, 18–19 Intellectual Property Valuation in Business ... · The Challenges of IP Valuation Peter...

15

The Challenges of IP Valuation Peter Kaldos Hungarian Patent Office H – 1054 Budapest Garibaldi u. 2 [email protected] Tel: +36 1 474 5814 , 18–19 Intellectual Property Valuation in Business | Helsinki, May 2009 You can‘t manage what you can‘t measure Peter Drucker "the father of modern management”

Transcript of , 18–19 Intellectual Property Valuation in Business ... · The Challenges of IP Valuation Peter...

The Challenges of IP Valuation

Peter Kaldos

Hungarian Patent Office

H – 1054 BudapestGaribaldi u. 2

[email protected]: +36 1 474 5814

, 18–19 Intellectual Property Valuation in Business | Helsinki, May 2009

You can‘t manage

what you can‘t measure

Peter Drucker "the father of modern management”

…to capture and increase business value

from IP assets through enabling optimum

management decisions

Why value Intellectual Property in business?

Important points:

• Introduction to IP valuation – Why value IP?– Approaches to IP valuation

• IP valuation at the Hungarian Patent Office– IP valuation pilot project

• High tech spin‐off company

• Specialisation: Real‐time microscopy + software development

• Market: Cutting‐edge brain research and pharmaceutical development

• Product line: Laser scanning microscopes + software

• Patent application (2007) for real time non‐linear microscope solution

Hungarian Patent Office IP Valuation Pilot Project (2009):„Research Microscope Technology”

© 2008 Juan Eduardo Donoso

= clearly defined patentable technology

Decisions, decisions…

Develop IP further?

Abandon patent?

Commercialise IP?

License out IP?

Sell IP to competitor?

Required information:

How much is the IP worth to the company? (internal value)

How much can we license it for / sell it? (market value)

What factors are opportunities and make the IP valuable?

What uncertainty factors are there which decrease the IP value?

How can we increase the value of the IP??

Why value IP in innovative organisations?

Access to financing

Business related and company law

IP Transfer transactions

Internal management

Accounting and taxation

Intellectual Asset Management +

Enabling management decisions

• Means to initiate dialogue

• Identify uncertainties / opportunities

• Decisions whether to file for patent protection

• Internal investment decisions

• Commercialise or licence out decisions

• Economic efficiency analysis / value orientated management

•….

Access to financing

Business related and company law

IP Transfer transactions

Internal management

Accounting and taxation

• Company formation (contribution in kind)

• Company transactions

• Due diligence

• Mergers and acquisitions

• Capital increase

• IPO

• Valuation of enterprise

• ….

Why value IP in innovative organisations?

Access to financing

Business related and company law

IP Transfer transactions

Internal management

Accounting and taxation

Technology transfer:

• Licence‐in / license‐out (with royalty stream)

• Sale of IP

• Alliance or partnership/joint venture

• Technology access

• Patent pools

• Employee inventor compensation related to technology transfer

Why value IP in innovative organisations?

Access to financing

Business related and company law

IP Transfer transactions

Internal management

Accounting and taxation

• Use of IP to attract investment

• Use of IP to attract venture capital

• IP as collateral for bank loans

• Showing the significance of IP when applying for grants and tenders

Why value IP in innovative organisations?

Access to financing

Business related and company law

IP Transfer transactions

Internal management

Accounting and taxation

• Taxation, Corporate Tax• Financial Accounting• Reporting

Why value IP in innovative organisations?

Challenge:

How do we assess the value of technoIogy / intellectual property?

Commonly used IP valuation methods:

quantitative qualitative

Assessment of the monetary value of IP

Analysis of IP based on factors which influence it’s value.

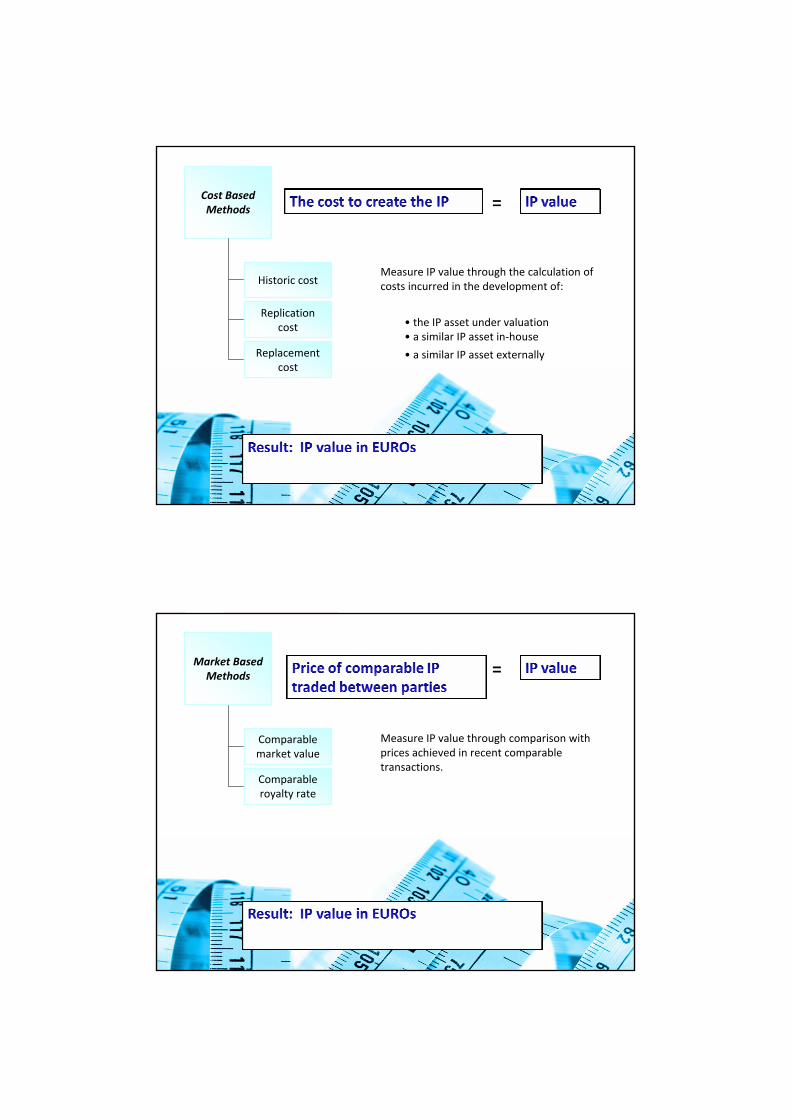

Cost Based Methods

Market Based Methods

Income Based Methods

(Option pricing based

methods)

Value indicator methods

=Cost Based Methods

Historic cost

Replication cost

Replacement cost

Measure IP value through the calculation of costs incurred in the development of:

• the IP asset under valuation • a similar IP asset in‐house

• a similar IP asset externally

=Market Based Methods

Comparable market value

Comparable royalty rate

Measure IP value through comparison with prices achieved in recent comparable transactions.

=Income Based Methods

Discounted Cash Flow (DCF)

Risk adjusted net present value

(rNPV)

Relief from Royalty

Measure IP value through estimating the potential future income from subject IP and discounting these

Patent information related value indicators

=Cost Based Methods

Value indicator methods

Value indicators

based method

Provide a value guide through scoring of different factors related to the IP.

These factors or “value indicators” can influence the value of the IP both positively and negatively.

Challenge: What are the appropriate IP valuation methods to use?

Quantitative Methodology Quali-tative

Cost based

Income based

Market based

Value indicators

based

*Internal Management * *Sale Price * *Licence (*) (*) (*)M &A * *Collateral for loans *Infringement Litigation *Financial Accounting *Taxation, Corporate Tax * *

Source: Watanabe, 2002.

Reasons for valuation

(*)

(*)= used to some extent*= used widely

*

IP Valuation Pilot Project (2009): Methodology toolbox

qualitative analysis tool

quantitative assessment tool

+ = Robust valuation

≈50 factors identified in 5 categories Each factor can affect the value of the IP positively or negatively

Each factor is represented by an indicatior

Experts in working group interviewed regarding each indicator

Value indicators based method

Results:

• Identification of uncertainties and opportunities related to the IP

• Analysis of uncertainties and opportunities

• Internal value of IP (qualitative score)

• Market value of IP (qualitative score)

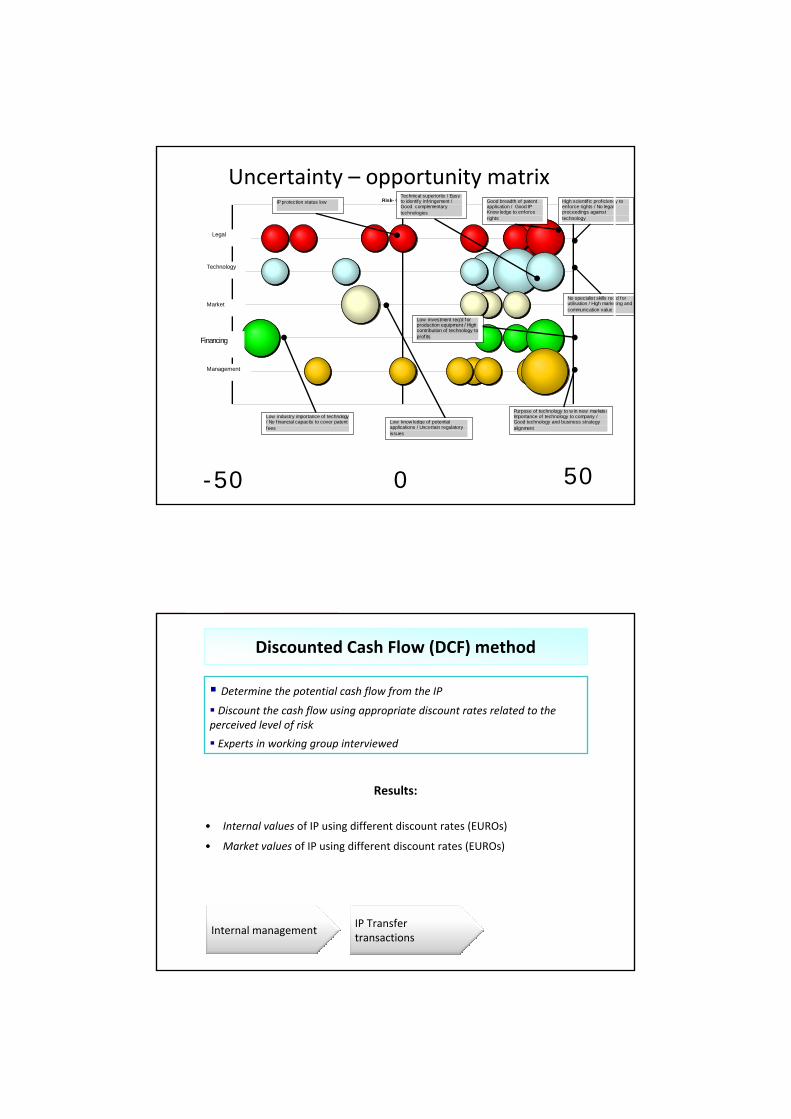

Internal management

Risk- Opportunity

Financing

Management

IP protection status low

Low industry importance of technology / No financial capacity to cover patent fees

Low know ledge of potential applications / Uncertain regulatory issues

High scientif ic proficiency to enforce rights / No legal proceedings against technology

Market

Technology

Legal

Purpose of technology to w in new markets / Importance of technology to company / Good technology and business strategy alignment

No specialist skills req’d for utilisation / High marketing and communication value

Technical superiority / Easy to identify infringement / Good complementary technologies

Low investment req’d for production equipment / High contribution of technology to prof its

Good breadth of patent application / Good IP Know ledge to enforce rights

-50 0 50

Uncertainty – opportunity matrix

Discounted Cash Flow (DCF) method

Determine the potential cash flow from the IP

Discount the cash flow using appropriate discount rates related to the perceived level of risk

Experts in working group interviewed

Results:

• Internal values of IP using different discount rates (EUROs)

• Market values of IP using different discount rates (EUROs)

Internal managementIP Transfer transactions

Diagram 3: Annual Discounted Cash Flow

-5000

5001000150020002500300035004000450050005500600065007000750080008500

2007

2008

2009

2010

2011

2012

2013

2014

2015

2018

Year

Valu

e (m

illio

n H

UF)

Risk free (10%) Risk adjusted (20%) Venture Capital (50%)

Annual discounted cash flow technology using different discount rates

Diagram 1: Technology Present Value with different discount rates

0

10000

20000

30000

40000

50000

60000

DCF

valu

e(ri

sk fr

eedi

scou

nt ra

te)

DC

F va

lue

(risk

adj

uste

d)

DCF

Valu

e(D

isco

unt r

ate

30%

)

DC

F Va

lue

(Dis

coun

t rat

e40

%)

DC

F Va

lue

(VEN

TUR

EC

APIT

ALR

ATE)

Discount Rates (%)

Pres

ent V

alue

(mill

ion

HU

F)

Present value of technology using different discount rates

Challenge: How can the results of an IP valuation capture and increase business value?

Diagram 1: Technology Present Value with different discount rates

0

10000

20000

30000

40000

50000

60000

DCF

valu

e(ri

sk fr

eedi

scou

nt ra

te)

DC

F va

lue

(risk

adj

uste

d)

DCF

Valu

e(D

isco

unt r

ate

30%

)

DC

F Va

lue

(Dis

coun

t rat

e40

%)

DC

F Va

lue

(VEN

TUR

EC

APIT

ALR

ATE)

Discount Rates (%)

Pres

ent V

alue

(mill

ion

HU

F)

Diagram 3: Annual Discounted Cash Flow

-5000

5001000150020002500300035004000450050005500600065007000750080008500

2007

2008

2009

2010

2011

2012

2013

2014

2015

2018

Year

Valu

e (m

illio

n H

UF)

Risk free (10%) Risk adjusted (20%) Venture Capital (50%)

Risk- Opportunity

Financing

Management

Market

Technology

Legal

By providing the required information…

…. to enable optimum managment decisions regarding IP

Develop IP further!

Abandon patent!

Commercialise IP!

License out IP!

Sell IP to competitor!

Thank you

Peter Kaldos

Hungarian Patent Office

H – 1054 BudapestGaribaldi u. 2

[email protected]: +36 1 474 5814