMETREQSigmaCALC® SSA NavigatorWeaving excellence into the fabric of business

©2000, 2003 Six Sigma Academy Valuing Intangible Projects Pg 23

Six Sigma Academy

www.6-sigma.com

US Tel: (480) 515-9501

US Fax: (480) 515-9507

International Tel: +44-1403-218-588

International Fax: +44-1403-218-788

8876 E. Pinnacle Peak Road, Suite 100

Scottsdale, AZ 85255

![INTANGIBLE VALUE –FACT OR FICTION - AI Home | … · [IAS 38.8] 3. INTANGIBLE VALUE –FACT OR FICTION ... 2.36 INTANGIBLE PROPERTY (INTANGIBLE ASSETS): Non-physical assets, …](https://static.fdocuments.us/doc/165x107/5af0812f7f8b9ac2468e1bc2/intangible-value-fact-or-fiction-ai-home-ias-388-3-intangible-value.jpg)