ual JPMorgan Global High Yield and Leveraged Finance Conference Presentation

Upload

alexander-goldenCategory

view

213download

0

1®

Service Corporation International

JPMorgan2007 High Yield ConferenceMiami, FLJanuary 22, 2007

Service Corporation International

®

Tom RyanPresident and CEO

3®

SCI strengths and investment considerations

Market leader in the death care industry

Acquisition of Alderwoods is value-enhancing transaction

Competitive advantage due to size, unparalleled network and national brand strategy

Diverse geographic exposure

Stable industry fundamentals

Large backlog of preneed revenues

Strong cash flow

Attractive credit profile

4®

Today SCI is well-positioned for profitable growth

LEVERAGEscale and drive operating discipline

APPROACHbusiness by customer segment

MANAGEfootprint of businesses

Profitable growth

Profitable growth

5®

Approach the business by customer segment

Consumer landscape is changing (from products to experience/value)

Segment our consumers based upon their needs

Tailor our business operating strategies to consumer segments

Drop our one-size-fits-all approach

Focus resources on most profitable segments

Respond better to changing demographic trends

Recently hired a Chief Marketing Officer who will help to further develop segmentation strategies

Funeral Cemetery

Quality/Prestige Premium/Prestige

Customs Conscious Standard

Convenience/Location

Price

Manage footprint

Leverage scale

Customer segmentation

6®

Leverage scale & drive operating discipline

Align pricing strategies with customer segments; centralize and simplify pricing process

Focus pricing on service and cemetery property, our competitive advantages

Implement operating standards

Develop clear yet flexible benchmarks and shared best practices for increased productivity

Focus preneed efforts on right product for right customer

Align incentives with product value to SCI; reward incrementality

Pursue affinity opportunities and more fully utilize our purchasing power

Manage footprint

Leverage scale

Customer segmentation

7®

Manage the footprint

Categorize our current footprint based on customer segmentation model

Target expansion growth differentially focusing on highest return segments

FUNERAL: Target segments that value high quality service/memorialization, our core competency

CEMETERY: Target combos and attractive stand-alones

Prioritize capital spending according to consumer model

Proactive funeral home facility capex to ensure facilities meet consumer expectations

Cemetery maintenance standards based on revenue, life-cycle stage and endowment care trust fund levels

Manage footprint

Leverage scale

Customer segmentation

8®

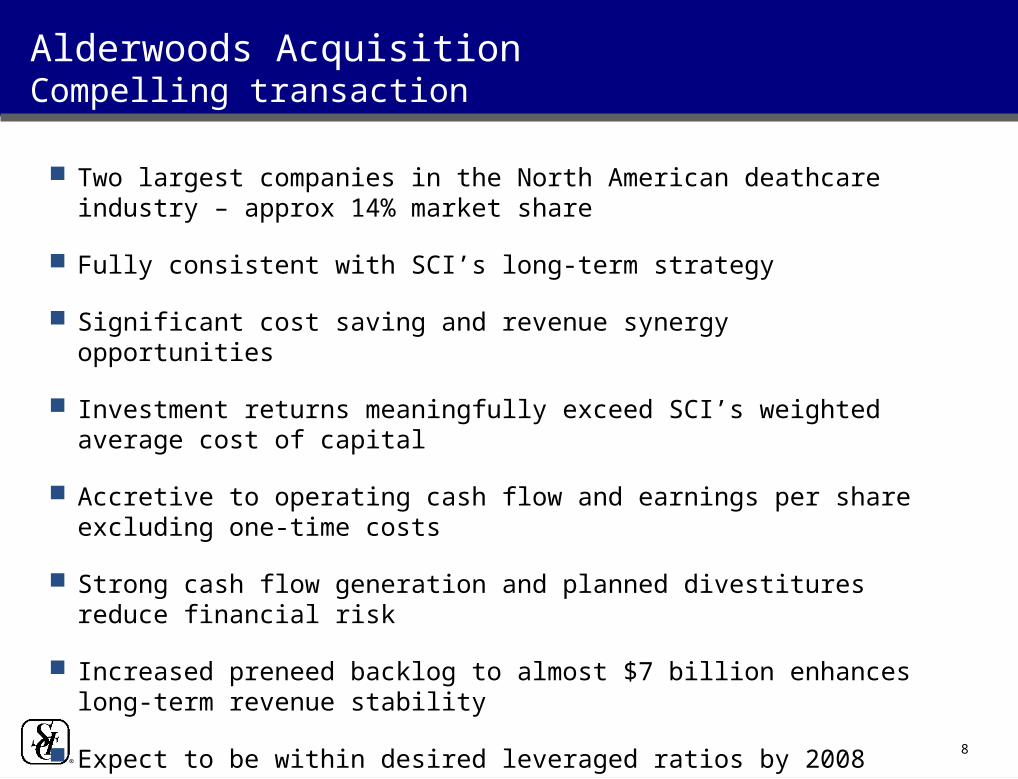

Alderwoods AcquisitionCompelling transaction

Two largest companies in the North American deathcare industry – approx 14% market share

Fully consistent with SCI’s long-term strategy

Significant cost saving and revenue synergy opportunities

Investment returns meaningfully exceed SCI’s weighted average cost of capital

Accretive to operating cash flow and earnings per share excluding one-time costs

Strong cash flow generation and planned divestitures reduce financial risk

Increased preneed backlog to almost $7 billion enhances long-term revenue stability

Expect to be within desired leveraged ratios by 2008

9®

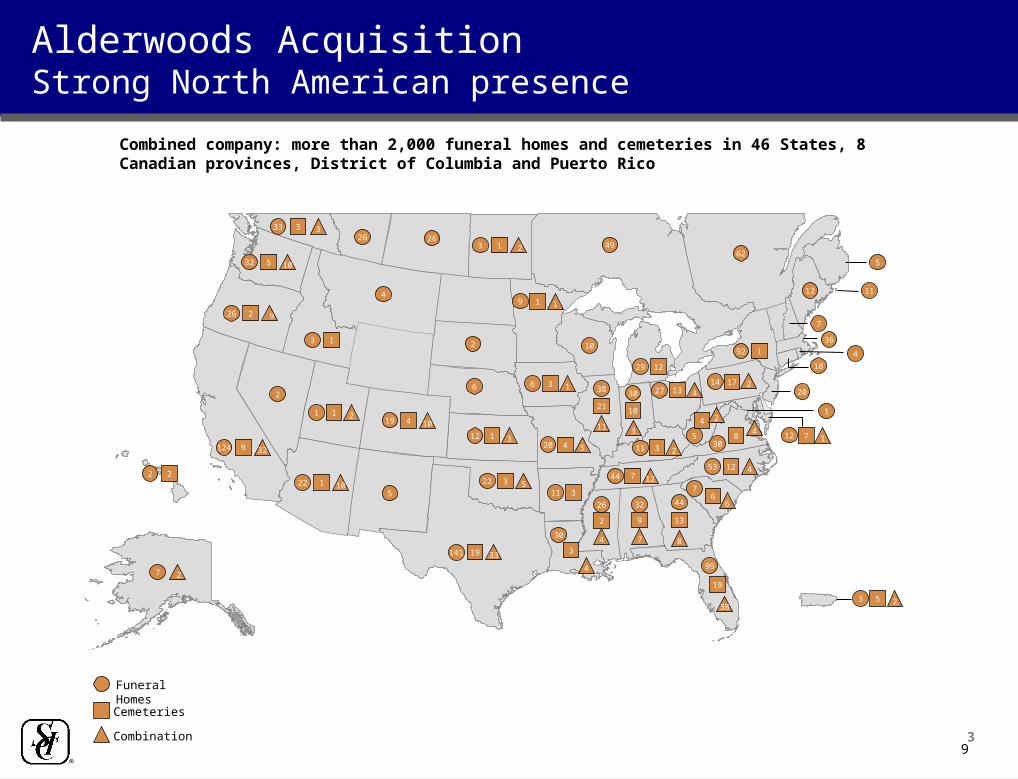

Alderwoods AcquisitionStrong North American presence

3

32

124

99

44

2

38 306

12

26

20

6

7

20

92

53

27

227

2

44

141

1

26

2649

62

11

18

4

19

9

9

19

13

2

21 10

3

2

4

12

13

3

6

7

19

1

2

3

4

26

1

Funeral Homes

36

Cemeteries

32

10

38

8

11 3

1

2

4

5

4

4

5

9

6

12

33

2

32 5 10

11

3 1 2

3 1

9 1 14

2

5

1

3 5 2

Combination

7

11 3

12 1 3

30

3

4

12 7 1

14 17 2

308

45

4 2

29

10

12

33 3 3

5

7 2

22 1 10

Combined company: more than 2,000 funeral homes and cemeteries in 46 States, 8 Canadian provinces, District of Columbia and Puerto Rico

10®

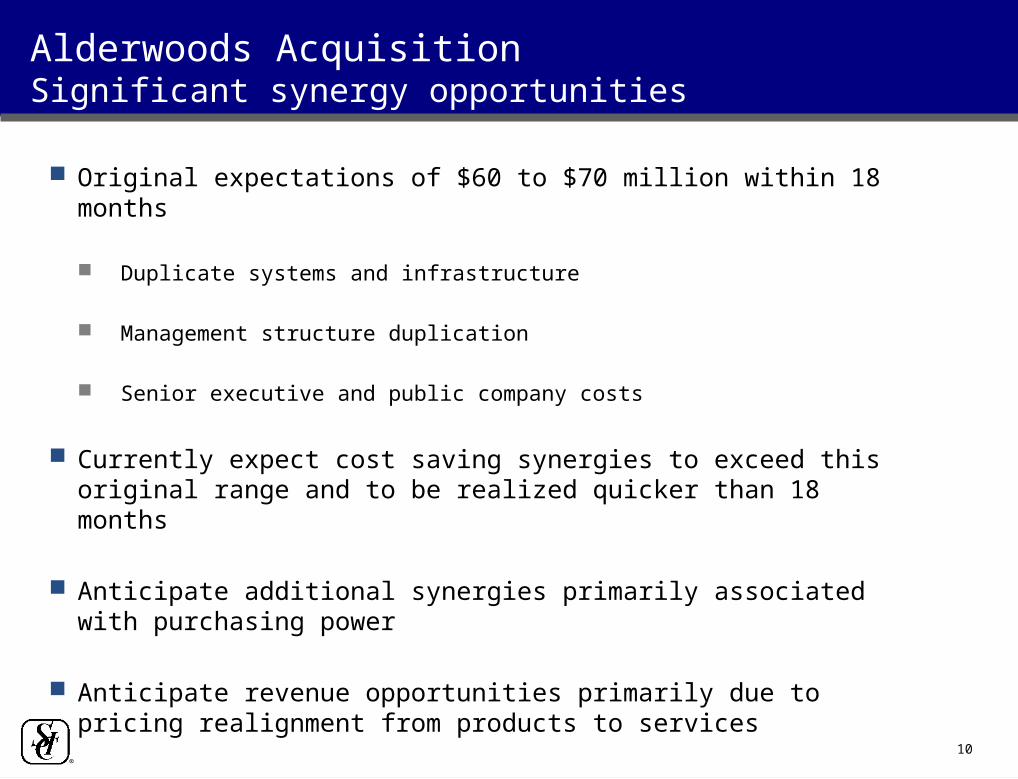

Alderwoods AcquisitionSignificant synergy opportunities

Original expectations of $60 to $70 million within 18 months

Duplicate systems and infrastructure

Management structure duplication

Senior executive and public company costs

Currently expect cost saving synergies to exceed this original range and to be realized quicker than 18 months

Anticipate additional synergies primarily associated with purchasing power

Anticipate revenue opportunities primarily due to pricing realignment from products to services

11®

Near term expectations

Significant focus on integration of Alderwoods

Build up of net cash balances due to asset sales and cash flows

Continued volume loss associated with the exit from low priced immediate cremation activities in certain markets

Continued strong increases in funeral averages due to strategic pricing initiatives

Favorable impact from operating staffing metrics

Improvements in cemetery sales production and efficiencies in selling cost metrics

Service Corporation International

®

Eric TanzbergerSenior Vice President and CFO

13®

Strong financial position

Cash on hand of approx $60 million

Total debt of approx $2.0 billion

Asset sales will expedite deleveraging

FTC mandated and other SCI divestitures are anticipated to generate $200 million of proceeds in the near future, while not impacting EBITDA materially

Expect to sell Mayflower (Alderwoods’ insurance company) for approx $65 million

Comprehensive review of combined properties expected to result in additional divestitures

With debt reduction in 2007 and full effect of anticipated synergies from the Alderwoods transaction, we expect Debt/EBITDA to range between 3.0 and 3.5

14®

Target 2008E

Target Ratios

Operating cash flow less certain capex1/Interest Expense

>1.5x 2.2x

Net Debt2/Operating cash flow less certain capex

5x to 7x 3.6x

Net Debt/Total Net Capital3 40% to 45% 38%

Note: 2008E assumes no share repurchases or debt re-financings

Target Ratios

1 Cash flows from operations (excluding unusual items) less capital expenditures (excluding expenditures to construct new funeral home facilities and other growth capital)

2 Total debt less cash on hand

3 Net debt (as defined above) plus stockholders’ equity

15®

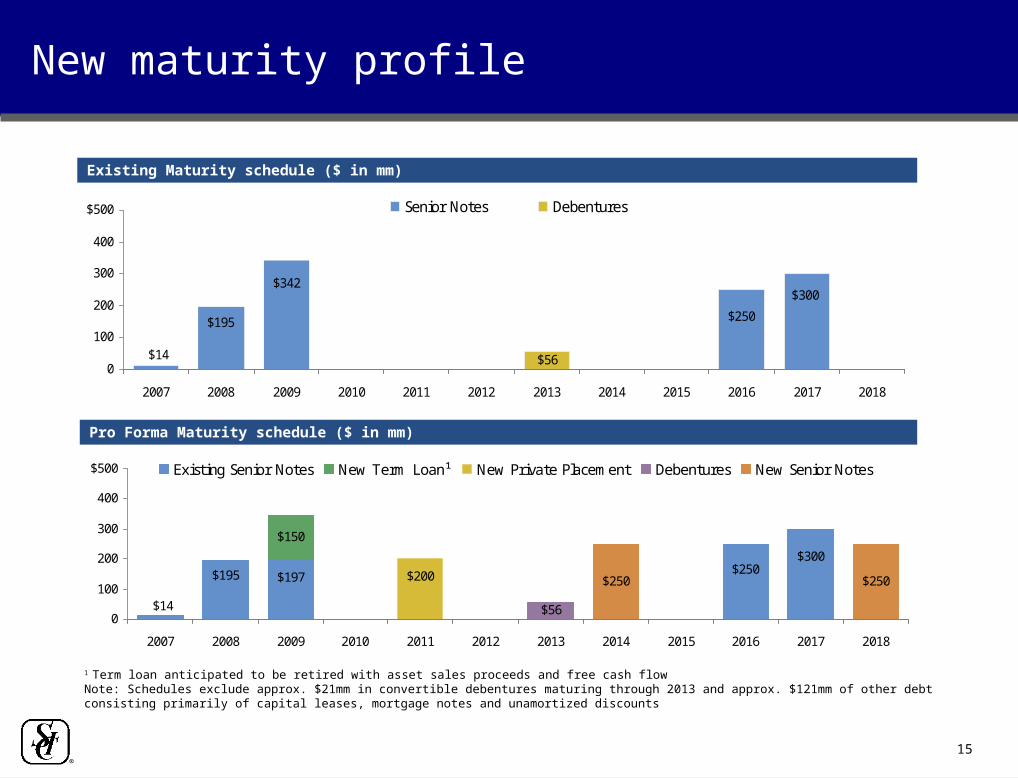

New maturity profile

$56

$300

$250

$342

$195

$140

100

200

300

400

$500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Senior Notes Debentures

Existing Maturity schedule ($ in mm)Existing Maturity schedule ($ in mm)

Pro Forma Maturity schedule ($ in mm)Pro Forma Maturity schedule ($ in mm)

$150

$250 $250$195

$14

$197$250

$300

$200

$560

100

200

300

400

$500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Existing Senior Notes New Term Loan¹ New Private Placement Debentures New Senior Notes

1 Term loan anticipated to be retired with asset sales proceeds and free cash flowNote: Schedules exclude approx. $21mm in convertible debentures maturing through 2013 and approx. $121mm of other debt consisting primarily of capital leases, mortgage notes and unamortized discounts

16®

Upcoming reporting schedule

Expect to provide 2007 guidance/outlook on February 15

Expect to report Q4 and fiscal 2006 results on February 28

Expect to be at high end or exceed our 2006 guidance ranges for EPS and cash flow from operations

EPS of $.30 - $.34 ($.32 - $.36 revised for France distribution)

Cash flow from operations of $290 - $315 million

17®

A bright future ahead

Predominant leader in a stable industry

Significant cash flows, liquidity and financial flexibility

Short-term growth opportunity

Successfully integrating the Alderwoods acquisition

Utilizing more centralization and standardization to take advantage of our scale

Aligning pricing and preneed strategies with customer segments and our competitive advantages

Long-term differential growth opportunity

Tailoring our business approach by customer segment

Footprint expansion in customer segments that we excel

18®

Service Corporation International

JPMorgan2007 High Yield ConferenceMiami, FLJanuary 22, 2007